Asia| Jul 08 2025

Asia| Jul 08 2025Economic Letter from Asia: The Final Countdown?

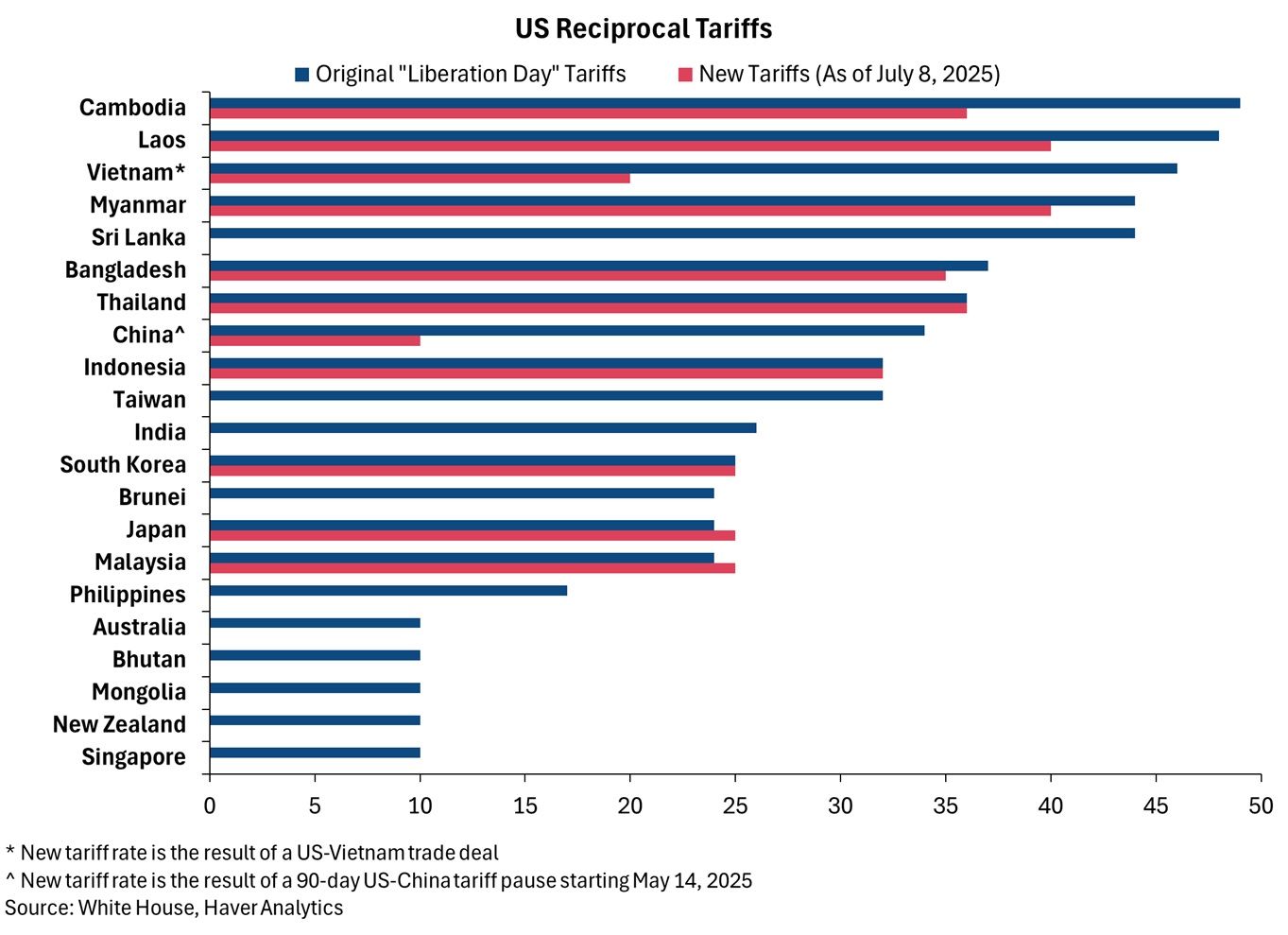

This week, we look at the latest US trade developments and their implications for Asia, as President Trump unveiled new tariff rates on 14 countries (chart 1). Though some rates were lower and implementation delayed to August 1, the move signals the US tariff pause is ending and deepens investor uncertainty in Asia. Market sentiment has weakened, reflecting both renewed policy risks and stalled trade negotiations in the region (chart 2).

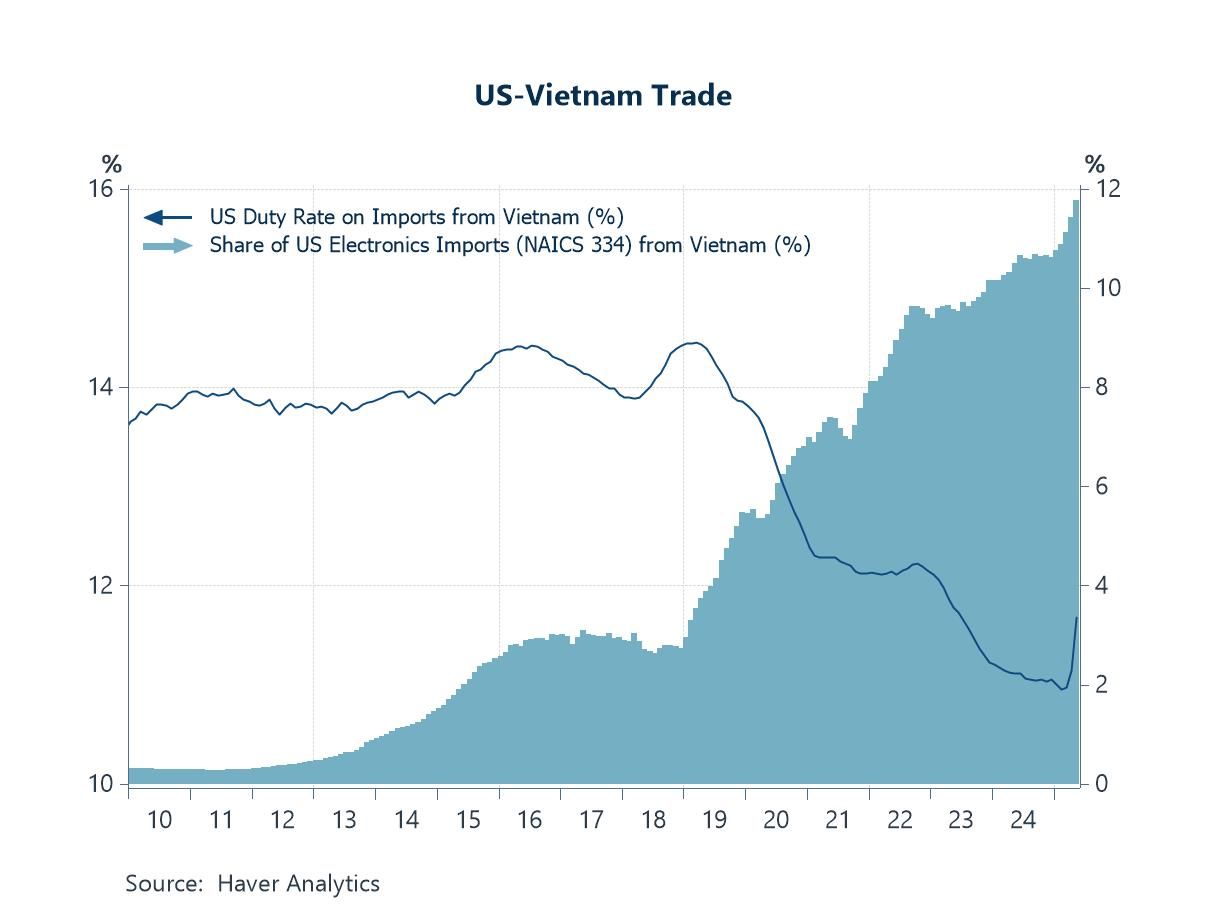

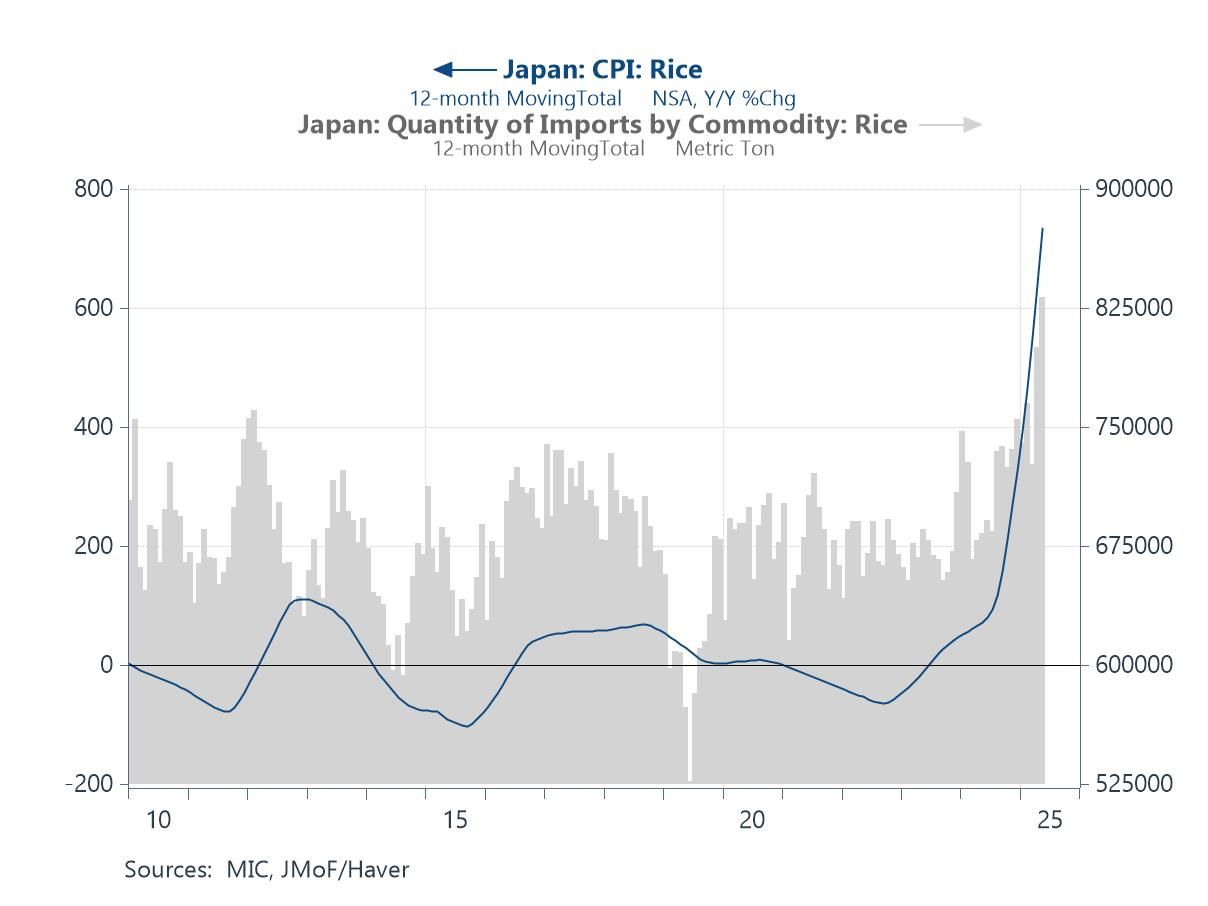

Vietnam stands out as a rare exception, having secured a deal with the US that reduced its tariff rate from 46% to 20%. However, the agreement includes a 40% tariff on “transshipments,” aimed at curbing indirect exports from third countries, such as China. In return, the US has gained tariff-free access to Vietnamese markets—an offsetting benefit for American firms. Nonetheless, the 20% rate remains high and could raise costs for US consumers if passed through supply chains (chart 3). Japan, by contrast, faces a more delicate balancing act. A 25% tariff was confirmed, while pressure persists over access for US agricultural exports—particularly rice (chart 4). Domestic sensitivities remain elevated amid a rice shortage and looming upper house elections, limiting Tokyo’s room to manoeuvre.

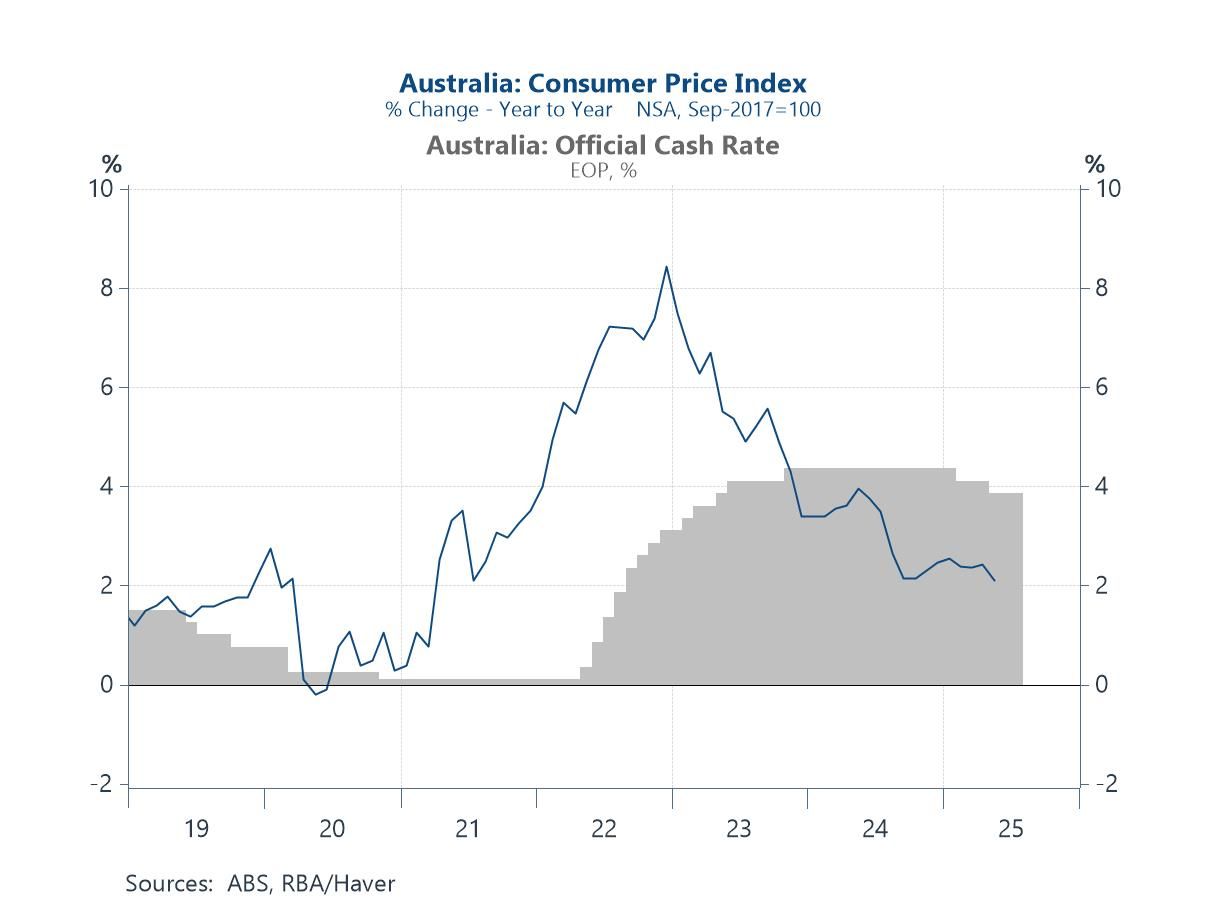

Regional central banks are responding cautiously. The Reserve Bank of Australia held rates steady, defying expectations of a cut and citing a need for more information (chart 5). Rate decisions from South Korea, New Zealand, and Malaysia are due this week, with South Korea’s central bank seen likely to hold, amid rising home prices and mortgage growth (chart 6).

Latest US tariff developments As previously signalled, US President Trump on Monday unveiled a new round of tariff rates targeting 14 countries, confirming initial fears that the US would move forward with reciprocal tariffs following its 90-day pause. While investor concerns—renewed late last week—have begun to materialize, there are two modest sources of relief. First, as shown in chart 1, many of the newly announced US tariff rates are actually lower than those initially unveiled on “Liberation Day,” April 2. Second, President Trump has delayed the effective date of the tariffs to August 1, offering a temporary window for countries that have not yet done so to negotiate trade deals with the US. However, while the extension allows more time for dialogue, it does not constitute a formal delay in implementation—at least for now. That said, progress in trade negotiations with the US remains limited across most Asian economies. In some cases, such as Japan, talks may have even come to an impasse—this will be explored further in subsequent sections. Vietnam, however, stands out as an exception, having secured a trade agreement with the US late last week; this development will also be discussed in more detail later on.

Chart 1: US reciprocal tariffs

Understandably, the earlier sense of relief—when tariffs appeared to have been delayed—has faded, giving way to renewed uncertainty. As this shift in sentiment takes hold, equity performance across advanced Asia has weakened slightly in recent days, as shown in chart 2. This likely reflects not only rising investor caution but also the lack of substantial progress in trade talks with the US, which contributed to the unveiling of tariff rates on Monday—unlike the more favourable treatment seen in Vietnam’s case. Looking ahead, investors focused on Asia will turn their attention to several country-specific trade discussions with the US for further cues. Growth and inflation outlooks are also likely to be revised, as not only first-round but also second- and subsequent-round effects of the tariffs are increasingly factored in. Another noteworthy development is US Treasury Secretary Bessent’s recent statement that around 100 economies and territories will now face a baseline tariff of 10%. If accurate—and if the 10% rate holds as the minimum—it suggests that many of the roughly 20 or more economies originally assigned that baseline rate have now been excluded. In effect, their relative trade position has worsened. In the Asia-Pacific region, key economies to watch in this context include Australia, New Zealand, and Singapore.

Chart 2: Advanced Asia equity index performance

Vietnam While trade deals with the US have been few and far between since the beginning of the tariff pause, Vietnam has stood out following the announcement of a new trade agreement with the US late last week. Originally facing a reciprocal tariff rate of 46%, Vietnam has reached a deal to reduce that rate to 20%. However, the agreement also includes a 40% tariff on so-called “transshipments”—a measure aimed at addressing US concerns that goods may be routed through Vietnam from other economies, possibly China, to circumvent higher tariffs or trade restrictions. In return, the US has secured tariff-free access to Vietnamese markets. While the 20% rate is a significant improvement over the initially proposed 46%, it remains relatively high—especially compared to the 10% reprieve level. This will likely translate into higher costs for American consumers unless the increase is absorbed by producers or suppliers. On the positive side, tariff-free access to Vietnam offers some offset, particularly for US input goods sent to Vietnam for further processing, which would avoid additional tariffs on that leg of trade. That said, there is still uncertainty around how the “transshipment” clause will be defined and enforced in practice. Given Vietnam’s role as a major supplier of electronics—including smartphones—to the US (chart 3), the increase from the 10% pause rate to 20% is significant. If the added costs are passed through the supply chain, it could lead to a noticeable impact on US consumer prices.

Chart 3: US-Vietnam trade

Japan Turning to Japan, the country is delicately balancing two competing pressures: minimising the economic fallout of renewed US tariffs while resisting trade concessions that could be seen as damaging to its domestic interests. A key sticking point is Washington’s push for greater access to Japan’s agricultural market—particularly for US rice. President Trump has criticized Japan as “spoiled” for resisting such demands and previously threatened tariffs of 30–35%. On Monday, however, a 25% tariff on Japanese goods was announced—slightly above the 24% rate first unveiled on “Liberation Day,” April 2. Meeting US demands would carry significant political risks for the Japanese government. Any perceived concession on rice would likely spark backlash from Japanese farmers, a core constituency of Prime Minister Ishiba’s political base. The issue is especially sensitive with upper house elections on the horizon. Complicating matters further, Japan is currently facing a domestic rice shortage that has been driving up prices. Given rice’s central role in the Japanese diet, the shortage is a growing cost-of-living concern. In response, Japan has already ramped up rice imports, as shown in chart 4, including by moving forward a tariff-free tender—originally scheduled for September—for 30,000 tons from the US, Australia, and Thailand. However, compared to Japan’s overall consumption needs, this added supply is little more than a drop in the bucket.

Chart 4: Japan rice prices and imports

Central bank decisions this week This week’s renewed US trade uncertainty threatens to complicate a busy calendar of central bank decisions across the region. First among the major announcements was the Reserve Bank of Australia (RBA), which defied consensus expectations by leaving its policy rate unchanged, rather than delivering the widely anticipated 25 bps cut. While the RBA acknowledged significantly cooled inflation—as shown in chart 5—it also pointed to a still-tight labour market and market sentiment suggesting that the most extreme US trade scenarios are likely to be avoided. Citing the need for more information before considering its next steps, the RBA opted to maintain its policy rate at 3.85% following its July meeting. Other key central banks set to announce decisions this week include those of New Zealand, South Korea, and Malaysia—the latter two of which are facing 25% US tariffs starting August 1, absent a trade agreement, as announced by President Trump on Monday.

Chart 5: Australia inflation and policy rate

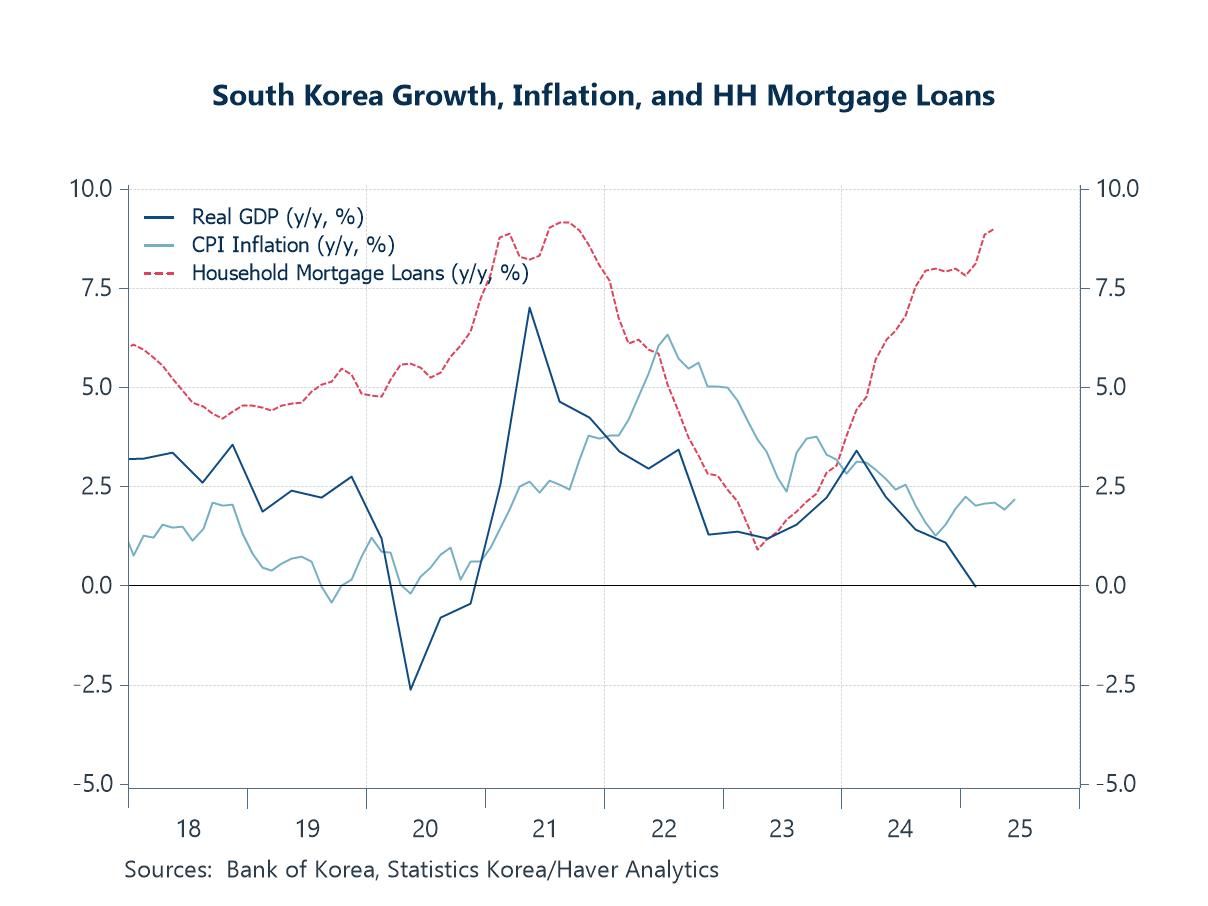

Lastly, turning to South Korea, the central bank (BoK) has already lowered rates four times since beginning its easing cycle last October and maintained a dovish tone at its most recent meeting in response to weakening growth momentum. However, the BoK is widely expected to hold rates steady this week. It is aiming to strike a balance between supporting growth—particularly with the potential reinstatement of US tariffs looming—and avoiding overheating in segments of the domestic economy. In particular, the BoK remains concerned about the property market, where housing prices have resumed their upward trend, and the household loan sector—especially mortgage lending—where loan growth has once again accelerated, as shown in chart 6.

Chart 6: South Korea GDP growth, inflation, and household mortgage growth

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief