Global

GlobalThe S&P manufacturing PMIs for July show a group of 17 countries plus an aggregate for the European Monetary Union. Across these 18 observations, there is broad, but uneven, improvement on a month-to-month basis.

The median reading for July increases slightly to 51.9, a gain of 0.5 diffusion points on a month-to-month basis.

44.4% of reporters are improving on a month-to-month basis. Measured over three months compared to six months, 33.3% are improving; over six months compared to 12 months, 66.7% are improving; and over 12 months compared to 12 months ago, 83.3% are improving. Despite the monthly statistics showing a mixed performance and evidence of some soft spots, the general trend for manufacturing is to show that improvement is in place.

The percentile standing for the July diffusion indexes on data back to 2021 shows an average standing of the 69th percentile across the 19 reporters. That means since 2021 the observations have generally been stronger than this only about 30% of the time, marking this as an ongoing improving situation for manufacturing.

The reporting countries with percentile standings below their medians (below a 50% standing on a queue basis) are China, Russia, India, Brazil, Indonesia, and Turkey.

The strongest countries on a queue percentile standing basis are Japan with a 91.0 percentile standing and Mexico with an 88.1 percentile standing. In addition, South Korea has an 85.1 percentile standing and Malaysia has an 83.6 percentile standing.

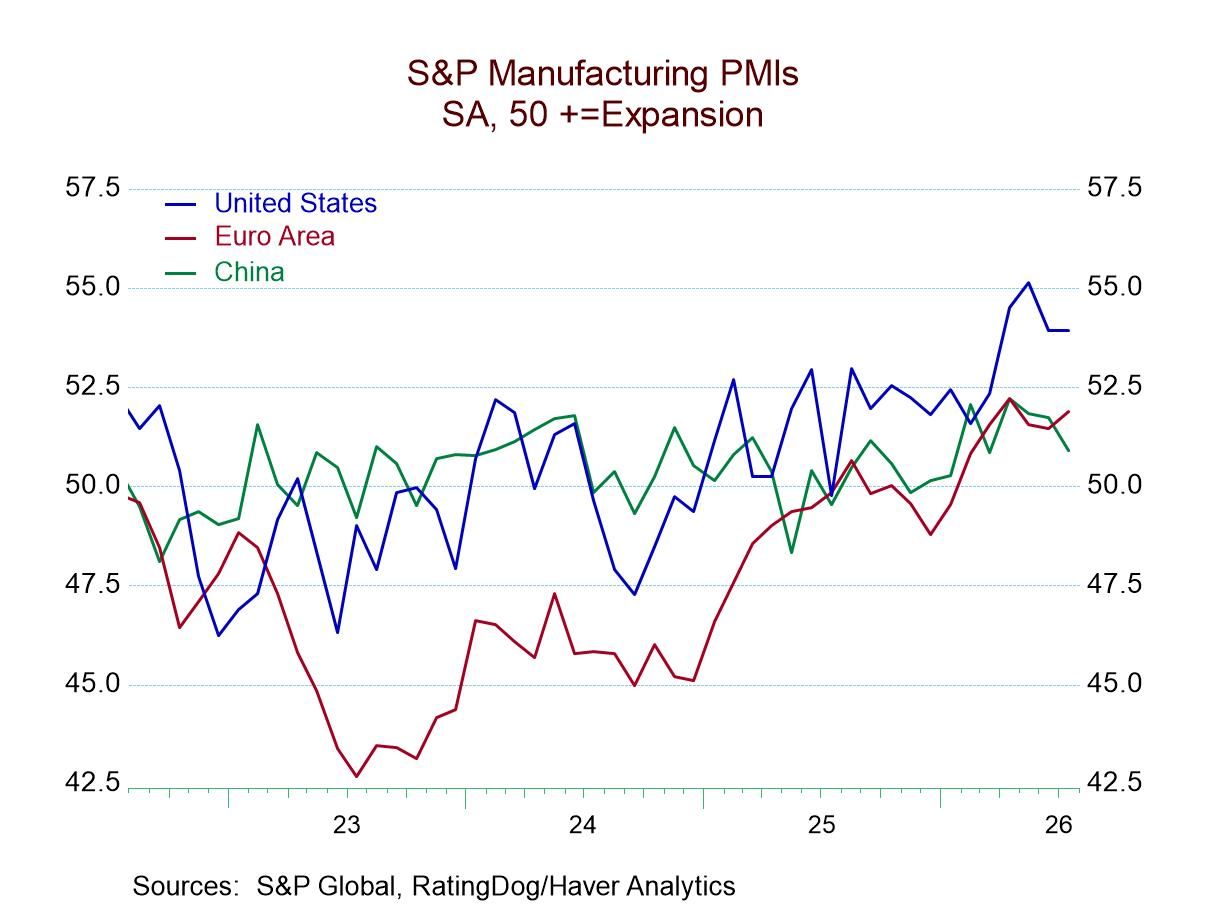

At the bottom of the table, we have groupings of countries by various areas or characteristics. The developed group—which includes the United States, the United Kingdom, the European Monetary Union, Canada, and Japan—has an average queue standing in its 72.5 percentile. The BRIC countries have a standing in their 21.6 percentile and the average for Asia is in its 64.7 percentile. While the BRIC countries are lagging, generally speaking they had been performing better during the past; as of July, China has a diffusion reading for its manufacturing sector at 49.2, Brazil at 47.5, Russia at 50.7, and India at 53.5. The BRICs generate a low percentile standing, but their July diffusion readings are more centrist than the rankings might seem to imply.

This report shows manufacturing engaged in some amount of recovery. However, there's still a lot of unevenness in the global economy, still a lot of work left to do, and still a lot of geopolitical risks in play.