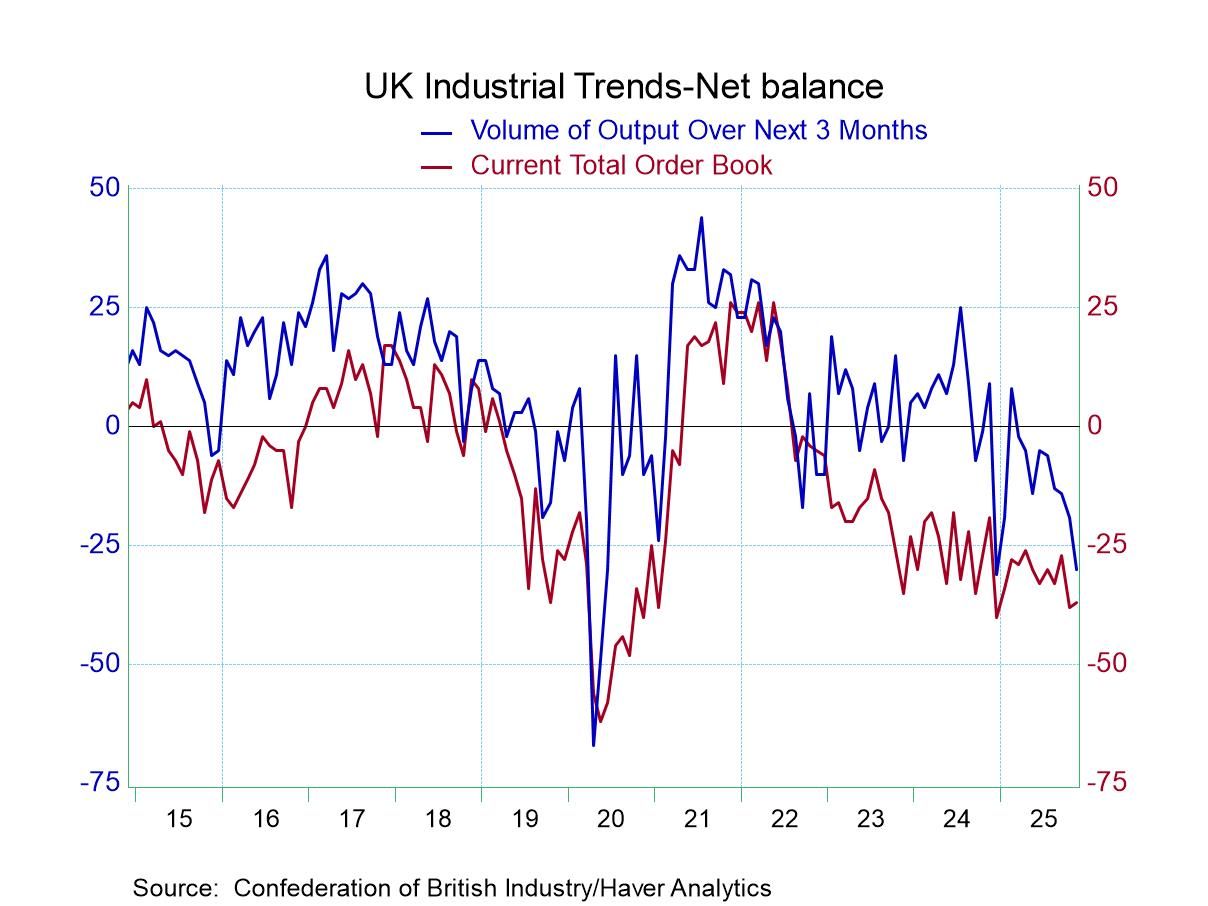

CBI Industrial Survey Seeing Ongoing Weakness and Deterioration Ahead

The survey of the industrial sector by the Confederation of British Industry (CBI) shows ongoing weakness for orders and export orders as stocks build slightly more aggressively. The build out in stocks when orders and expectations for volume are falling is not a good sign and suggests that the inventory buildup may be involuntary and that may be setting the stage for weaker economic performance ahead.

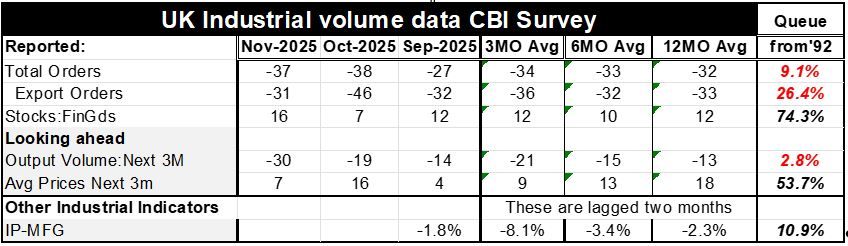

Total orders in November notch a reading of -37 on the net diffusion reading, about the same as the -38 logged in October. Both of those are significantly weaker than September's -27 and compare to a six-month and 12-month average around minus 32 and minus 33.

Export orders are improved in November but still quite weak at a reading of -31 compared to -46 in October. At -31 the November net reading for exports is similar to the six- and 12-month averages which are -32 and -33, respectively.

Stocks of finished goods in November have moved up to +16 from +7 in October they were higher than the 12-month average and the higher than the six-and 12-month averages, the latter 2 hovering around values of 10 and 12 compared to this month's value of 16.

An accelerating weakening appears, looking ahead for output volume over the next three months. The reading drops to -30 in November from -19 in October and -14 in September; the 12-month average stands at -13 with the six-month average of -15. This is a severe deterioration

Average prices over the next three months, however, as expected output volume deteriorates sharply in November is expected to see less pressure. The November value for prices in 3-months at a reading of +7 compares to score if +16 in October. At +7 the price expectations are well below the 12-month average which has been 18 and the six-month average which checks in at +13. With economic cooling expected, cooling in price pressures are expected to accompany that slow down.

Standings by the numbers: The queue standings of the November variables are uniformly weak. The exception is stocks of finished goods which have a 74-percentile standing displaying strength in that measure while orders and expected output volume are weak as a bad sign. Average prices, while losing some momentum in November, still have a standing at their 53.7 percentile, slightly above their median- so these are still somewhat heated price readings although the pressure is off compared to October and compared to 6-month and 12-month standards. Total orders have a 9-percentile standing; export orders have a 26-percentile standing and the expectation for output volume over the next three months has only a 2.8 percentile standing.

The activity and expected activity portions of the survey remain very weak. Their results support the idea that the economy may need more help from the Bank of England despite some ongoing inflation overshoot. As mentioned in yesterday's write up the inflation metrics are beginning to converge toward values that the Bank of England will find more acceptable although the current levels of variables measuring inflation are still too high. The momentum is in the right direction and with economic weakness in train, it's hard to imagine the Bank of England holding the line or standing on ceremony because inflation is still above target. The economy is beginning to emit signs that are a more significant outcry for help.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global