Global| Feb 05 2026

Global| Feb 05 2026Charts of the Week: Balanced Policy, Resilient Data and AI Narratives

by:Andrew Cates

|in:Economy in Brief

Summary

Financial markets have experienced renewed gyrations in recent weeks, as shifting geopolitical risks, questions around Federal Reserve independence, renewed talk of US dollar “debasement,” and ongoing enthusiasm surrounding artificial intelligence have combined to drive volatility across asset classes. These cross-currents have also contributed to a degree of rotation away from high-flying technology stocks, as investors reassess valuations and the timing of anticipated AI-driven gains. Against this backdrop, the charts in this week’s COTW highlight several important themes. Policy rate expectations now appear more balanced globally, marking a clear shift away from the one-sided easing bias of the past two years (chart 1), even as resilient US data—underscored by the unexpected jump in the January ISM index and a run of positive economic surprises—continues to complicate the outlook for monetary easing (chart 2). At the same time, US financial conditions remain relatively benign, with limited evidence of widespread credit stress or aggressive tightening in lending standards (chart 3). Meanwhile, the sharp rebound in semiconductor sales and the accelerating rollout of large-scale AI models underscore why investors remain so focused on the AI narrative, even as Europe lags behind due to weaker industrial momentum and a smaller footprint in advanced chip production (charts 4 and 5). Finally, while some scepticism about AI’s ultimate economic impact persists, the latest survey results suggest a moderation in concerns that markets are materially overestimating its gains (chart 6). Taken together, these developments paint a picture of a US economy that remains more resilient than many had anticipated, set against a financial landscape increasingly shaped by powerful—if sometimes competing—narratives around geopolitics, policy, and technological transformation.

The Global Monetary Policy Consensus The latest Blue Chip Financial Forecasts survey points to a notably more balanced global monetary policy outlook over the coming year. In contrast to the pronounced easing bias that dominated much of the past two years, expectations are now more symmetric, with a similar number of central banks projected to raise rates as to ease policy. Japan is seen delivering further tightening, while Canada is expected to initiate an interest rate hike in coming months. In Australia’s case, this tightening guidance was reinforced this week, with the Reserve Bank lifting its policy rate by 25 basis points. Elsewhere, and in contrast, the euro area, UK and US are expected to move in the opposite direction.

Chart 1: Blue Chip Financial Forecasts: Expected change in policy rates over the next 12 months

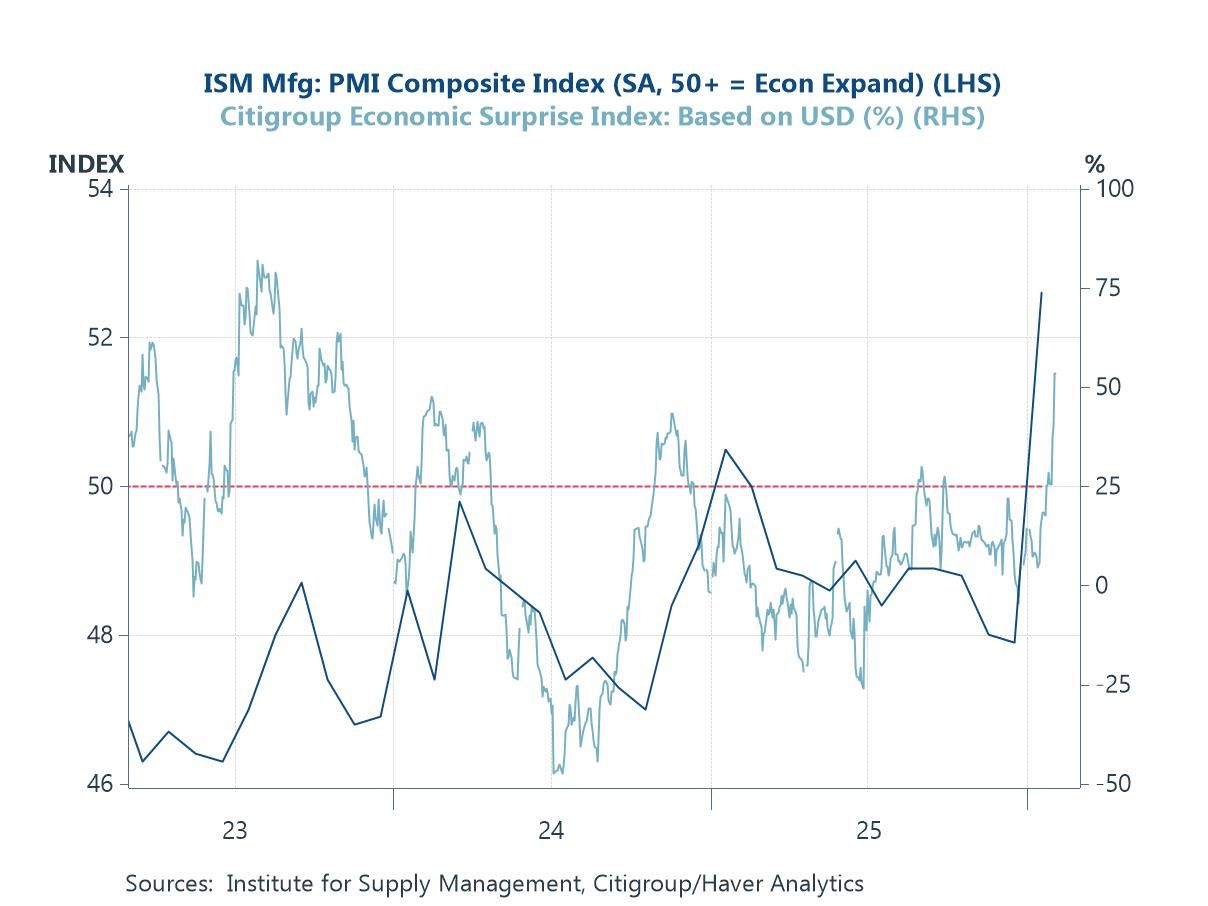

US manufacturing activity The second chart underscores the recent improvement in US economic momentum, highlighted by an unexpected surge in the January ISM manufacturing PMI. After spending much of the past year hovering below the 50 threshold consistent with stagnation, the index jumped sharply back into expansionary territory, signalling a renewed pickup in industrial activity. This rebound has coincided with a broader run of stronger-than-anticipated US economic data, as reflected in the upswing in the Citigroup Economic Surprise Index. Together, these developments point to a US economy that continues to display notable resilience, complicating expectations of monetary easing in the near term.

Chart 2: US Manufacturing ISM Index versus Citigroup’s US Growth Surprise Index

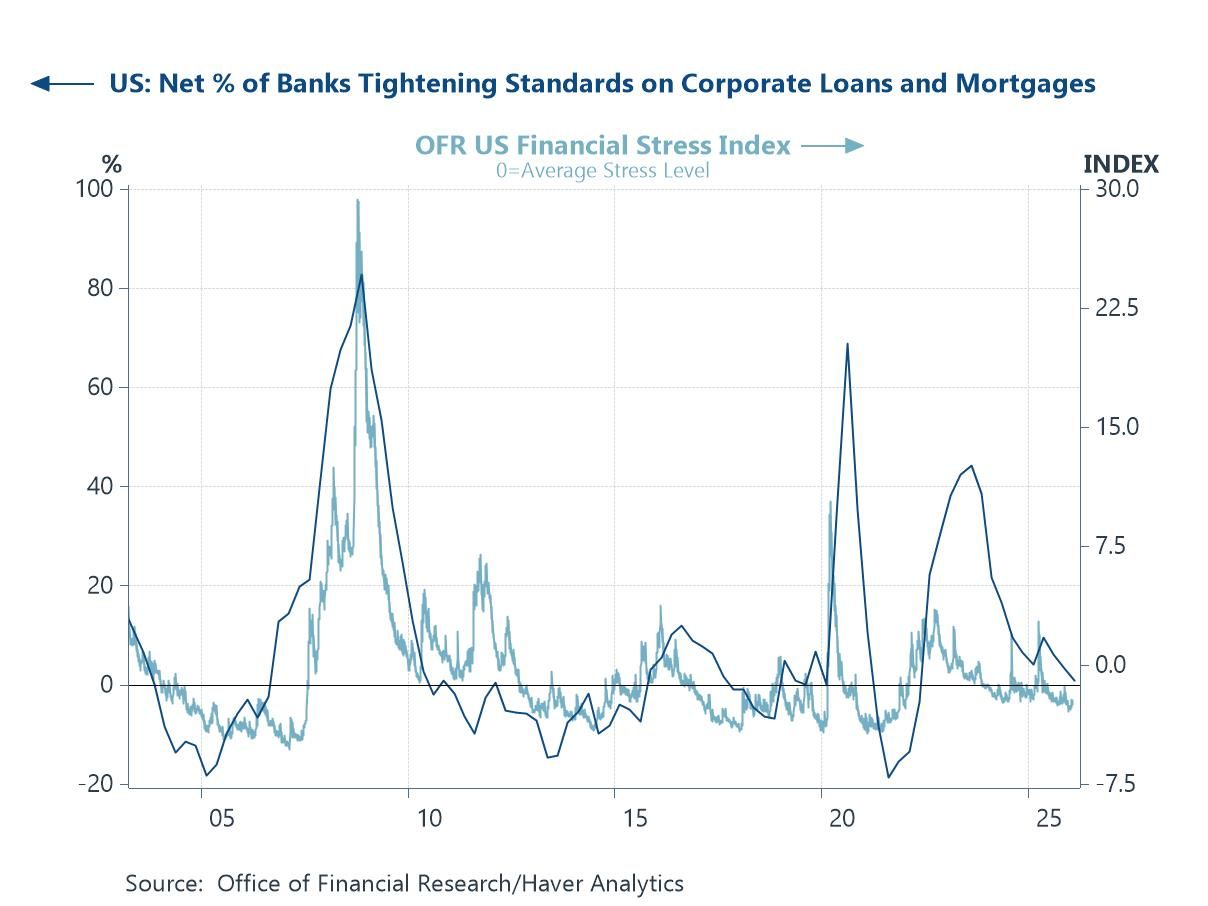

US Bank Lending Standards and Financial Stress The next chart turns to US financial conditions, highlighting the latest readings from the Senior Loan Officer Opinion Survey. The net proportion of banks tightening lending standards on corporate loans and mortgages is now more modest by historical standards, and well below the extremes seen during past episodes of financial stress. Some easing in credit headwinds has occurred alongside relatively subdued readings on the OFR Financial Stress Index, which continues to hover below its long-run average. Together, these indicators suggest that the US financial system has continued to avoid the kind of acute stress typically associated with sharp slowdowns in credit availability—helping to underpin the recent resilience in economic activity.

Chart 3: US Credit Standards On Corporate and Mortgage Lending Versus Financial Stress

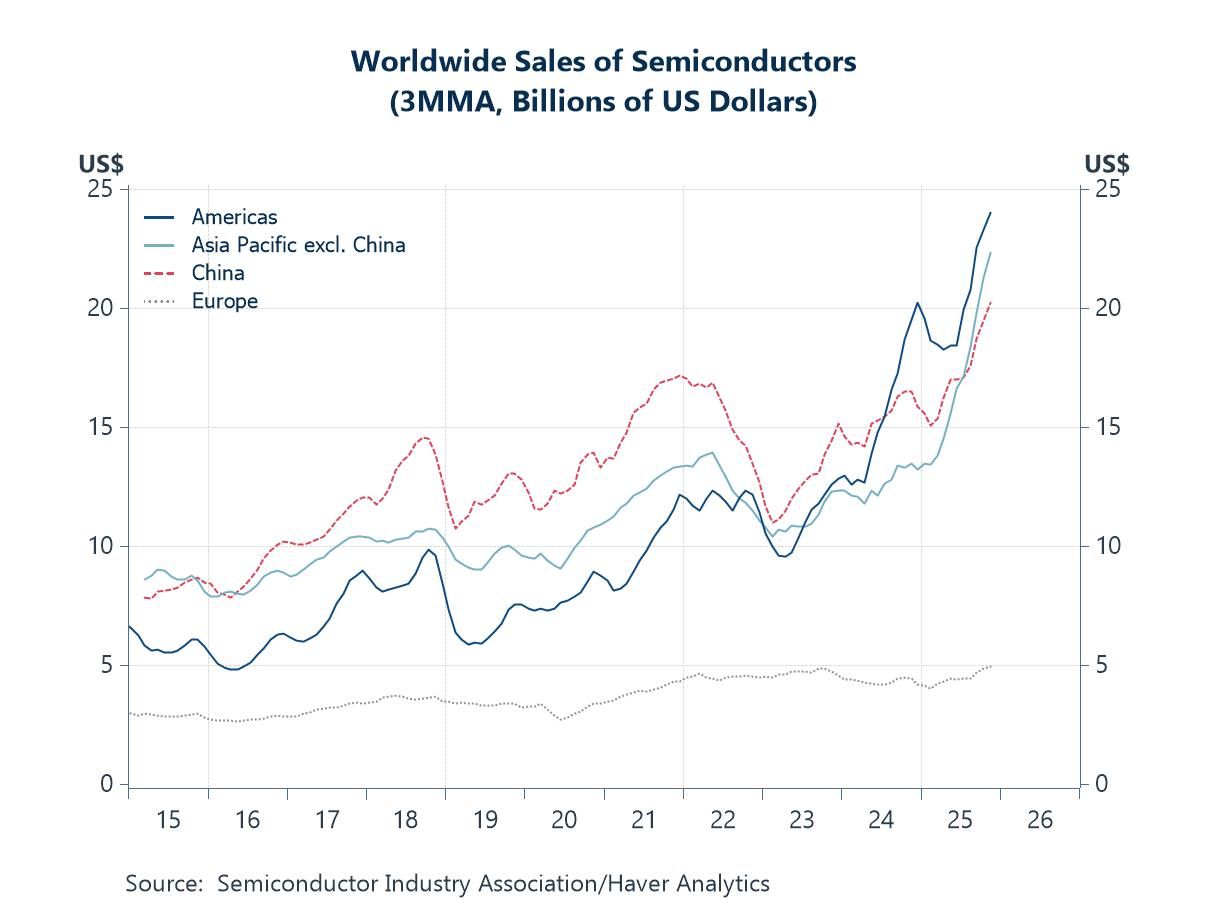

Semiconductor Sales The fourth chart highlights the renewed surge in global semiconductor sales, with momentum strengthening sharply over recent months across the Americas, China and the broader Asia-Pacific region. After the cyclical downturn in 2022–23, sales have rebounded to fresh highs, reflecting a powerful revival in demand for advanced chips and related technologies. This upswing has taken place amid intense investor preoccupation with artificial intelligence, with expectations that AI adoption will drive a sustained wave of capital spending on data centres, cloud infrastructure and high-performance computing. In contrast, semiconductor sales in Europe remain comparatively subdued, reflecting the region’s smaller footprint in high-end chip manufacturing, weaker industrial demand, and the ongoing impact of slower economic growth. While semiconductors are inherently cyclical, markets have increasingly interpreted the current rebound elsewhere as structural rather than purely cyclical—underpinned by the belief that AI represents a transformative and durable source of demand growth.

Chart 4: Worldwide Sales of Semiconductors

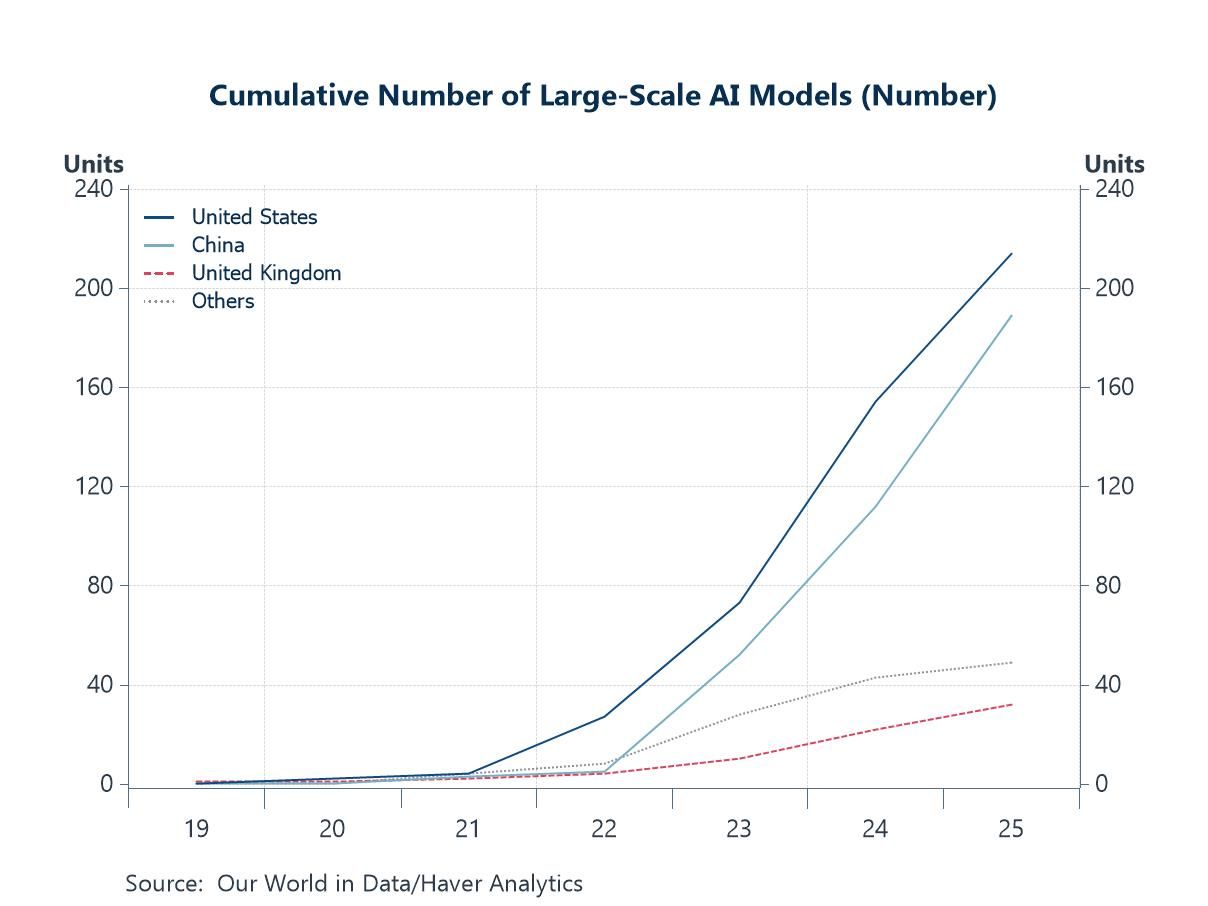

Large-Scale AI Models The next chart illustrates the rapid proliferation of large-scale AI models globally, with newly updated data for 2025 pointing to a further sharp acceleration in development activity. The United States continues to lead by a wide margin, while China has also seen a steep rise in model deployment in recent years, underscoring the intensifying technological competition between the two economies. Growth in the UK and other regions has been more modest by comparison, highlighting the increasingly concentrated nature of AI innovation. Taken together with the surge in semiconductor sales, these trends help explain the market’s strong preoccupation with AI as a potential driver of future productivity and investment cycles—although the geographic concentration of activity also raises questions about the uneven distribution of any resulting economic gains.

Chart 5: Cumulative Numbers of Large-Scale AI Models

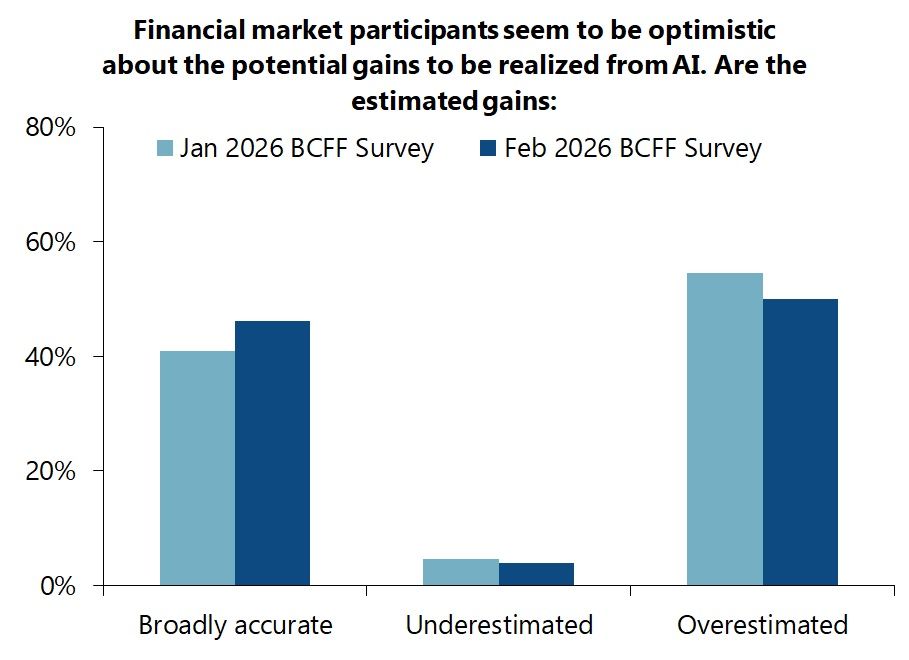

An AI Bubble? The final chart draws on the latest Blue Chip Financial Forecasts special questions, highlighting market participants’ perceptions of the economic gains likely to be delivered by artificial intelligence. While a sizeable share of respondents still believe that financial markets may be overestimating AI’s potential benefits, an increasing proportion now judge current expectations to be broadly accurate, with only a small minority viewing the gains as underestimated. Notably, this represents a softening in scepticism compared with the survey results from last month, when concerns about excessive market optimism were more pronounced. The shift suggests a growing acceptance that AI-related investment and innovation could translate into meaningful economic impacts—though uncertainty remains high around the scale, timing and distribution of these gains.

Chart 6: Blue Chip Financial Forecasts: Market Participants’ Views on AI

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief