Asia| Jun 30 2025

Asia| Jun 30 2025Economic Letter from Asia: Tariff Deadlines

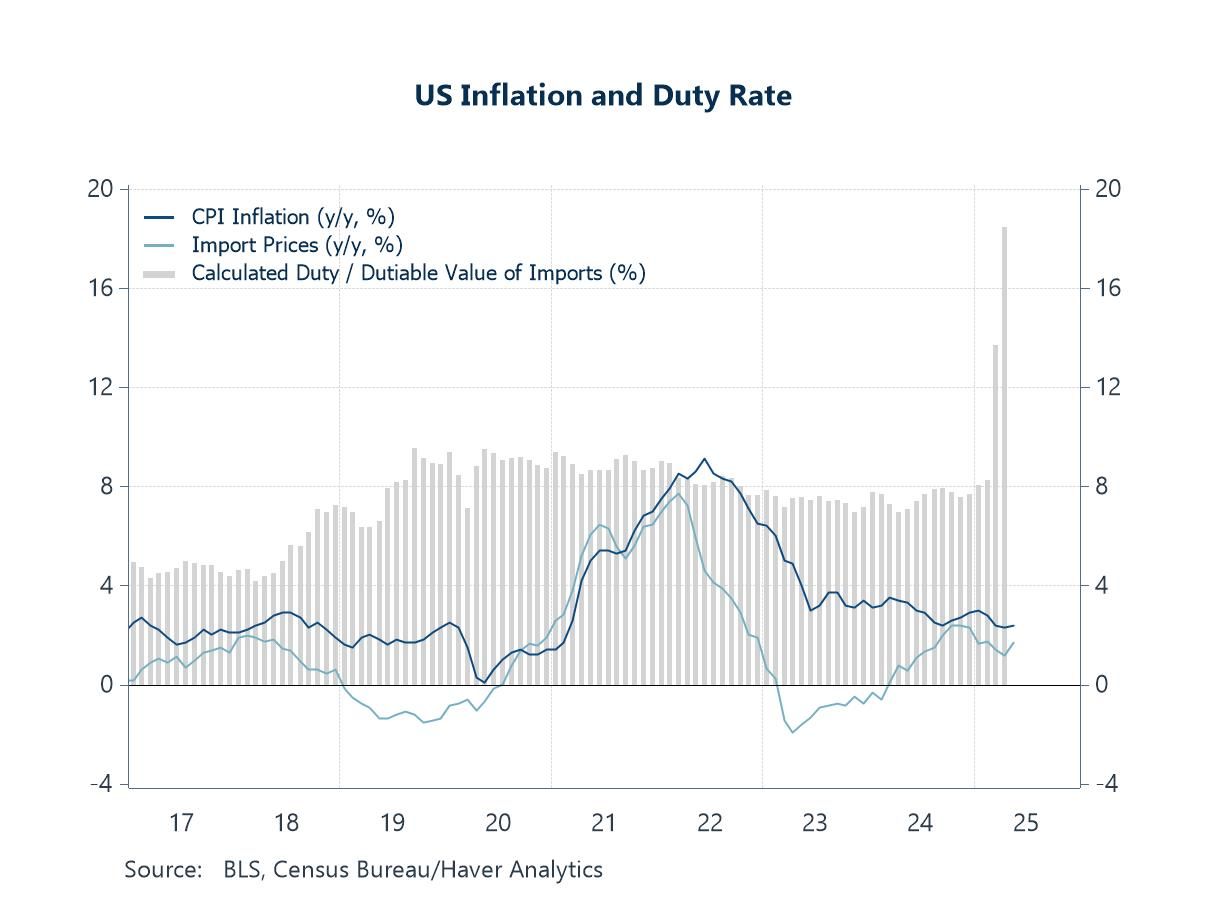

This week, we look at the state of US–Asia trade talks as the July 9 expiration of the US’ 90-day tariff pause approaches. Despite early activity, few deals have been finalized. So far, the US has reached only a limited agreement with the UK and rolled back mutual tariffs with China, alongside a framework on rare earth exports. Much of the action has focused on undoing previous measures rather than making new advances. Still, Asian markets have shown signs of stability (chart 1), though volatility may return as the tariff deadline nears. The outcome remains uncertain. President Trump has indicated flexibility on the deadline, and Treasury Secretary Bessent has suggested more deals may come only by Labor Day in September. Meanwhile, US effective tariff rates have already risen (chart 2), though inflation impacts have been muted, likely due in part to importers absorbing costs.

Among Asian partners, India shows the most near-term promise, with ongoing talks focused on mutual market access, though barriers remain in agriculture and dairy (chart 3). Japan has made no breakthroughs despite pressing concerns over auto and metal tariffs—sectors key to exports and GVA (chart 4). South Korea, just emerging from political transition, is only beginning substantive talks (chart 5). In Southeast Asia, Indonesia and Vietnam are among the most likely to reach agreements. Both face steep tariff hikes if talks fail, particularly Vietnam with a potential 46% rate. Indonesia has submitted proposals, while Vietnam remains optimistic. Thailand, still early in talks and politically distracted, is unlikely to meet the July 9 deadline (chart 6).

US trade deals so far this year We have already reached the end of the first half of the year, and the US’ flurry of trade-related actions has so far yielded tangible outcomes with only a few countries. To date, the US has concluded a limited trade deal with the UK and reached an agreement with China to roll back many of the tariffs both sides imposed earlier this year. More recently, the US and China also established a framework concerning China’s rare earth export controls. That said, much of the world remains without new US trade deals. Most of the developments thus far have focused on partially reversing measures implemented earlier this year, rather than advancing beyond the pre-inauguration day baseline. Still, a measure of market calm has returned—at least in Asia—as reflected in recent rallies across some of the region’s equity indexes (chart 1). However, renewed volatility may lie ahead as the July 9 expiration of the US’ 90-day pause on reciprocal tariffs approaches.

Chart 1: Asia equity performance

The situation, however, remains highly fluid. While US President Trump may reimpose his “Liberation Day” tariffs if no deals are reached by the July 9 deadline, he could also opt to extend the pause—especially if there appears to be potential for favourable trade agreements. This possibility was hinted at by Trump himself, who remarked that the US “could do whatever we want,” including extending or even shortening the deadlines. Also, US Treasury Secretary Scott Bessent has suggested that additional trade deals are more likely to materialize by Labor Day on September 1 instead of the July 9 deadline. Complicating progress on US trade talks with other countries is a string of recent geopolitical flashpoints—including US involvement, directly or indirectly, in the Israel-Iran, Israel-Hamas, and Russia-Ukraine conflicts. These crises have dominated headlines and may have also diverted the President’s attention. In the meantime, US effective tariff rates have already increased, as shown in chart 2, reflecting the impact of tariffs already in force. Interestingly, US inflation has not yet spiked as might have been expected. This could be partly due to importers absorbing some of the tariff costs by cutting prices.

Chart 2: US inflation and effective tariff rates

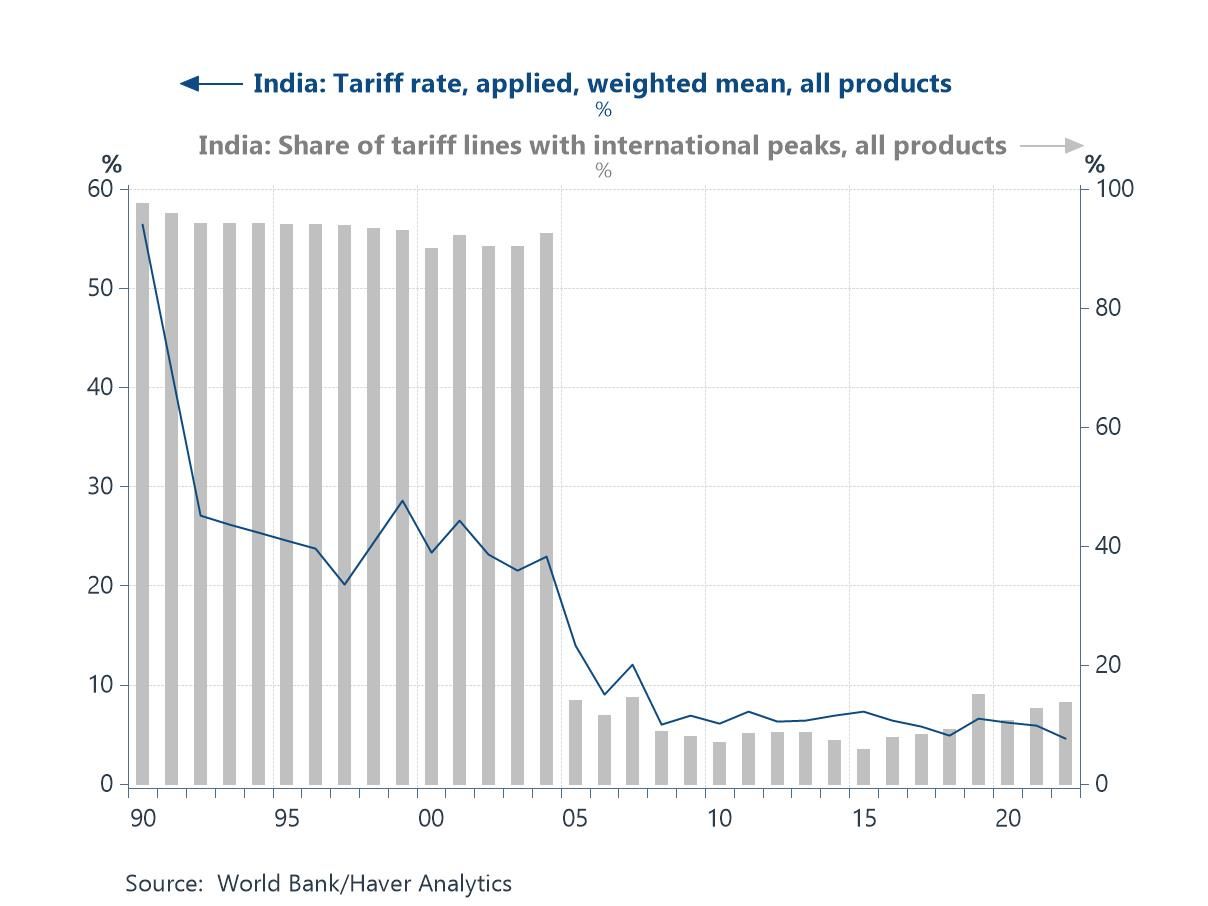

India Setting aside the agreements already reached, the country that currently appears to hold the most promise for the next tangible US trade outcome is India. US President Trump has indicated that a “very big” trade deal with India is likely on the horizon. Whether a first phase of that deal can be finalized before the July 9 deadline remains uncertain, with just over a week to go. However, the progress made so far may be enough to earn India some additional breathing room before the reintroduction of the US’ “Liberation Day” tariffs. Of particular interest to the US is greater access to India’s domestic markets, which have traditionally been heavily protected by both tariff and non-tariff barriers (chart 3). So far, India has shown some reluctance to fully open certain key sectors—particularly dairy and agriculture. In turn, India is seeking expanded access to US markets, especially in labour-intensive sectors such as textiles and leather goods, which are important for its workforce.

Chart 3: India’s tariff and non-tariff barriers

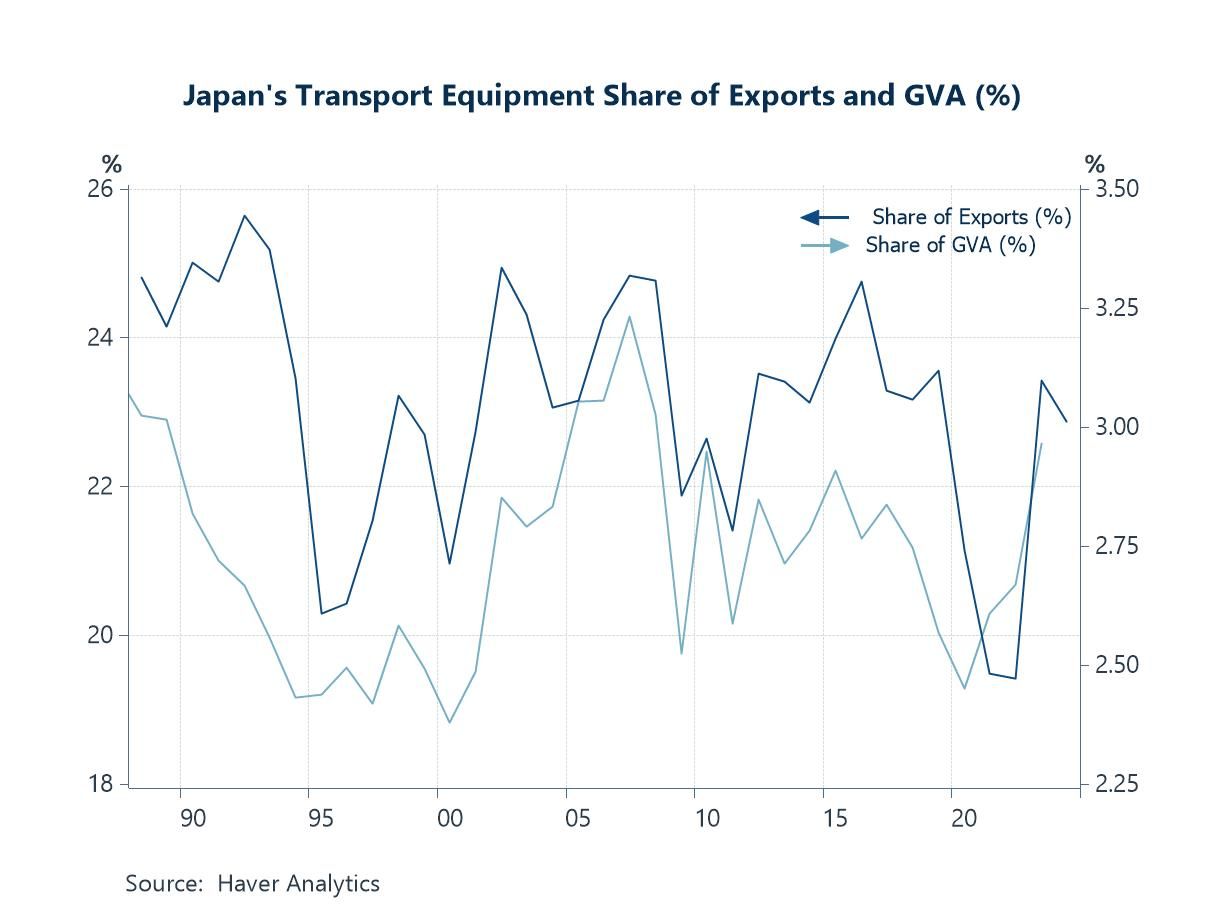

Japan Turning to Japan, progress on a trade deal with the US appears more elusive than in the case of India. So far, there have been no reported breakthroughs in US–Japan talks. While Japan has put forward proposals, the US has yet to move forward on talks, and Japan still faces significant hurdles in resolving its key concerns—namely, US tariffs on autos, steel, and aluminium. The auto industry, in particular, is vital to Japan’s economy. Though it accounts for just under 3% of gross value added (GVA), it contributes substantially to export revenues (chart 4), with the US serving as Japan’s largest export market for vehicles. This underscores the economic weight of the US’ 25% auto tariffs. With time running short, final-hour efforts are ramping up. Following Prime Minister Ishiba’s inability to reach a deal with President Trump at the recent G7 summit, Japan’s chief negotiator, Akazawa, has extended his seventh visit to Washington to help push talks forward.

Chart 4: Japan’s transport equipment share of exports and GVA

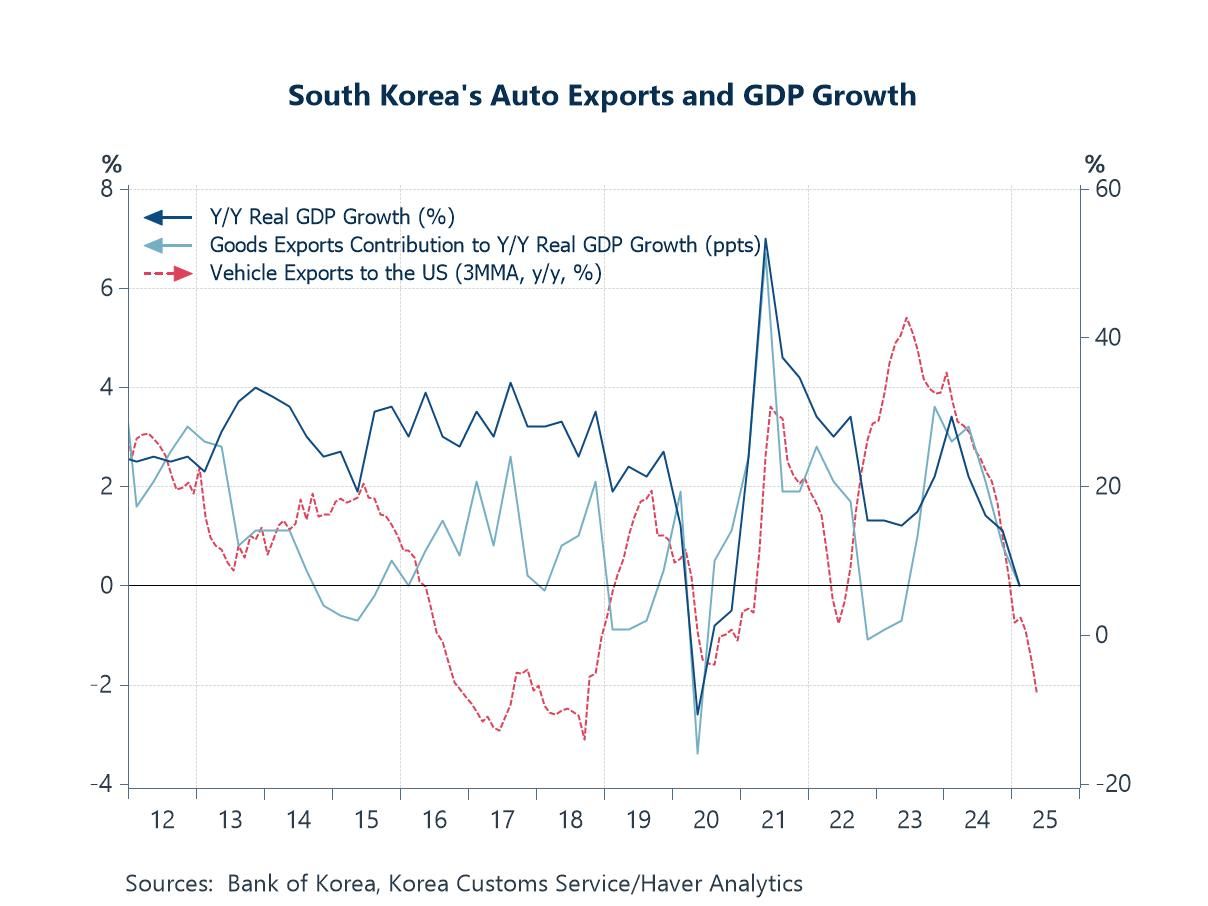

South Korea Like Japan, South Korea faces similar tariff-related pain points with the US—particularly on autos and steel—given the importance of these sectors to Korea’s economy (chart 5). However, unlike Japan, Korea’s trade discussions with the US have understandably been slowed by domestic political uncertainty. The country only recently concluded its elections after a prolonged period of instability, and its new Trade Minister, Yeo, only recently held his first meeting with US counterparts, having just assumed office. As a result, the pace, structure, and direction of Korea’s trade talks with the US remain at a very early stage, with significant progress yet to be made. Given this context, a substantive trade deal by the July 9 deadline appears unlikely, though a limited initial agreement may still be possible.

Chart 5: South Korea’s auto exports and real GDP growth

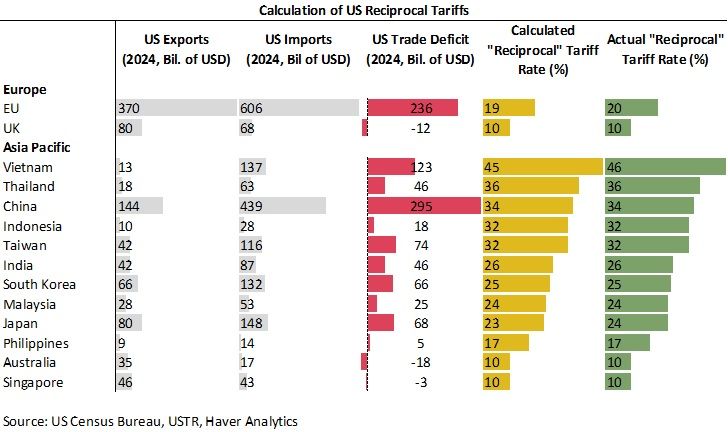

Southeast Asia Lastly, we turn to Southeast Asia, where reports of substantial progress on trade deals with the US have been limited. However, two countries—Indonesia and Vietnam—stand out as among the most likely to secure agreements before the July 9 deadline. Both have strong incentives to do so, as they face the steepest potential reversal of the US' “Liberation Day” tariff pause, with rates shown in chart 6, should no deal be reached and no extension granted. In mid-April, Indonesia and the US agreed to fast-track negotiations, targeting completion within 60 days. The Indonesian side has reportedly submitted all required documentation for its proposal and is now awaiting a response from the US. As part of its offer, Indonesia has pledged cooperation on critical minerals and committed to increasing energy imports from the US, among other concessions.

Vietnam, meanwhile, is also pushing to finalize a deal before the deadline. Its Prime Minister has expressed confidence that an agreement will be reached in time. Missing the deadline would trigger a steep 46% tariff on Vietnamese exports to the US—an outcome that would significantly impact the Vietnamese economy, given the importance of the US market. Thailand, another economy facing one of the highest prospective “Liberation Day” tariff rates, is in a less advanced position. It has only recently begun trade discussions with the US, making a substantial deal by July 9 unlikely. Additionally, domestic political uncertainty—intensified by the recent leak of Prime Minister Paetongtarn’s phone call—adds another layer of complexity.

Chart 6: US original “Liberation Day” tariffs

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.