Asia| Jul 28 2025

Asia| Jul 28 2025Economic Letter from Asia: Dealing with it

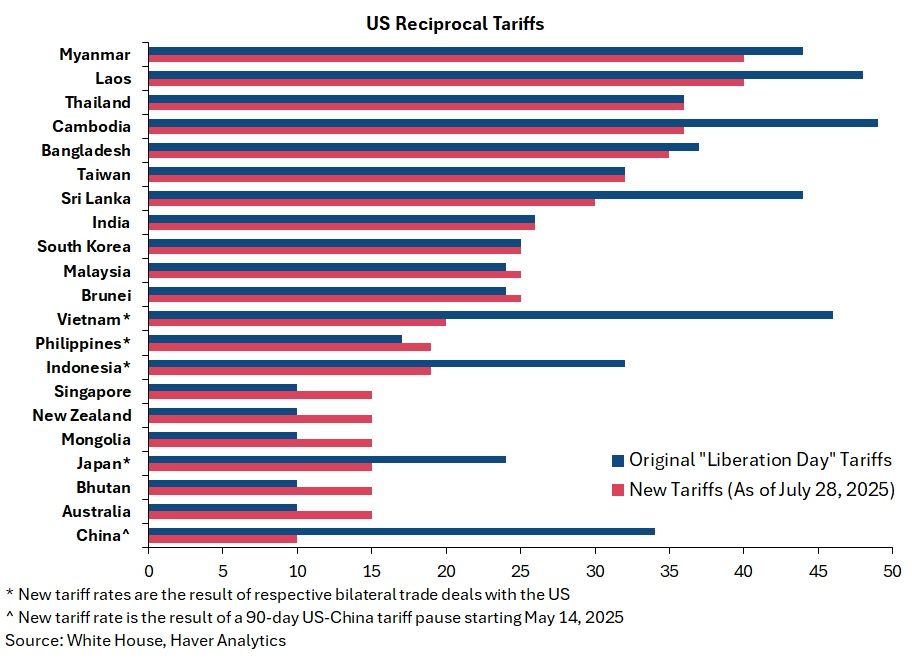

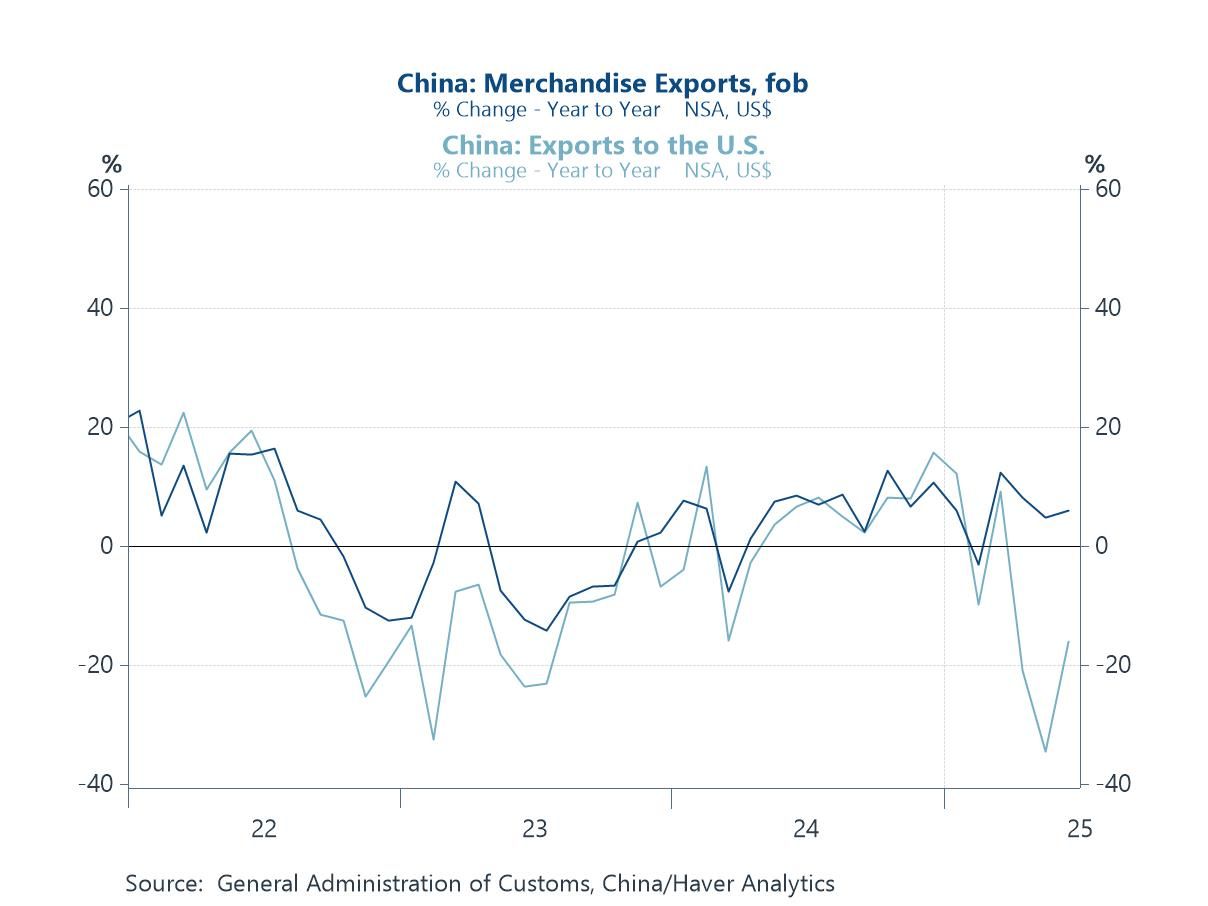

This week, we examine a series of major US trade and tariff developments since early July. The US has expanded its network of bilateral trade deals, including deals with Indonesia and the Philippines, both securing tariff rates of 19%. Meanwhile, former President Trump has seemingly raised the general tariff floor from 10% to 15%, potentially affecting countries like Australia, New Zealand, and Singapore (see chart 1). India, once expected to be among the first to reach a deal, has yet to finalize an agreement ahead of the August 1 deadline. Attention remains on China’s suspected use of transshipments through third countries to circumvent tariffs. One possible, though inconclusive, indicator is the decline in China’s direct exports to the US alongside stable overall export levels—suggesting either the use of transshipment routes or a broader redirection of exports to other markets (see chart 2).

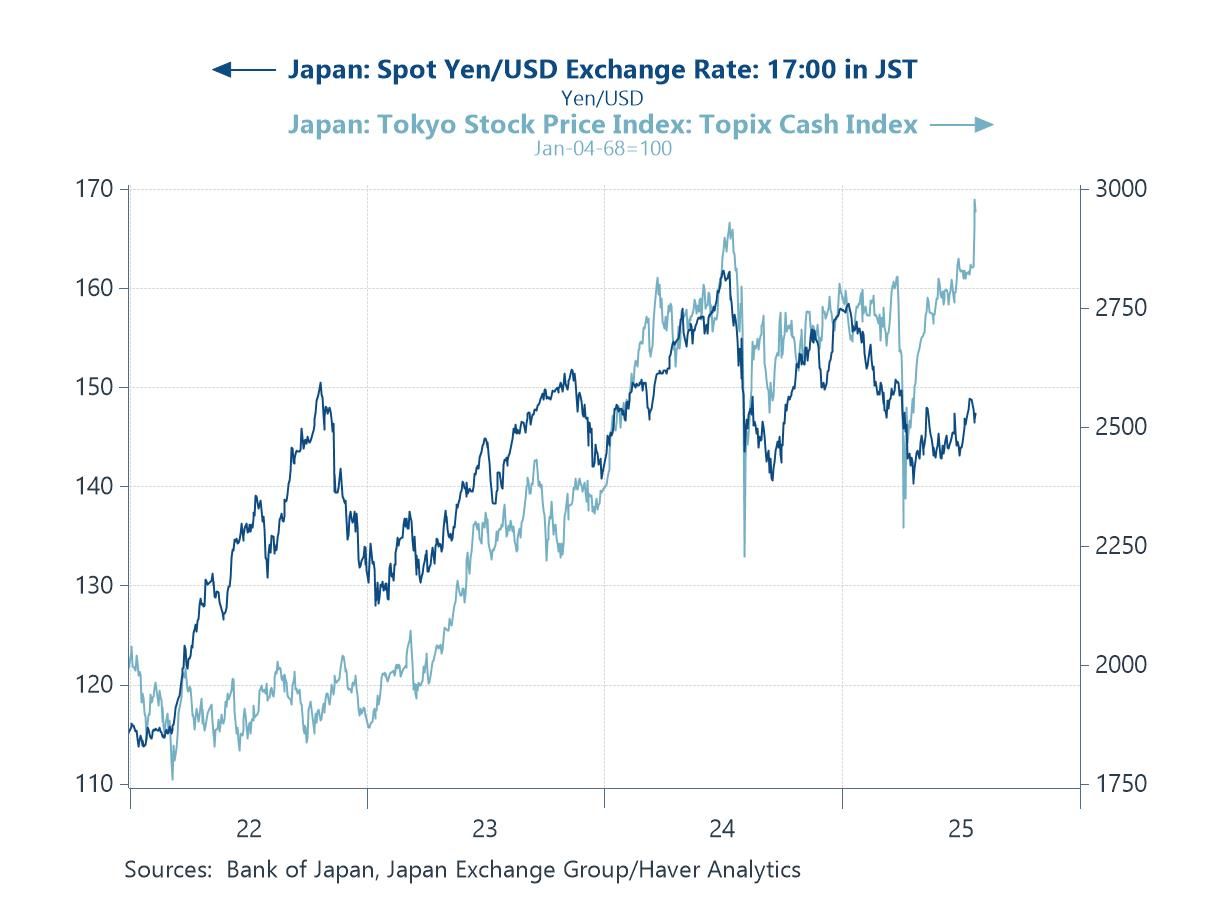

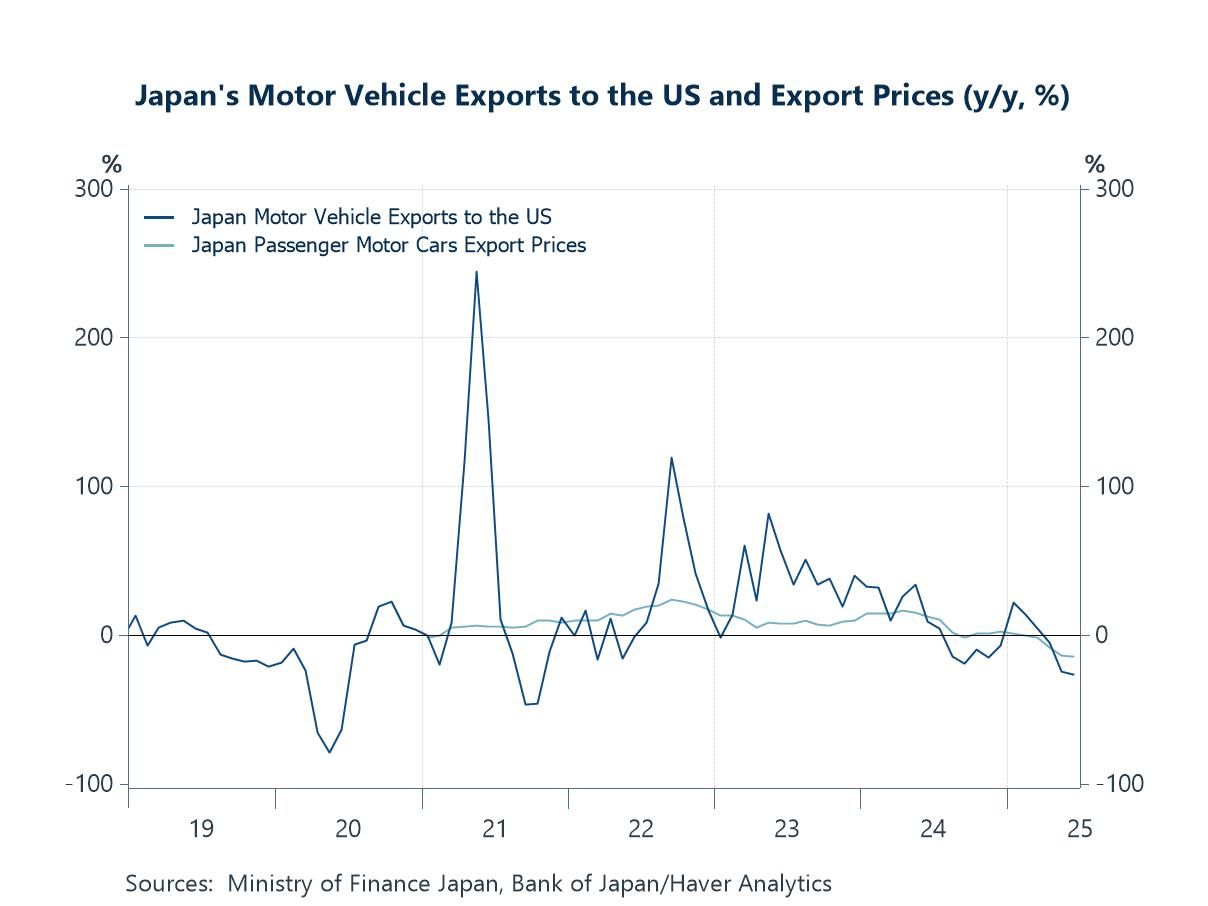

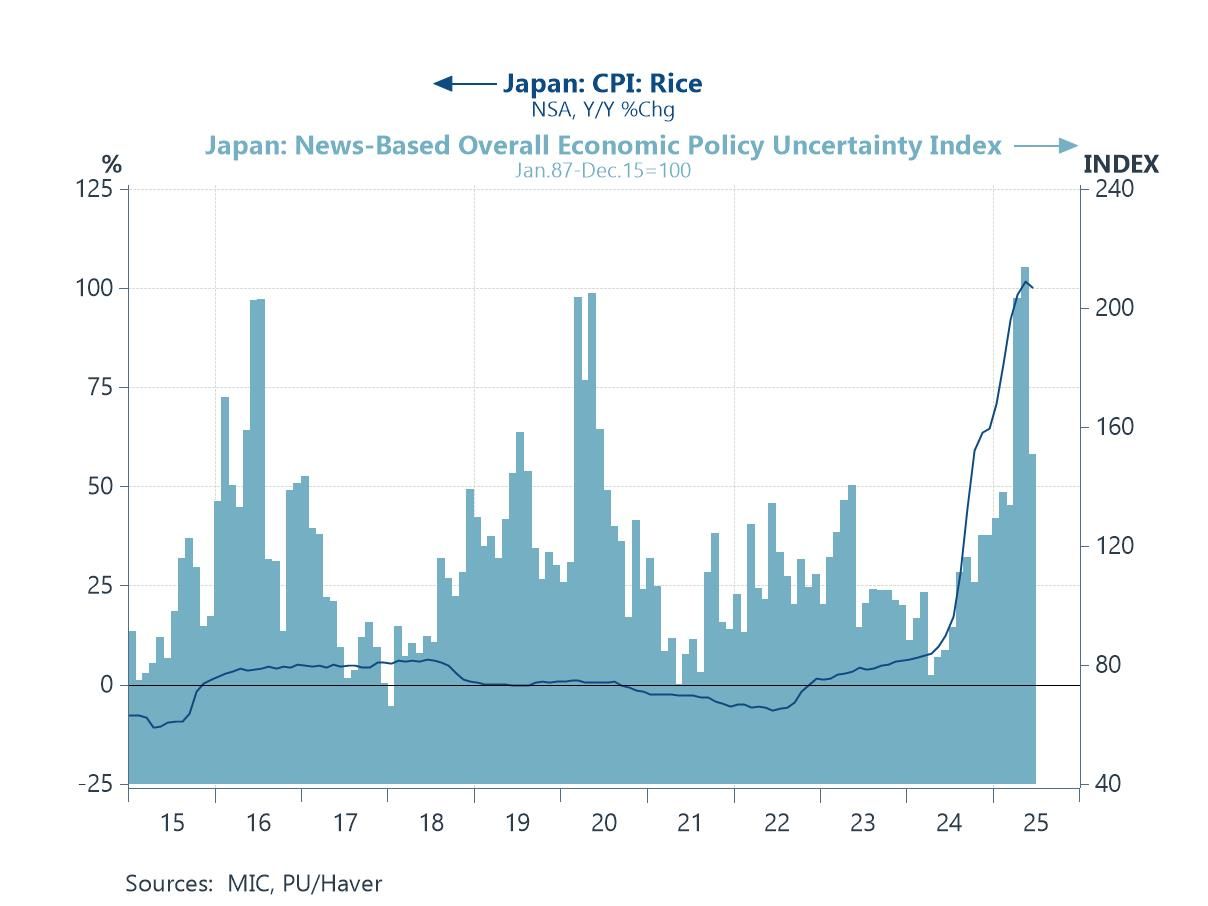

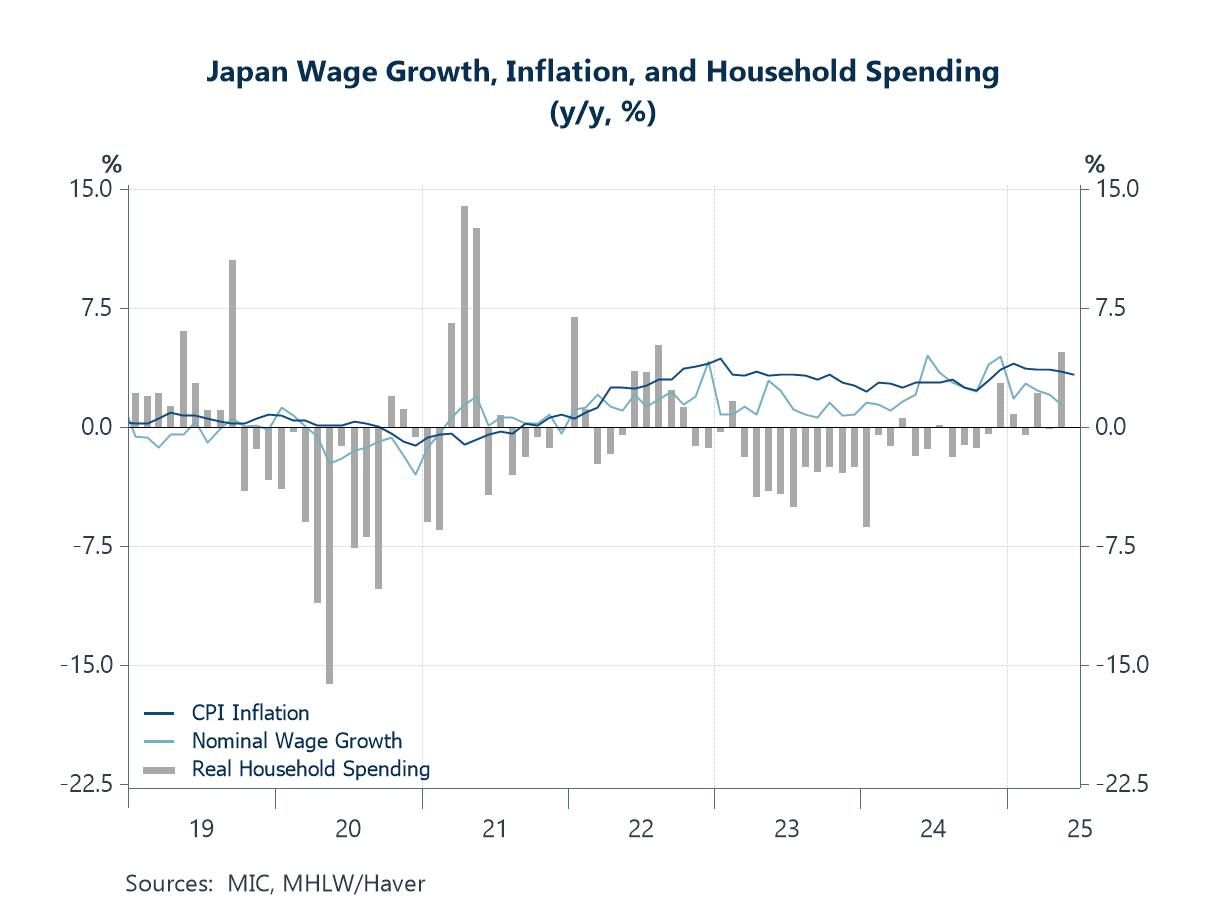

Japan also recently struck a significant deal with the US, reducing its reciprocal tariff from 24% to 15%. This announcement boosted Japanese equities and the yen (see chart 3). However, Japan’s auto exports to the US continue to decline, with firms absorbing tariff-related costs to maintain competitiveness (see chart 4). Despite political uncertainty following the ruling LDP’s losses in recent upper house elections, Japanese markets have remained resilient (see chart 5). As the Bank of Japan prepares to announce its next rate decision, real wages have posted their sharpest decline in two years, while household spending—driven by car purchases—has surged (see chart 6).

Latest US tariff developments Several significant US trade developments have occurred since early July. Notably, the number of bilateral trade deals secured by the US has increased. For instance, Indonesia reached an agreement that reduced tariffs from 32% to 19%, while the Philippines avoided a previously threatened 20% rate, settling instead at 19%. Meanwhile, former President Trump has reportedly raised the tariff floor from 10% to 15%. This suggests that countries previously facing the 10% rate—such as Australia, New Zealand, and Singapore (which runs a trade surplus with the US)—will now be subject to higher duties, as illustrated in chart 1. In contrast, India, once expected to be among the first to reach a deal, has yet to produce a substantive agreement as the August 1 deadline approaches.

Chart 1: US reciprocal tariffs

Among the ongoing discussions, a key talking point remains the US's continued concern over China’s use of transshipments through third countries to circumvent US tariffs. One Asian economy that has come under scrutiny is Vietnam. While Vietnam has secured a trade deal with the US—lowering its general tariff rate to 20%—the agreement includes a specific provision: “transshipments” of goods face a 40% tariff. As shown in chart 2, there are signs, though not confirmations, that such practices may be occurring. For example, while China’s direct exports to the US have been declining, its overall export growth has remained steady. This could suggest, among other causes, the use of transshipment routes or simply a rerouting of Chinese exports to other markets to sustain growth.

Chart 2: China’s exports and exports to the US

The US-Japan trade deal Japanese equities and the yen have surged following the announcement of the US–Japan trade deal (chart 3), which lowered Japan’s reciprocal tariff rate from an original 24% to 15%. In exchange, Japan has reportedly agreed to, among other terms, a $550 billion package of investments in, and loans to, the US. The country’s auto industry, which had previously faced a 27.5% tariff—due to the US’s 25% sectoral tariff and an existing 2.5% duty—also saw its rate reduced to 15%, likely to the great relief of Japanese carmakers. That said, while the new 15% rate marks a substantial drop from the earlier 24%, Japan remains worse off compared to the pre–Liberation Day baseline. As for the yen, it had already begun to strengthen prior to the deal’s announcement. Despite the ruling Liberal Democratic Party (LDP) suffering a notable loss in the recent upper house elections, the outcome appeared to fall within investor expectations, possibly triggering a round of precautionary yen selling beforehand. More on Japan’s elections will be covered in a later section.

Chart 3: Japanese equities and the yen

Japan’s auto industry Meanwhile, sectoral tariffs on key Japanese industries—particularly autos—continue to weigh on the country’s economic outlook. Many of Japan’s major car exporters have reportedly avoided raising prices significantly, choosing instead to absorb most of the cost from US auto tariffs, likely in an effort to maintain market share. However, gradual price increases may follow if automakers can no longer sustain these margins. As shown in chart 5, the value of Japan’s motor vehicle exports to the US has already declined sharply. This is likely due to manufacturers absorbing the tariff burden, a trend also reflected in Japan’s export price data. As such, the impact on Japanese automakers’ bottom lines is already becoming evident. That said, the production capacity of Japanese carmakers in the US—which many firms are actively working to expand—offers some relief from declining exports. Additionally, the recently announced reduction in US auto tariffs on Japan will likely alleviate, though not eliminate, the pressure on Japan’s auto industry.

Chart 4: Japan’s motor vehicle exports to the US and export prices

Japan’s upper house elections Japanese assets have rallied despite heightened policy uncertainty (chart 5), as the ruling Liberal Democratic Party (LDP) suffered a major setback in recent upper house elections, losing its majority along with coalition partner Komeito. This follows an earlier defeat in the October 2024 snap elections, when the LDP also lost its majority in the lower house. As a result, the coalition must now rely on support from opposition parties to pass legislation in both chambers—granting opposition groups, which hold diverse and often conflicting policy views, greater influence over future policymaking. The election results come amid mounting domestic challenges, particularly inflation, with rising rice prices drawing widespread concern. Speculation has intensified over whether Prime Minister Ishiba may resign, though he has consistently denied any such plans.

Chart 5: Japan rice inflation and economic policy uncertainty

The Bank of Japan Lastly, we turn to the Bank of Japan (BoJ), which is set to announce its interest rate decision this week. Markets broadly expect the BoJ to keep rates unchanged for now, with any further hikes likely deferred. This comes amid heightened political uncertainty following the ruling LDP’s significant defeat in the recent upper house elections, casting fresh doubt on Prime Minister Ishiba’s leadership. The BoJ’s path toward further policy normalisation is also being complicated by weakening wage growth. Earlier momentum has faded, with nominal wages rising just 1.4% year-on-year in May, as shown in chart 6. Combined with still-elevated inflation, real wages posted their sharpest decline in two years during the month. Nonetheless, household spending saw a notable surge in May. However, this was largely driven by car purchases, which benefited from low base effects due to safety-related scandals a year earlier.

Chart 6: Japan’s wage growth, inflation, and household spending

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief