German Orders Gain Pace- Clear Uptrend

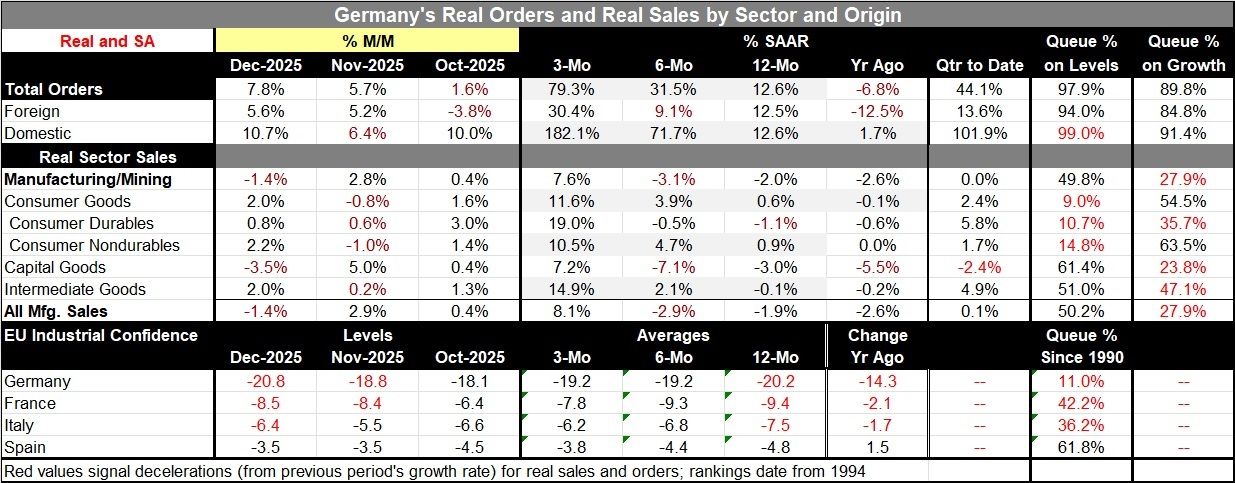

German real orders in December adjusted for inflation rose strongly again, gaining 7.8% month-to-month after rising 5.7% month-to-month in November. Foreign orders were up by 5.6% in December compared to 5.2% in November. Domestic orders surged by 10.7% in December after rising 6.4% in November and 10% in October.

Real sales Real sales were mixed in December with overall sales falling 1.4% month-to-month mostly on weakness in capital goods sales.

Broad categorical acceleration Many flows are accelerating this month. Sequential growth rates show acceleration. Total real orders accelerate from a year ago, to the current year, to six-months, and to three-months. Sales growth rates for consumer goods, consumer nondurables, and intermediate goods all show accelerations in gear. The exceptions are foreign orders that are not as strong over six months compared to their 12-month growth. And on the sales side, consumer durables sales and capital goods sales are weak.

Quarter-to-quarter Quarterly annualized growth is complete for Q4 with this report. Foreign orders are the ‘weak flow’ expanding at a 13.6% annual rate – certainly not a weak growth rate. But domestic real orders are up at an astounding 101.9% annual rate. The net impact on the total real orders growth is to lift it to a pace of 44.1%.

Order ranking is very strong The table provides two rankings: one based on the level of variables and the other based on its year-on-year growth. The rankings this month for real orders overall, foreign, and domestic orders all reside in their top 80th to 90th percentiles- extremely strong based on level or growth. Sales do not follow suit. This gives us some reason to suspect that there is some lumpiness involved in the manufacturing data as distinct from strength. That will be something to watch. Overall mining and manufacturing sales growth is essentially at its historic median at a rank of 49.8. However, capital goods, intermediate goods and manufacturing sales all have rankings at or above their medians - as high as a 61-percentile standing for capital goods.

Industrial confidence Industrial confidence for Germany, France, Italy and Spain (the EU’s big-four economies) show rankings based on these survey levels that are much lower at the 11th percentile for Germany, the 42nd and 36th percentiles, for France and Italy, respectively. Spain scores better with a 61.8 percentile standing on its industrial confidence measure.

On balance, there is now an accelerating profile that is broad in sales trends and especially strong order trends. Perhaps Europe, under the pressure to stimulate its miliary capabilities, has a core of demand to help drive output ahead more consistently. This is something to watch in the coming months.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global