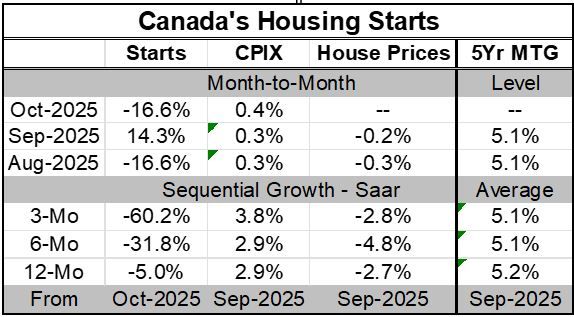

Canadian Housing Starts Show Erosion

Canadian growth has been in its own trajectory with some solid consumer spending in gear and some slight slowing in GDP growth. Housing has begun to show some wear and tear in this environment even as mortgage rates have remained well off peak and have begun to stabilize around the 5% mark for 5-year mortgage financing.

Canada has been cutting its policy target rate faster than the Fed has been reducing the Fed funds rate. Canada’s unemployment rate has hovered above the rate for the US and it has been rising; rising - not quickly - but with a bit more purpose than in the US. This may have encouraged the Bank of Canada to cut rates more aggressively with inflation fluctuating is the desired range set by the back of Canada.

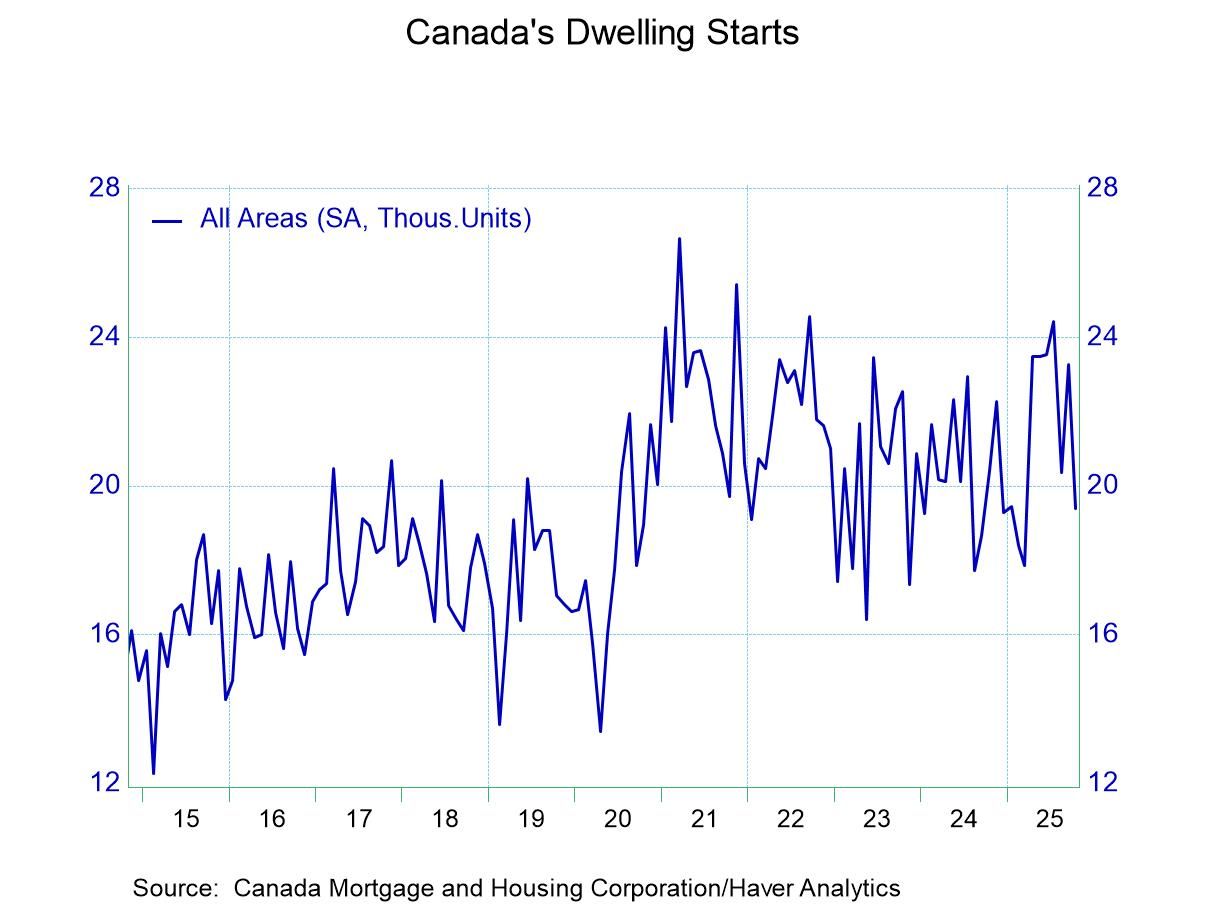

Canadian housing starts show the ‘signature slowing’ during Covid and the strong post-Covid recovery that actually has boosts starts well above the average it had maintained for the five-year previous to Covid. Even not with new episode of weakness in train Housing starts are above the pre-Covid average in Canada- and facing higher financing rates than before.

Canada, like the US, is going through some difficult fiscal times. In addition, there is an ongoing Trump-Carney spat that is a heavy overlay on the bilateral relations so important to both economies. Canadian PM Mark Carney just survived a confidence vote over his budget. The Carney budget aims to pump funds into the Canadian provinces to boost infrastructure and house-building. In Canada builders also face development fees that some want altered but the offer of reducing them has not been put on the table. Not surprisingly Canada is under some of the same pressure as the US for the government to act and supply answers for the housing shortage that has emerged. Carney’s platform on which he was elected had made some substantial promises and they still are not coming to fruition.

Covid seems to have upset a number of apple carts many of them related to housing. Prior to Covid housing demand had not been so vigorous. But Covid may have triggered something that reminded people how important housing can be especially in a crisis when you become house-bound. In the wake of Covid US and Canadian housing demand strengthened. And since the bank of Canada made the same policy mistake as the Fed driving interest rates to the brink of the zero bound during Covid it also created a period of super low mortgage rates which now has the effect of trapping people in their own homes- a form of "golden-handcuffs" that keep people in a house because of cheap financing. While mortgage rates are nearly 150bp below their post Covid peaks, they are still more than 100bps above their pre-Covid averages. The housing market remains under duress.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global