The global macro backdrop remains dominated by instability in the Middle East and the lingering inflation concerns associated with elevated energy prices. Yet recent days have at least offered some tentative relief. Oil prices have softened amid heightened hopes that negotiations between the US and Iran could eventually ease tensions and help stabilise energy markets, even if the broader geopolitical situation remains fragile and key shipping routes continue to face disruption. Against this backdrop, the latest survey data continue to highlight an uneven global economy, with Europe looking particularly vulnerable given its greater sensitivity to higher energy costs and its weaker links to the global AI investment boom (chart 1). At the same time, rising gasoline prices continue to weigh heavily on US household confidence (the Michigan measure), raising concerns about the resilience of consumer demand (chart 2). An important question confronting markets in the meantime is whether inflation fears are now becoming overstated. Unlike during the post-pandemic inflation shock, central bank balance sheets are now shrinking rather than expanding aggressively, while money supply growth remains relatively weak across many major economies (charts 3 and 4). Meanwhile, the extraordinary boom in AI-related infrastructure spending — spanning data centres, utilities, water systems and semiconductors — continues to provide a major offset to broader macroeconomic weakness and remains a key pillar supporting global equity markets despite elevated geopolitical and inflation concerns (charts 5 and 6).

Introducing

Andrew Cates

in:Our Authors

Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

Publications by Andrew Cates

Global| May 28 2026

Global| May 28 2026Charts of the Week: The AI Boom Meets Inflation Angst

by:Andrew Cates

|in:Economy in Brief

Global| May 21 2026

Global| May 21 2026Charts of the Week: Surprise, Surprise

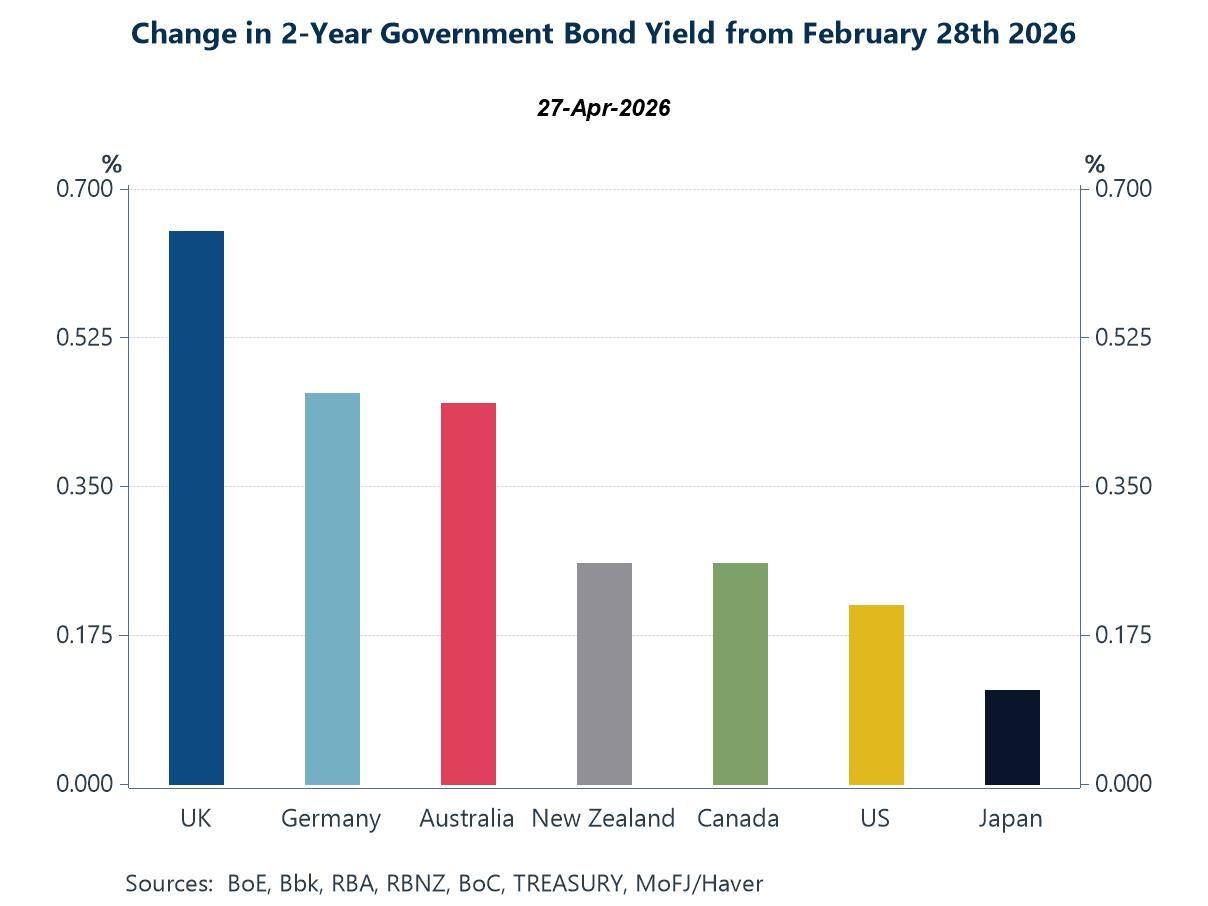

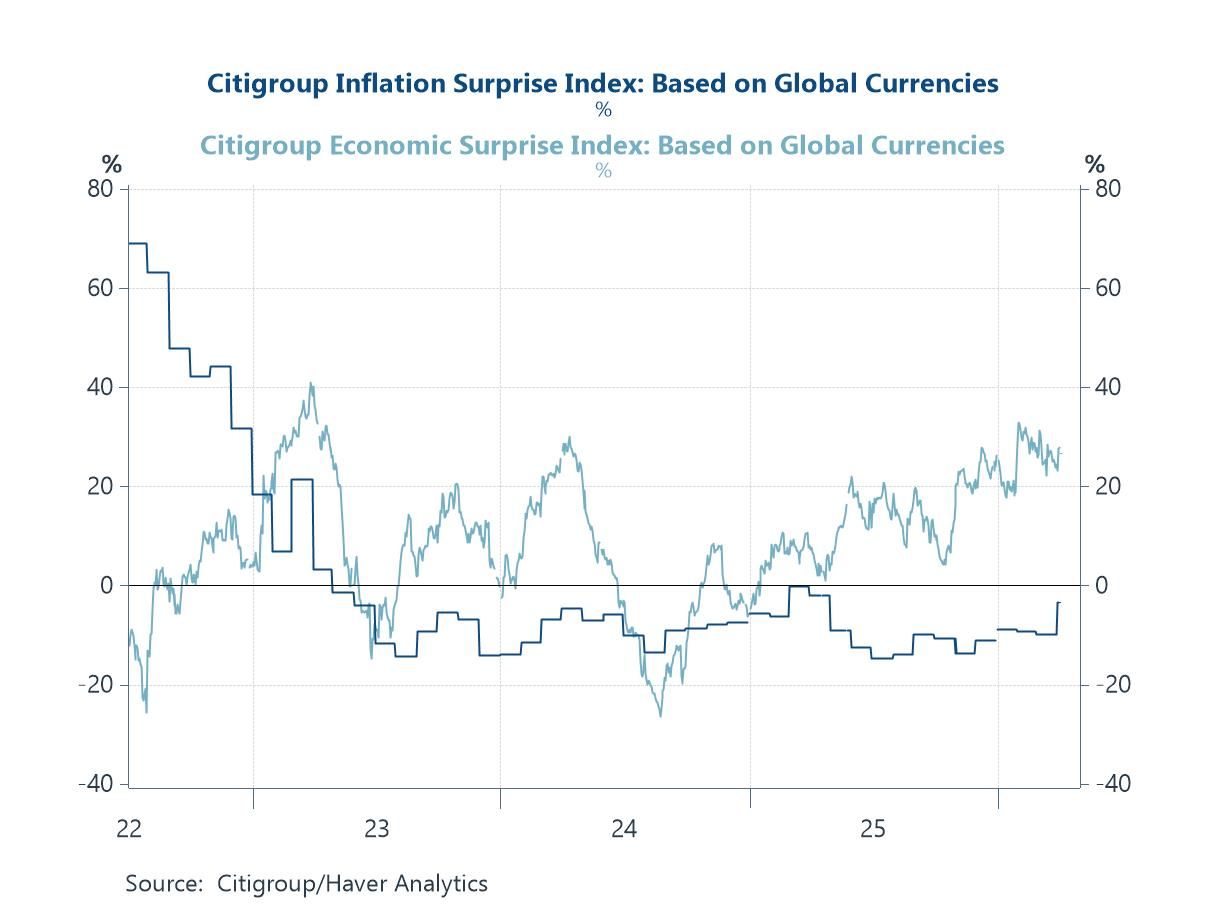

Ongoing geopolitical tensions in the Middle East and the associated surge in energy prices have pushed inflation and bond market concerns back to the forefront of global financial markets. Investors are increasingly worried that central banks may now face even greater difficulty in bringing inflation fully under control, particularly in economies where underlying price pressures had already remained sticky prior to the latest energy shock. Recent upside surprises in US labour market and inflation data have already contributed to higher Treasury yields and a broader global backup in short-term government bond yields across the major economies (charts 1 and 2). Yet the picture is not entirely one-sided. Labour’s share of US national income remains historically weak, suggesting limited underlying wage bargaining power and helping explain why broader inflation persistence could ultimately remain contained (chart 3). Meanwhile, oil prices have remained elevated despite some moderation in broader geopolitical risk indicators, reflecting persistent supply-side disruption and ongoing stress surrounding key global energy and shipping routes (chart 4). Even so, recent core inflation data from economies including the UK, Canada and Austria suggest that pass-through from higher energy costs into broader underlying inflation has so far remained relatively limited (chart 5). At the same time, financial markets continue to be supported by an extraordinary AI-driven investment boom, with technology firms engaged in an unprecedented surge in spending on data centres, semiconductors and energy infrastructure (chart 6). Increasingly, the global economy appears caught between two powerful and competing forces: renewed supply-side inflation risks on one side and a historic wave of AI-driven technological investment on the other.

by:Andrew Cates

|in:Economy in Brief

Global| May 14 2026

Global| May 14 2026Charts of the Week: The Tug of War

The global economy is still caught between two powerful and competing forces. On one side, the AI investment boom continues to support growth, industrial activity and equity markets, particularly in the US and parts of Asia. On the other, renewed Middle East tensions and higher energy prices are adding to inflation risks and broader policy uncertainty. The latest Blue Chip survey reflects this divide clearly: growth expectations have generally held up best in economies tied to AI-related investment and technology supply chains, while inflation forecasts have risen more sharply in more energy-exposed economies such as the UK and euro area (chart 1). Forecasters still largely expect only limited pass-through from higher energy prices into core inflation, although recent US CPI data suggest underlying price pressures remain somewhat sticky (charts 2 and 3). At the same time, the extraordinary continued surge in global AI investment — now approaching $300 billion annually — highlights the sheer scale of capital being deployed into semiconductors, data centres and digital infrastructure, particularly in the United States (chart 4). The divergence in industrial production trends also reinforces the growing gap between economies benefiting from structural growth drivers — such as Taiwan’s semiconductor sector and Denmark’s pharmaceutical industry — and those struggling with higher energy costs and weaker competitiveness, notably Germany and the UK (chart 5). Meanwhile, improving Chinese activity indicators suggest policy support and stronger technology demand may finally be helping to stabilise growth (chart 6). Overall, the world economy remains resilient, but increasingly uneven, with AI-related investment continuing to offset — though not eliminate — the drag from geopolitical fragmentation and rising energy insecurity.

by:Andrew Cates

|in:Economy in Brief

Global| May 07 2026

Global| May 07 2026Charts of the Week: Still Standing

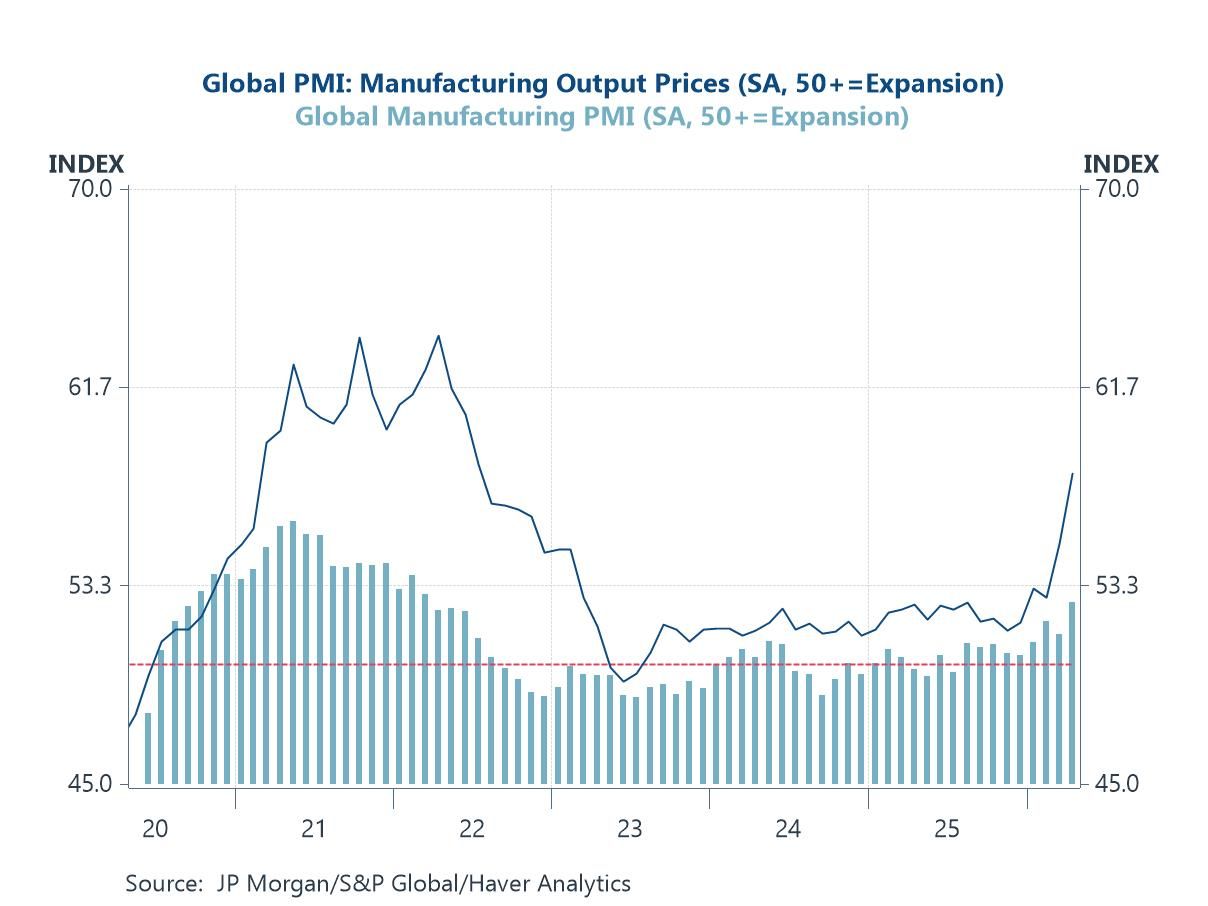

Recent developments point to the possibility of a peace settlement in the Middle East, which has offered some tentative relief to energy markets. Financial markets have responded with cautious optimism, but the outlook remains highly uncertain, with much depending on whether any agreement proves durable and supply disruptions are fully unwound. Against this backdrop, our charts this week highlight a global economy that is holding up better than expected but facing renewed cost pressures. Manufacturing activity remains resilient, supported by AI investment, reduced tariff disruption and defence spending, even as output prices firm (chart 1). Supply-side frictions are also still evident: shipping costs have risen, broader supply chain pressures are rebuilding (chart 2), and crude oil production has been curtailed by export and storage constraints among key regional producers (chart 3). These dynamics have reinforced inflation risks and shifted policy expectations in a more hawkish direction (chart 4). Meanwhile, US credit conditions appear broadly neutral, suggesting neither strong deleveraging nor releveraging pressures (chart 5). Finally, wage growth remains central to the outlook, particularly in the UK, where pressures are still comparatively elevated (chart 6). Taken together, the message is one of resilience under strain: growth is holding up, but the balance between inflation and activity is becoming increasingly delicate, leaving policymakers—and markets—navigating a narrow and uncertain path ahead.

by:Andrew Cates

|in:Economy in Brief

Global| Apr 30 2026

Global| Apr 30 2026Charts of the Week: Tension Beneath the Surface

Against a backdrop of persistent geopolitical tensions, firmer energy prices and a busy week of central bank meetings—including the Fed, ECB, BoE and BoJ—financial markets have remained notably resilient, even as the macro narrative has softened at the margin. The message from this week’s charts is one of growing tension beneath that surface calm. Front-end bond yields have moved higher, signalling a shift toward a more cautious, “higher-for-longer” policy outlook (chart 1). At the same time, real-time recession indicators for the United States suggest risks remain contained for now (chart 2). Consumer confidence data paint a more uneven picture, with sharper declines in the euro area and UK than in the US, highlighting regional vulnerabilities to the current energy shock (chart 3). The ECB’s latest bank lending survey reinforces this, pointing to tighter credit conditions and weaker demand—factors that are likely to weigh further on European growth (chart 4). By contrast, developments in the semiconductor sector underline a different dynamic: an intensifying global boom, with accelerating price pressures reflecting both strong AI-driven demand and emerging supply-side constraints linked indirectly to energy and logistics disruptions (chart 5). Finally, labour market data confirm that the AI surge is not merely a market narrative but a tangible structural shift, with hiring for AI-related roles accelerating across economies (chart 6). Taken together, these signals point to a more complex macro environment—one in which resilient markets coexist with softening growth, more persistent inflation risks and increasingly delicate policy trade-offs.

by:Andrew Cates

|in:Economy in Brief

Global| Apr 23 2026

Global| Apr 23 2026Charts of the Week: Risks Build, Markets Shrug

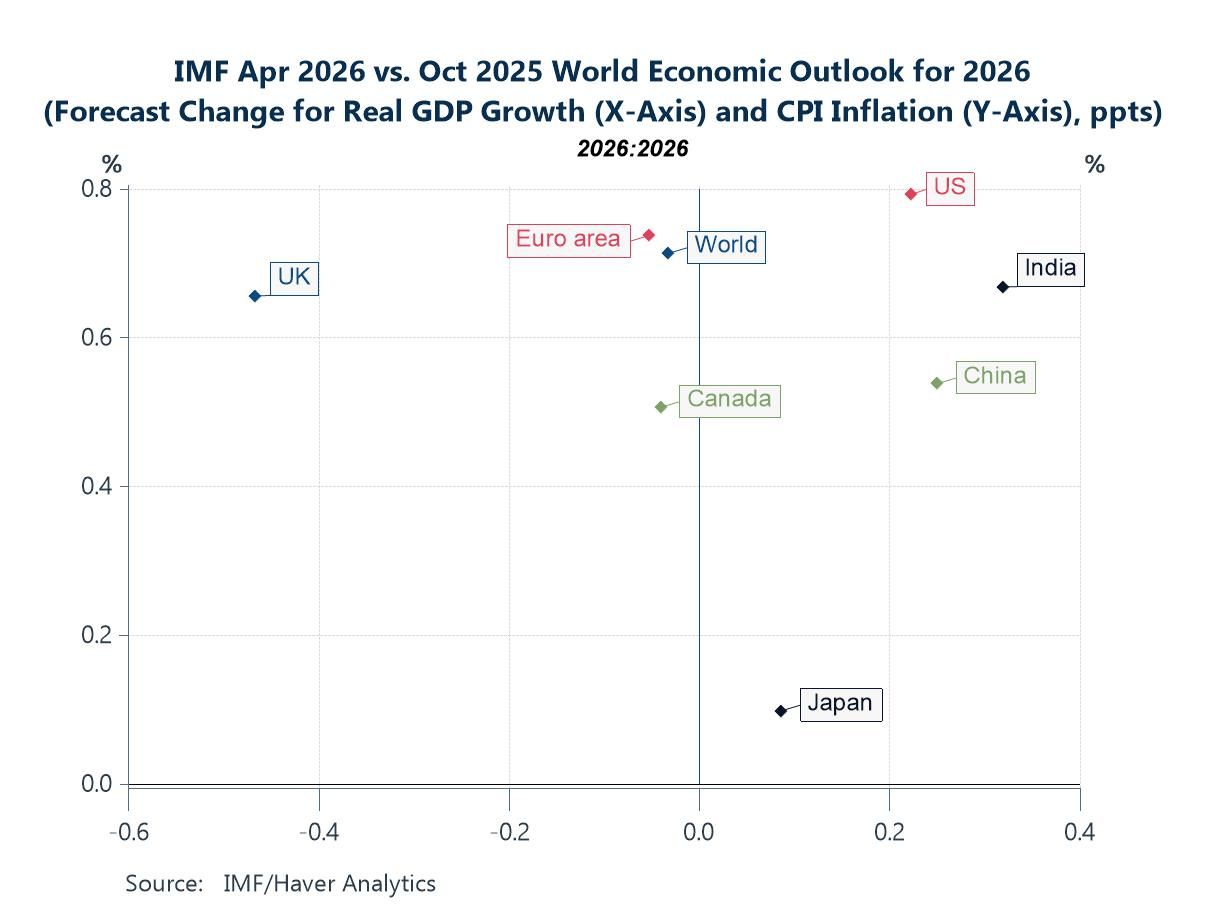

Financial markets have remained notably calm in recent weeks despite rising geopolitical tensions in the Middle East, a more downbeat macroeconomic narrative and elevated uncertainty. Measures of financial stress and volatility remain low, and equity markets continue to look through both the conflict and softer data. That resilience sits alongside a more nuanced macro backdrop. The IMF’s latest WEO revisions point to a classic stagflationary energy shock—growth downgraded and inflation revised higher—although the global impact remains modest and uneven, with some economies still benefiting from stronger momentum (chart 1). At the same time, market pricing appears increasingly detached from the data flow, with volatility declining even as growth surprises have turned more negative relative to inflation (charts 2 and 3). Incoming inflation data reinforce the idea of a largely headline-driven shock, with nowcasts rising in line with higher energy prices but only limited pass-through into core inflation so far (charts 4 and 5). However, it remains early days. Survey evidence, such as the latest ZEW release, suggests that inflation expectations may already be responding in a more concerning way, with a marked rise alongside weakening growth sentiment (chart 6). Taken together, the key question for markets is whether this remains a contained, energy-driven shock that can be looked through—or whether it begins to embed more persistently via expectations, forcing a reassessment of the currently benign outlook.

by:Andrew Cates

|in:Economy in Brief

Global| Apr 09 2026

Global| Apr 09 2026Charts of the Week: From Oil Shock to Policy Dilemma

Amid further tentative signs of de-escalation—most notably President Trump’s decision on April 7th to step back from further escalation—financial markets have stabilised somewhat, but the macroeconomic implications of the Middle East crisis remain highly uncertain. As our charts show, the global economy entered this shock from a position of relative strength, with positive growth surprises and easing inflation pressures still evident in the data (chart 1). However, that benign backdrop now looks vulnerable. Central banks are already reassessing the outlook, with expectations for policy easing being pared back (chart 2) and a growing consensus that any response to persistent energy-driven inflation will likely involve delaying cuts rather than tightening aggressively—albeit with significant regional divergence (chart 3). Financial markets, for their part, are not yet signalling a loss of inflation control, but the rise in real yields suggests increasing concern around the broader policy mix, particularly fiscal pressures (chart 4). Finally, the adjustment to the shock is unlikely to be uniform. Structural differences in domestic energy capacity are already driving wide divergences in electricity prices, leaving more import-dependent economies exposed to higher costs and sharper trade-offs between growth and inflation (charts 5 and 6). Taken together, the message is clear: even if geopolitical tensions ease, the economic aftershocks are likely to be uneven, persistent and increasingly shaped by structural constraints.

by:Andrew Cates

|in:Economy in Brief

Global| Apr 01 2026

Global| Apr 01 2026Charts of the Week: Strait Stress

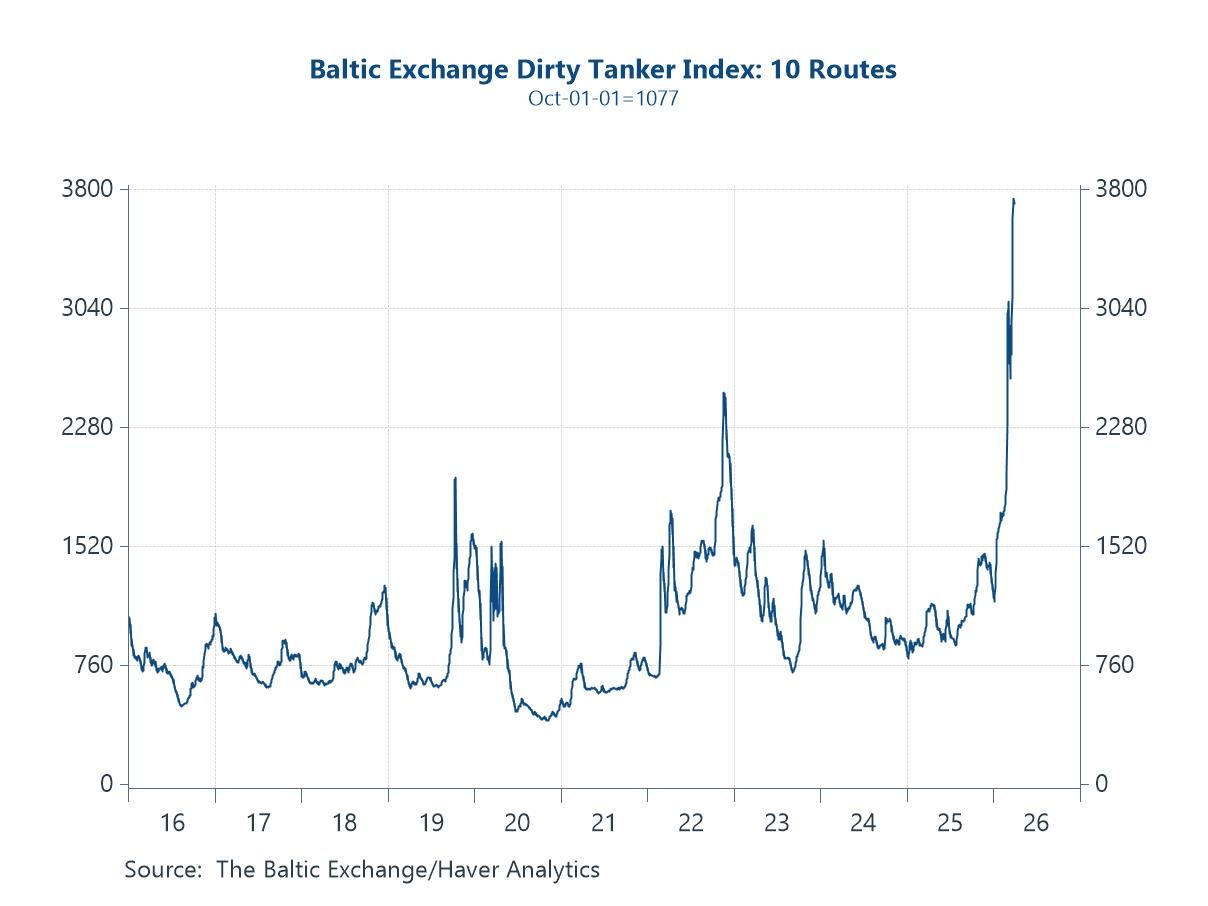

Amid tentative signs of de-escalation from the US administration over the past 48 hours—including suggestions that the conflict with Iran could conclude relatively quickly—financial markets have begun to retrace some of last week’s sharp repricing of Middle East risk. Oil prices have come off their highs, while equities and bonds have rallied as risk premia ease. That said, the earlier phase of the week saw a decisive adjustment: oil surged, front-end yields moved higher, and uncertainty rose as investors grappled with the implications of disrupted energy flows. Even now, the overall adjustment has been uneven—volatility has picked up, but not to levels typically associated with sustained geopolitical stress—raising questions about how fully markets are internalising both the risks and the rapidly shifting outlook. Our charts this week capture these cross-currents. Tanker rates have spiked as shipping routes are disrupted and capacity tightens (chart 1), while PMI delivery times point to early signs of supply chain strain feeding into the real economy (chart 2). At the same time, the divergence between elevated policy uncertainty and relatively contained market volatility suggests there could have been a degree of complacency (chart 3). The rise in oil prices is already feeding into higher short-term yields, though this is being tempered by cooling labour markets, anchored inflation expectations and more cautious central bank signalling (charts 4 and 5). Meanwhile, euro area flash CPI has picked up, but core inflation remains relatively benign, suggesting underlying price pressures are still contained for now (chart 6).

by:Andrew Cates

|in:Economy in Brief

Global| Mar 26 2026

Global| Mar 26 2026Charts of the Week: A Supply-Constrained World Comes into Sharper Focus

Recent de-escalation signals in the Middle East have offered some relief to markets, but the economic aftershocks from the earlier escalation are still feeding through—particularly via energy prices and heightened geopolitical risk. Crucially, these shocks are not hitting a clean cyclical backdrop. Instead, they are amplifying a set of pre-existing supply-side pressures—fragmented trade, strained supply chains, and a more complex policy environment—that have been building for some time. The charts this week pick up that theme. Forward-looking sentiment indicators suggest global growth has lost some momentum, even if activity remains in expansion territory (chart 1). At the same time, broader measures of uncertainty remain elevated (chart 2), while supply chain stress is once again moving higher, reinforcing the idea that disruption is becoming more structural (chart 3). Financial markets are reflecting this shift, with increased uncertainty around the future path of policy rates (chart 4), and survey evidence pointing to a more fundamental challenge around the credibility and transmission of monetary policy itself (chart 5). And yet, there are some offsets. Despite the recent spike in oil prices, medium-term inflation expectations—at least in the US—remain relatively well anchored (chart 6). Even so, the overall message is one of a more fragile, supply-driven cycle—where shocks like the Middle East do not just disrupt the outlook, but intensify the underlying constraints shaping the global economy.

by:Andrew Cates

|in:Economy in Brief

- Global| Mar 24 2026

Shock, Supply and Constraint

The Middle East crisis and the limits of the global economy

For three decades, macroeconomics has leaned on a simple idea: that demand management can stabilise the system. In reality, that framework has been fraying for years. The latest escalation in the Middle East doesn’t just reinforce the point—it sharpens it. This is not another cyclical shock, but a reminder that the global economy is increasingly governed by supply-side constraints that policy cannot easily offset.

Even with tentative signs of de-escalation emerging this week, the episode has brought into much sharper focus a theme I have been returning to repeatedly: the global economy is no longer primarily demand-constrained. It is increasingly shaped—and at times paralysed—by supply-side limits.

by:Andrew Cates

|in:Viewpoints

Global| Mar 19 2026

Global| Mar 19 2026Charts of the Week: Energy Shock — Early Signals, Uncertain Fallout

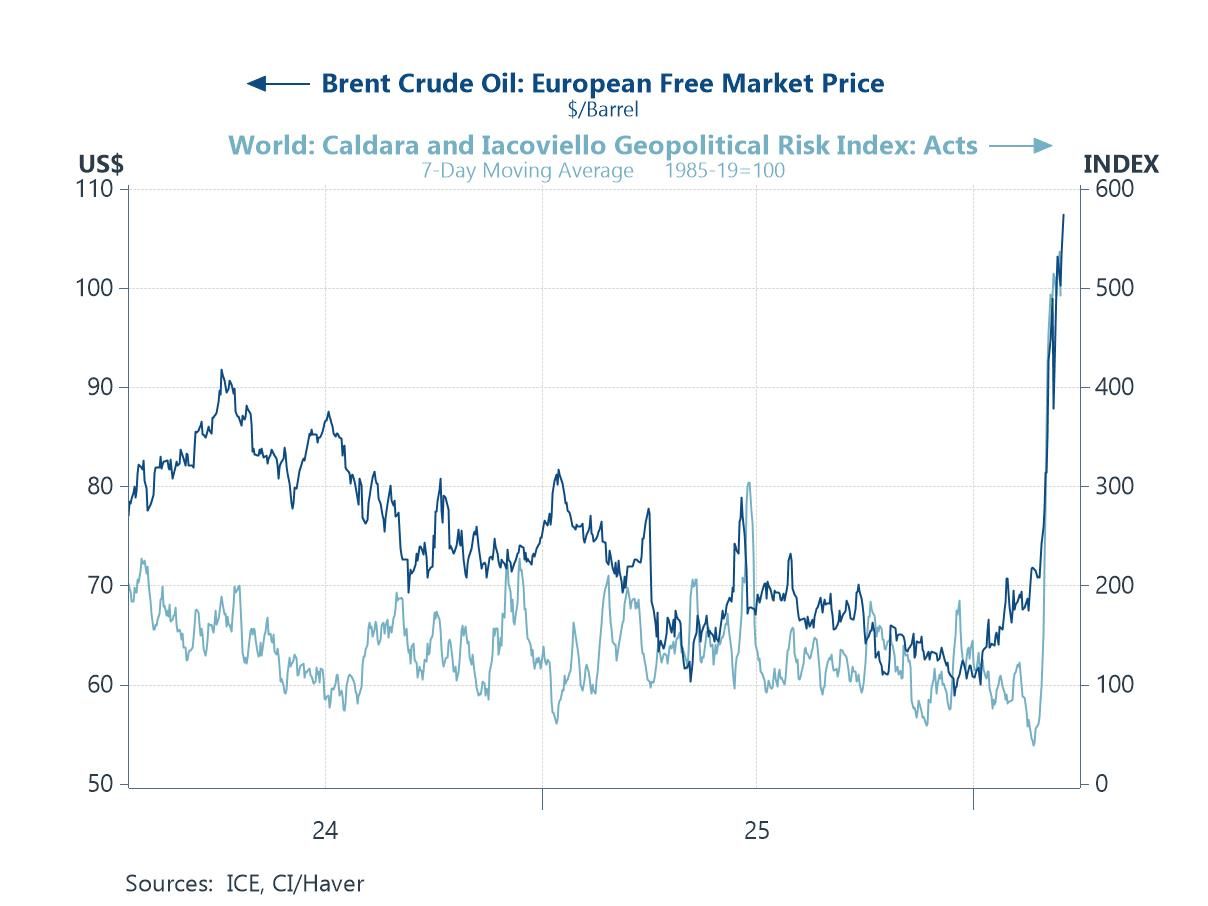

The past few weeks have seen a sharp escalation in tensions in the Middle East, triggering a rapid repricing across energy markets and a rise in geopolitical risk (chart 1). This comes at a time when the global economy is still heavily dependent on fossil fuels, leaving it structurally exposed to such shocks (chart 2), while longer-run increases in energy use per capita—driven in large part by industrialisation in China and elsewhere—have contributed to a rise in real energy prices over time (chart 3). Financial markets have been responding, with short-dated bond yields edging higher as expectations of monetary easing are reassessed (chart 4), and forward-looking sentiment indicators are showing early signs of softening (chart 5). At the same time, and of note, there are some tentative signs of stabilisation in parts of the global economy, notably in China where investment has picked up at the margin, supported by policy-led infrastructure spending (chart 6). Even so, it remains early days, and the balance of risks continues to tilt toward a more fragile outlook should the instability in the Middle East persist.

by:Andrew Cates

|in:Economy in Brief

Global| Mar 11 2026

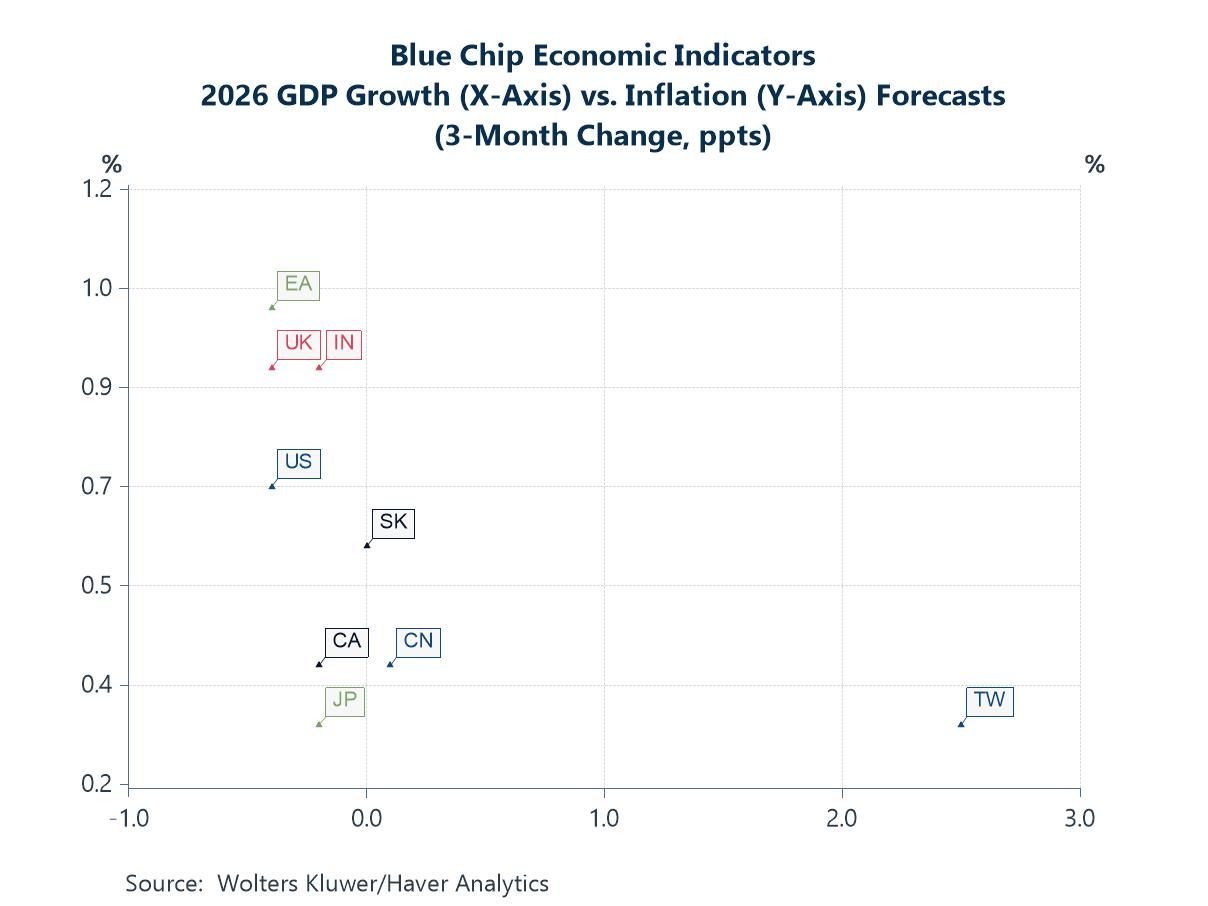

Global| Mar 11 2026Charts of the Week: Geopolitics Meets the Global Economy

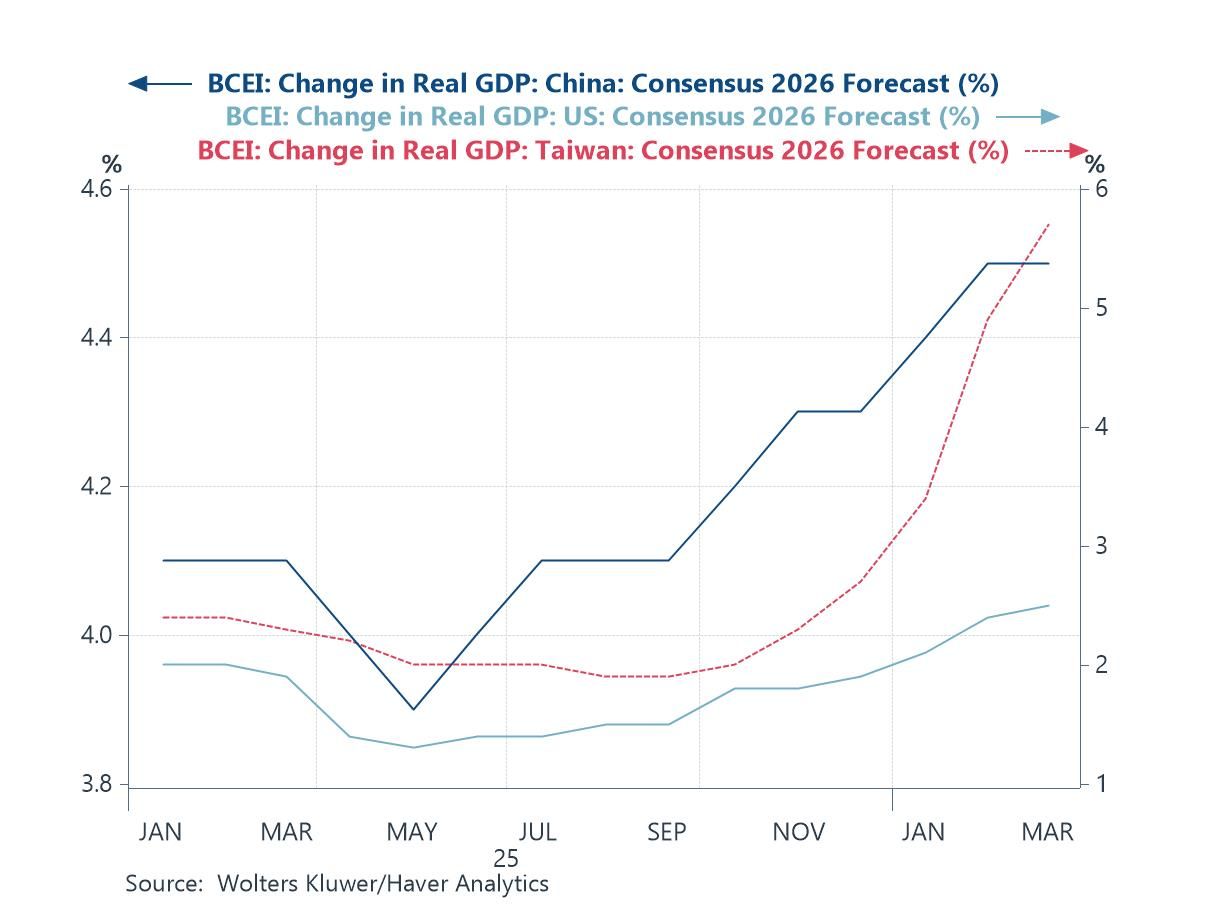

The past few days have seen financial markets rattled by a sharp escalation of tensions in the Middle East, with oil prices rising, risk assets wobbling and investors reassessing the potential macroeconomic fallout from a possible energy shock. Yet, taken together, this week’s charts suggest that the global economic outlook has so far remained relatively resilient. Blue Chip consensus forecasts for 2026 growth have held steady in recent months, with Taiwan’s steadily improving outlook hinting at the ongoing influence of the global AI investment cycle. That said, forward-looking sentiment indicators are beginning to show some cracks: the latest Sentix expectations index registered a sharp deterioration in March, potentially reflecting rising geopolitical uncertainty. Inflation expectations, by contrast, have shifted only modestly, with forecasters making few meaningful revisions despite the recent surge in oil prices. Financial markets appear to share that view, as movements in two-year US Treasury yields—often a proxy for expectations of Federal Reserve policy—have not mirrored the sharp rise in crude prices, suggesting investors currently see the oil shock as temporary. The final charts highlight why energy markets nonetheless remain central to the outlook: many major economies remain significant net oil importers, and in much of Asia oil price movements feed quickly into consumer energy inflation. Should geopolitical tensions persist and keep crude prices elevated, these channels could yet transmit broader macroeconomic pressures in the months ahead.

by:Andrew Cates

|in:Economy in Brief

- of23Go to 2 page