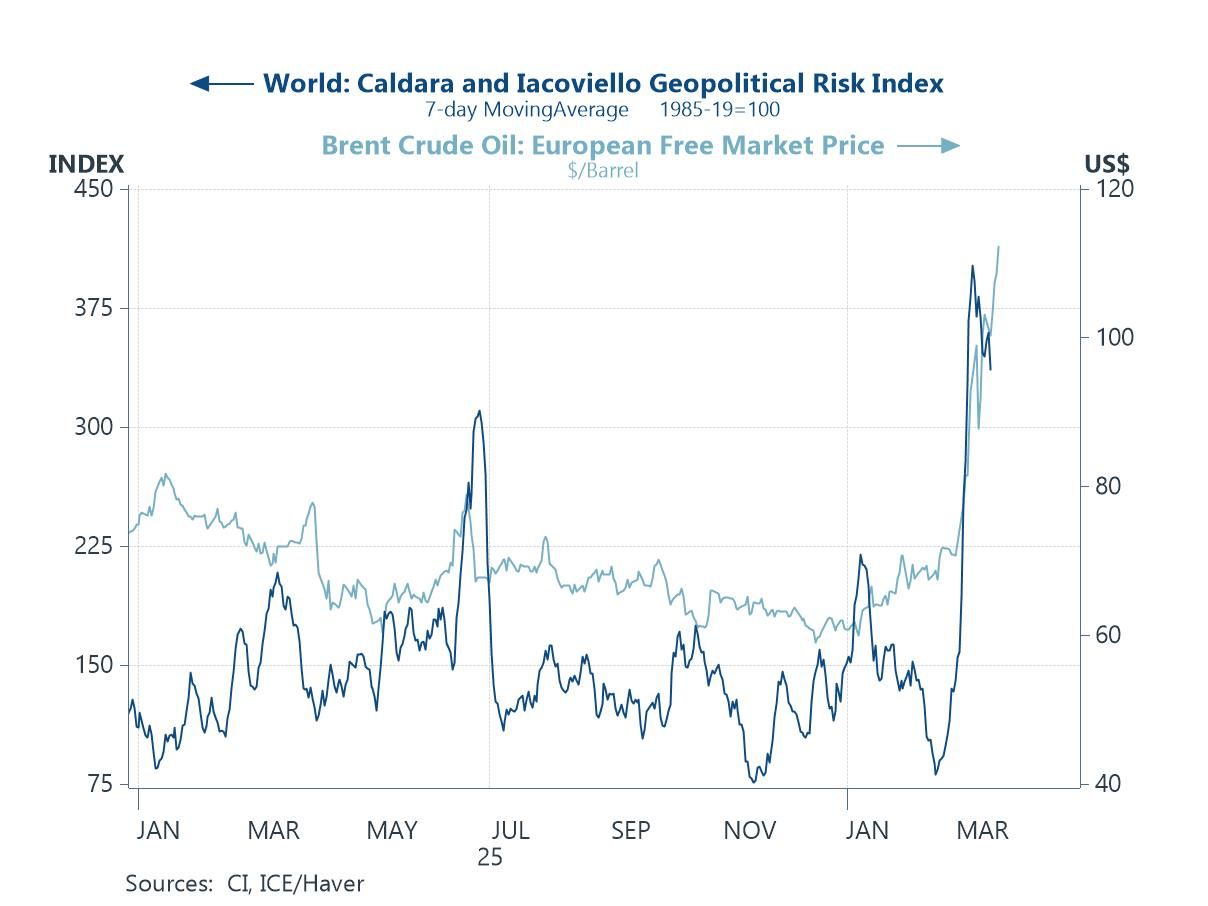

Recent de-escalation signals in the Middle East have offered some relief to markets, but the economic aftershocks from the earlier escalation are still feeding through—particularly via energy prices and heightened geopolitical risk. Crucially, these shocks are not hitting a clean cyclical backdrop. Instead, they are amplifying a set of pre-existing supply-side pressures—fragmented trade, strained supply chains, and a more complex policy environment—that have been building for some time. The charts this week pick up that theme. Forward-looking sentiment indicators suggest global growth has lost some momentum, even if activity remains in expansion territory (chart 1). At the same time, broader measures of uncertainty remain elevated (chart 2), while supply chain stress is once again moving higher, reinforcing the idea that disruption is becoming more structural (chart 3). Financial markets are reflecting this shift, with increased uncertainty around the future path of policy rates (chart 4), and survey evidence pointing to a more fundamental challenge around the credibility and transmission of monetary policy itself (chart 5). And yet, there are some offsets. Despite the recent spike in oil prices, medium-term inflation expectations—at least in the US—remain relatively well anchored (chart 6). Even so, the overall message is one of a more fragile, supply-driven cycle—where shocks like the Middle East do not just disrupt the outlook, but intensify the underlying constraints shaping the global economy.

Global| Mar 26 2026

Global| Mar 26 2026Charts of the Week: A Supply-Constrained World Comes into Sharper Focus

by:Andrew Cates

|in:Economy in Brief

More Commentaries

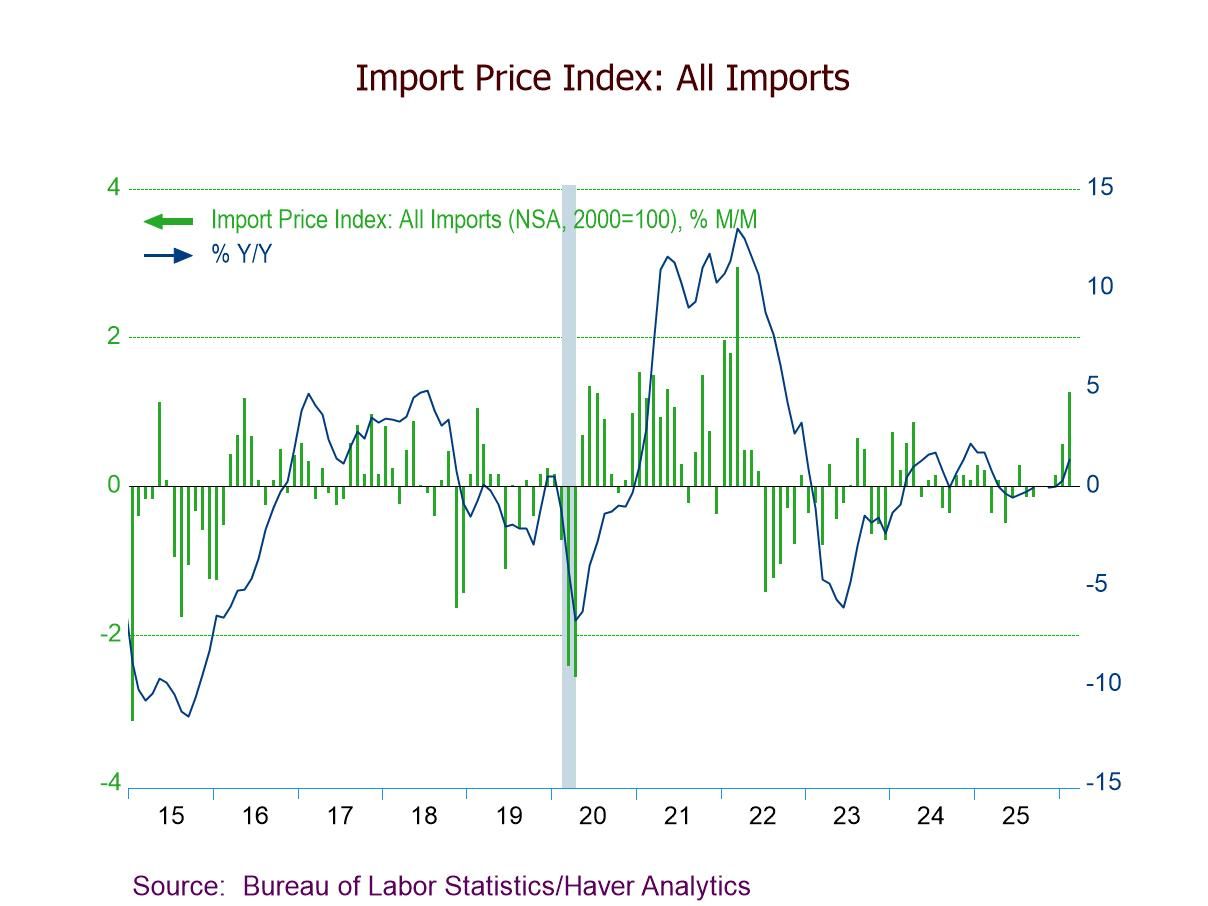

- Import prices +1.3% m/m (+1.3% y/y) in Feb., led by a 3.8% rebound in fuel import prices.

- Excluding fuels, import prices +1.1% m/m (+2.5% y/y) after a 0.8% Jan. increase.

- Export prices +1.5% m/m (+3.5% y/y), driven by a 1.7% gain in nonagricultural exp. prices.

USA| Mar 25 2026

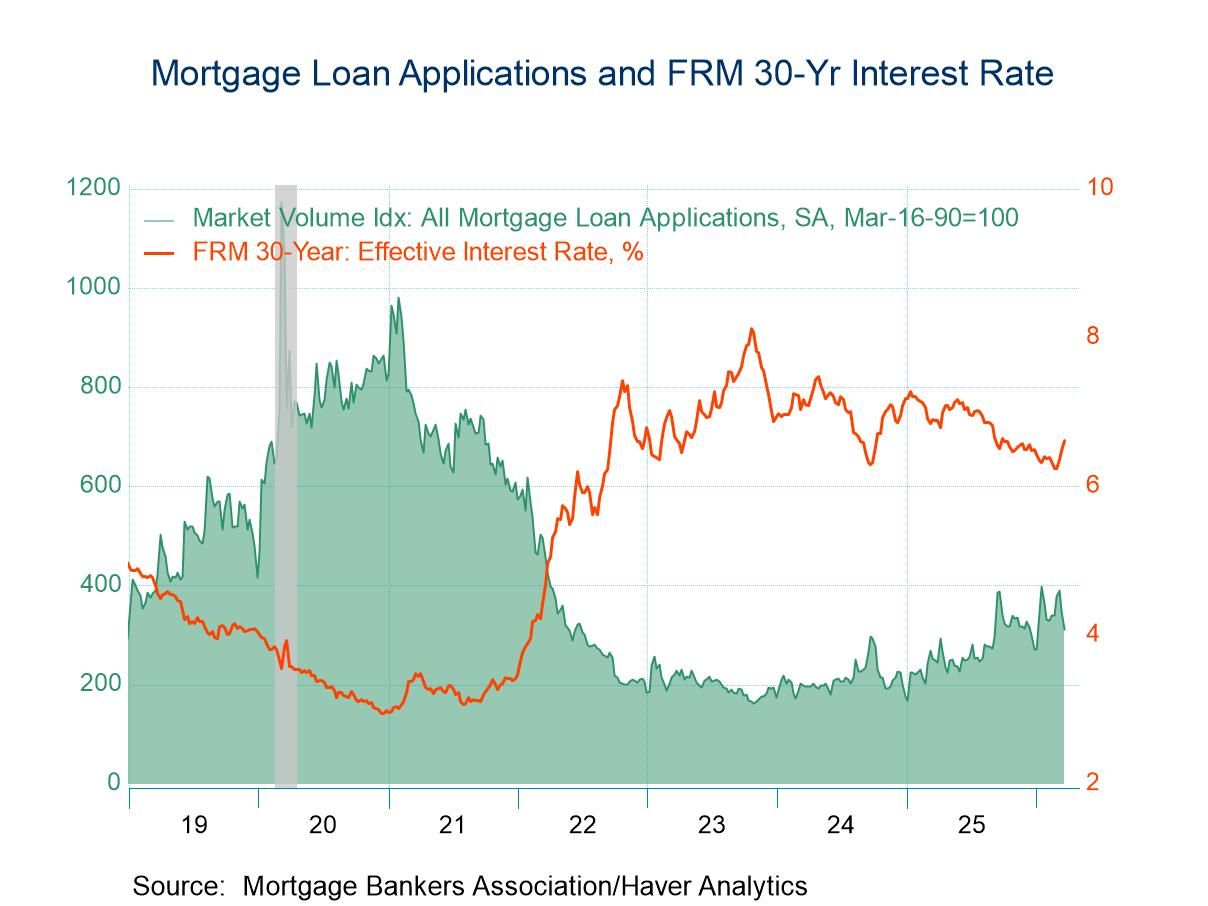

USA| Mar 25 2026U.S. Mortgage Applications Dropped in the March 20 Week

- Both applications for loans to purchase and for loan refinancing dropped in the latest week.

- Double-digit basis-point rises in all interest rates.

- Average loan size declined.

Germany| Mar 25 2026

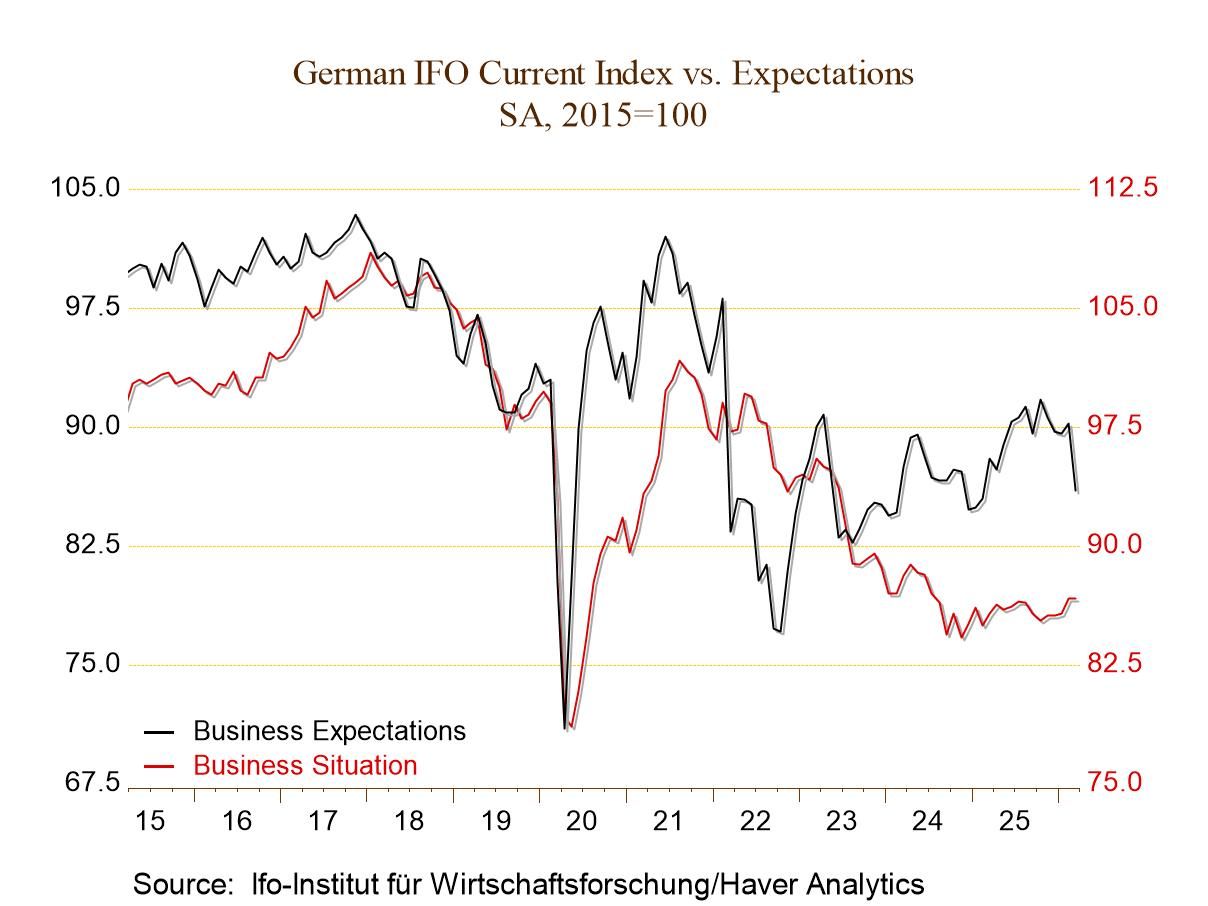

Germany| Mar 25 2026German IFO Sinks Even as the Current Reading Improves

The IFO readings for March 2026 show that the all-sector climate fell to -17.9 from -14.9 in February. The current conditions index improved by the smallest amount possible, rising to -2.4 after reaching -2.5 in February. Expectations, however, were clobbered, with the index in March falling to -19.7 after posting a -10.8 reading in February.

This expectations module for businesses in March registers a month-to-month drop of nearly 9 points; it ranks 246th out of 252 monthly changes, marking it as an occurrence that is this bad or worse, only 2.4% of the time (only 7 worse readings in the last 21 years). It's a stunning one-month backtrack in expectations for Germany.

Early reactions and developments We are currently in late March, so the reading reflects some reaction to the Iran war, and the reaction that we see certainly suggests that there is a relatively severe reaction by the business community to this war. Of course, the initial phase went extremely well from the standpoint of the United States and Israel, not from the standpoint of Iran. As the war has gone on, the U.S. and Israel have continued to register extremely successful military operations with very few of their own losses. However, it has also become clear that Iran intends to fight back on the ground and has tried to spread the conflict regionally using its missile capabilities—which appear to be more far-reaching than previously thought. We are left with the impression that Iran is prepared to engage in guerrilla warfare, which would be very difficult for conventional military operation to completely stamp out. The U.S. has resisted a call for boots on the ground although Donald Trump appears to be sending some paratroopers into the region. The U.S. has threatened to take control of Iran’s crown jewel of oil operations, Kharg Island. This threat has been made to counter Iran’s efforts to try to close the Strait of Hormuz, probably its only trump card. The U.S. has issued additional threats against Iran if it doesn't reopen the strait and allow oil traffic to pass again.

These conditions are, in many ways, a worst-case scenario for Europe and certainly a worst-case scenario for China and Japan that are so incredibly dependent on oil imports. Europe gets its oil imports substantially from the Middle East, meaning that those imports have to flow through the Strait of Hormuz. And then there's the embargoed Russian oil. There has been Iranian oil that has been on the market, having slipped through embargoes using clandestine tankers. U.S. actions in Venezuela have shut down the Venezuelan shipments that were substantially to China. All of these moves create a great impact, an impasse from oil scarcity, which has led to rising oil prices even though the U.S. has uncorked its strategic petroleum reserve and has promised to make more supplies available from that source. Unlike during 1973-75, the U.S. sits in the catbird seat.

The oil weapon has been broken out, and at the same time, turnabout has become fair play as the U.S. now has the upper hand on oil as Iran crimped the supply through the Strait of Hormuz. Strangely, much of Europe had said it would opt out of the U.S. plan to reopen the strait, but after a short period of time, 22 countries have now signed on to help unplug this strait.

Beyond oil (...sort of) The IFO survey shows expectations have dropped exceedingly hard in response to these events, with the expectation standings by industry ranging from a high of 16.1% in manufacturing to a low of 3.1% in retailing and 5.8% for services in general. The net diffusion readings for March range from a negative reading of -39.3 in retailing to a negative reading of -13.8 in manufacturing.

The current conditions rankings range from a high percentile standing in its 70.6 percentile for construction to a low standing in its 16.9 percentile for services.

And this is a report that has not given survey respondents a lot of time to see and react to events.

USA| Mar 24 2026

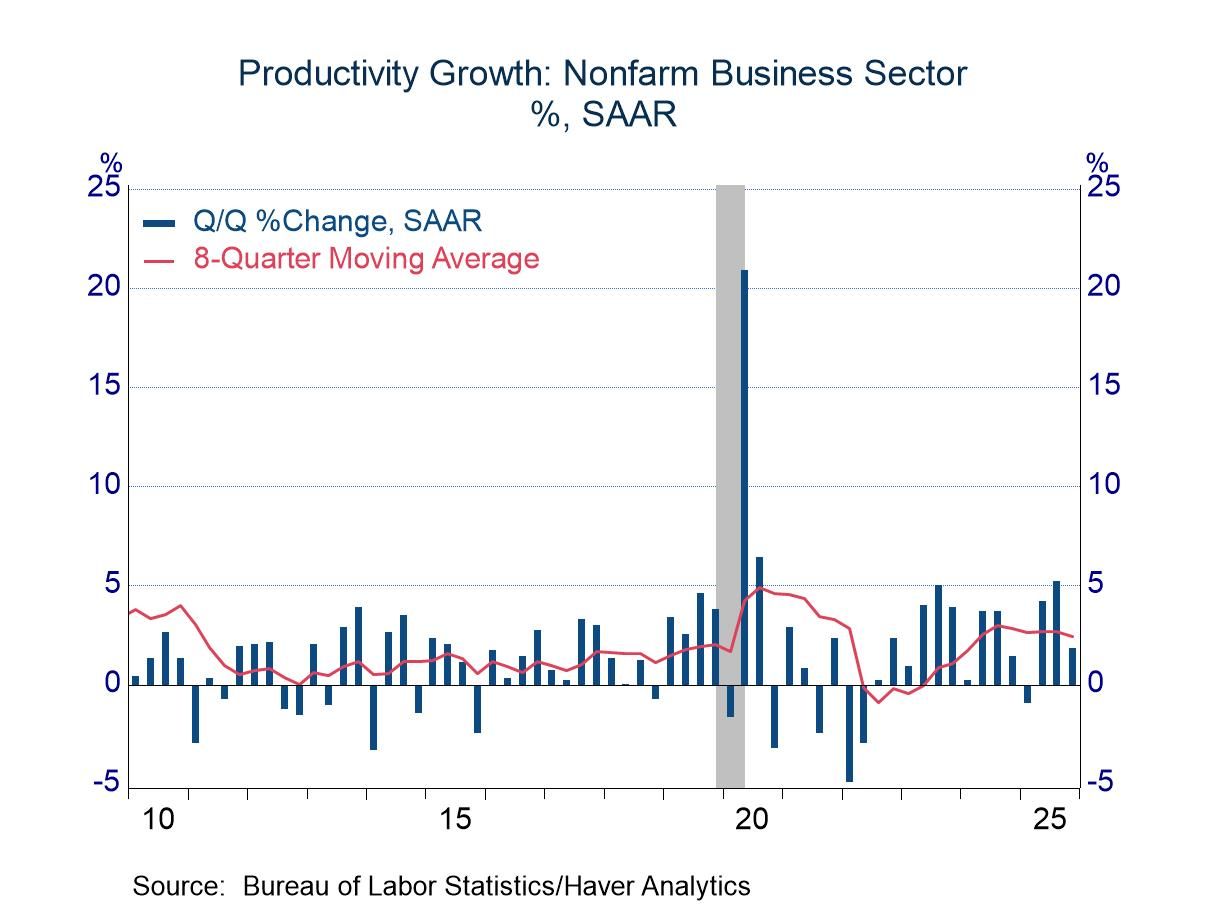

USA| Mar 24 2026Productivity Growth: Downward Revision in Q4

- Productivity growth was a percentage point slower than previously believed, but still respectable.

- A notable upward revision in unit labor cost is more concerning.

Global| Mar 24 2026

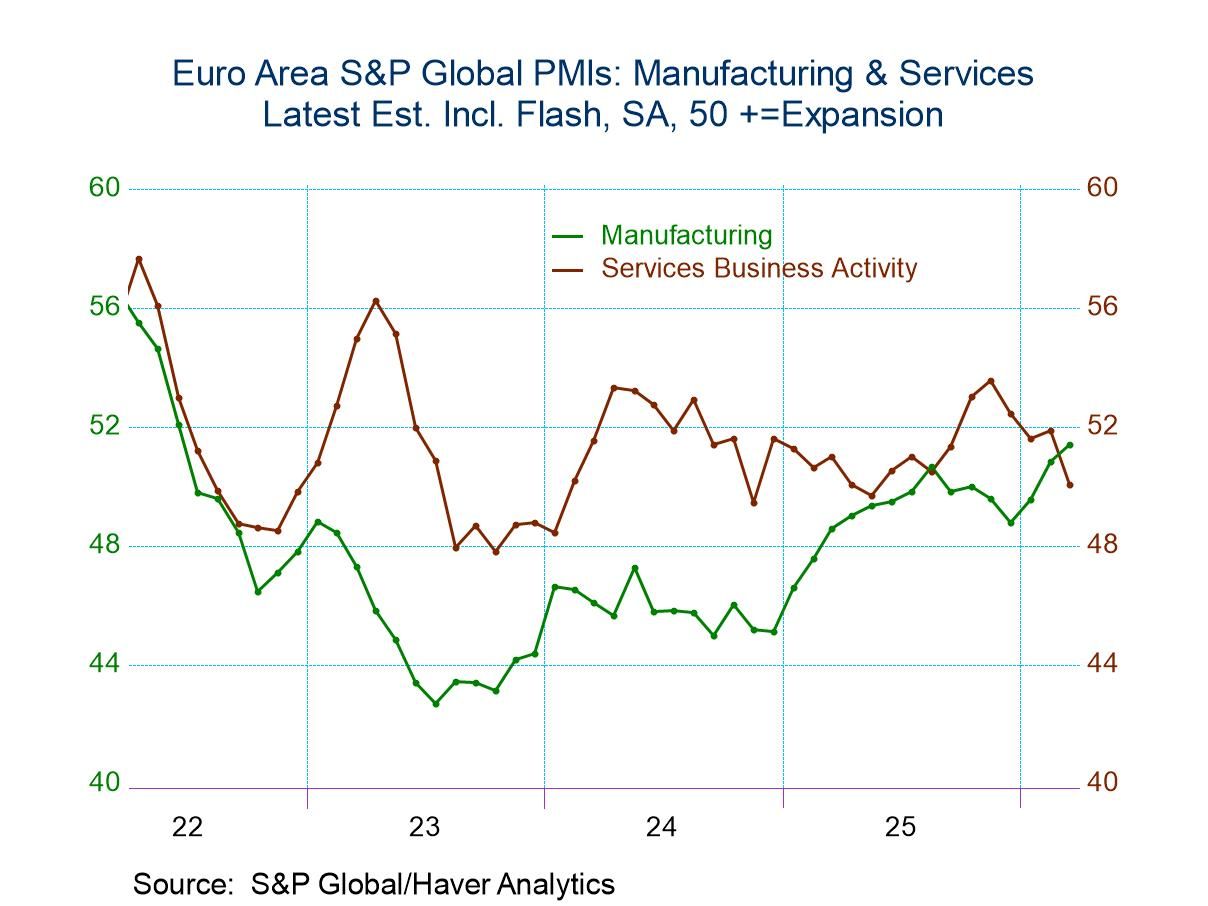

Global| Mar 24 2026S&P PMIs Show Weaker March; Iran War Disrupts Recovery Process

A Broad Weakening The Standard and Poor’s global PMI data show broad weakness in March compared to February. The early ‘flash’ report provides sector details for seven countries plus the consolidated European Monetary Union reading. For each reporting unit, there are readings for the composite, the manufacturing sector, and services. In March, there was a weakening on a month-to-month basis for every reporter in all sectors except manufacturing. The four manufacturing exceptions were the United States, France, Germany, and the monetary union as a whole. That means India, Australia, Japan, and the United Kingdom recorded weakening in their composite, manufacturing, and services readings in March. Meanwhile, the monetary union, Germany, France, and the U.S. that posted stronger readings in manufacturing were still dominated by weaker readings in services, causing their composites to weaken month-to-month without exception.

A Sudden Weakening These results compare to February when 13 of 24 reporters recorded stronger sector or composite readings month-to-month. In February, the monetary union and Germany reported stronger readings in all three measures—the composite, manufacturing, and services; Japan did the same. January had a much stronger month overall, with increases in most sectors across most reporting units with a few exceptions. France reported weaker services and a weaker composite, the monetary union reported weaker services and a weaker composite, and Germany reported only a weaker services sector. The remaining five reporters recorded stronger readings in all three sectors. The war in Iran has clearly interrupted what had appeared to be a strengthening, though still uneven, economic recovery.

Sequentially Different Patterns Sequential data (3-month, 6-month, and 12-month averages) do not include March since March data are still preliminary. Sequentially, the trends are mixed, with the monetary union and Germany showing weaker conditions over the three months compared to six months, but stronger conditions over six months compared to 12 months for all three sectors The United States also reports weaker conditions over three months compared to six months, and it reports weakening over six months compared to 12 months for services as well. As for manufacturing, although the U.S. services sector is weaker consistently including for 12 months compared to 12 months ago, the United Kingdom and France show strengthening in all three sectors over three months compared to six months and over six months compared to 12 months. Japan shows strengthening on that same basis, except that there's a weakening of services over three months compared to six months.

There is a mixed picture as far as trend is concerned and some areas have been stronger consistently, and others have progressed faster than others. But March has brought weakness across the board.

The Percentile Averages: The queue standings (or rank standings) show and average percentile standing for the composites (unweighted) at 41.7% over all data since January 2022. Manufacturing currently is relatively strong on this comparison with a 66.9 percentile standing. Services are weak with a 30.4 percentile standing.

The Diffusion Average: Based on data since January 2022, the average composite reading for this set of reporters is 51.9. The manufacturing average is 50.0, and the services average is 52.4. So, all rankings are relative to that set of data. Since 2022, France has had the lowest diffusion reading, with a composite average at 49.2—it has been consistently shrinking.

Manufacturing: Manufacturing has been weakest in German, with an average PMI reading of 46.6. However, France, the United Kingdom, Japan, and the EMU also have average manufacturing sector readings below 50, indicating ongoing manufacturing contraction.

Services and Comparisons: Only France has averaged a service sector contraction since January 2022. Over this period, India has had the strongest diffusion readings across all sectors. The U.S. has logged the second-strongest PMI readings in services, manufacturing, and the composite.

The U.S. as a benchmark and sticky conditions: For the U.S., the average has been 52.2 for the composite, 51.0 for manufacturing, and 52.4 for services. Since these are the second-strongest set of readings, it makes clear that the readings for this period have been quite tepid. Whatever recovery was in progress was probably slow and fairly fragile. Central banks had largely brought inflation down and, in some sense, ‘under control,’ but still, not to target. These sticky realities have been dogging policy-makers. It has been a difficult period. Of course, the Russia-Ukraine war dragged on, Hamas attacked Isreal, Iran’s nuclear facilities were destroyed, the Trump tariffs remained in place, and a second attack on Iran—intended to undermine its surviving nuclear ambitions—was launched with a goal to degrade its huge cache of missiles and drones as well.

USA| Mar 23 2026

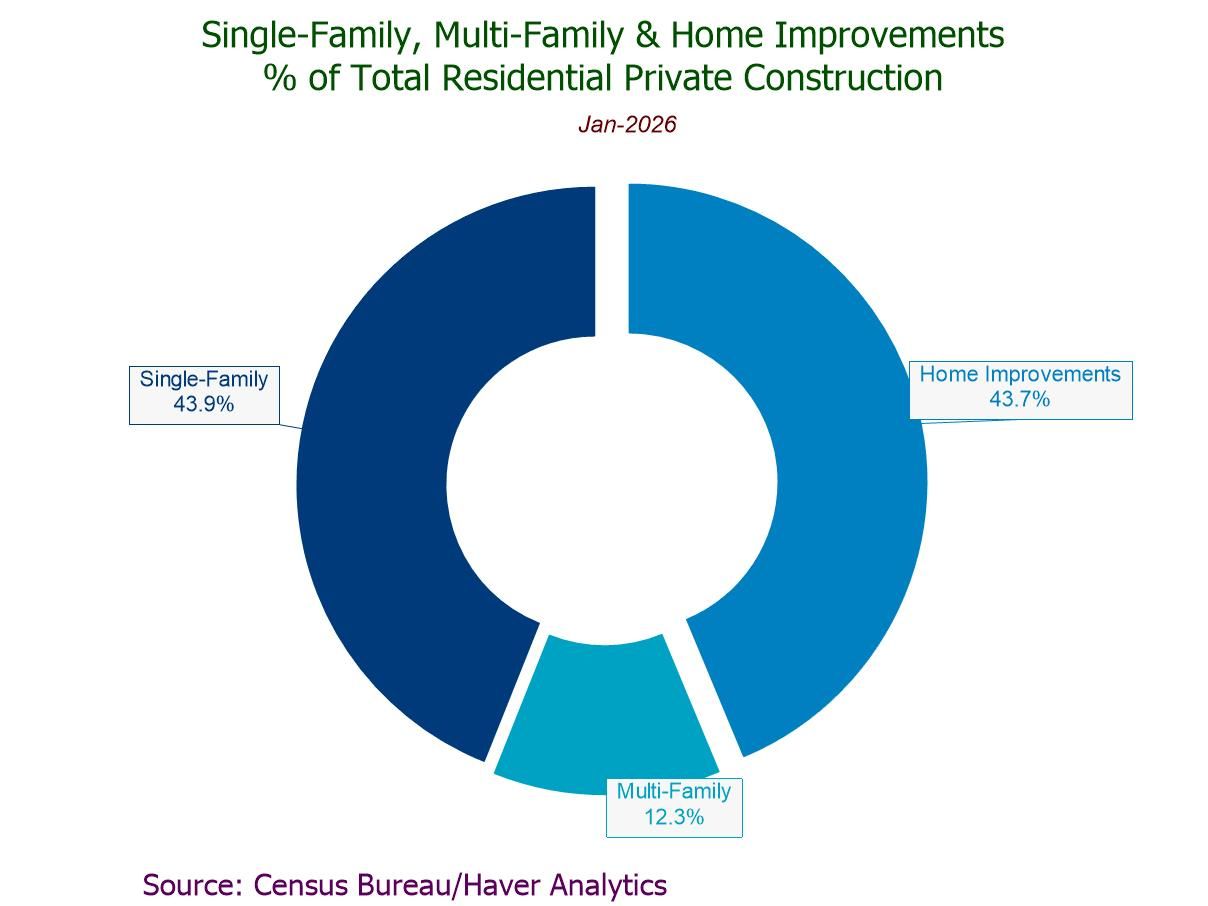

USA| Mar 23 2026U.S. Construction Spending Unexpectedly Declines in January

- Headline -0.3% m/m, first monthly decrease in three mths.; +1.0% y/y for the second straight mth.

- Residential private construction -0.8% m/m, led by a 1.4% drop in home improvement building.

- Nonresidential private construction -0.4% m/m, sixth fall in seven months.

- Public construction +0.6% m/m, driven by a 0.6% rebound in nonresidential public building.

Belgium| Mar 23 2026

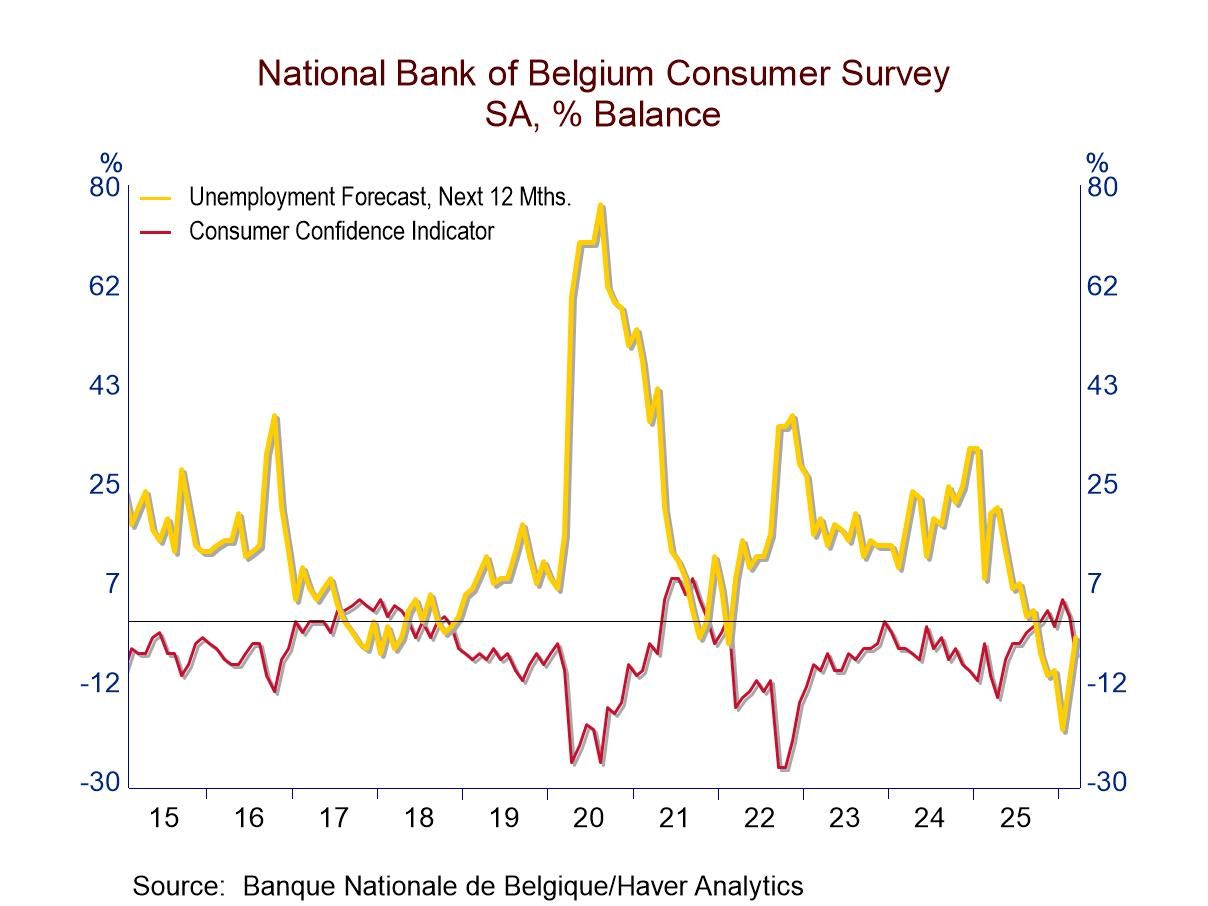

Belgium| Mar 23 2026Belgian Consumer on the Edge?

The Belgian consumer may be on the edge of a sudden deterioration based on responses to the National Bank of Belgium Consumer Survey for March. The consumer confidence reading registered at -6 in March compared to +1 in February. And on data back to 1991, this gives the consumer confidence metric a ranking in its 53rd percentile, slightly above the median for this span. For ranked data, the median occurs at the 50th percentile.

However, the response by consumers to the current situation appraisal gives them an extremely high 94.9 percentile ranking which suggests that the Belgian consumer is quite happy; however, the financial situation for households as appraised over the next 12 months has a reading of -3 in March, with a queue percentile standing at a 23.9 percentile mark in the lower quartile of its ranked responses since 1991. It's clearly a very difficult situation to be extremely happy with the current situation but to be concerned about your financial situation over the next 12 months.

Households rate the next 12 months as relatively inhospitable to make major household purchases as well. The reading at -17 in March is just a tick higher than -18 in February and has a rank standing in its 39.5 percentile. Despite the upbeat ranking of the current situation, households do not rank the current situation as a good time to buy as the favorability to purchase goods at present has a ranking in its 13.8 percentile. Clearly, the Belgian consumer is facing cross-currents and a deteriorating trend.

Among those cross-currents, however, is not a great concern about unemployment. The unemployment reading did rise month-to-month to -3 in March from -11 in February and from -20 in January. Concerns about unemployment have been rising; however, they still have a very low 5.5 percentile standing.

One of the concerns percolating in the background is about inflation. Price trends over the last 12 months had eased to some extent, to 66.2 percentile standing. However, over the next 12 months the reading has picked up to 53 from 31 previously, to a 99.5 percentile standing; concerns about inflation have turned around and now are extremely high.

Consumers rate the economic situation at a -45 in March compared to -25 in February looking ahead to the next 12 months. The queue standing for this reading is in its 0.7 percentile, one of the lowest ratings that we have seen since 1991. The assessment for the previous 12 months has a raw diffusion net score of -42, with the standing in its 23rd percentile. Conditions have deteriorated extremely rapidly in terms of the outlook for the economic situation.

Asia| Mar 23 2026

Asia| Mar 23 2026Economic Letter from Asia: A Crude Awakening

In this week’s Letter, we take stock of the ongoing Iran conflict, review key developments across Asia, and assess consumer sentiment in the region. The conflict continues to weigh on markets, with oil prices remaining elevated (chart 1). At the same time, global pressure is building against the continued disruption of flows through the Strait of Hormuz, though concrete actions to restore shipments remain uncertain.

Amid this backdrop, several Asian central banks delivered policy decisions last week (chart 2), with the Middle East conflict explicitly cited as a key consideration. In effect, higher oil prices have either reinforced existing tightening biases or reduced the likelihood of rate cuts, reflecting mounting inflation concerns. On the domestic front, Thailand stood out, where Prime Minister Anutin’s decisive parliamentary re-election has eased lingering political uncertainty. Attention now shifts to how the new government will address longstanding challenges, particularly elevated debt levels (chart 3), alongside broader economic reforms. Looking ahead, the regional calendar remains active. Beyond flash PMI releases, focus will turn to Japan’s latest inflation print (chart 4) and China’s industrial profit data.

Turning to the Asian consumer, sentiment in China and Japan has improved in recent months (chart 5), supported in part by government policy and expectations of further consumer-focused measures. However, the Iran conflict poses downside risks, particularly through higher energy prices. Elsewhere in Asia, consumer confidence has stabilised (chart 6), though it remains exposed to similar risks, with the ongoing conflict threatening to weigh on sentiment across the region.

Iran conflict and energy prices The Iran conflict continues to rage, with shipping through the critical Strait of Hormuz still heavily constrained. This has kept a tight lid on crude supply, leaving oil prices significantly elevated (chart 1) relative to recent history. The resulting supply drag and price surge are adding upward pressure on inflation and, potentially, weighing on growth—particularly for oil-importing economies across Asia. That said, momentum is building on the diplomatic front. More than 20 countries have now backed a joint statement calling for safe navigation through the strait. Still, it remains unclear how this will translate into concrete actions, or—crucially from an economic perspective—how quickly it might restore disrupted oil flows.

- of2705Go to 1 page