Global

GlobalFor much of the past decade, the working assumption was that interest rates, having collapsed after the financial crisis, would eventually fall back once the latest disturbance had passed. Events are now overturning that assumption—and not only in the United States. Both consensus forecasters and the Federal Reserve's model for estimating the equilibrium rate across advanced economies point to the same conclusion: the real rate of interest—the price of capital after inflation is stripped out—has risen and is likely to remain higher. The question is no longer whether this shift has occurred, but why so much of the financial system is still configured for a world we have left behind.

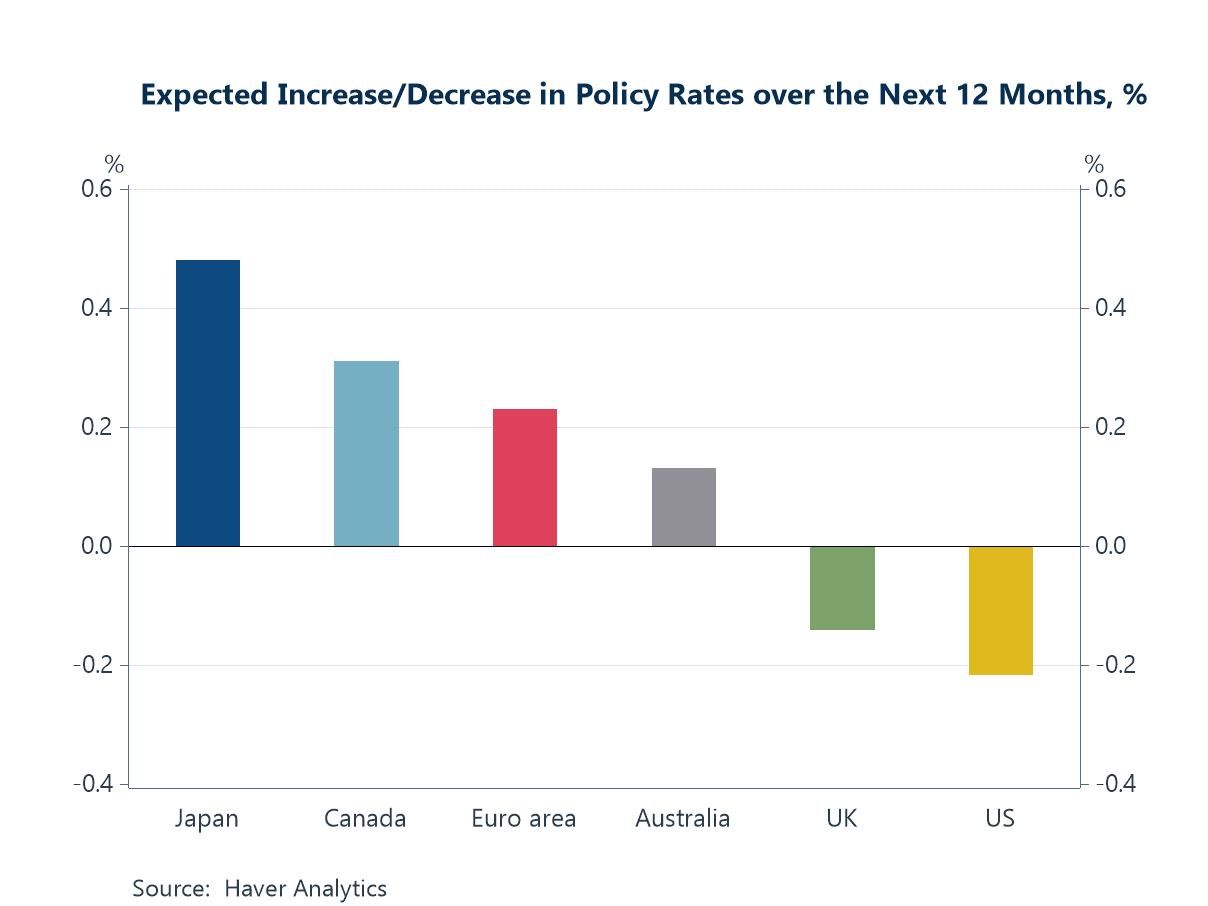

The evidence is clearest in the United States. The driver is the demand for capital: an investment cycle in artificial intelligence, defence and the reshoring of supply chains is competing for scarce savings, capacity and labour, and that raises the return the economy has to offer to fund it. It now shows up in the forecasts. Over the past six months the Blue Chip consensus for the US policy rate one year ahead has risen by about 44 basis points, while the consensus for inflation over the same horizon has barely changed; only around ten of those basis points reflect higher expected inflation. The remaining 34 are a higher expected real rate. Forecasters are not marking up the price outlook so much as the return on capital the economy can sustain.