Global| Dec 04 2025

Global| Dec 04 2025Charts of the Week: Diverging Paths, Converging Risks

by:Andrew Cates

|in:Economy in Brief

Summary

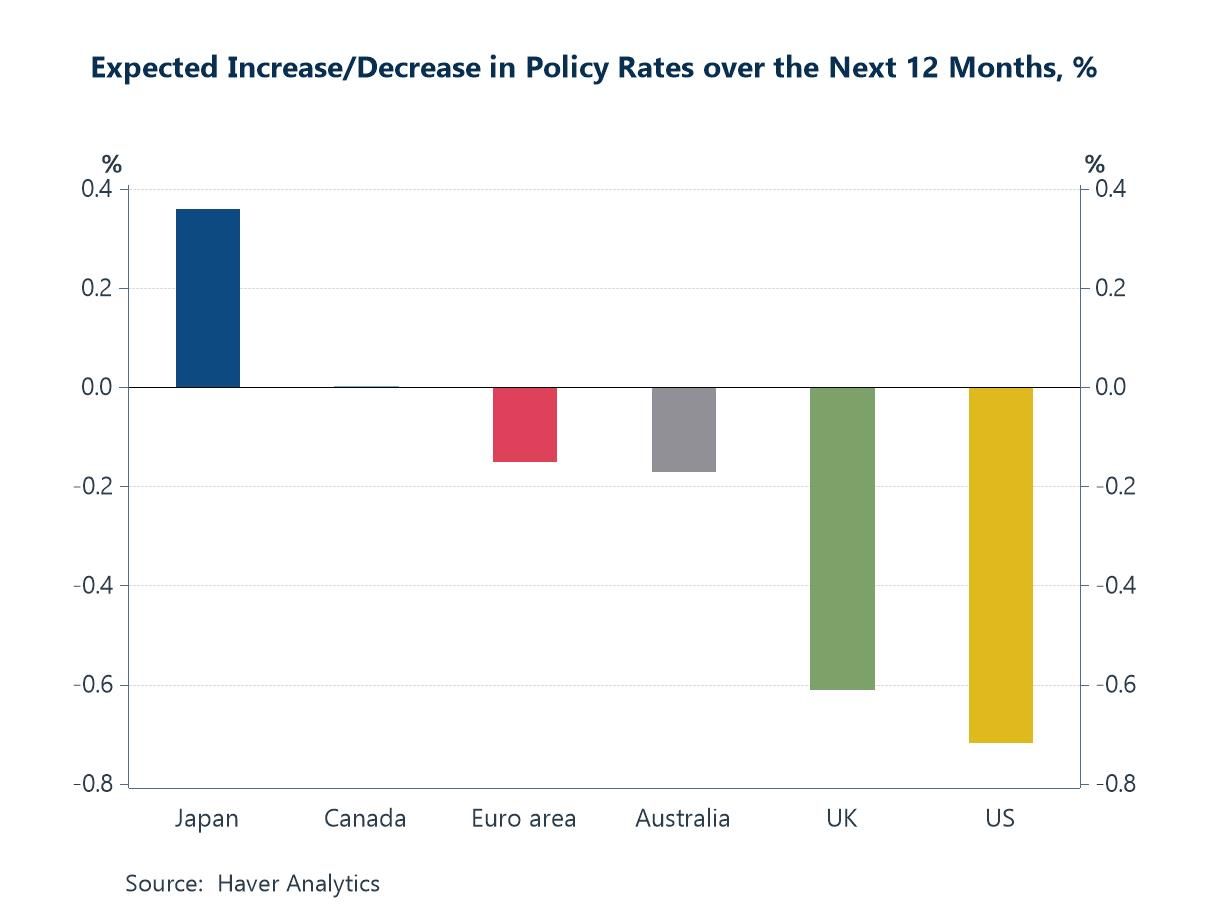

Global financial markets have been navigating a more unsettled backdrop in recent weeks, with choppier risk sentiment and shifting rate expectations reshaping the macro narrative. US assets have been particularly sensitive to signs of cooling labour-market momentum and the temporary loss of official payroll data during the government shutdown, while rising real yields in Japan and renewed fiscal tightening in the UK have added further cross-currents. Against this backdrop, Blue Chip forecasts point to a world edging gradually toward easier monetary policy, but with a striking divergence between a more dovish Fed and a still-normalising Bank of Japan (chart 1). The softening in US private payroll growth, captured by the ADP data, reinforces the case for Fed easing at a time when official data are unavailable (chart 2). In the euro area, sticky underlying inflation could leave the ECB wary of further meaningful cuts (Chart 3). Japan’s climb in real JGB yields, underpinned by stronger capex and supportive policy signals, continues to reverberate through global rate markets (chart 4). In the UK, the gilt–Treasury spread has widened over the year but narrowed slightly post-Budget as investors priced the growth-dampening effects of fiscal tightening (chart 5). And in the global goods sector, while the manufacturing PMI still points to only mediocre growth, the revival in South Korean semiconductor exports underscores the extent to which AI-related demand remains one of the few clear bright spots in an otherwise subdued industrial landscape (chart 6).

The global policy rate consensus Blue Chip forecasters continue to mark down the path for global policy rates over the next twelve months, but with a striking divergence at the core. The US remains the standout on the downside: expectations for the Fed have shifted decisively toward deeper easing amid cooling inflation readings, softer labour-market signals, and a meaningful tightening in financial conditions as equity markets have turned choppier and long-term yields have retreated. Japan sits firmly at the opposite end of the spectrum. Markets now anticipate further incremental tightening by the Bank of Japan as it continues its slow-motion normalisation—supported by firmer wage settlements, persistent services inflation, and a strategic push to lock in a durable exit from the deflationary era. Elsewhere, the modest expected cuts for the euro area and Australia and the absence of any change from Canada largely reflect the fact that much of the heavy lifting has already been done. Policy rates in these economies are no longer meaningfully restrictive, and in some cases are arguably drifting toward neutral or even slightly loose territory. The result is a global policy map that is gently tilting toward accommodation, but with one unmistakable fault line: a widening Fed–BoJ divergence that looks set to define the macro narrative over the coming year.

Chart 1: Blue Chip Financial Forecasts: Expected change in policy rates over the next 12 months

The US labour market US labour-market conditions continue to soften at the margin, and this week’s latest ADP data offer an even more critical guide than usual given the US government’s recent shutdown and the absence of official payroll numbers. November’s ADP report specifically showed a 32,000 decline in private employment—far weaker than expectations, which were centred on a modest 5,000 gain. Both ADP’s three-month change in private employment and the BLS series have eased markedly from last year’s highs, underscoring a loss of hiring momentum across private industries. In the near term—and with the official BLS data for November unavailable until December 16th—the ADP numbers will carry disproportionate weight in shaping market expectations and the narrative around the Fed’s next steps.

Chart 2: The ADP employment report versus the BLS employment report

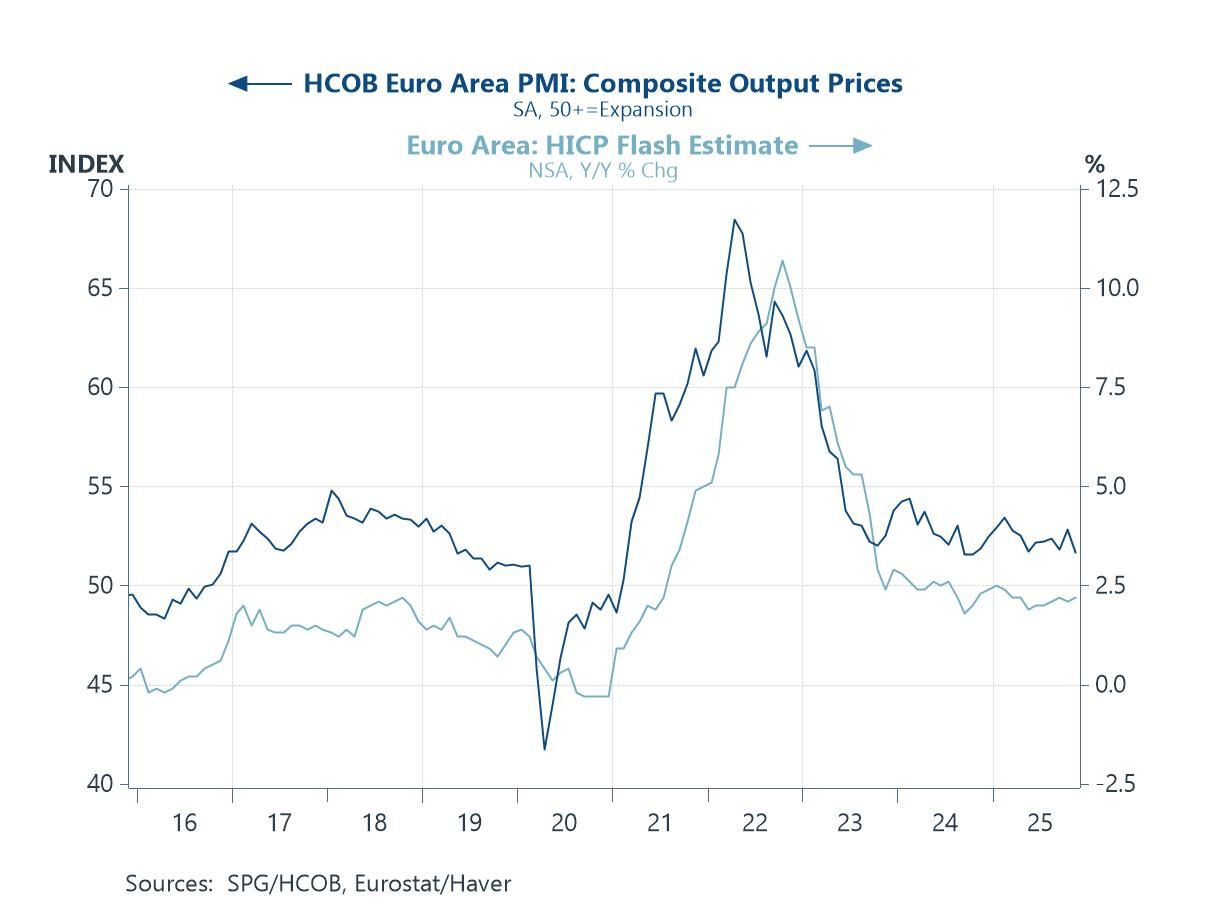

Inflation in the euro area The euro area’s disinflation trend has continued to progress, but the latest data underline why the ECB remains cautious about endorsing a more aggressive easing path. Composite output price pressures from the PMI survey have settled into a narrow band consistent with only modest disinflation, while the flash HICP estimate, though dramatically lower than its 2022 peak, appears to be levelling off rather than pushing decisively back toward target. This combination of sticky underlying inflation and still-fragile growth keeps the ECB in a delicate position: policy is no longer restrictive, but not clearly loose either, and the Governing Council has been careful to stress that further meaningful rate cuts will require clearer evidence that price dynamics are on a sustained downward trajectory. For now, the data suggest a eurozone economy that has stabilised, but with inflation still just firm enough to prevent the ECB from moving more decisively.

Chart 3: Output price signals from the euro area composite PMI versus headline CPI inflation

Japan’s JGB yields Japan’s upward drift in government bond yields has become one of the more consequential global market developments in recent weeks, and this chart helps explain why. While nominal JGB yields have been rising, the underlying driver is increasingly real yields rather than inflation expectations. That shift reflects a meaningful pickup in private non-residential investment, which has gained momentum alongside stronger corporate balance sheets, tighter labour markets, and an improving outlook for productivity-enhancing capex. The new prime minister has reinforced this narrative by signalling policy continuity on structural reforms and a renewed focus on incentivising domestic investment, helping to anchor expectations that the recent rise in real rates is part of a more durable normalisation process. For global capital markets, the implications are significant: higher real JGB yields increase Japan’s relative appeal as a destination for domestic savings, potentially reducing outward capital flows and exerting upward pressure on global real rates at the margin. After years in which Japan exported excess savings to the rest of the world, even a modest reversal of that pattern is being watched closely.

Chart 4: Japan’s real JGB yields versus real nonresidential investment growth

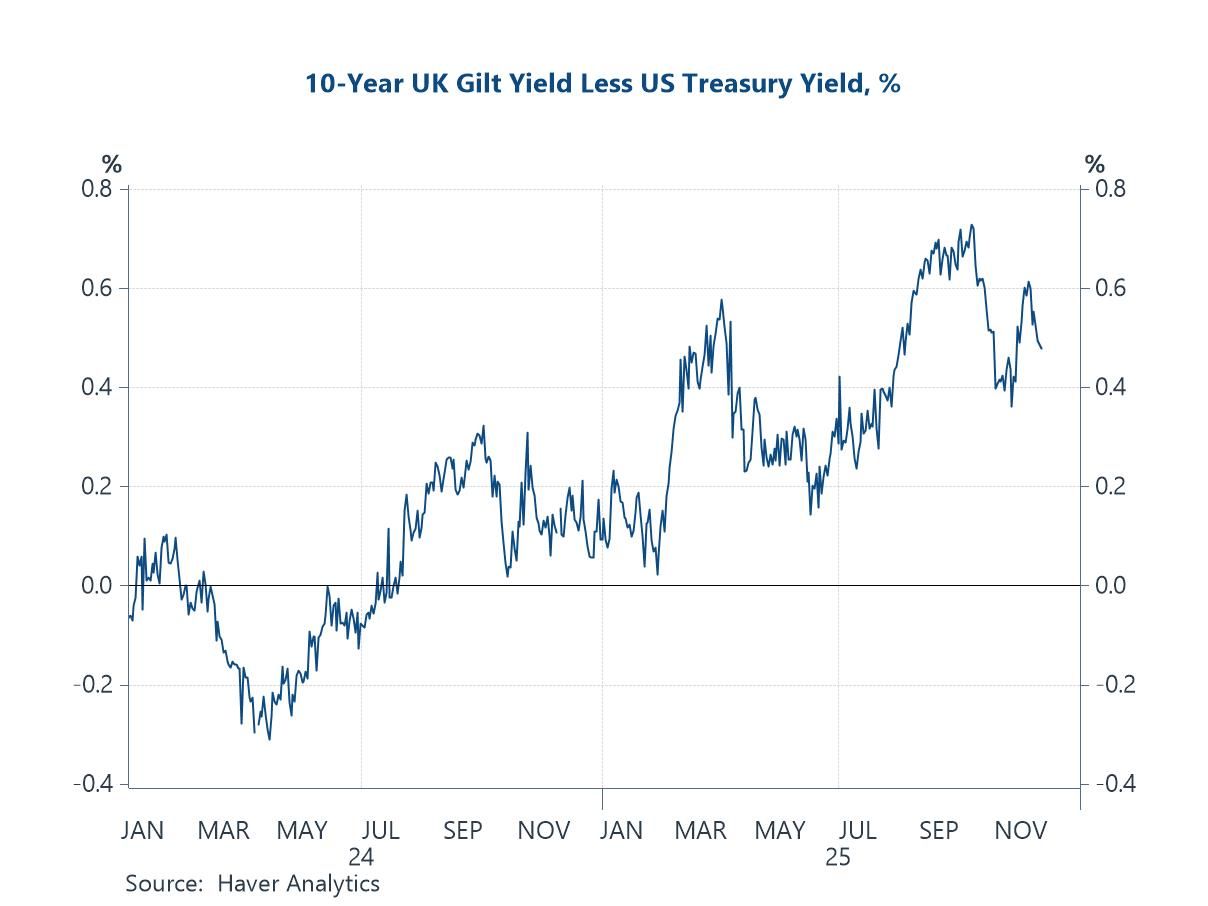

UK government debt The spread between 10-year UK gilts and US Treasuries has narrowed notably in recent weeks, unwinding part of the sharp premium that had built up through the summer and early autumn. This spread effectively represents the additional compensation investors demand for holding UK sovereign debt, and its further modest decline since the UK Budget last week suggests some easing of the political and fiscal risk premia that had accumulated earlier in the year. However, rather than reflecting improved confidence or clearer fiscal signalling, this move arguably appears driven more by the Budget’s explicit fiscal tightening and the associated downgrade to the UK’s growth prospects. Markets have interpreted the consolidation package—mainly through higher taxes—as dampening future demand, reducing inflationary pressure at the margin, and thereby lowering the expected path for UK gilt yields relative to Treasuries.

Chart 5: UK governnment bond yields versus US Treasury yields

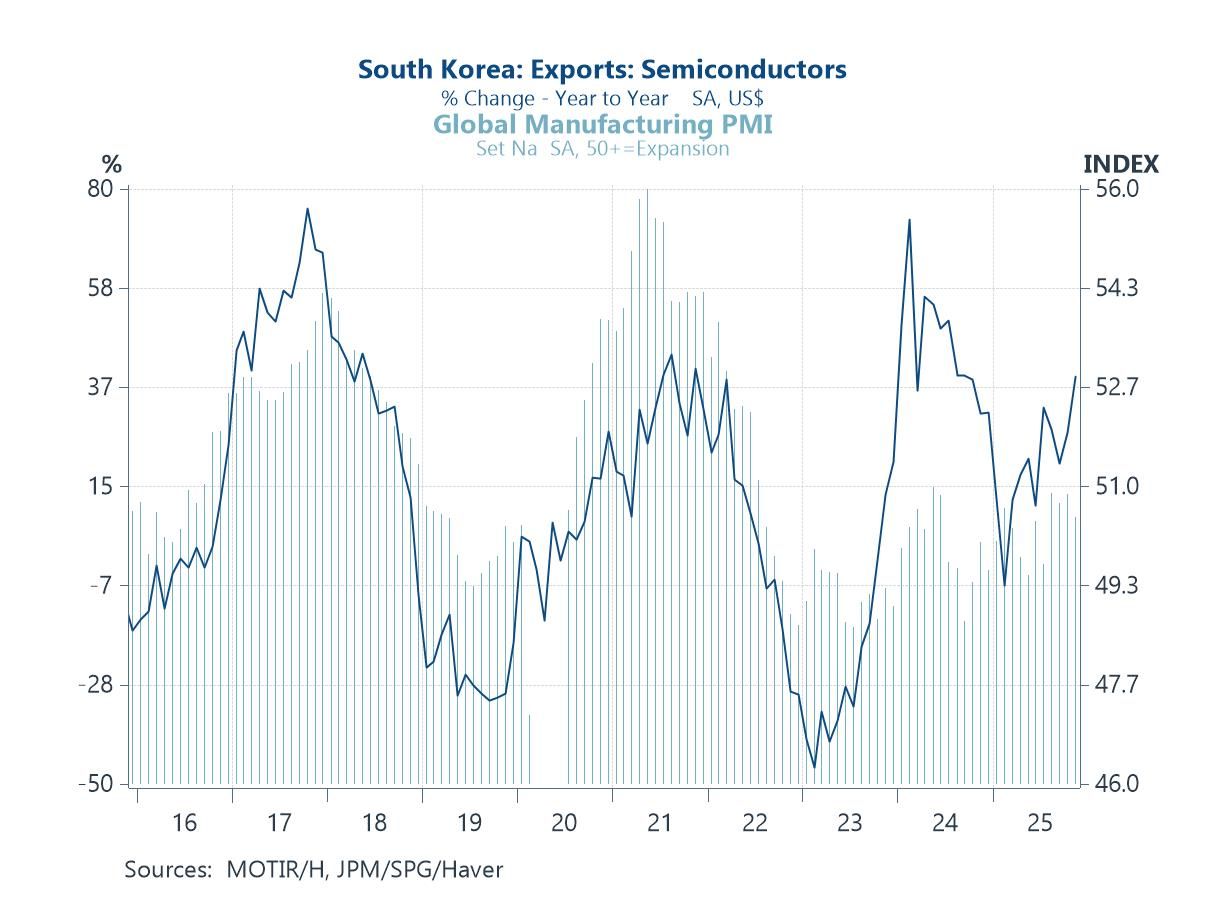

South Korea’s trade South Korea’s semiconductor export rebound continues to highlight how strongly the AI investment boom is feeding into global manufacturing. Chip exports, long a bellwether for the broader tech cycle, have swung firmly back into positive territory, historically a sign of improving global factory activity. The global manufacturing PMI has edged higher alongside this upswing, but it is worth noting that the PMI is still only pointing to very mediocre growth overall. In that context, the resurgence of semiconductor trade stands out even more clearly as one of the few genuine tailwinds in an otherwise subdued industrial landscape. For export-oriented Asian economies in particular, the AI-driven demand for advanced processors and memory chips is providing an important counterweight to broader global softness.

Chart 6: South Korea’s semiconductor export growth versus the Global Manufactuing PMI

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief