Unemployment Claims: Modest Changes

Summary

- Initial claims remain range bound at a low level

- Continued clams are drifting upward

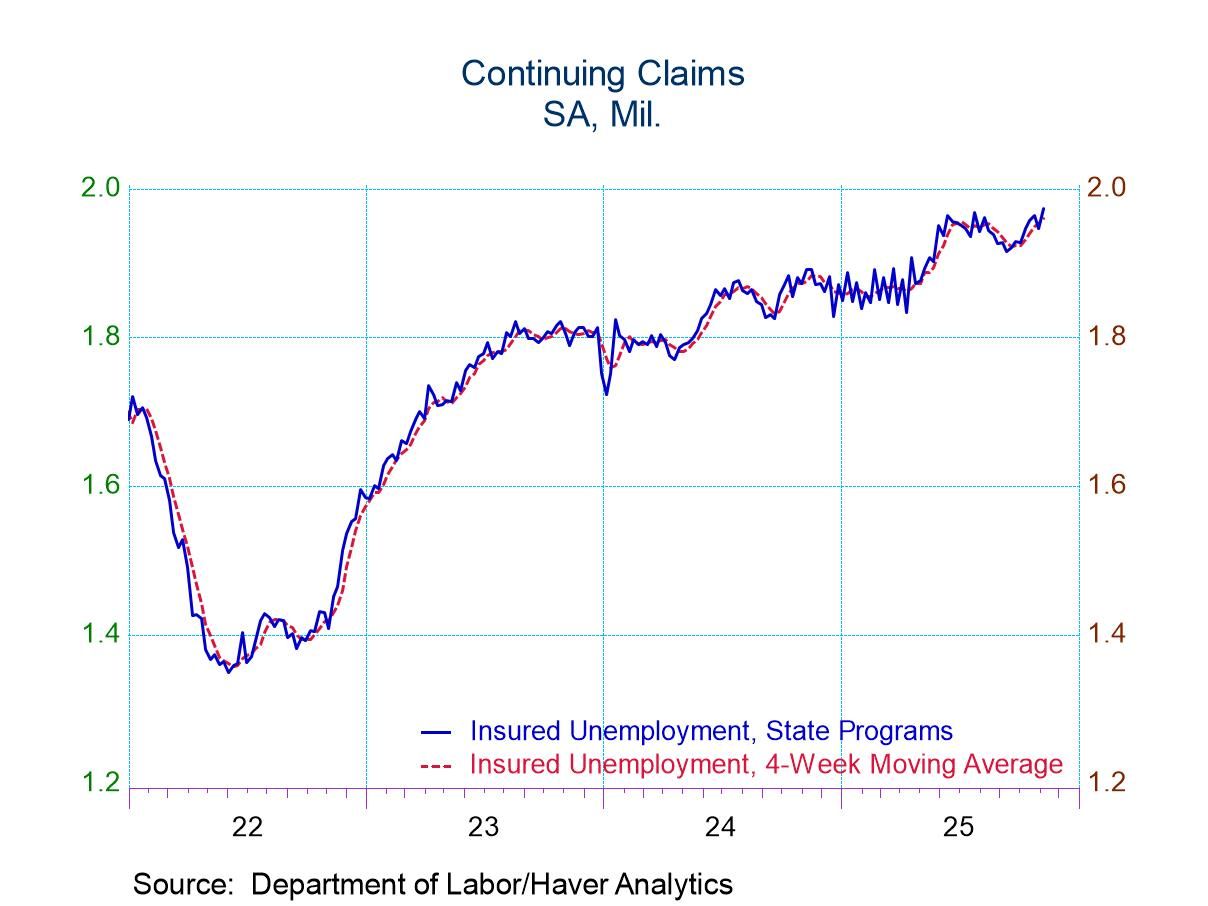

After a seven-week hiatus because of the government shutdown, the Department of Labor this week resumed the publication of data on claims for unemployment insurance. The newly available figures for initial claims showed essentially no change in the comfortable underlying trend. Continued claims (i.e. the number of individuals receiving unemployment benefits) took a small step higher and added to an upward drift that began in the spring. Although continued claims have drifted higher, they are not at an alarming level relative to historical standards.

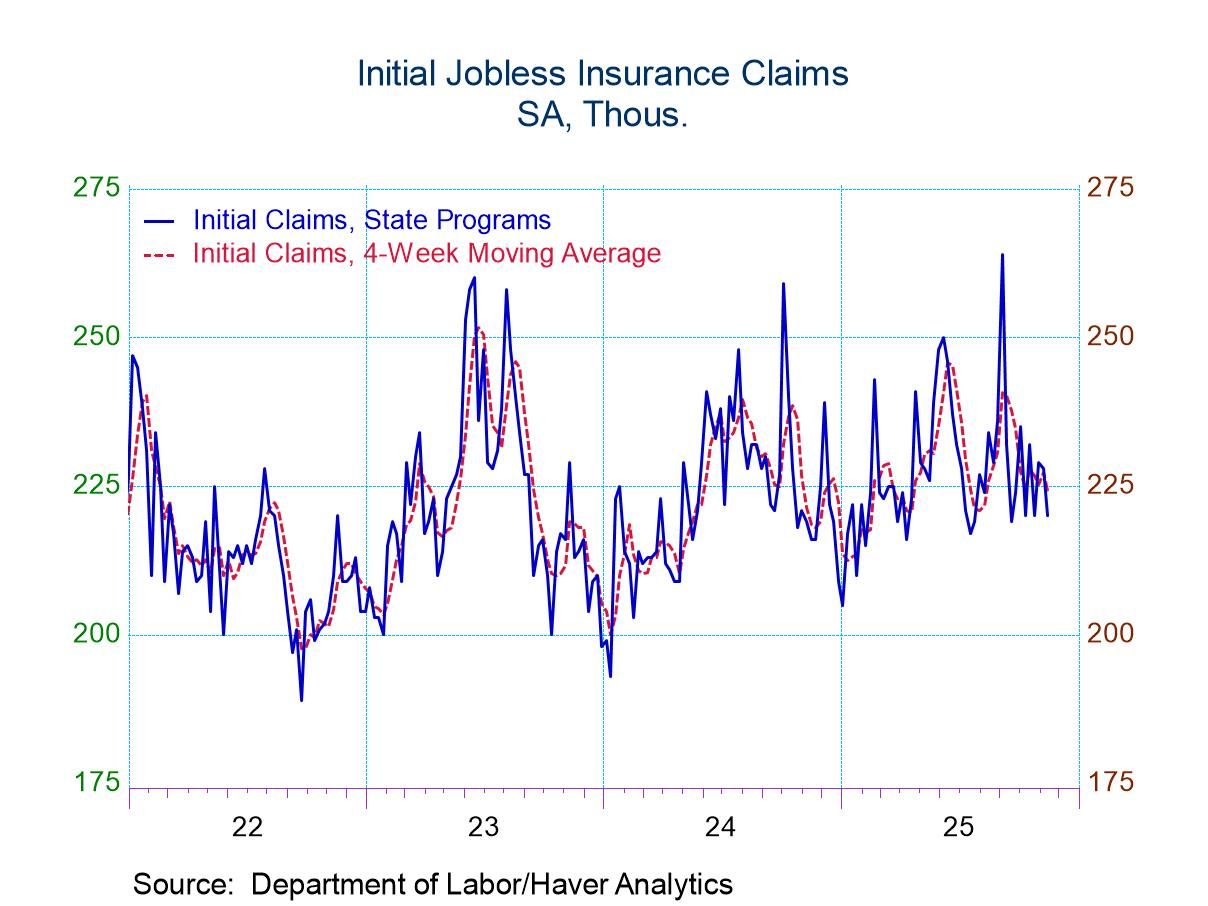

Initial claims totaled 220,000 in the week ended November 15, a reading that is comfortably within the range of the past three years and low by historical norms. Indeed, the latest reading and the average of 228,000 for the year to date is close to the pre-pandemic average of 219,000 in 2018 and 2019, when the labor market was viewed as strong. The range of observations from this year might strike some observers as wide, but initial claims carry a strong random element, and fluctuation this year were within the normal range of volatility. The standard deviation so far this year has totaled 11, essentially identical to results in 2018 and 2019 and a bit lighter than the average in the prior two years.

Steady trends in initial claims seem out of step with announcements of layoffs by major corporations in recent weeks and with slow net job growth in recent months (average payroll growth of 39,000 in the past five months). Announced layoffs by corporations often are implemented gradually, and thus the layoffs would affect claims with a lag. Soft payroll figures are perhaps reflective of cautious hiring by businesses rather than a jump in separations.

A reluctance to hire is evident in the upward drift in continued claims for unemployment insurance. The strong recovery after the pandemic pushed this measure to the low end of its historical range in 2022. The increase in 2023 and 2024 was not especially troubling, as the number of individuals receiving unemployment benefits was still comfortable by historical standards. The upward drift since the spring could be viewed as a shift in the tone of the labor market, but the rate of change and the level are not suggestive of marked weakening. The latest reading of 1.974 million exceeds the average of 1.718 during the strong labor market of 2018-19, but it is still in the low end of the historical range and far below results seen during recessions. The measure has reached levels of approximately 4.0 million in most past recessions and it exceeded 6.5 million in the depth of the Great Recession in 2009.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global