Asia| Aug 04 2025

Asia| Aug 04 2025Economic Letter from Asia: New Duty Roster

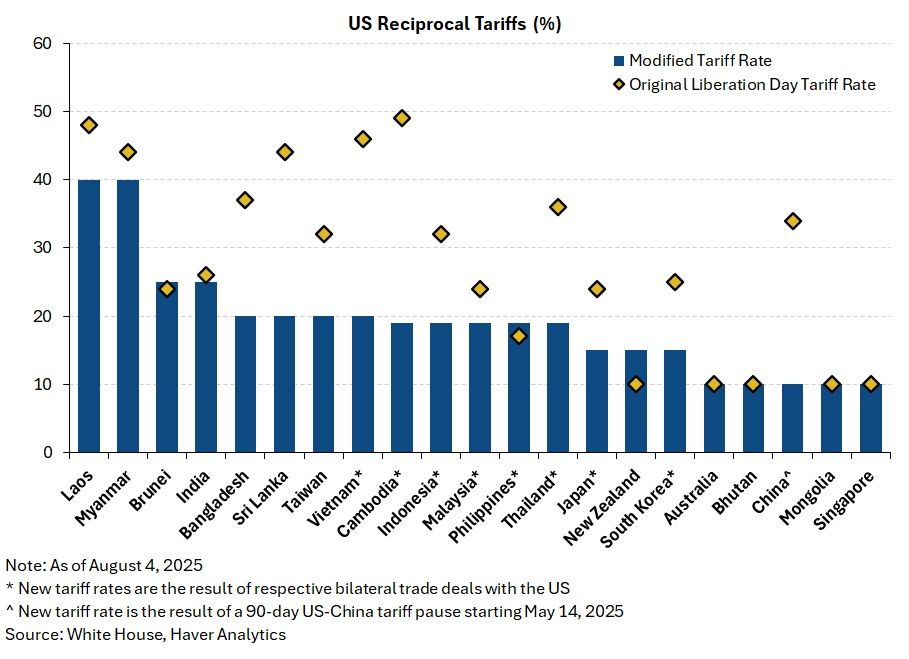

This week, we examine the latest wave of trade developments across Asia as the US unveiled a full list of its modified reciprocal tariff rates, set to take effect on August 7. As anticipated, many of the updated rates are now lower than the original tariffs, with Cambodia and Vietnam seeing the sharpest reductions (chart 1). However, from peak tariff levels, China stands out—continuing to benefit from a 10% pause rate, down from triple-digit highs.

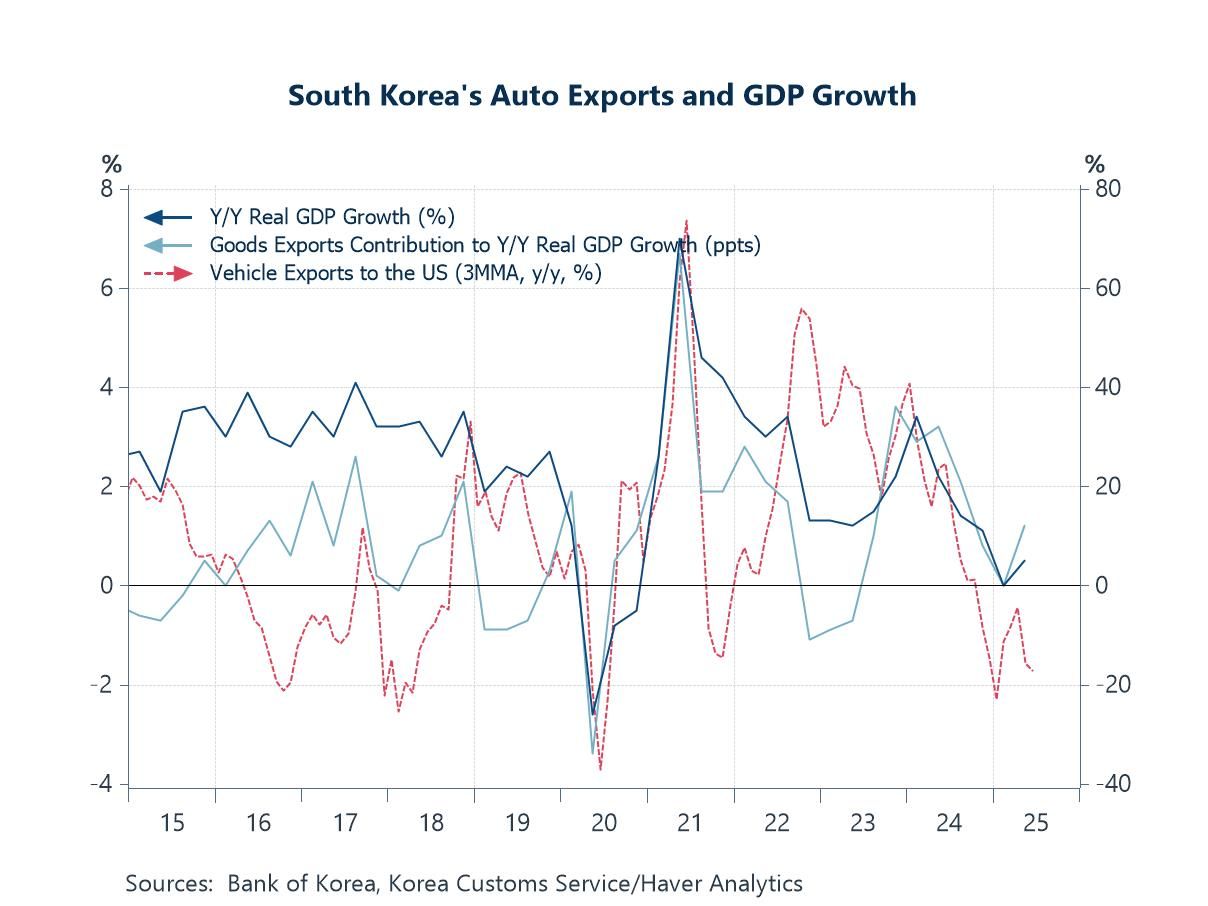

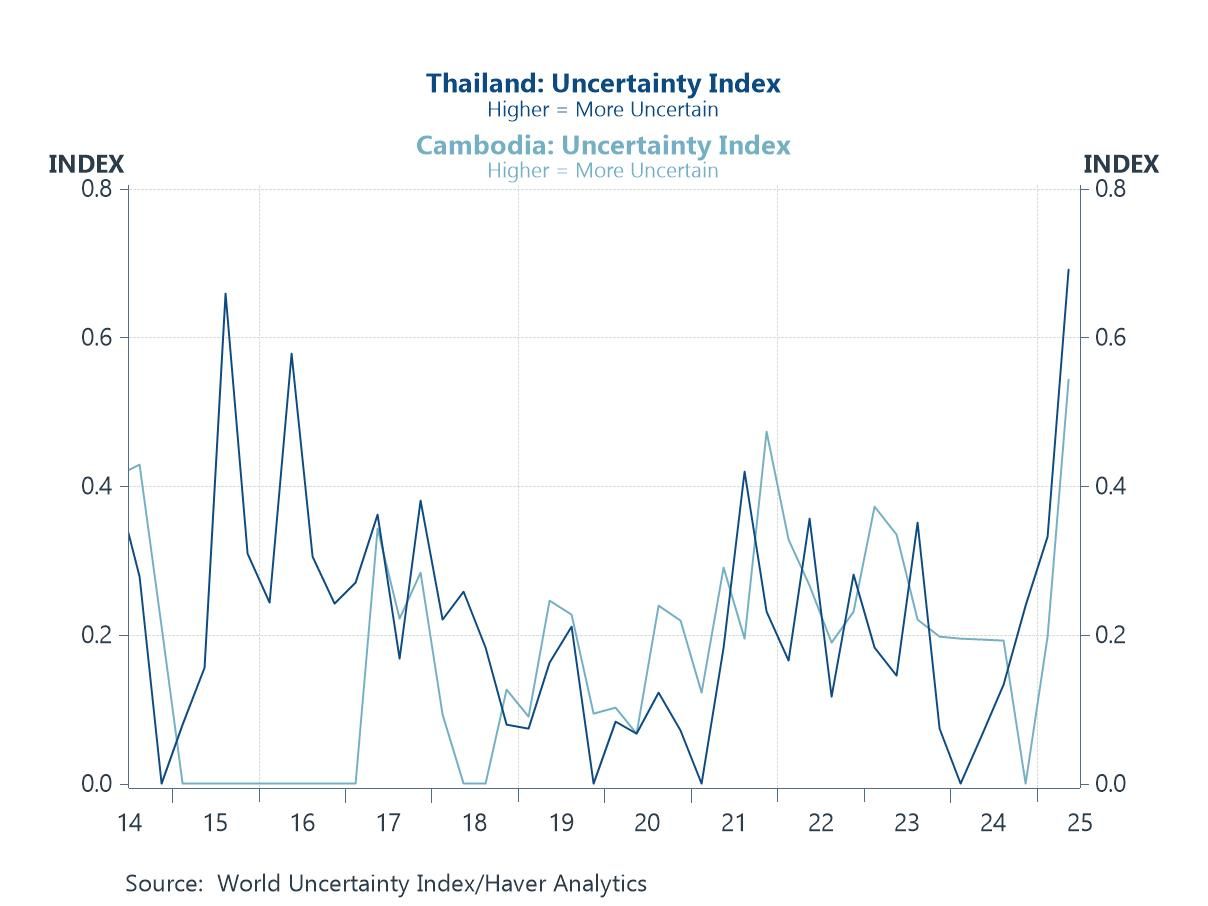

South Korea secured a deal just before the deadline, lowering its tariff from 25% to 15%. The new rate also applies to auto exports, offering relief to Korean automakers (chart 2). Thailand and Cambodia followed with US trade agreements after agreeing to an unconditional ceasefire following earlier military clashes. Their US-imposed tariffs dropped from 36% to 19%, highlighting how US trade policy can intersect with geopolitical interests and, in this case, may help reduce trade uncertainty (chart 3).

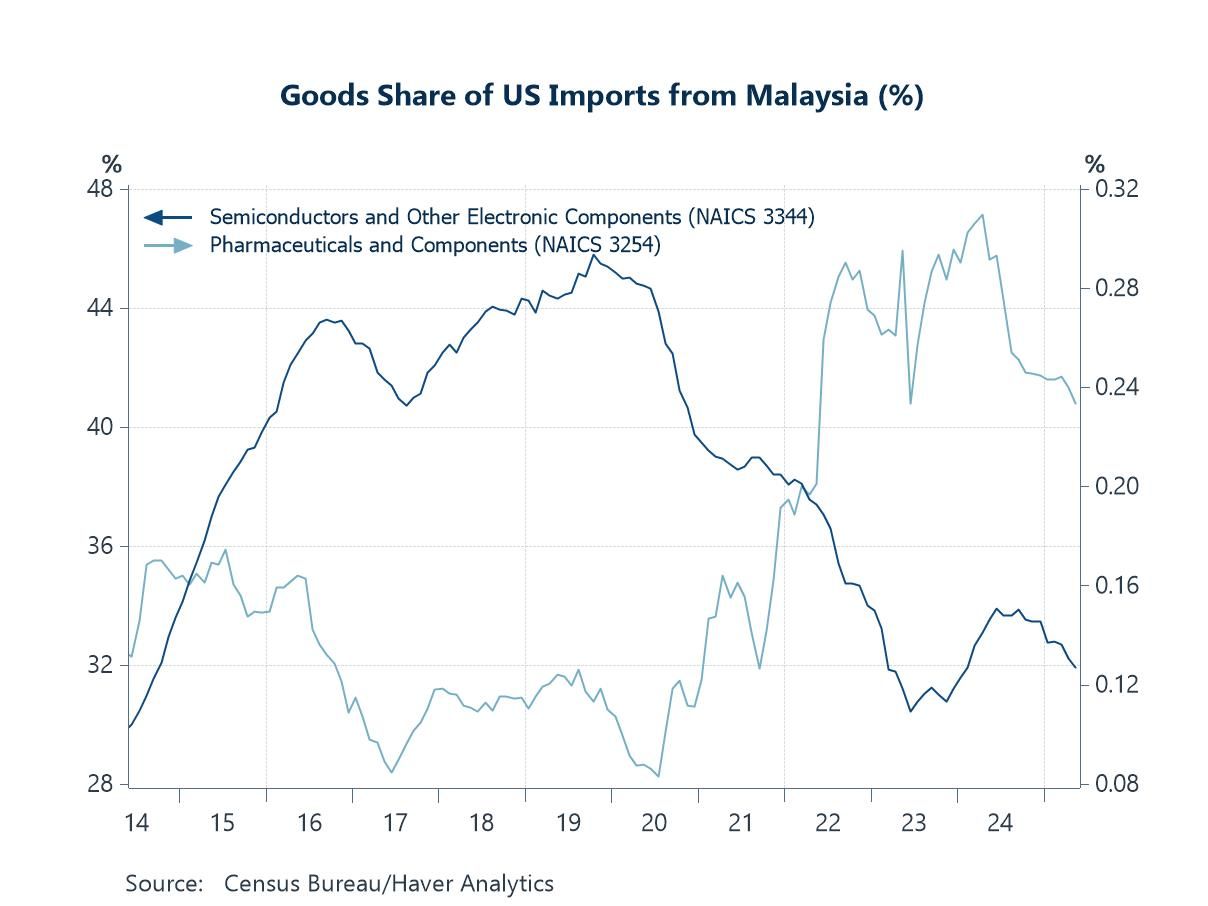

Malaysia, a key mediator in the ceasefire, also finalized a trade deal, reducing its tariff rate to 19% and gaining exemptions on key exports such as semiconductors (chart 4). Turning to Japan, while its US trade deal helped avert immediate tensions, the vague terms and a headline $550 billion investment—mostly in the form of loans—leave room for future friction (chart 5). China, however, remains a wildcard. Talks to extend its tariff pause are ongoing, but failure could see a return to extreme tariff levels (chart 6). Meanwhile, tech tensions linger, despite eased restrictions on Nvidia AI chip exports.

Latest US tariff developments We gained further clarity on the new reciprocal tariff rates announced by the US administration last week, as the White House released a full list of the modified rates on Thursday. It also announced that the new rates will take effect on August 7, giving partner countries a bit more time to negotiate new terms. Overall, as earlier indications suggested, Trump’s post-pause tariff rates—regardless of whether trade deals were secured—have often ended up lower than the original rates, as shown in chart 1. The largest reductions from original tariff levels have so far come from Cambodia and Vietnam. However, when looking at the steepest reductions from peak tariff rates, China stands out. It continues to benefit from a 10% tariff pause—down sharply from the triple-digit rates imposed at the height of US-China trade tensions earlier this year. On the flipside, a handful of economies—including New Zealand, the Philippines, and Brunei—are now facing modified tariff rates that are actually higher than their original Liberation Day levels. Notably, the Philippines ended up in this group despite having secured a trade deal with the US.

Chart 1: Modified vs. original US reciprocal tariffs

South Korea As for South Korea, the US reduced its tariff rate to 15% just ahead of the August 1 deadline, a significant drop from the original Liberation Day rate of 25%. In return, South Korea committed to, among other terms, $350 billion in investments into the US. Of that total, $150 billion will go specifically toward shipbuilding cooperation—supporting the entry of Korean firms into the US shipbuilding industry—while the remaining $200 billion will be directed toward semiconductors and other sectors. Similar to Japan’s arrangement, the new 15% tariff rate will also apply to South Korean auto exports, likely providing relief to the country’s automakers. As shown in chart 2, South Korea’s vehicle exports—and, by extension, its export-driven growth—have come under pressure, with more recent headwinds stemming from the broad 25% auto tariffs imposed by the US. Notably, South Korea’s dealmaking pace with the US has been considered exceptionally swift, especially given that the country had only recently undergone an administrative transition following its presidential elections, leaving limited time to initiate formal trade negotiations.

Chart 2: South Korea vehicle exports to the US and GDP growth

Thailand and Cambodia Moving to other parts of Asia, one of the more notable developments last week was the signing of two additional US trade deals—specifically with Thailand and Cambodia. The two countries had recently been engaged in escalating border clashes but agreed to an unconditional ceasefire after mediation by Malaysia and the US. In reality, tensions between Thailand and Cambodia had been simmering for some time, likely driving in part the heightened uncertainty shown in chart 3, though other factors may have played a role. Notably, US President Trump stated that he had made it clear to both governments that no trade deal would be considered while they remained in conflict—an ultimatum that may have incentivized both sides to pursue de-escalation. Ultimately, US trade deals with both countries were announced, reducing their tariff rates from the original Liberation Day level of 36% to 19%. This illustrates how the US approach to dealmaking goes beyond trade, sometimes factoring in broader geopolitical considerations as well.

Chart 3: Thailand and Cambodia uncertainty index

Malaysia Touching further on Malaysia, which played a key role in mediating the Thailand-Cambodia conflict mentioned earlier, a last-minute US-Malaysia trade deal also materialized shortly after the agreements with Thailand and Cambodia were hinted at. Under the new terms, Malaysia’s tariff rate was reduced to 19%, down from the original 24%. Malaysian Trade Minister Zafrul described the deal as a “win-win,” noting that Malaysia has either reduced or eliminated tariffs on nearly all American products. Notably—and perhaps offering some interim relief—Malaysia also secured tariff exemptions for its exports of semiconductors and pharmaceuticals. This is especially significant, as semiconductor exports account for a substantial share of Malaysia’s shipments to the US, as shown in chart 4.

Chart 4: Goods share of US imports from Malaysia

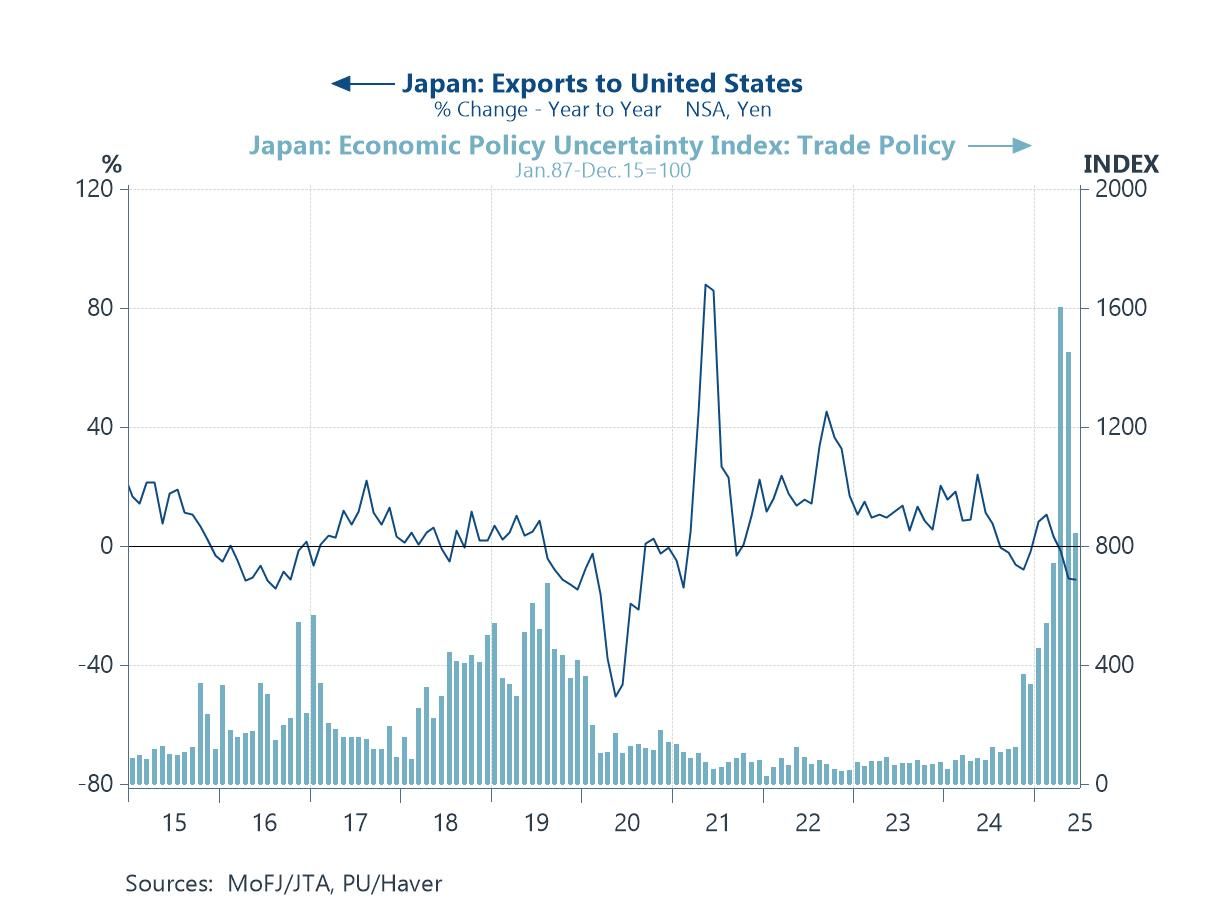

Japan Turning to Japan, the recent US-Japan trade deal appears to have averted the worst for now. However, many key details remain unclear, particularly regarding Japan’s reported $550 billion investment into the US. While the headline figure is striking, Japan’s chief trade negotiator, Akazawa, later clarified that only 1–2% of the amount would constitute actual investment, with the remainder largely consisting of loans. More critically, the deal—like several other recent US-Asia trade agreements—was not accompanied by formal documentation, leaving its terms vague and, perhaps more concerning, open to future revision. These loose ends present ongoing risks to US-Japan economic relations and could potentially unwind recent market gains driven by trade optimism, as uncertainty remains and may yet resurface (see chart 5). This lingering uncertainty likely contributed to the Bank of Japan’s decision to hold its policy rate steady last week. The central bank adopted a wait-and-see approach before considering further rate hikes, while notably revising its inflation forecasts upward and presenting a slightly improved growth outlook for the fiscal year.

Chart 5: Japan exports to the US and trade policy uncertainty

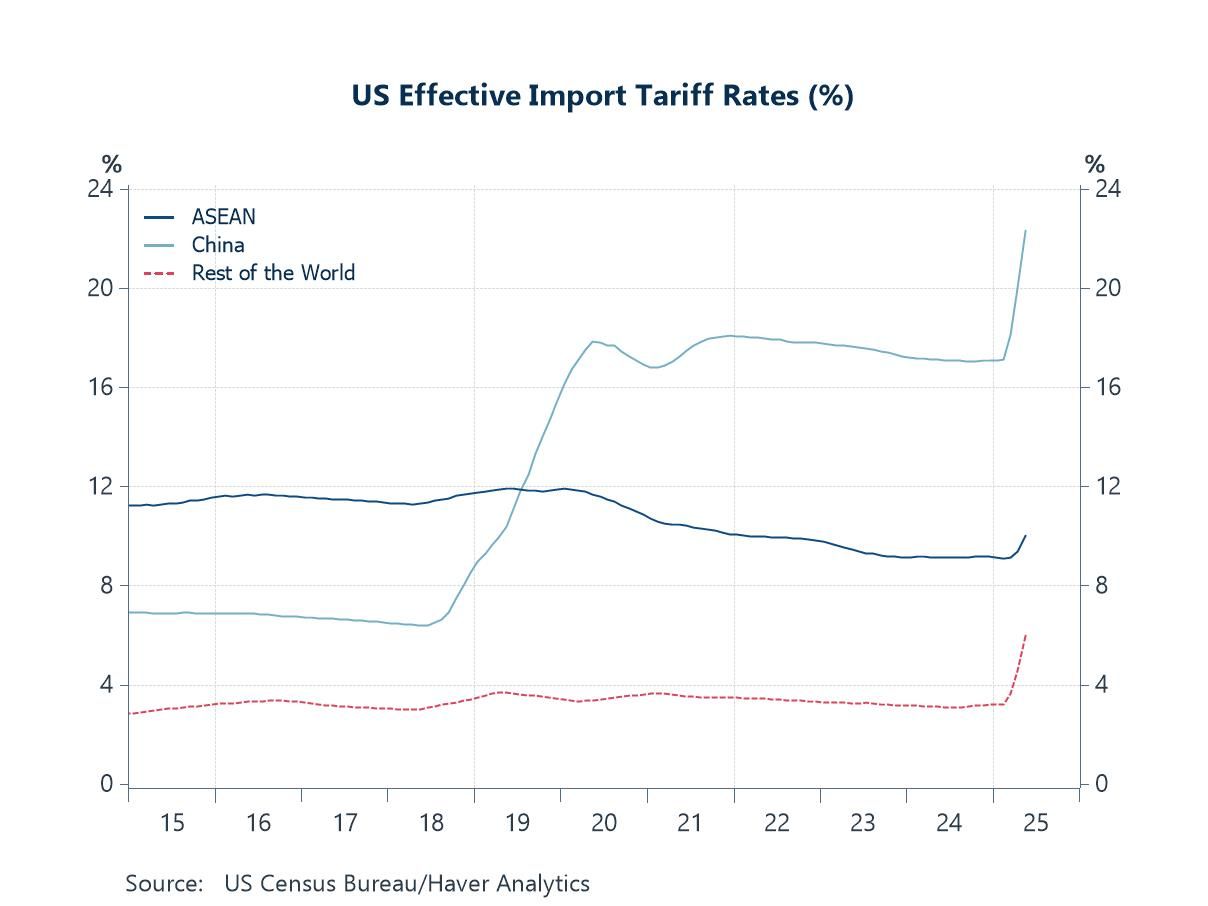

China Amid the recent flurry of US trade deals, one critical issue that may have slipped from the spotlight—but remains central to the global outlook —is China. Ongoing discussions between the two countries aim to extend China’s current tariff pause. If talks break down, US Treasury Secretary Scott Bessent has warned that the existing 10% tariff on Chinese exports could “boomerang” back to its previously exorbitant levels. This could potentially drive the US effective import tariff rate on China well above its already-elevated levels, as shown in chart 6. Meanwhile, the recent reversal of export restrictions by the US on Nvidia’s H20 AI chips may have brought temporary relief to China’s AI sector. However, Chinese authorities have raised national security concerns over the chips’ built-in tracking features and potential remote shutdown capabilities—adding yet another layer of complexity to the already tense US-China trade relationship and broader economic rivalry.

Chart 6: US effective import tariff rates

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief