- U.S. nonfarm payrolls unexpectedly fell 23,000 in July with meaningful downward revisions to both May and June.

- The market consensus looked for an 85,000 increase.

- The unemployment rate edged down to 4.1%, its lowest since June 2025, from 4.2%, due mostly to another significant decline in the labor force.

- Average hourly earnings edged up 0.1% m/m (3.2% y/y), meaningfully lower than expectations.

USA| Aug 07 2026

U.S. Payroll Employment Unexpectedly Declined in July

by:Sandy Batten

|in:Economy in Brief

More Commentaries

- New claims rose by 1,000 to 199,000 in the week of August 1.

- Continuing claims rose by 24,000 to 1.801 million in the week ending July 25.

- The insured unemployment rate was unchanged at 1.2% in the week of July 25.

USA| Aug 05 2026

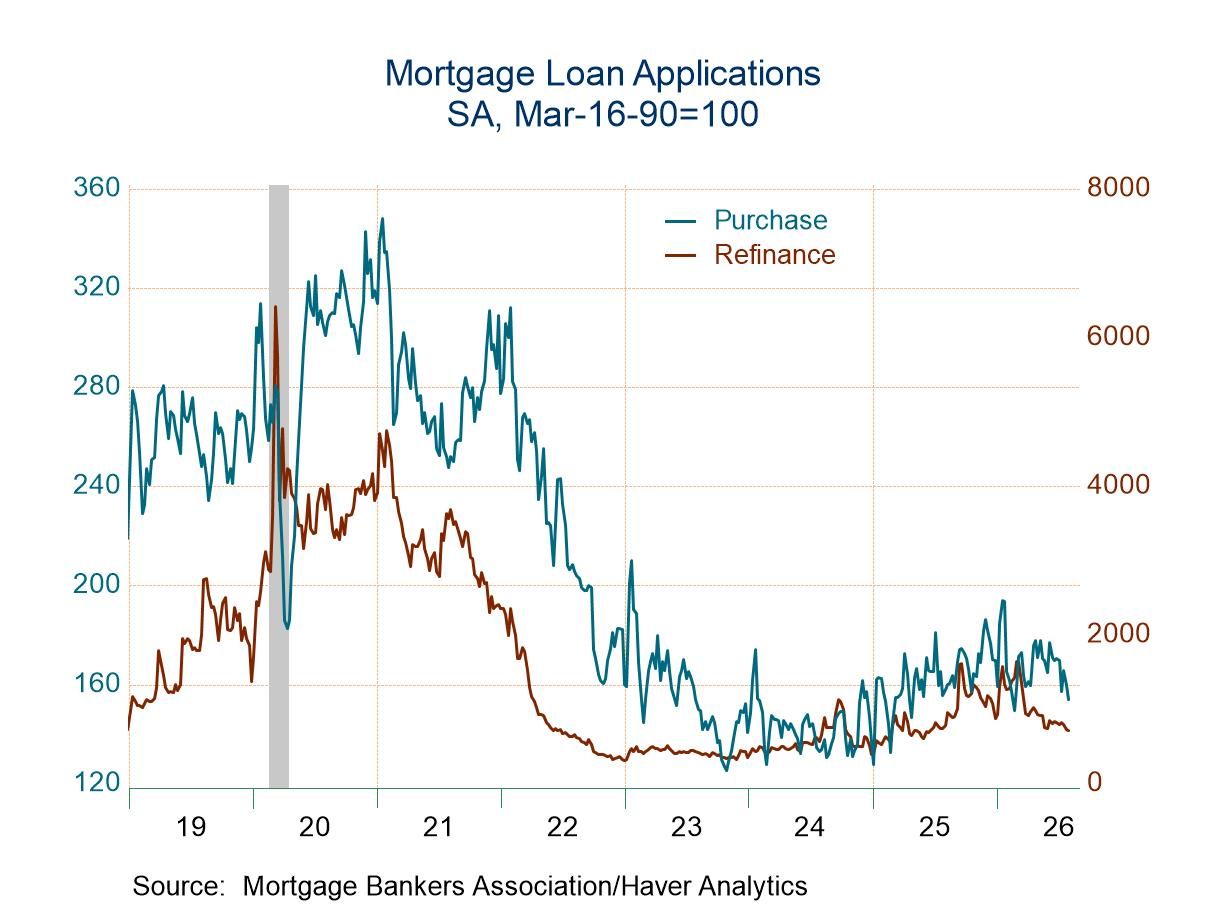

USA| Aug 05 2026U.S. Mortgage Applications Declined in the July 31 Week

- Both applications for loans to purchase and applications for loan refinancing declined in the latest week.

- Interest rate on 30-year fixed-rate loans rose 3bps to 6.99%, the highest since July 2025.

- Average loan size edged down.

USA| Aug 05 2026

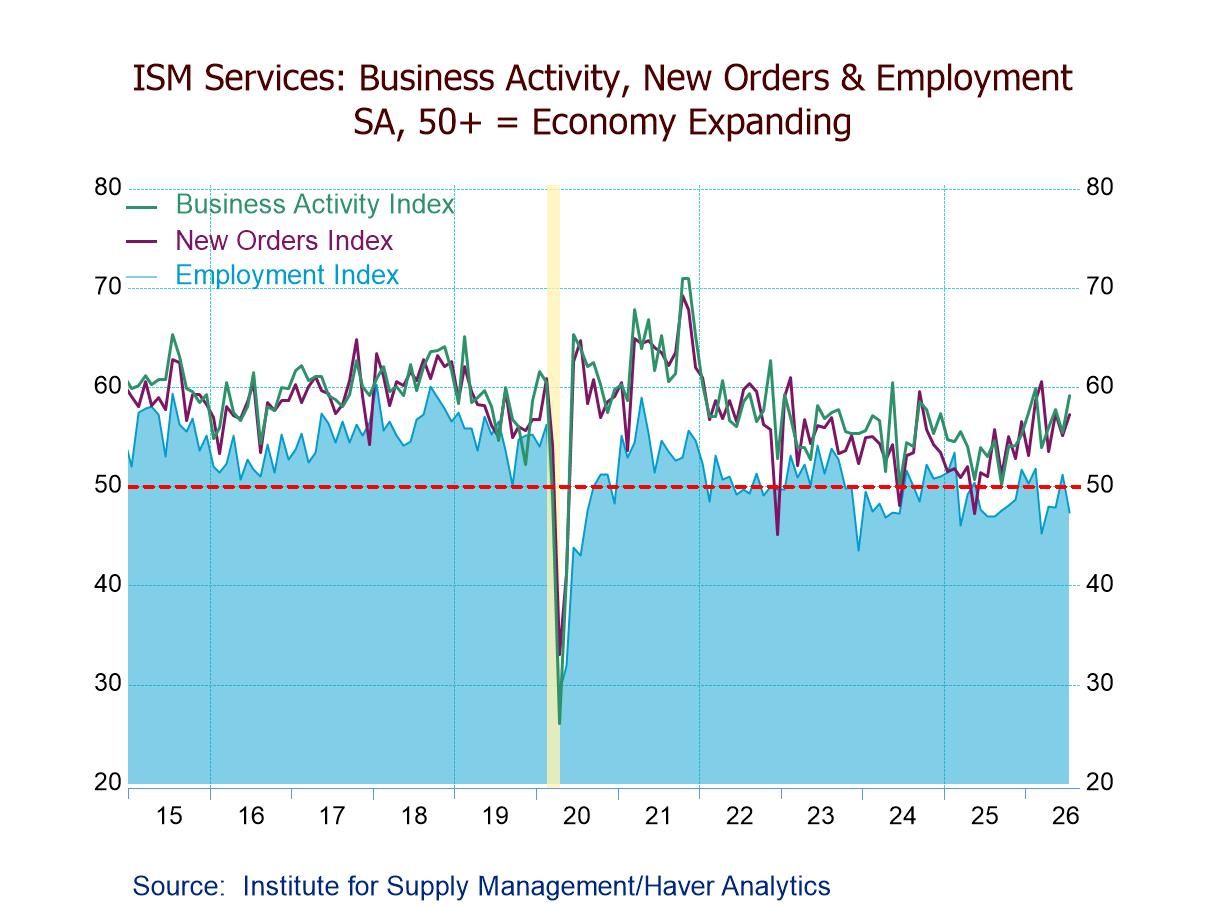

USA| Aug 05 2026U.S. ISM Services PMI Edges Up in July, Indicating Expansion for the 25th Straight Month

- ISM Services PMI slightly up to 54.1 in July, remaining above the 12-month avg. of 53.4.

- Business Activity (59.1) expands for the 25th consecutive mth.; New Orders (57.2) for the 14th straight mth.; Employment (47.4), at a four-month low, contracts in four of five mths.; Supplier Deliveries (52.8 vs. 54.4).

- Prices Index (70.3) elevated and above 70 for the fourth time in five mths., indicating prices rising since June ’17.

USA| Aug 05 2026

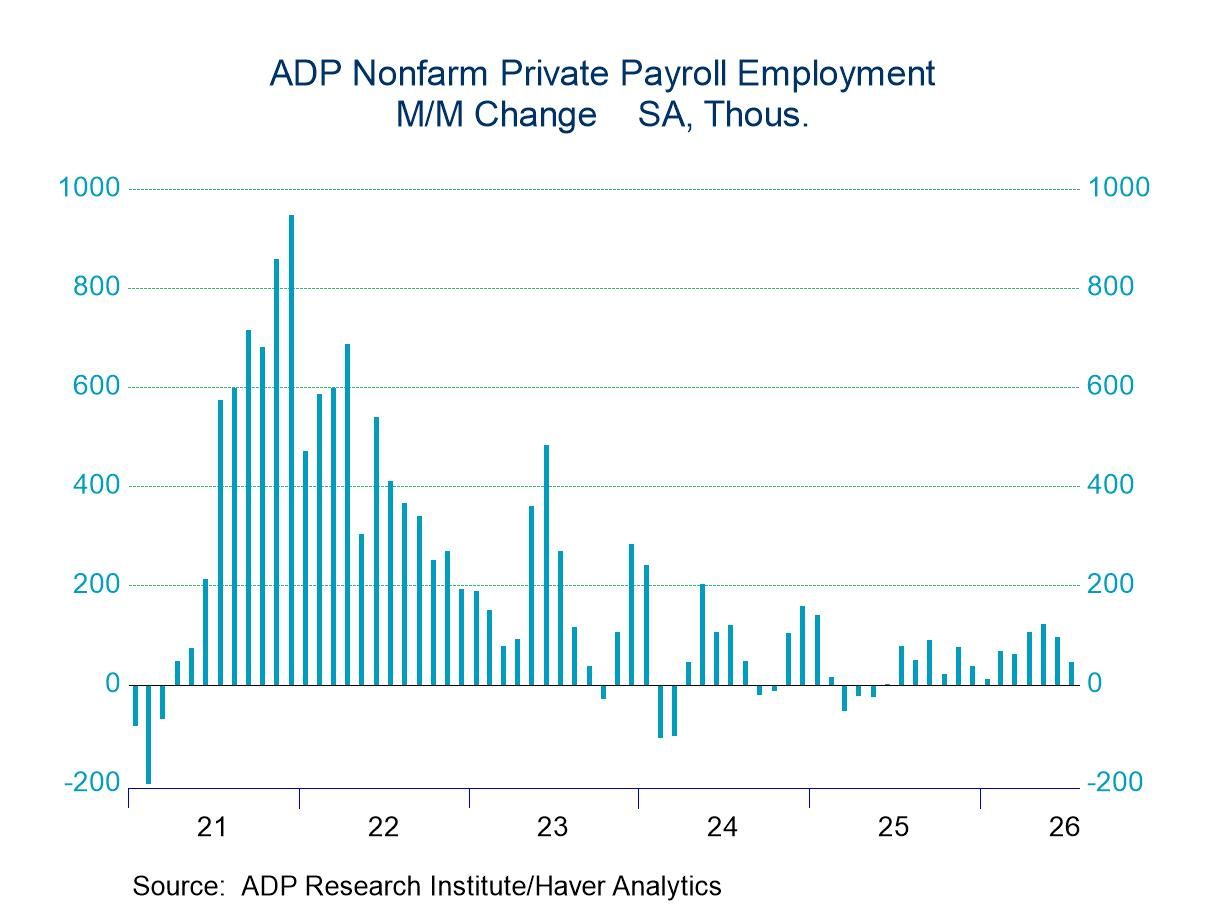

USA| Aug 05 2026U.S. ADP Employment Disappoints in July

- Private sector jobs rose only 44,000 in July versus 95,000 in June.

- Goods-producing jobs fell 3,000, the first monthly decline in seven months.

- Service-producing jobs rose 47,000, the smallest monthly increase in four months.

- Wage growth for job changers picked up for the second consecutive month.

by:Sandy Batten

|in:Economy in Brief

Global| Aug 05 2026

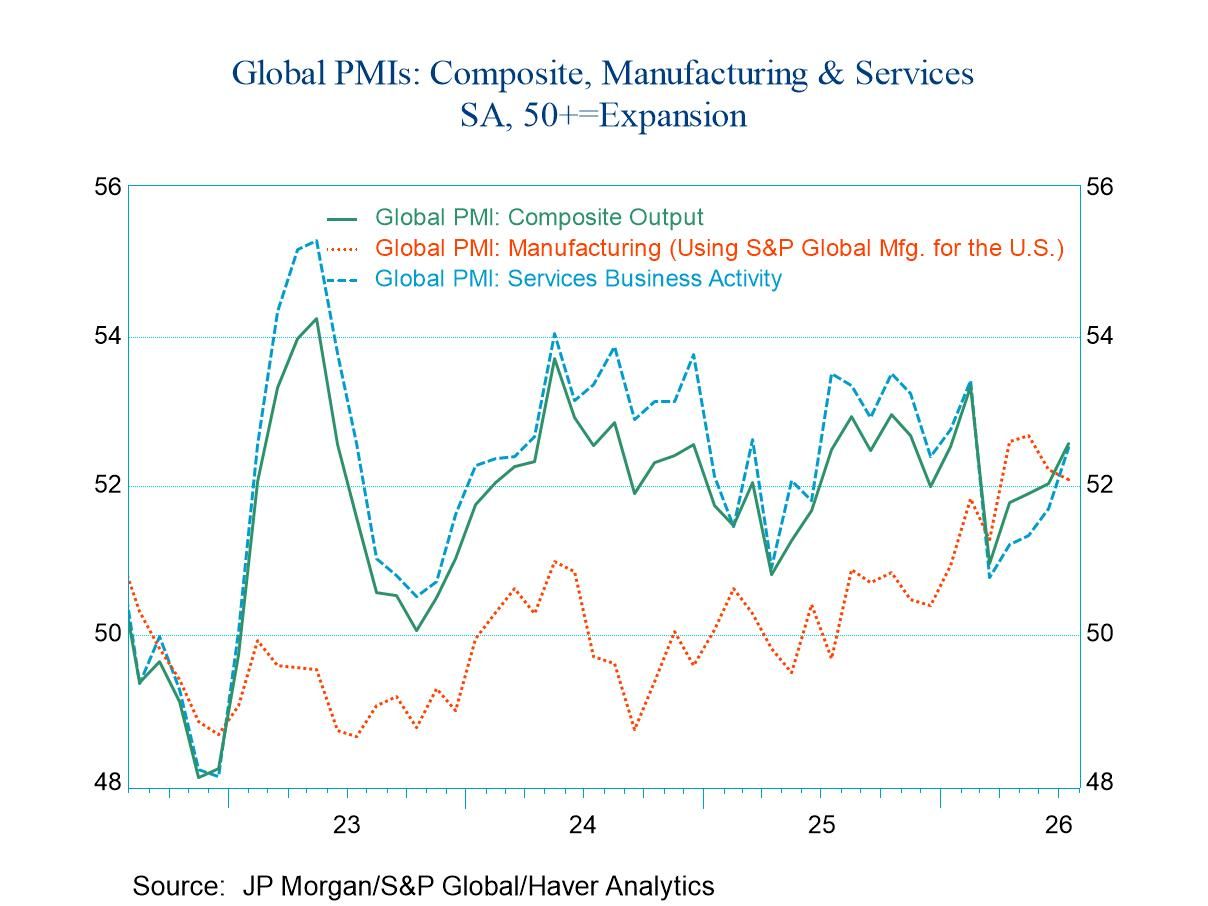

Global| Aug 05 2026Total PMIs Show Confused Trends

The total or composite PMIs in July released by S&P showed mixed performance although the average and median readings for the 25 reporters improved slightly month-to-month. The average reading rose to 52 in July from 51.3 in June, and the median reading rose to 52.2 from 50.8.

Contraction is mostly avoided, but not rare In July, seven of the reporters showed total PMI gauges below 50, indicating that those economies are contracting. The seven economies with that characteristic are France, Russia, Brazil, Zambia, Ghana, Egypt, and Qatar. For the most part, these are smaller economies. France, of course, is a large European economy; Russia is engaged in its ongoing war with Ukraine, which is taking a toll on its economy; and Brazil is one of the large BRIC economies.

The contracting count worsened, then stopped In June, nine countries had PMIs below 50, the same as in May. Over broader periods, such as three months, 10 countries show PMI values averaging below 50. That compares to seven over six months and six over 12 months. The slippage has actually progressed from 12 months to six months to three months, then improved on monthly data.

Contraction seems more structural than cyclical The shaded parts of the table correspond to PMI values below 50. We see that there's a long string of those readings in France, Russia, Egypt, and Qatar. For those countries, the one-month appearance of a below-50 reading in July was not episodic; it was structural. Germany has had two months in a row and a three-month average below 50; however, Germany turned stronger in July. The European Monetary Union as a whole had two months below 50 as well as very weak three-month and six-month averages, but it also turned higher in July. Zambia has a recent string of ongoing weakness; Ghana has a nearly unbroken streak of values below 50 as well. Brazil’s signal is like a flashing light.

There is good news However, the good news is that only eight of the reporting areas actually got weaker month-to-month in July, compared to nine in June and 11 in May. Over three months, we see 13 areas reporting PMIs that have weakened month-to-month. That compares to 21 that weakened over six months. On year-over-year comparisons, only 11 are weaker period-to-period. The weakening trend is much reduced in the recent monthly data.

Lingering weakness PMIs chronicle a great deal of lingering weakness, although for the most part conditions aren't worsening month-to-month over the past two months. However, there are a number of areas where activity, as designated by the PMI values, is declining. The sequential readings confirm that the growing weakness is a real factor and has only reversed in the last two months, if that result can be durable. How much of this weakness and subsequent rebound is linked to the war in Ukraine and the new deterioration and stalemate in the Middle East; those up-and-down dynamics are going to be hard to puzzle out.

Activity and performance assessments The queue percentile standings show that 12 of the 25 reporting entities have standings below their medians on data back to January 2021. That means nearly half are weaker in July than they have been on readings back to January 2021. On that timeline, conditions have not been strong, with an average diffusion (PMI) reading across the board of 52.3 and a median of 51.4. It has been a low-growth period in general.

The rich get richer? Even if only slowly... The large, developed economies, for the most part, have PMI rankings and queue standings above their 50th percentiles. The exception is the United Kingdom, with a 47.8 percentile standing. The exceptions also include the BRIC countries: Russia having a 26.9 percentile standing, India with an exceptionally low 9.0 percentile standing, Brazil with an 11.9 percentile standing, and China with a 22.4 percentile standing.

USA| Aug 04 2026

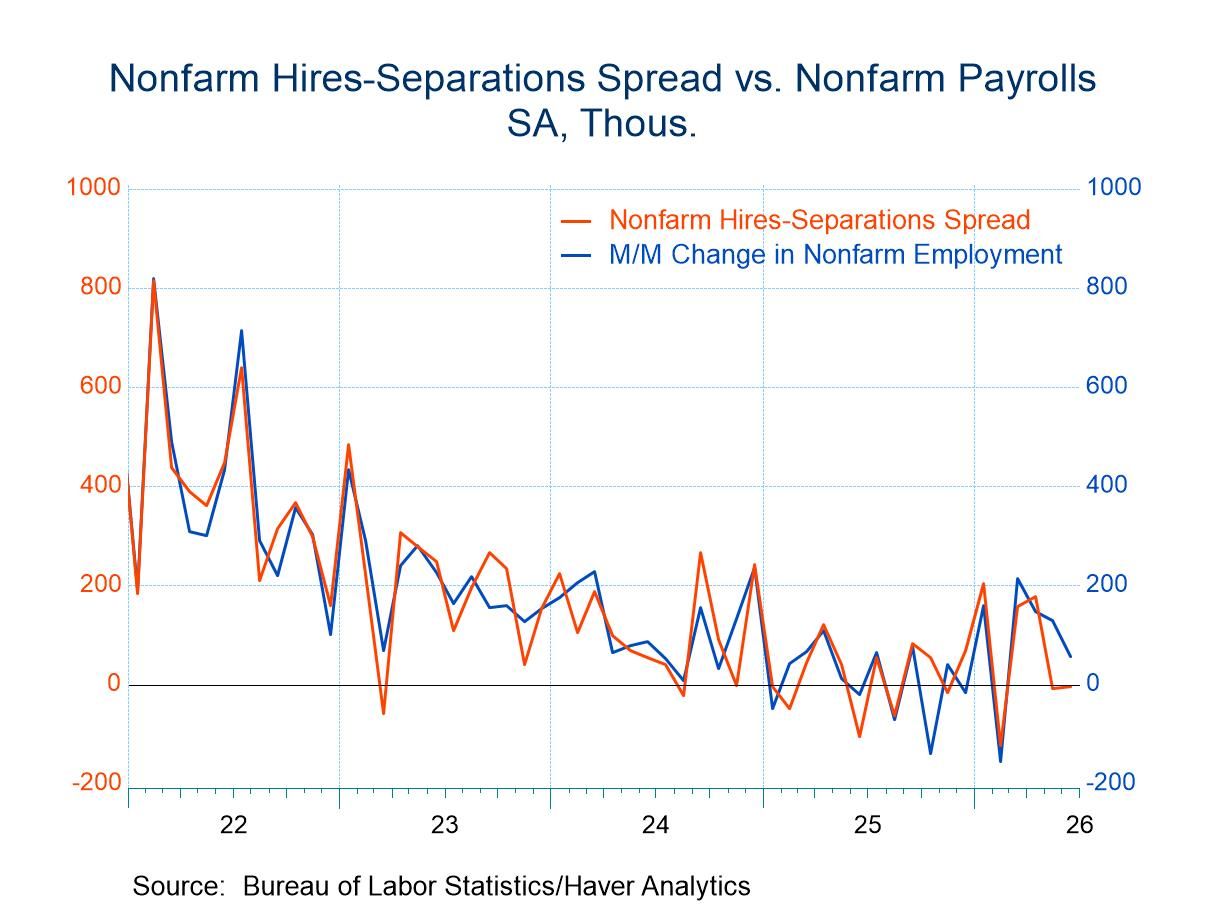

USA| Aug 04 2026U.S. JOLTS: Labor Demand Takes a Breather in June

- Sideways tracks reinforced for job openings and hires.

- Quits continue to signal wage disinflation.

- Hires-Separations point to May and June downward nonfarm payroll revisions.

USA| Aug 04 2026

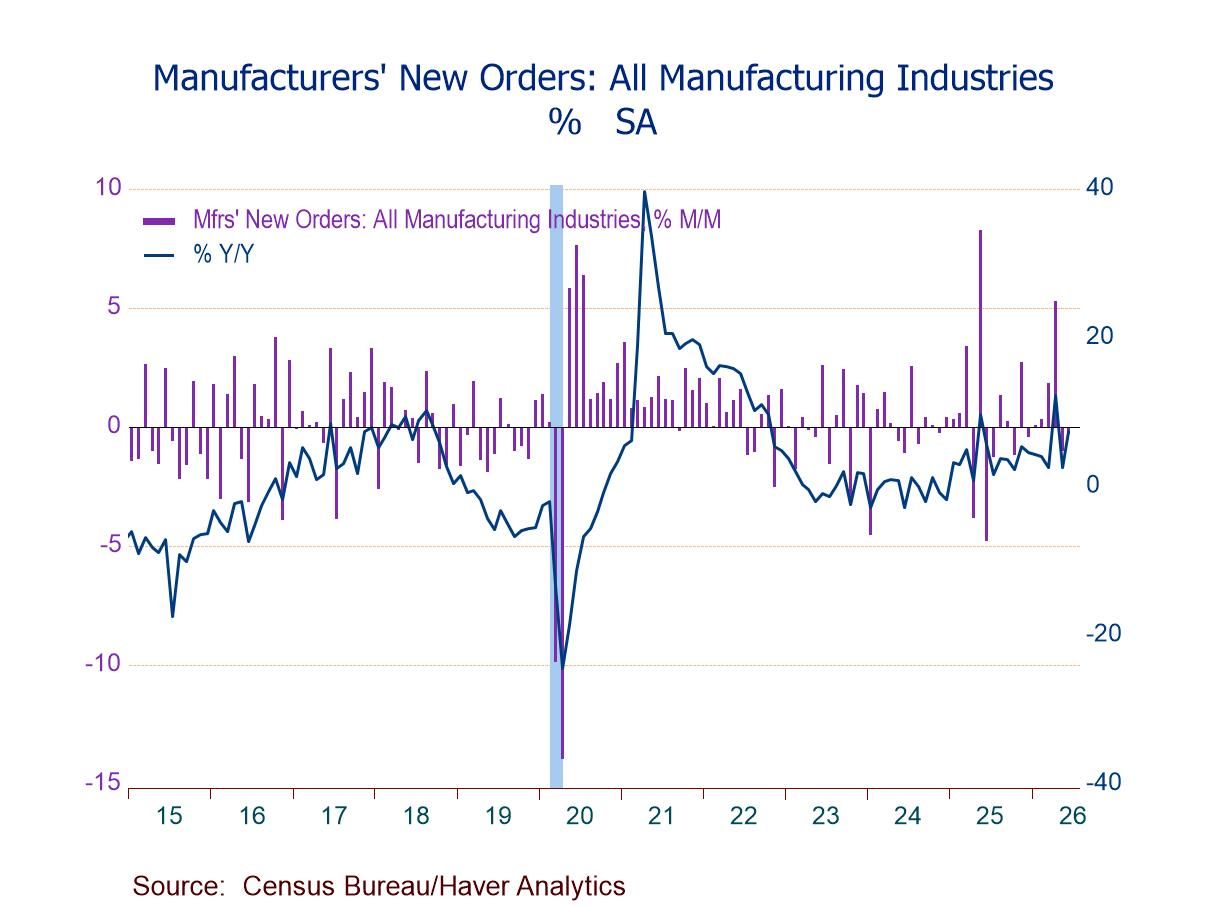

USA| Aug 04 2026U.S. Factory Orders Unexpectedly Decline in June

- Factory orders -0.3% (+7.4% y/y) in June, second straight m/m decrease; still 14.0% above the Jan. ’24 low.

- Durable goods orders +0.5%, third m/m gain in four mths.; nondurable goods orders -1.2% and shipments -0.2%, first m/m declines since Nov.

- Mining, oil field & gas field machinery -27.2%, steepest m/m drop since Apr. ’16.

- Transportation orders -0.1%, led by m/m falls of 7.2% in defense aircraft orders and 3.9% in ships & boats.

- Unfilled orders +0.6%, 11th straight m/m rise.

- Inventories +0.1%, eighth consecutive m/m increase.

USA| Aug 04 2026

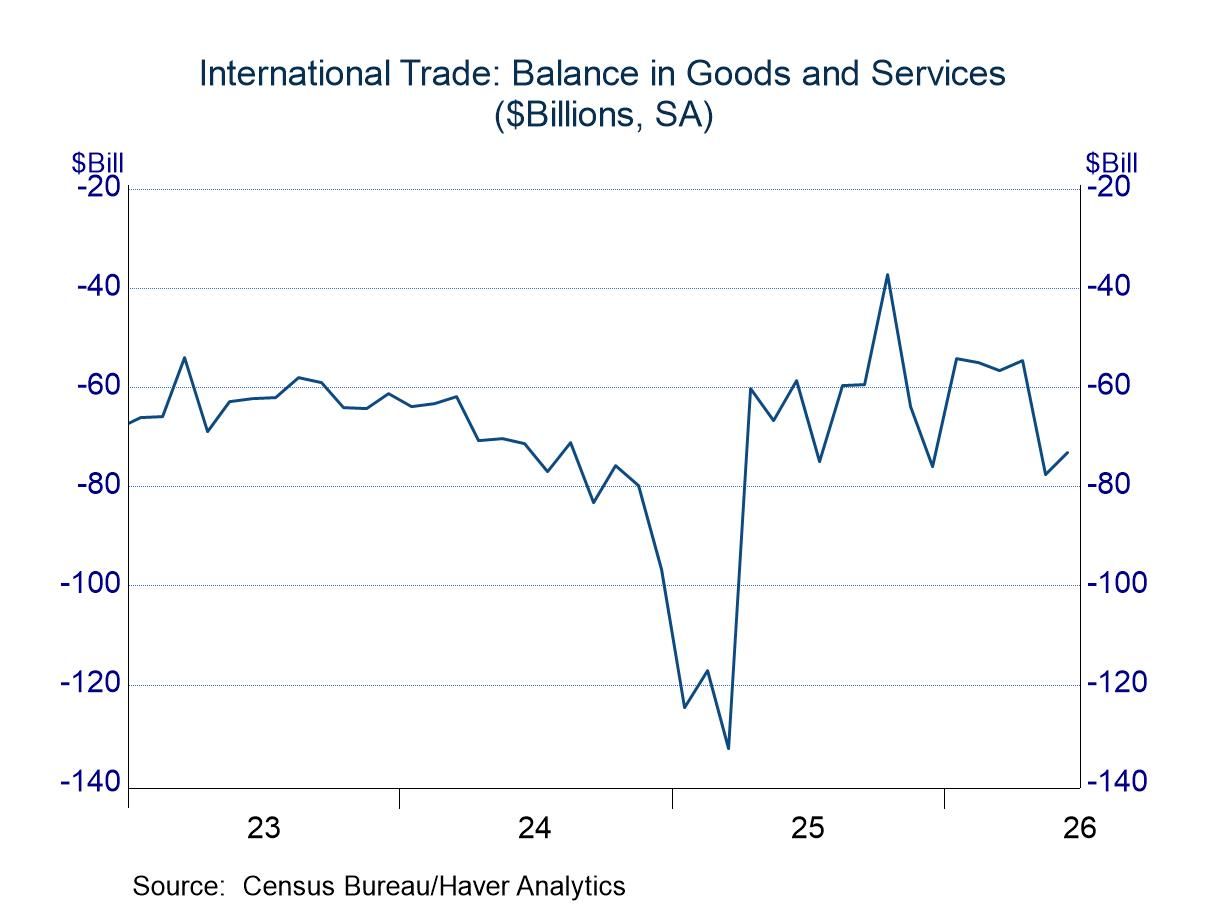

USA| Aug 04 2026US International Trade in June: Searching for Normal

- Both exports and imports cool after strong performances in early 2026.

- The US trade balance is moving sideways within a wide range.

- of2735Go to 1 page