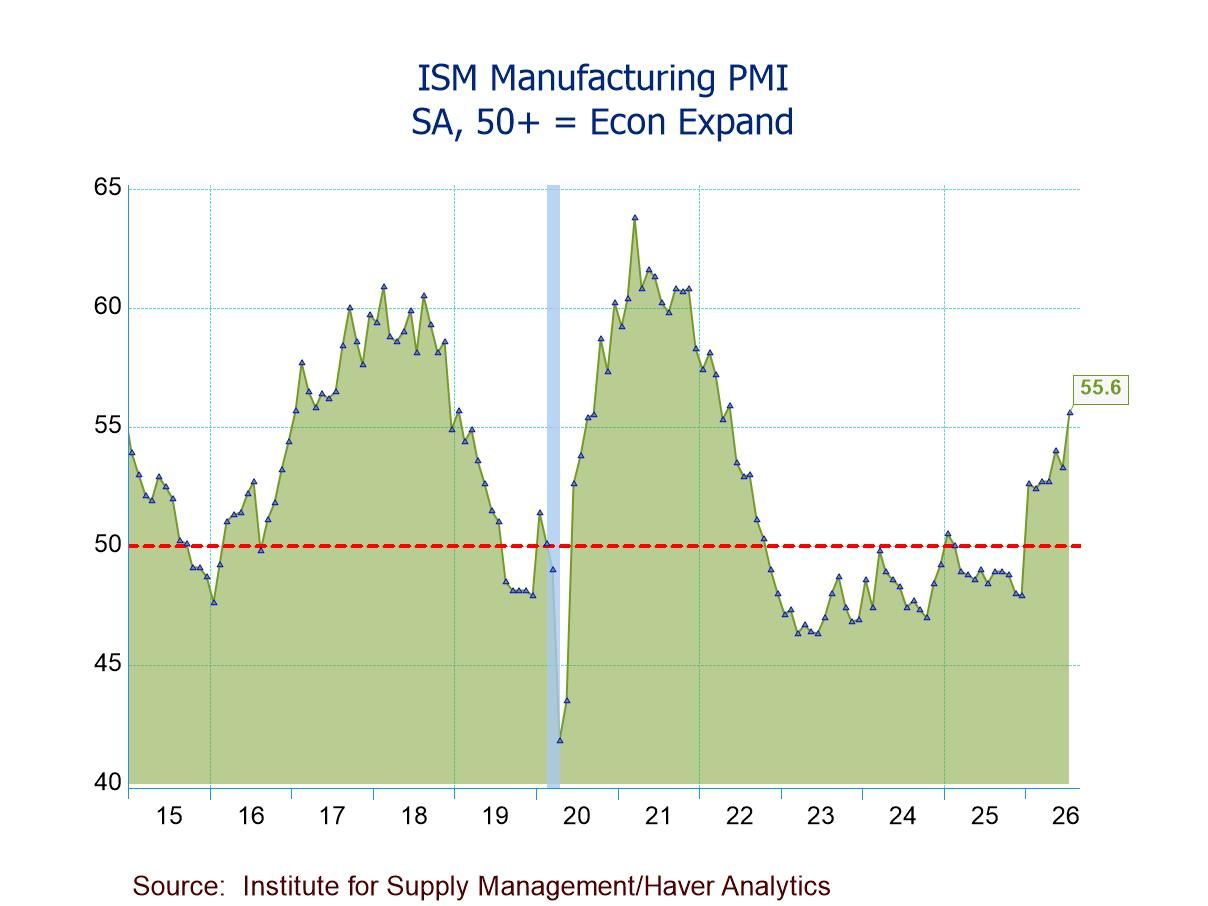

- ISM Mfg. PMI up to 55.6 in July; seventh straight month above 50.

- Production (58.5) reaches highest level since Nov. ’21 and expands for the ninth consecutive mth.; new orders (56.7) for the seventh successive mth.

- Employment (52.8) above 50 for the first time since Sept. ’23; at highest level since Aug. ’22.

- Prices Index (71.1) at a five-month low, still indicating prices rising for the 22nd straight mth.

- Exports (53.0) highest since Mar. ’22; imports (55.7) highest since June ’21.

USA| Aug 03 2026

U.S. ISM Manufacturing PMI at Highest Level Since May ’22; New Orders, Production, and Employment Growing

Asia

Asia

More Commentaries

USA| Jul 30 2026

USA| Jul 30 2026Personal Income, Consumption, and Prices in June

- (Temporary?) relief on price pressures

- Respectable income gain and active spending by consumers

USA| Jul 30 2026

USA| Jul 30 2026U.S. GDP Increased 1.5% in Q2

- The quarterly gain was led by personal consumption and business spending on equipment and intellectual property.

- Inventory investment and net exports were meaningful drags on overall growth.

- Domestic demand growth accelerated to well above trend.

- Reflecting the jump in energy prices after the escalation of the US-Iran conflict, GDP inflation accelerated markedly.

by:Sandy Batten

|in:Economy in Brief

USA| Jul 30 2026

USA| Jul 30 2026U.S. Initial Unemployment Claims Rose in the Week of July 25

- New claims rose by 9,000 to 197,000 in the week of July 25, after reaching their lowest level since 1969 in the July 18 week.

- Continuing claims declined by 7,000 to 1.782 million in the week ending July 18.

- The insured unemployment rate was unchanged at 1.2% in the week of July 18.

Europe| Jul 30 2026

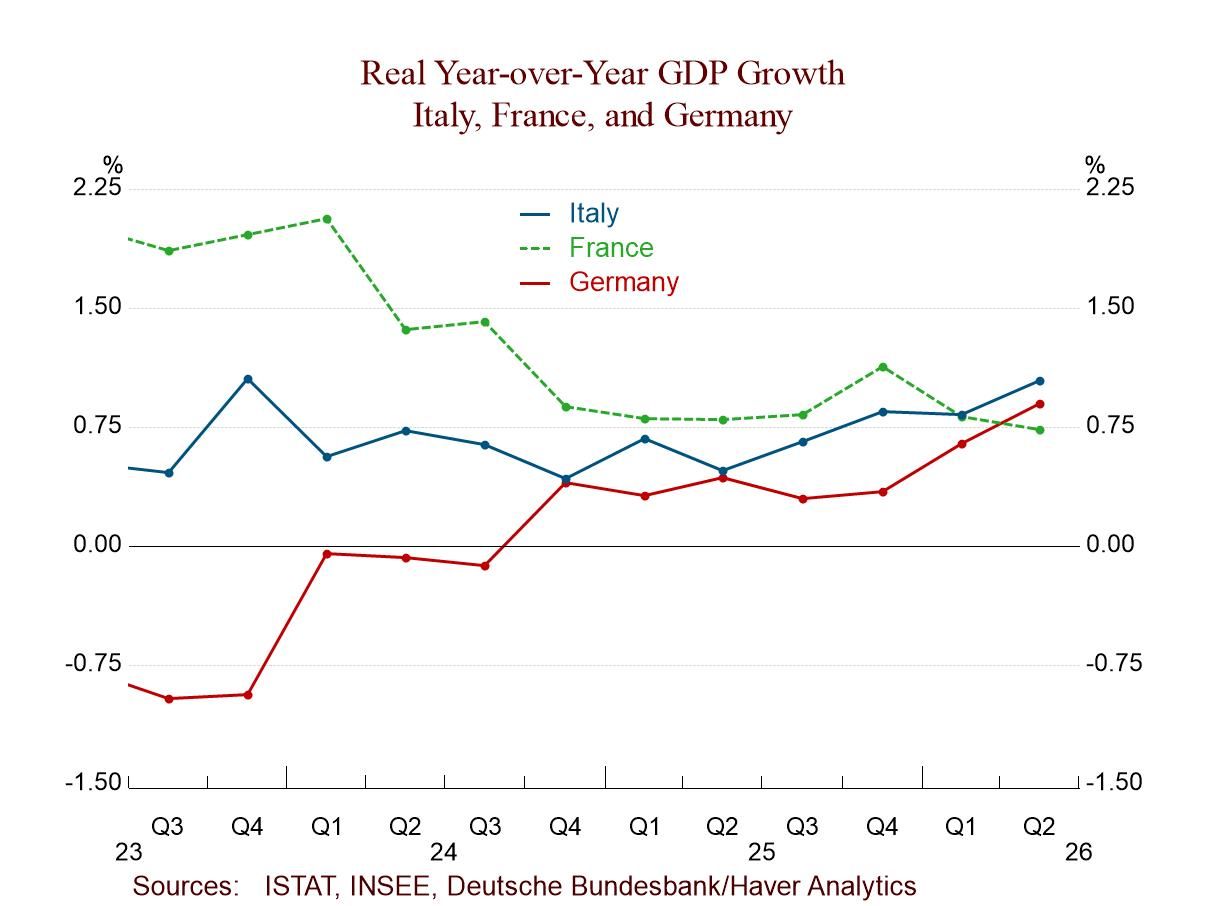

Europe| Jul 30 2026European GDP Improves in Q2

GDP in the second quarter accelerated for most of the countries in the monetary union. The overall figure for the EMU improved to 1.8% as an annualized quarter-over-quarter gain from 0% in the first quarter and 0.8% in the fourth quarter. Among the 8 early reporters of GDP, there was a deceleration in Italy, Germany, and Belgium, while the other five countries showed an increase in their growth rates in the second quarter compared to the first quarter.

The four largest monetary union economies showed a technical weakening, but at the one-digit level, growth was 1.1% in the second quarter, the same as in the first quarter. The rest of the monetary union saw an increase in growth from -2.9% annualized in the first quarter to a gain of 3.7% at an annualized rate in the second quarter, a huge shift.

On a year-over-year basis, growth rates improved for all but three countries: Belgium, France, and Spain. For Spain, the year-over-year growth rate was unchanged at 2.7% in the second quarter. For France, the growth decelerated from 0.8% in the first quarter to 0.7% in the second quarter; for Belgium, the growth rate slowed from 0.8% to 0.5%.

The overall monetary union growth rate rose to 1% in the second quarter compared to a 0.5% increase in the first quarter. The four largest economies showed stronger growth at 1.1% year-over-year compared to 1% last quarter, while the rest of the monetary union showed a GDP gain of 0.5% compared to a year-over-year decline of 0.9% in the first quarter.

Evaluating growth over a longer timeline, three early-reporting monetary union members have standings in their growth rates above their respective 50th percentiles. Those countries are Portugal at 69.6%, Italy at 60.9%, and Spain at 51.1%.

The four largest monetary union economies, pooled together, have a growth ranking year-over-year in their 43.5 percentile. The rest of the monetary union has a growth ranking at the 25th percentile. From this, we can conclude that most of the growth has come from the four large economies, even though in the current quarter it's the smaller economies that seem to be performing much better.

On these same timelines, the United States posted a weaker quarterly growth rate in the second quarter at 1.5%, compared to 2.1% in the first quarter. U.S. growth at 2.1% year-over-year is slower than its 2.7% year-over-year growth rate in the first quarter; it has a queue-percentile standing of its growth rate on data back to 2001 in its 37.5 percentile, a standing well below its historic median for the period. U.S. consumer spending held up pretty well in Q2 and business investment spending remained strong, but the trade account did a turnaround and sucked a lot of life out of the growth rate in the second quarter, keeping the U.S. economy as an important driver of global growth.

USA| Jul 29 2026

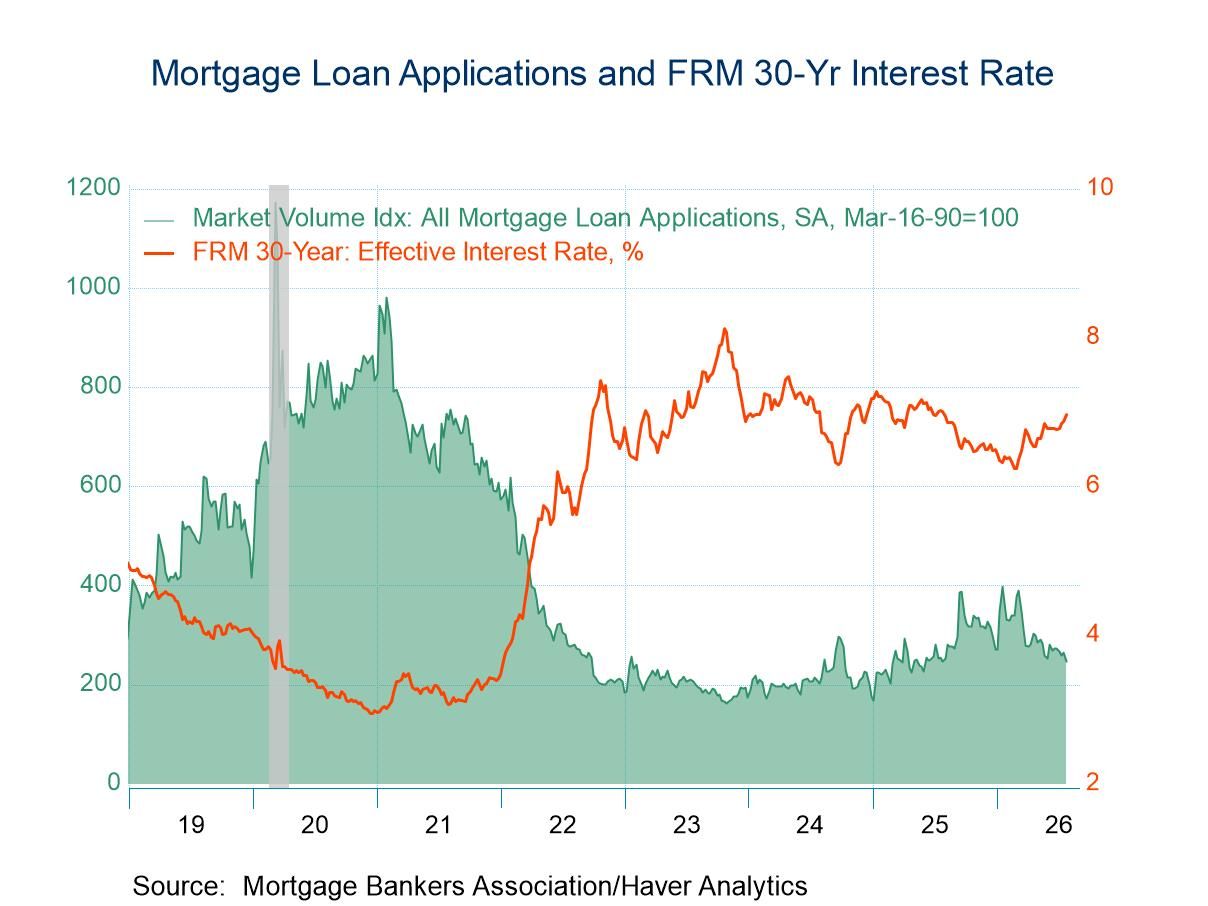

USA| Jul 29 2026U.S. Mortgage Applications Declined in the July 24 Week

- Both applications for loans to purchase and applications for loan refinancing declined in the latest week.

- Interest rate on 30-year fixed-rate loans rose 9bps to 6.96%.

- Average loan size edged up.

USA| Jul 28 2026

USA| Jul 28 2026U.S. Consumer Confidence Continues Downtrend in July

- The Conference Board’s measure of consumer confidence fell to 90.8 in July from 92.2 in June, continuing its downtrend since early last year.

- The Present Situation index fell to 114.9, its lowest reading since February 2021. The Expectations index was unchanged at 74.7.

- Inflation expectations one year ahead fell to 4.5% in July from 4.9%.

- The labor market differential fell to 3.1% in July, its lowest level since February 2021, from 3.8%, pointing to further softening of labor market conditions.

by:Sandy Batten

|in:Economy in Brief

- Deficit: $101.46 bil. in June, down $4.43 bil. (-4.2%) from May’s $105.89 bil.

- Exports -1.8%, second straight m/m decline to a five-month low, driven by a 4.4% drop in exports of industrial supplies & materials.

- Imports -2.6%, first m/m decrease since Jan., w/ all end-use import categories down, led by drops of 6.3% in other goods and 3.8% in nonauto consumer goods.

France| Jul 28 2026

France| Jul 28 2026French Household Confidence Improves

Household confidence in France improved in July, rising to 86.4 from 84.3 in June. Confidence was last higher in March, and the average for confidence over the last 12 months is 87.7. The July value, despite its climb, is still below that average; confidence is still weak in a historic context. According to data back to 2001, the current confidence metric in July has a 16.2 percentile ranking, an extremely weak reading. The mean of confidence readings back to 2001 is 95.1. The July reading is nearly nine points below that.

Weak but improved living standards readings: Living standards in July improved slightly compared to June. The assessment of the last 12 months is -79 compared to -81 previously. However, the 12-month average is a rating of -74; the July reading is still short of that. Looking to the next 12 months, living standards are expected to improve; the reading of -59 in July compares to -65 logged a month ago. It compares to a 12-month average of -61. The expectation for living standards over the next 12 months is higher than it has been on average for the last 12 months, although the reading itself is still quite weak. The standing in its 10th percentile for a current rating at -59 is below its full-period average of -38.

Fewer unemployment worries: Unemployment over the next 12 months is expected to be less of a concern, but the reading in July drops to 55 from 61 in June; however, the July reading is still above the 12-month average of 52. The ranking for unemployment concerns has a 72nd percentile standing, putting it in the top third of its historic range of readings.

Inflation fears drop, comparatively: Price developments show that over the past 12 months inflation has been a concern, with the July reading falling relative to June to 17 from 22, but this reading is much higher than its 12-month average of +2. However, looking to the next 12 months, the July reading is -33 compared to -15 in June, and it compares to -20 on average over the last 12 months. Inflation expectations are for conditions to show weaker inflation pressures. The ranking of the July reading is at its 44th percentile, below its historic median; the medians on rankings occur at a ranking of 50. Of course, all these readings will be dependent on how oil prices evolve.

Saving/spending: Both the favorability and the ability to save improved in July compared to June; both readings in July are above their respective 12-month averages. The rankings of these observations are around their high 90th percentiles; for the favorability to save, the reading is the highest in the whole period back to June 2001. The ability to save is often not a good reading but rather one that reflects consumer defensiveness, and we see that as we move to the next metric, the favorability to make a major purchase. In July, that reading improved to -36 from -38 in June, but it's weaker than its 12-month average of -31.8. In historic context, it's extremely weak and has an 8.3 percentile standing. So, the favorability to make a major purchase is in the lower 10th percentile of all monthly observations back to June 2001, indicating considerable consumer defensiveness.

Financial situation: The financial situations over the past 12 months and projected over the next 12 months show slightly improved readings compared to June. The past 12 months reading is weaker than its 12-month average, while the expectation for the next 12 months is the same as its 12-month average. The rankings of the two financial situations are just below their respective 40th percentiles, placing them about 10 percentile points below their historic medians.

Summing up The consumer in France sees some improvement in July, and conditions remain mixed across these various components. But most of the rankings for the components are quite weak, with the exception being concerns about unemployment and the favorability to save, which was a defensive reading. The weighting scheme for this survey gives us a slightly more positive read on the month, but it's clear that the French consumers are still concerned about economic conditions and the future.

- of2733Go to 1 page