German IP Reveals Chaotic Trends

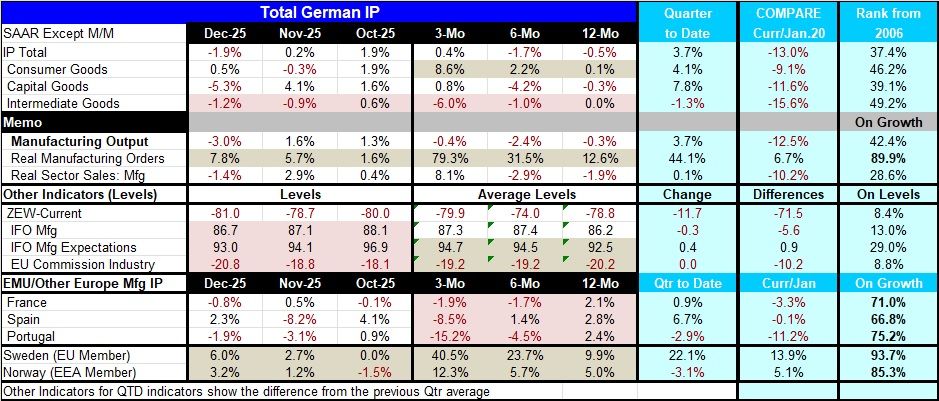

With the December report, Germany’s production and some of the early European industrial production data reveal a good deal of chaos in terms of the embedded trends. On the month, German industrial production fell by 1.9%, with consumer goods output up by 0.5%, capital goods output falling by 5.3%, and intermediate goods output falling by 1.2%. Among the early reporters in the monetary union—France, Spain, and Portugal—only Spain showed an increase in manufacturing IP in December; however, Spanish industrial production is notoriously volatile.

Broader IP trends in Germany and elsewhere in Europe As for other early industrial production reporters, both Sweden and Norway showed strong-to-solid gains in December and each of them showed two-months of gains in a row. Beyond that, sequential growth rates from 12-months to six-months to three-months show accelerating growth in German consumer goods output against decelerating growth for intermediate goods. Real manufacturing output and real sales show mixed results- no clear trends; however, real manufacturing orders in Germany are off the map strong.

German manufacturing/industrial Surveys German industrial surveys from the IFO for manufacturing shows persistent weakening as well as for IFO manufacturing expectations, and in the EU Commission industrial index in the last three months. More broadly, Germany shows some modest but ongoing step up all of these based on average levels from 12-months to six-months to three-months for IFO expectations and the EU Commission industrial readings with mixed results for other survey readings.

IP trends in Europe For the early reporting EMU members France, Spain, and Portugal, who report industrial production trends, each show mixed monthly trends against ongoing decelerations for manufacturing output over the broader sequential periods (12-month, to 6-month, to 3-month). However, for other Europe, Sweden and Norway, manufacturing trends are steadily accelerating on this broader timeline.

A feeling of ‘Deja- What?’ These combinations of opposed trends mixed with a lack of trends leave us with this sense of confusion about what's going on in manufacturing. For Germany, the extreme strength in orders is reassuring since orders should be forward-looking rather than backward-looking or even contemporaneous. But orders can also be a fickle series and so we'll have to watch it to see if the trends for German orders hold up.

Current quarter-What’s been happening now In addition, current quarter growth for Germany actually looks quite good with industrial production up 3.7% at an annual rate in the current quarter, led by output increases in manufacturing against a decline in the intermediate goods output. Real orders in the quarter are surging at a 44% growth rate, while real sales in manufacturing only had a 0.1% uptick at an annual rate. The industrial indicators for Germany in the quarter show weakness or flatness with the only exception being IFO manufacturing expectations that advanced by a small amount. The three EMU members who report industrial production data show positive growth in the just-completed quarter except for Portugal where industrial production is falling at a 2.9% rate in the fourth quarter. Sweden and Norway, European countries but not monetary union members, show a strong 22% annual rate gain in Sweden against the 3% annual rate decline in Norway.

Rankings How growth rates stack up… Moving away from short-term trends, the rankings of growth rates of these various metrics using 12-month growth rates on data back to 2006, show below-median growth rates for German industrial production and all three of its major sectors. All of them have rankings below the 50% mark where the median resides. Germany’s manufacturing output growth rate is below its median as is the growth of real sales; and once again real manufacturing orders break out and show a stunning 90th percentile standing, extremely strong compared to other growth rates on this period.

Indicator rankings are poor However, the survey based industrial indicators for Germany, ranked based on their index levels, are all extremely weak and much weaker than German sector or other German metrics. The strongest indicator reading is the 29th percentile standing for IFO manufacturing expectations while the current ZEW index, IFO manufacturing index, and the EU Commission industrial readings, all reside below their 15th percentile. The survey rankings suggest that industrial sentiment is in much worse shape than activity and growth.

IP elsewhere in Europe However, the growth ranking of manufacturing industrial production for the reporting EMU members and other European members are all quite solid, with percentile standings ranging from the 66th up to the 93rd percentile.

Summing up From these data, Germany emerges as the weak economy compared with historic norms based on industrial production growth and indicator readings. However, there's a glimpse of positivity from the growth of real orders, and at the same time, some concern about ongoing sentiment for manufacturing in Germany as distinct from actual performance.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global