Asia

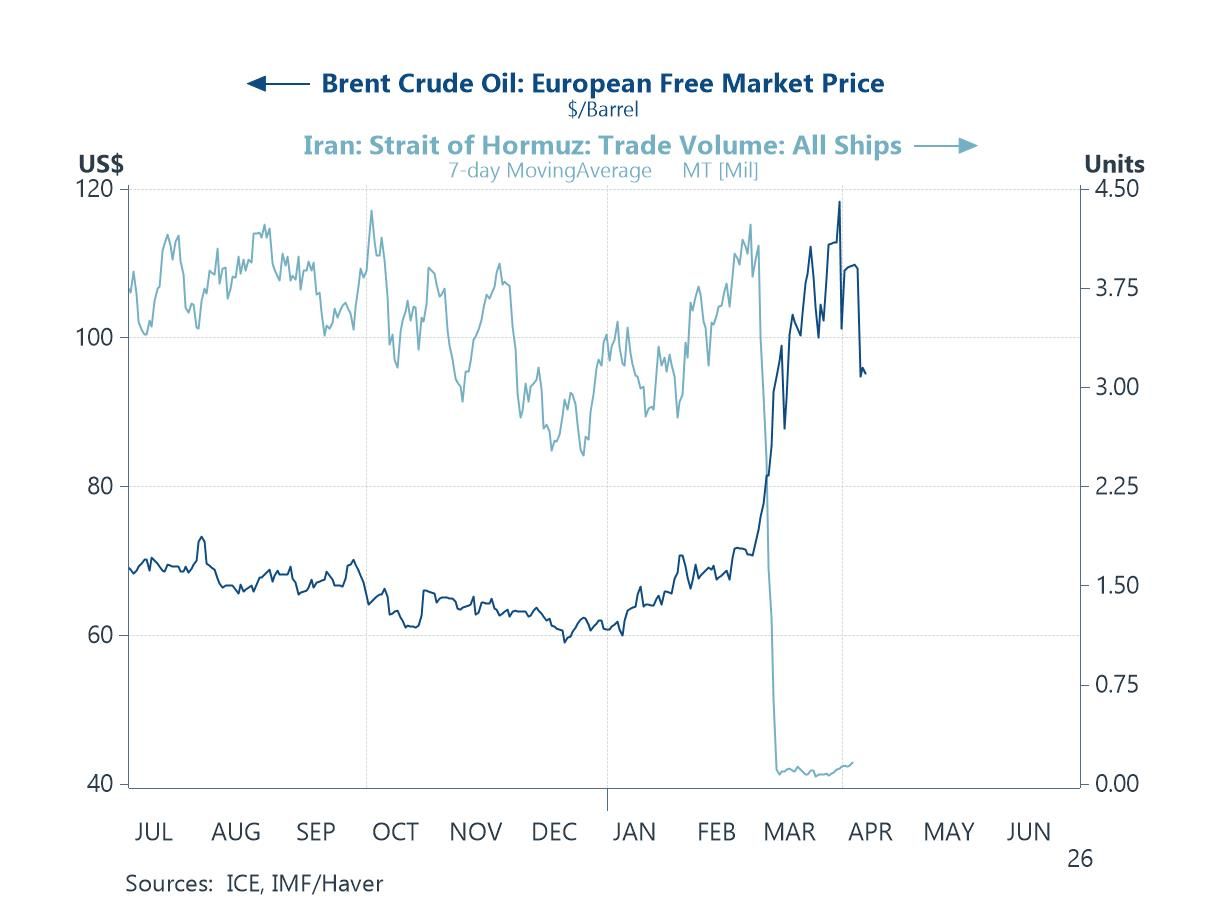

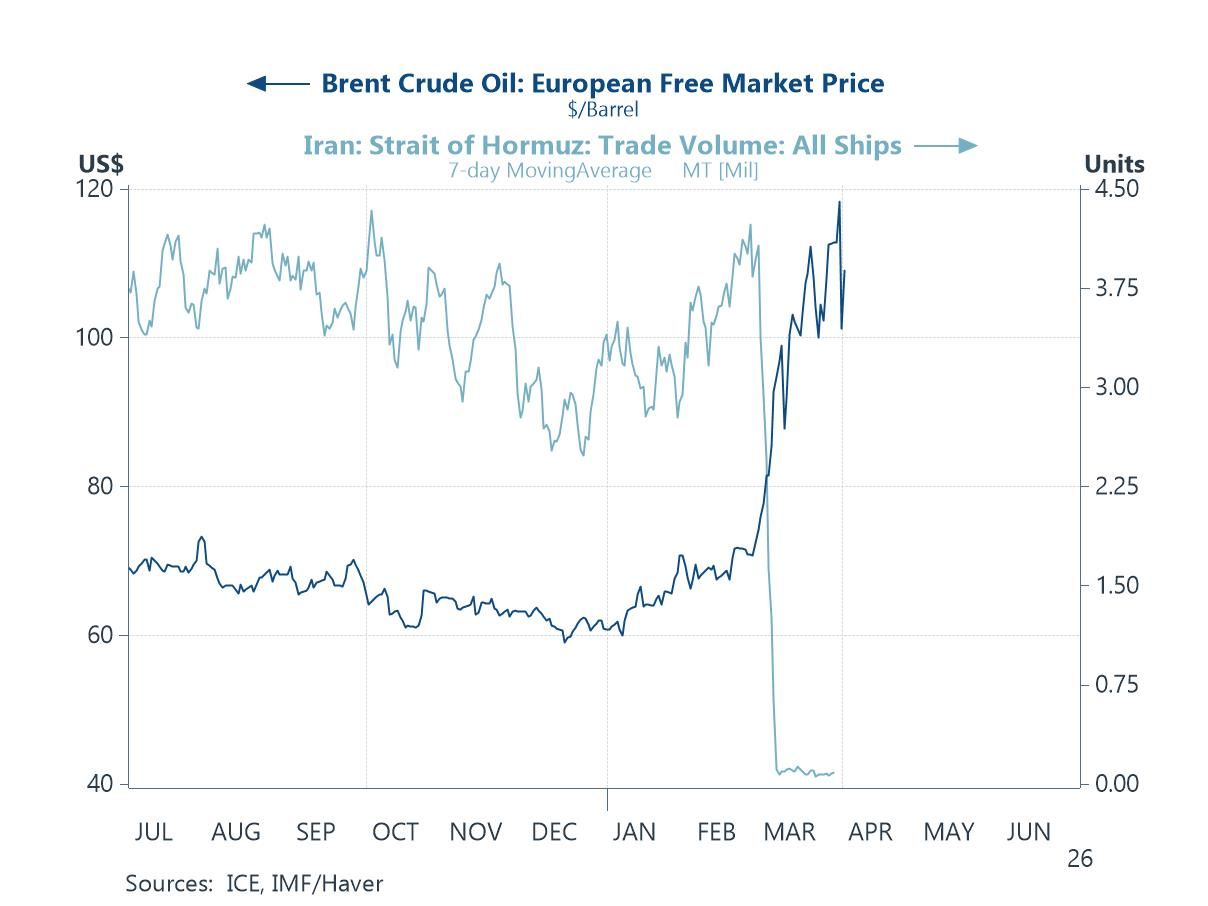

AsiaIn this week's Letter, we explore the significant pullback in oil prices that followed the US-Iran memorandum of understanding and consider its broader economic implications. The agreement saw a fragile ceasefire ensue and a gradual resumption of shipping flows through the Strait of Hormuz (chart 1). We acknowledge that this major pullback will certainly be welcome to policymakers across the region and beyond. Previously elevated energy prices had added to the fiscal burdens of governments and sharpened the dilemma facing central banks (chart 2). That dilemma pits the need to rein in inflation against the risk of choking off economic growth. That said, while one source of inflationary pressure seems to be ebbing, another looks to be emerging on the horizon. It stems from a potential "Super El Niño" event, which meteorologists have been warning about for some time now. Asia sits at the centre of such risks, as past strong El Niño events have directly and adversely affected crop production (chart 3). The impact is not limited to potential surges in headline inflation via food supply shocks, especially in Asia. It extends directly to growth as well (chart 4), given the nontrivial share of GDP that agriculture still commands in many Asian economies (chart 5). Should price pressures simply rotate from energy to food, government subsidies may follow suit (chart 6). Central bankers, for their part, may find themselves unable to ease off the tightening pedal just yet. Some Asian economies, however, would still manage to offset such a growth shock through other engines. Electronics and semiconductors, buoyed by the current AI upcycle, offer one such cushion for the more fortunate. For others, lacking such offsets, the agricultural hit may simply have to be borne in full.

The US-Iran conflict and oil prices The recent memorandum of understanding between the US and Iran, aimed at working towards a final deal, has already brought visible relief to crude oil markets (chart 1). This relief has held despite the renewed tensions that have followed the agreement, which markets seem to have largely looked past. The easing in prices should go a long way towards unwinding the inflation concerns that elevated oil prices had previously stoked. Much of the pullback reflects anticipation of the substantial supply now expected to return to global markets. Yet some shipping trackers, such as the IMF's, already point to a marked pickup in traffic through the Strait of Hormuz. Even so, those volumes still remain well below the levels seen before the conflict began in the region.