German Industrial Production Perks Up-Surprise!

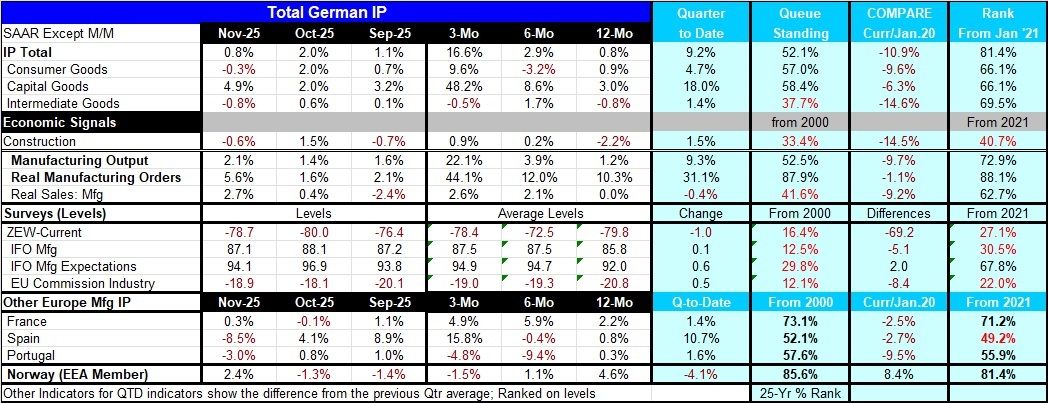

German industrial production advanced by 0.8% month-to-month in November performing better than had been expected. Consumer goods output fell by 0.3% month-to-month, capital goods output soared with a 4.9% gain, while intermediate goods output fell back by 0.8%.

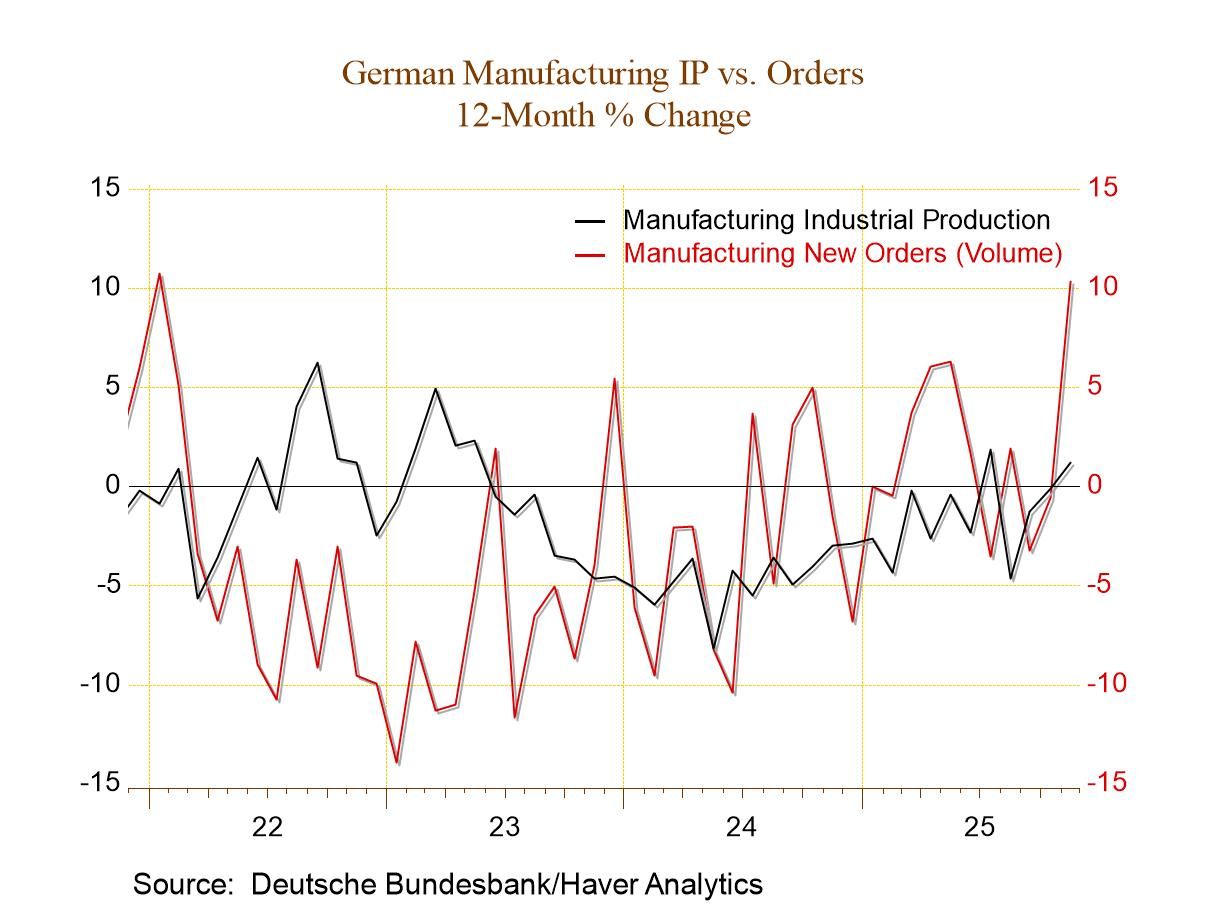

On the whole, manufacturing output had been expected to be weak. But looking at manufacturing alone, rather than total industrial production, the gain was even stronger at 2.1% month-to-month. Real manufacturing orders in November rose by 5.6%, real sales in manufacturing rose by 2.7%. This is solid performance.

Survey data have been weak and listless However, apart from anecdotal evidence, as monthly data unfold, the kinds of numbers that we have to look at first are various economic surveys that come from diffusion data. The ZEW’s current index was slightly stronger month-to-month at a still very weak -78.7 (net) reading compared to -80 in October although both of those were weaker than the ZEW net September reading of -76.4. IFO manufacturing weakened month-to-month in November at 87.1 compared to 88.1 in October and it was slightly weaker than its September value as well. IFO manufacturing expectations slipped to 94.1 in November from 96.9 in October although expectations were slightly higher than their level in September. The EU Commission index weakened in November to -18.9 from -18.1 in October although there was an improvement from -20.1 in September.

These comparisons show us that the survey data which we had in hand before getting the industrial production reading from Germany had given us a lot of weak readings and a lot of very weak momentum.

Compare survey data to IP data using ranking technique We can compare industrial production data to survey data using two different columns in this table. The first is the queue standing column where we see the industrial production data with rankings mostly in their 50th percentile: intermediate goods have a ranking of 37.7% with construction at 33.4%; they are the weaker exceptions. We rank IP data by sector according to their annual growth rates compared to past growth rates. However, by comparison the survey data (that we rank on levels) range between 12.1% and 29.8%; all of those are very weak readings. No wonder a focus on survey data leads to a weak upcoming assessment of production data. We can also look at a slightly more up-to-date, but shorter ranking, from January 2021. There we see that the industrial production data average rankings from the mid-60th percentile up to the 81.4 percentile for total industrial production. Surveys generally have rankings in the 20th and 30th percentile with the exception of IFO manufacturing expectations which reaches 67.8%, which is a solid reading.

Survey data signals should be downgraded? These comparisons show us that while it's hard to compare industrial output directly to the diffusion readings if we take those two metrics over the same timeline and compare the level of the diffusion index to the growth rate of the manufacturing index we get the capability to compare the two on more even footing. When we do that, we see that manufacturing data are doing better than the survey data very broadly speaking. So, while there's some surprise on the strength of manufacturing data, maybe we should place a greater emphasis on it because those data come from a real accounting process rather than from a survey process that is much less closely linked to magnitudes. And, essentially, we are really much more interested in magnitudes than just if something is higher and lower.

Other Europe doing ‘well’, too Not so incidentally the industrial production readings for France, Spain, Portugal, and Norway, all of whom are fairly early reporters of industrial production data, rank well on the queue standing column as well as in the shorter rank standing column from January 2021. In fact, for these countries the difference in ranking between the two periods is not markedly different, certainly not as markedly different as it is for Germany. On the whole, it may be that Europe has been doing better than we thought because we've been spending too much time looking at the more up-to-date survey data on a PMI basis, rather than waiting for the more traditional and lagging industrial production reports that are accounting-based data and more thorough.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia