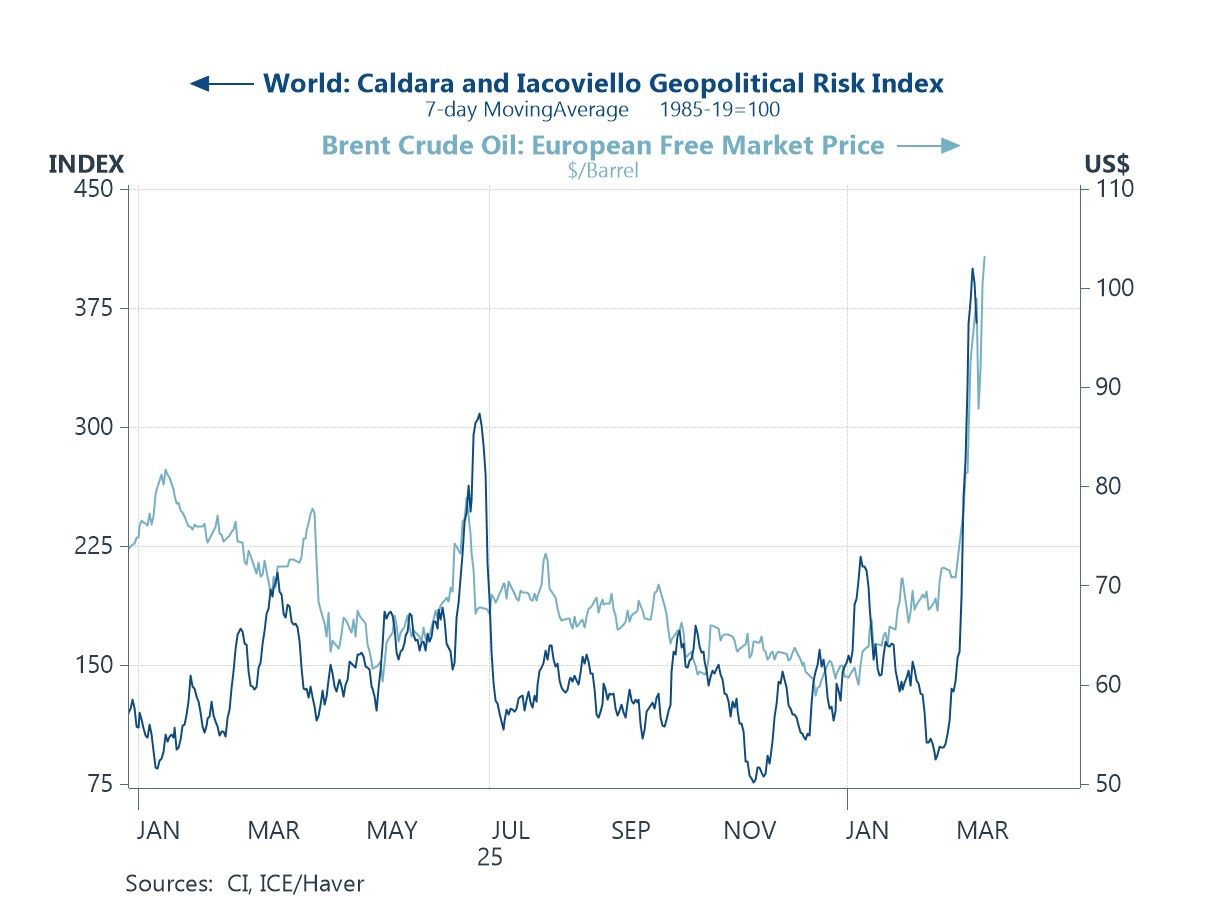

Asia

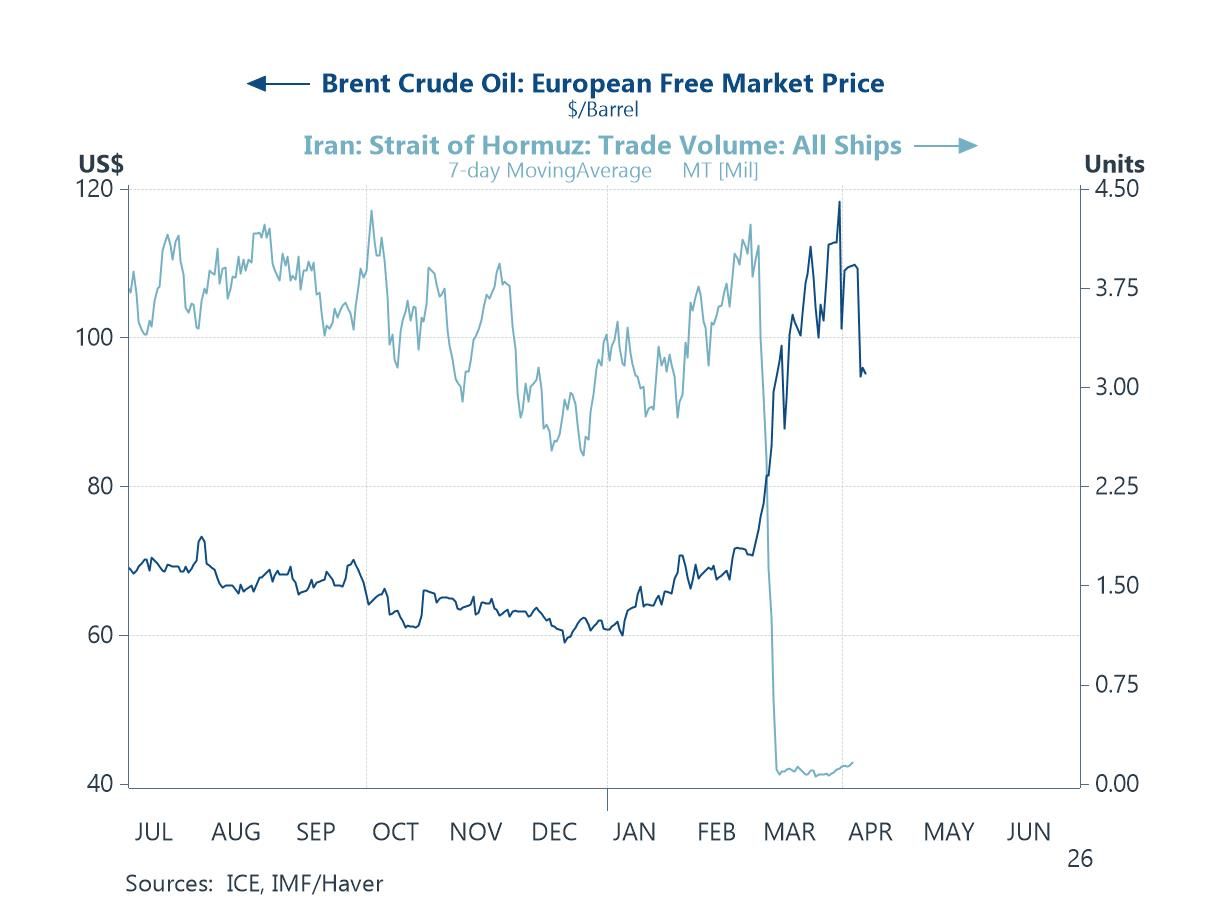

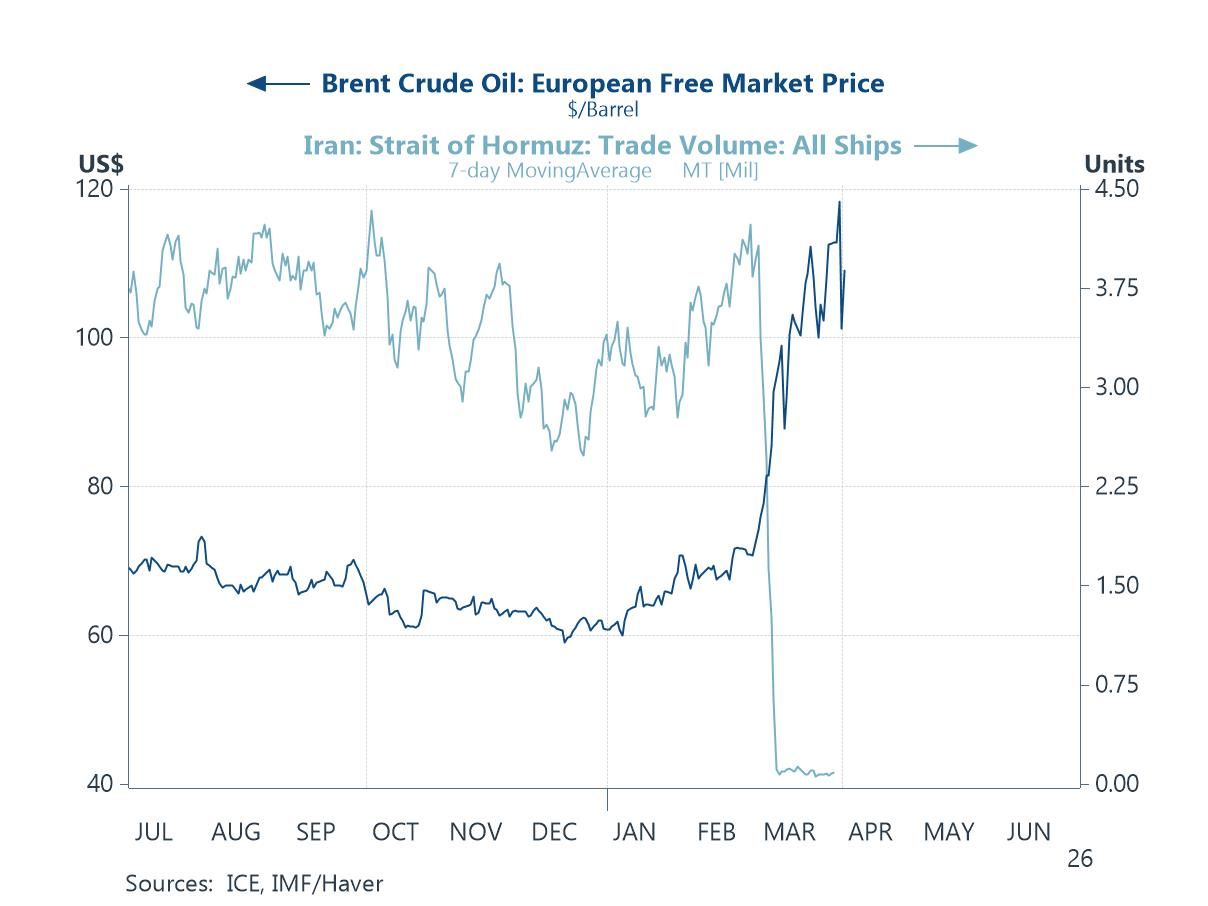

AsiaIn this week’s Letter, we cover the latest developments and implications of the Middle East conflict for Asia, while also making space for other important themes, including artificial intelligence (AI). The Middle East conflict remains in a no deal state coming out of the weekend, though some early Monday optimism emerged in Asian markets following Iran’s reported offer to reopen the Strait of Hormuz (chart 1). Nonetheless, as the Strait closure drags on, so too do the fiscal costs of domestic fossil fuel subsidies across Asia, which have been shown to move closely with crude oil prices (chart 2). While such measures offer direct relief by cushioning household energy costs, they remain difficult to sustain over the long haul.

Over the week, we also saw a further fraying in regional monetary policy trends, with the Philippines hiking its policy rate for the first time in about two years amid inflation concerns, while Indonesia stood pat on rates (chart 3). Investor attention is likely to remain fixed on monetary policy this week, with the Bank of Japan due to decide on policy. Expectations for an April hike have faded amid the persistent Middle East conflict, though yen weakness continues to present a source of concern (chart 4). The week also brings China’s latest PMI readings (chart 5), adding to the recent run of hard data accompanying the Q1 GDP release.

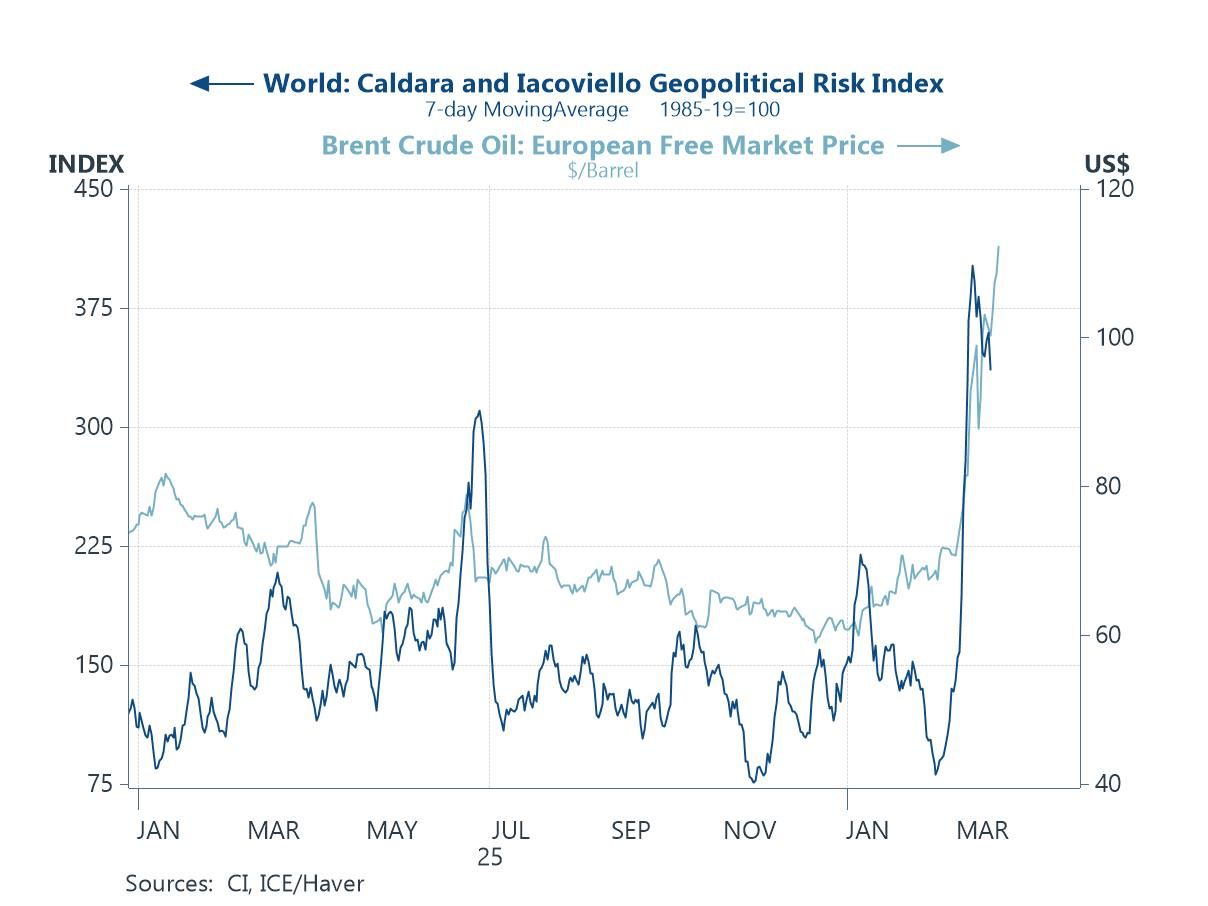

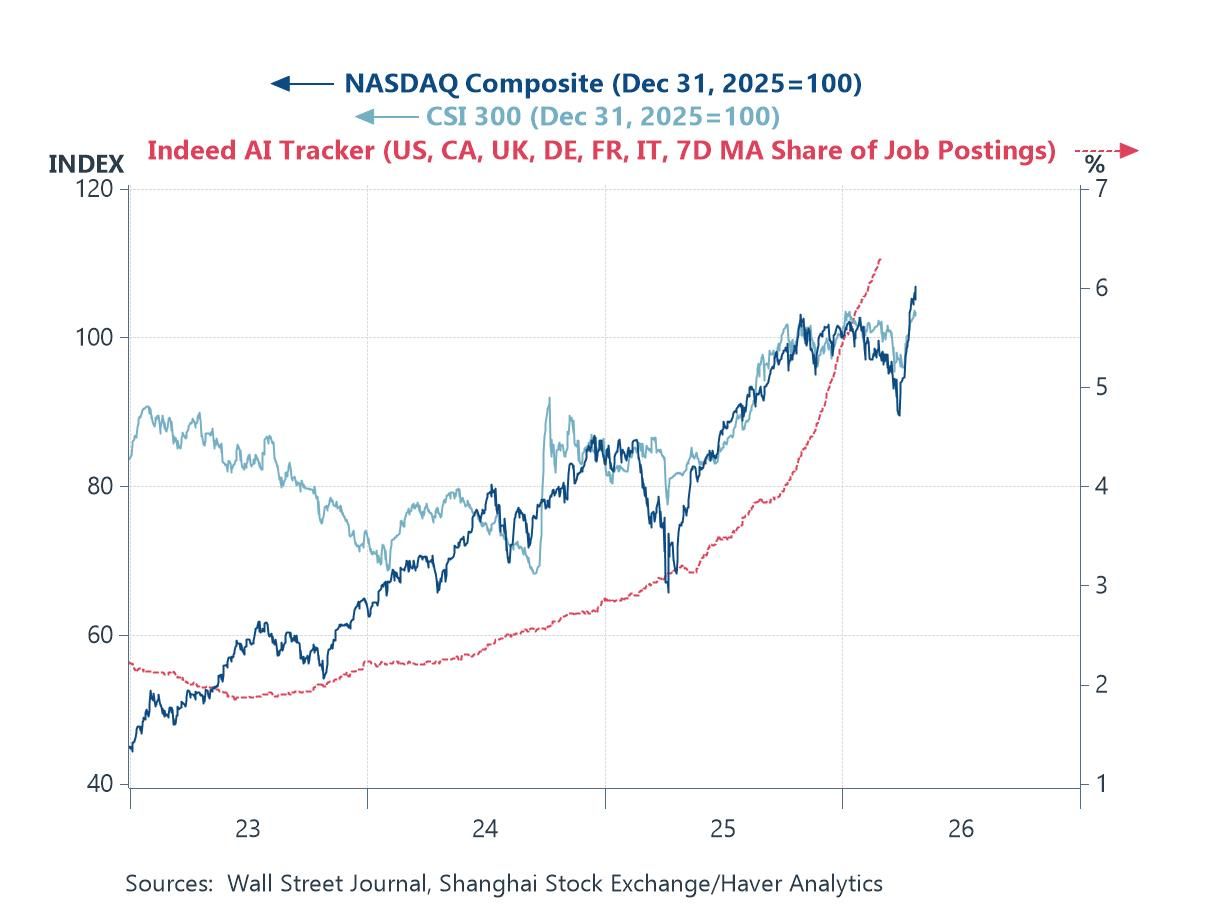

Beyond the Middle East conflict, the evolution of AI continues to demand close attention. Before geopolitical tensions took centre stage, AI was the dominant market narrative — and that enthusiasm has hardly faded. If anything, recent developments suggest the story is broadening: use cases are expanding, scalability is improving, and access is widening beyond large corporates to the mass market — increasingly spilling into the realm of physical AI. It may well be this persistent wave of optimism that is helping to underpin equity valuations, even as the geopolitical backdrop darkens (chart 6).

The Middle East conflict About two months in, we remain stuck in the limbo of the US-Iran conflict, which has left the Strait of Hormuz largely closed and much of the world starved of the critical oil flows needed to power the global economy. The back and forth between the US and Iran has persisted in recent weeks, with both sides again failing to reach a peace deal over the weekend, though Monday’s news of Iran offering to reopen the Strait has revived some hope in markets. In truth, commodity and market valuations do not hinge so much on a peace deal itself, but rather on the resumption of oil flows through the Strait, something that could materialise even in the absence of a formal deal, though any agreement that includes and credibly delivers such a reopening would likely be warmly received by markets. Until then, market gyrations are likely to persist, with prices fluctuating in response to each new snippet of news. And until then, the world will continue both to be starved of, while gradually adapting to, the drip feed of oil flows emerging from the Strait.