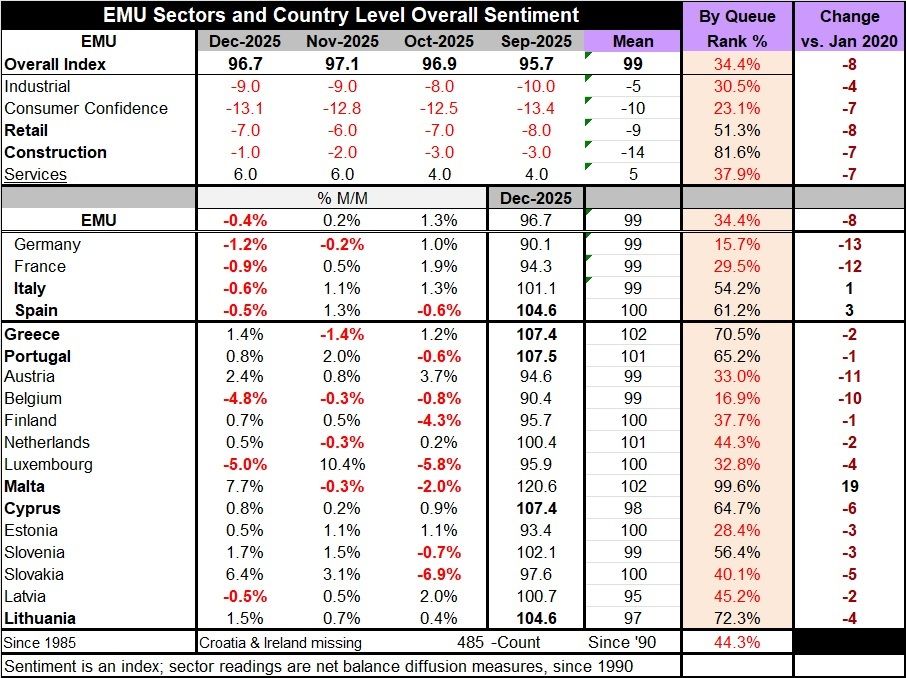

EU Indexes for EMU Weaken at Year-End

The EU indexes for December 2025 showed slight slippage as the overall index fell to 96.7 from 97.1 in November for the whole of the European Monetary Union. Sectors showed slippage in consumer confidence and retailing; confidence slipped to -13.1 in December from -12.8 in November as the retail rating slipped to -7 in December from -6 in November. The services sector and the industrial sector were each unchanged on the month, with the industrial reading at a net standing of -9 and the services reading at +6. Improving month-to-month was construction where the index rose to a -1 in December from -2 in November.

Queue standings of sectors The queue (or rank) standings for the overall reading as well as the sector readings largely cluster around the lower one-third of the range of values on data back to 1985, where applicable. Retailing and construction are exceptions, with retailing at an above-median standing at a 51.3 percentile and construction at a solid and strong 81.6 percentile standing in December. The weakest reading is for consumer confidence at the 23.1 percentile standing followed by the industrial sector at a 30.5 percentile standing; services check in at a 37.9 percentile standing. The rank standing for the overall monetary union is at 34.4%, just slightly above the bottom one-third mark for all ranked observations over the period.

Country results 18 countries report detail in this survey. Seven of the 18 showed declines in December; this is up substantially from November when five showed declines and compares to October when eight countries showed declines. An unfortunate feature of December is that the headline reading for the monetary union weakens as well as readings for each of the four largest monetary union economies Germany, France, Italy, and Spain.

The two largest monetary union economies, Germany and France, have the weakest rank standings among the BIG4 with Germany at a 15.7 percentile standing and France at a 29.5 percentile standing. Italy and Spain each have standings above the 50% mark placing them above their medians for Italy with a reading of 54.2 percentile, while for Spain it's a 61.2 percentile standing.

Standings across smaller economics Across the remaining monetary union countries, six of the 14 readings are above their 50th percentile, while eight of the 14 are below their 50th percentile. Well, the large countries are experiencing a significant split; the rest of the monetary union appears to be in much the same condition, with approximately half of them performing at above-median conditions and half performing at below-median conditions.

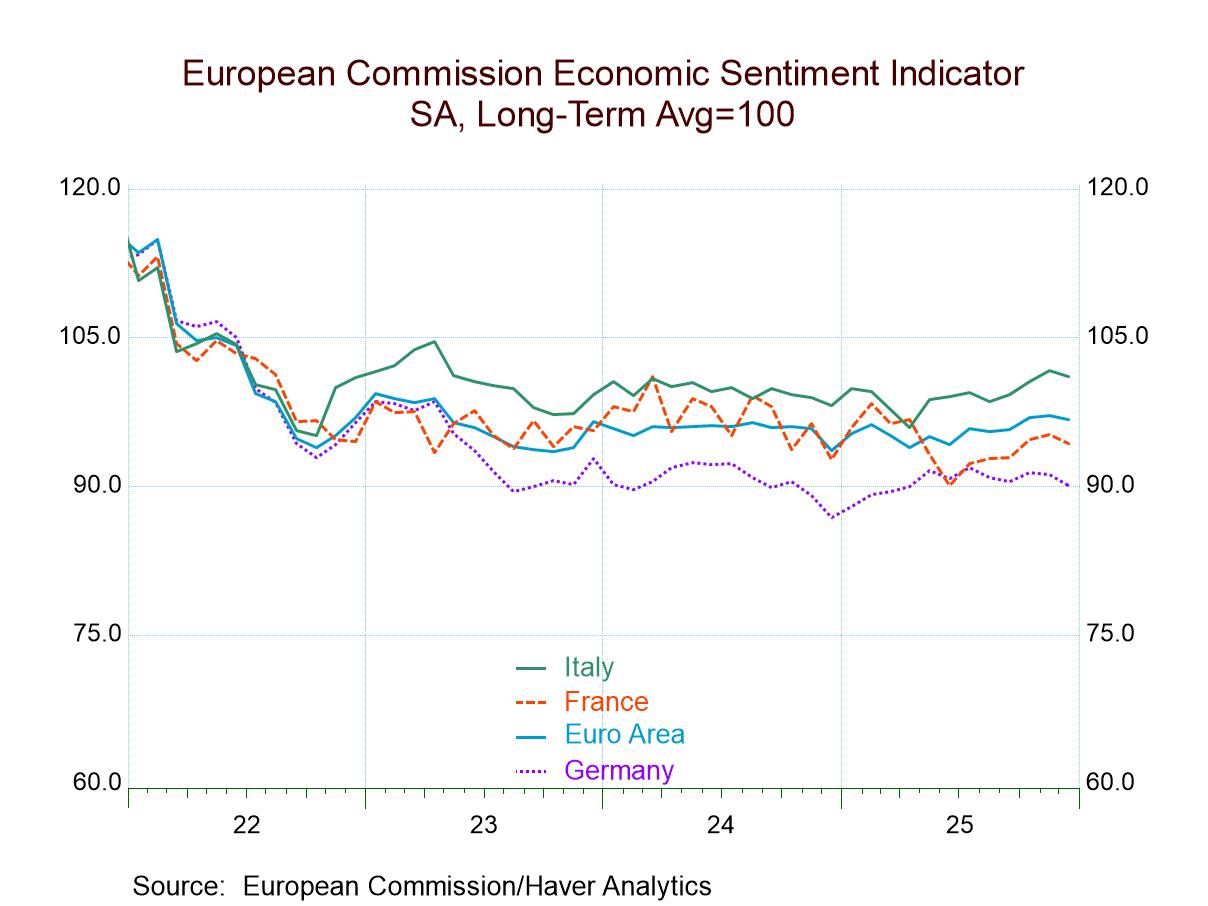

Country stories The chart of the monetary union indexes by sector shows us that there has been little change and little trend in these observations. Across countries Germany has definitely been the weakest country among the BIG4, while Italy has been the strongest. Inflation data have showed inflation beginning to heat up in Spain, and Spain does have the strongest queue standing among the four largest monetary union economies - so that might be something to keep an eye on going forward. Conditions in Germany and France are still quite weak and seem unlikely to force an increase in inflation.

Smaller economies- some specifics And so, the rest of the monetary union economies show tiny Malta, which is hardly a price-maker, has a strong 99.6 percentile standing, followed by 70th percentile standings in Greece and then Lithuania. Portugal and Cyprus have readings in their 60th percentiles. For the most part, these are modest readings but above their medians, of course. Among the weak economies in the rest of the union, the weakest is Belgium with a 16.9 percentile standing, followed by Estonia at a 28.4 percentile standing, Luxembourg at a 32.8 percentile standing, and Austria at a 33-percentile standing. After that, Finland’s standing goes to 37.7 percentile with the Netherlands, Slovakia, and Latvia all with readings in their 40th percentiles indicating moderate undershooting relative to their respective medians.

Summing up On the whole, the EMU area weakened into 2025 with the large economies turning up weaker numbers than what we'd prefer to see and with sectors split although with the important job creating services sector holding steady for two months after having picked up in November. The recent month-to-month weakness stems from consumer confidence and retailing and we have seen some of that play out in data from Germany where retail sales were unexpectedly weak. Broader concerns about unemployment in the monetary union have not moved excessively. In the consumer survey, unemployment expectations are at 51.9% just slightly above their historic median, a relatively normal reading. The weakest readings on the consumer side are from expectations for the financial situation over the next 12 months and the economic situation over the next 12 months. By country, each of the four largest economies has a consumer confidence percentile standing below its historic median. So the consumer is not poised to lead the monetary union out of the wilderness into growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global