Global| Nov 13 2025

Global| Nov 13 2025Charts of the Week: The Year in Review

by:Andrew Cates

|in:Economy in Brief

Summary

The global economic story of 2025 has been one of resilience amid disruption. Despite a succession of shocks — from a renewed U.S.–China trade confrontation and elevated geopolitical risks, to a sharp rise in fiscal activism and the energy-intensive AI investment boom — the world economy has held up better than many feared. Activity data have consistently surprised on the upside, supporting buoyant equity markets and keeping volatility contained. Meanwhile, inflation has continued to ease and central banks have cautiously shifted toward easier policy, even as large government deficits have kept longer-term real yields elevated. At the same time, US tariff policies have re-emerged as a defining force in global trade, with steep new duties on Chinese, Canadian, and Mexican goods disrupting supply chains and prompting renewed fragmentation in world commerce. These measures have cooled bilateral trade flows and added another layer of uncertainty to an already unsettled policy environment. Yet uncertainty itself remains the dominant feature of 2025 — geopolitical tension, technological exuberance, and diverging fiscal and monetary paths have left investors navigating a world where optimism and fragility coexist.

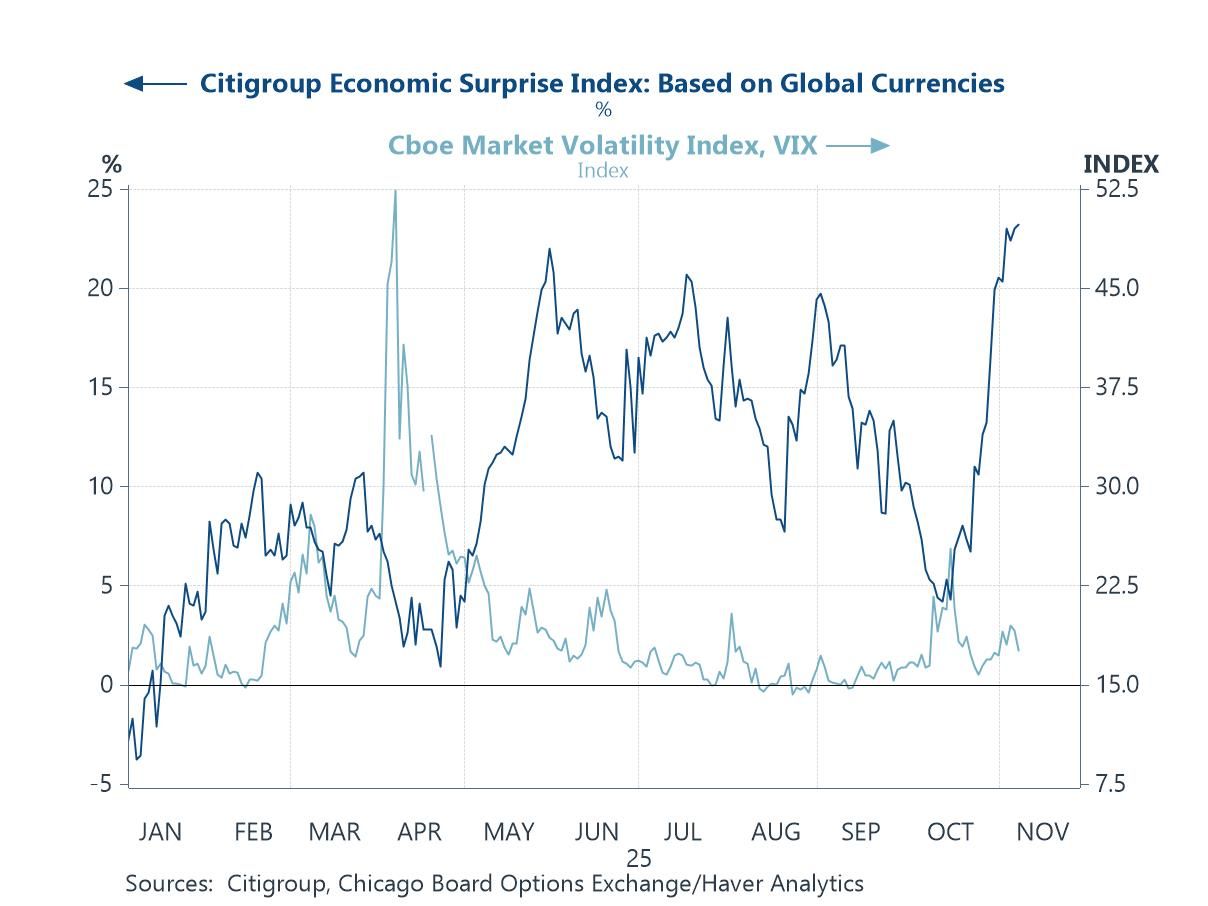

Upbeat investors Despite a year marked by major headwinds — from renewed US tariffs and persistent geopolitical strains to shifting interest-rate expectations — incoming global economic data have consistently outperformed forecasters’ expectations. The Citigroup Economic Surprise Index has remained in positive territory for most of 2025, indicating that growth, labour, and spending indicators have been “less bad” or outright stronger than consensus predicted. That resilience has helped to underpin market sentiment: while bouts of concern have occasionally lifted the Cboe Volatility Index (VIX), volatility has stayed relatively subdued, and equity markets have remained buoyant. In effect, 2025 has been a year in which the real economy has quietly outpaced the gloom, keeping risk appetite supported even as the macro narrative remained fraught with shocks and uncertainty.

Chart 1: Citigroup’s global growth surprise index versus the US VIX index

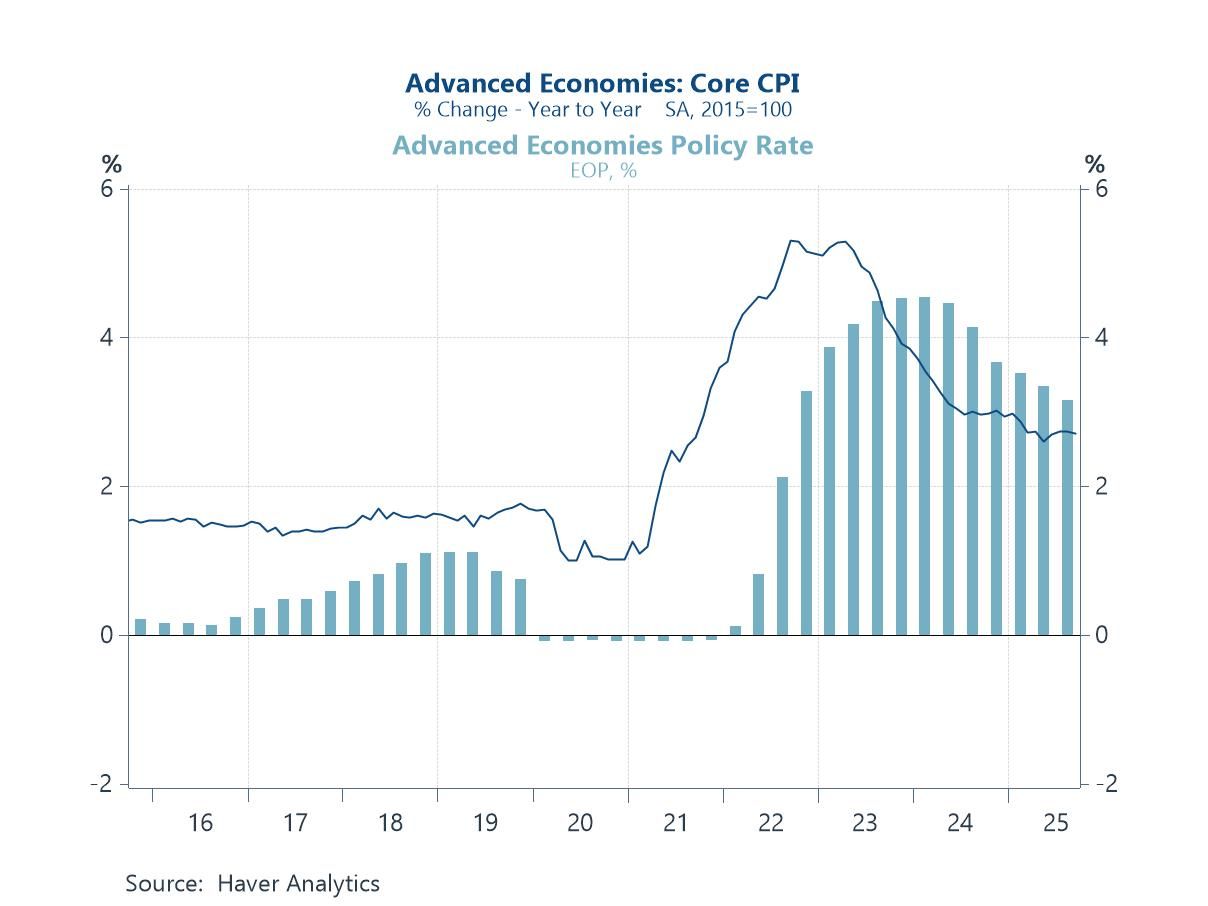

Less restriction from monetary policy Another key source of support for investors through 2025 has been the steady easing in both inflation and monetary policy across the major advanced economies. Core CPI has continued to trend lower from its 2022–23 highs, reflecting softer goods prices, moderating wage growth, and the lagged effects of tighter policy. With inflation now back within sight of central bank targets, policy rates have been edging down for the first time in several years. That shift has eased financial conditions, lowered real borrowing costs, and helped sustain asset valuations even as growth expectations have moderated. In effect, 2025 has marked the transition from a phase of inflation anxiety and policy restraint to one of gentle disinflation and tentative monetary normalisation—an environment that has kept liquidity abundant and risk assets well supported.

Chart 2: Average policy rates in advanced economies versus average rates of core CPI inflation

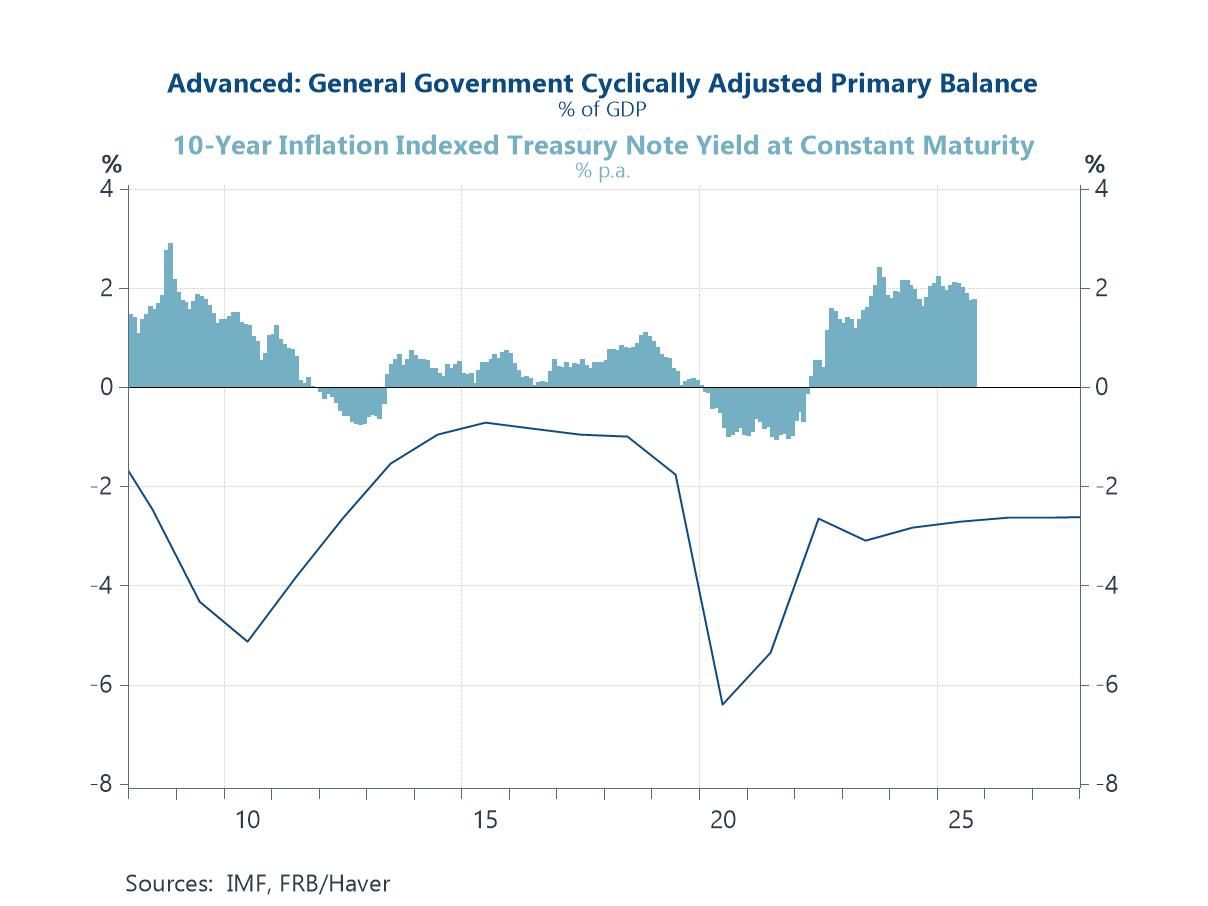

A thrust from fiscal policy A further policy tailwind in 2025 has come from the fiscal side, where governments in the major advanced economies have largely resisted meaningful consolidation despite earlier pledges to rebuild buffers. Across the US, Europe, and Japan, the cyclically adjusted primary balance remains firmly expansionary, helping to sustain demand at a time when private investment and trade have softened. In the United States, spending linked to industrial policy, energy transition, and defence has continued to underpin activity; in Europe, fiscal policy has remained loose as governments balance social pressures and investment needs; and in Japan, the new prime minister has signalled further stimulus to support household income and productivity growth. Yet this persistent fiscal support has also had a side effect: it has kept longer-term real yields unusually elevated, reflecting both heavy sovereign issuance and investor recognition that governments are still running structural deficits even in a low-growth environment. In other words, fiscal policy has been a crucial prop for near-term growth—but also one reason why the “new normal” for real yields now looks higher than in the pre-pandemic decade.

Chart 3: Advanced economies’cyclically adjusted budget balance versus US 10-year real yield

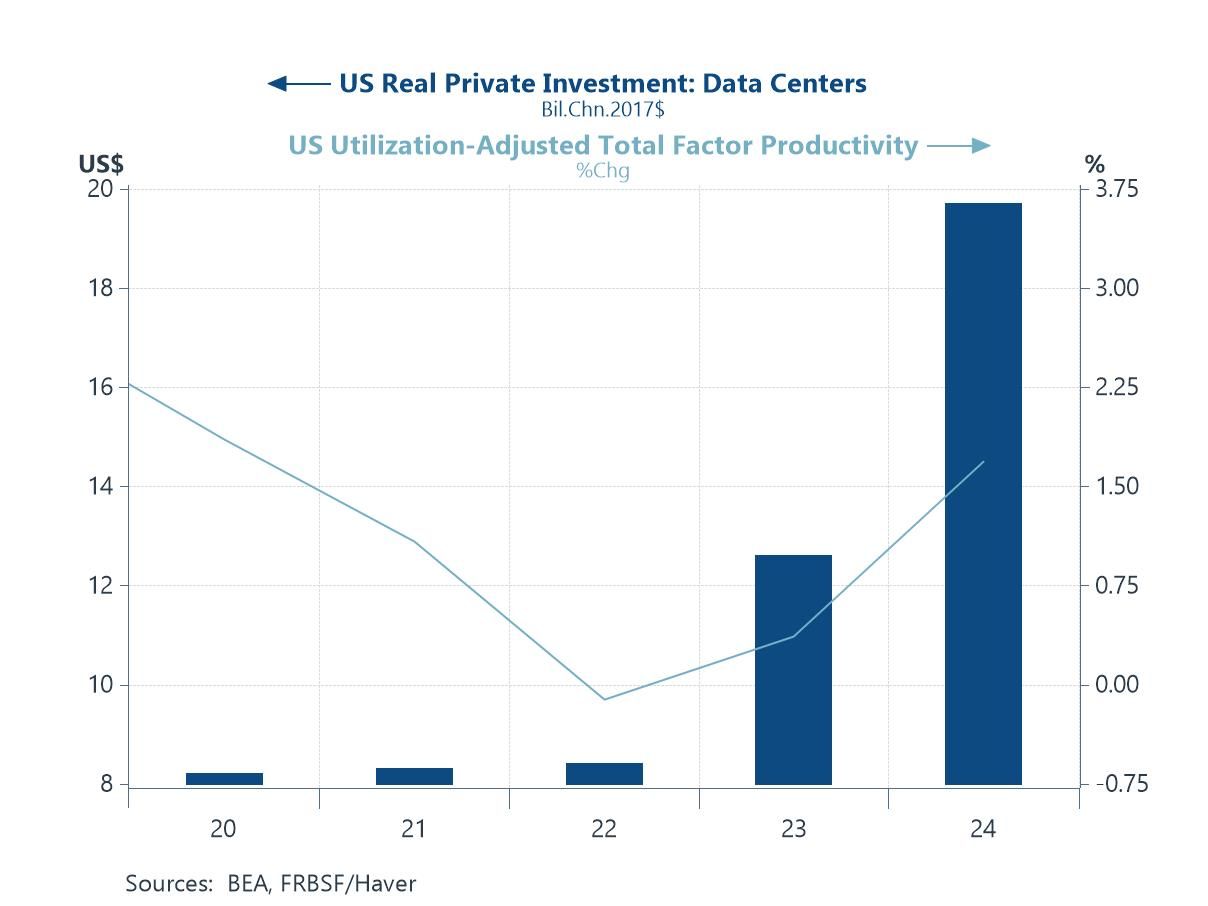

The AI Boom One of the defining features of 2025 has been the AI investment boom, centred on the extraordinary surge in spending on US data centres and digital infrastructure. Real private investment in this sector has soared to record highs as firms race to expand computing capacity, driven by optimism about artificial intelligence and its potential to transform productivity. The pickup in utilisation-adjusted total factor productivity suggests that some efficiency gains may already be materialising, though it remains too early to tell whether these effects will endure. Investors have largely welcomed this capital deepening as a sign of renewed US dynamism, but it also carries familiar late-cycle risks — from valuation bubbles in AI-related equities to mounting energy demands and strain on power grids. The key question for 2026 and beyond is whether this unprecedented capex wave will deliver the sustained productivity lift needed to justify its scale, or whether it proves another costly technological exuberance.

Chart 4: US investment in data centres versus the SF Fed’s estimates of TFP growth

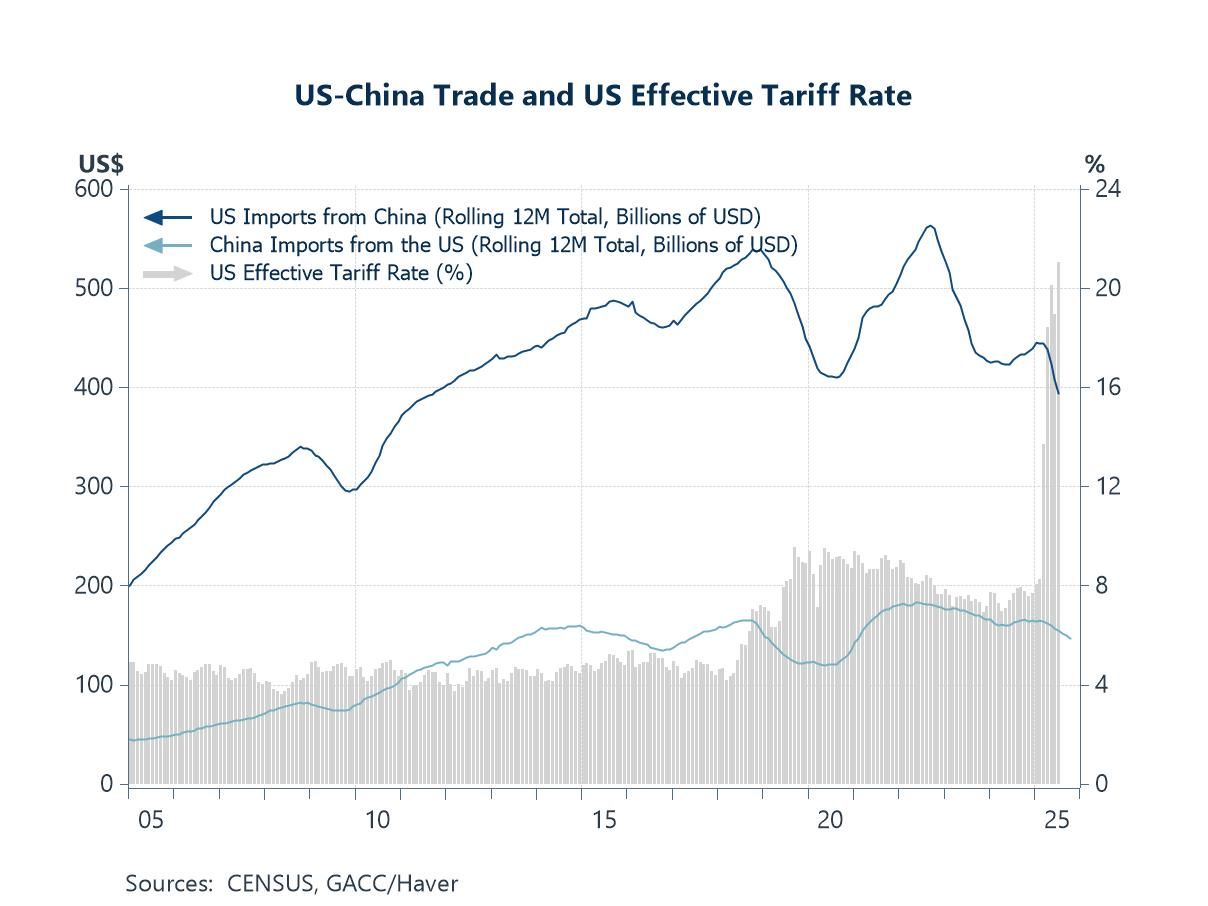

Global trade fragmentation Global trade came under renewed strain in 2025 as President Trump moved quickly in his second term to escalate tariff actions against China and several key trading partners. The US effective tariff rate has surged from below 8% at the end of 2024 to around 21% by mid-2025, marking the most aggressive trade tightening since the late 2010s. The back-and-forth imposition of tariff and non-tariff barriers between Washington and Beijing has led to a sharp pullback in bilateral trade flows, with US imports from China falling markedly and Chinese imports from the US also sliding. The broader ripple effects have been significant: global supply chains are once again being re-routed, firms are diversifying production toward third-country hubs, and world trade growth has slowed. This latest round of protectionism has reinforced the trend toward strategic fragmentation — a more regional, politically filtered form of globalisation — that continues to reshape the post-pandemic trading landscape.

Chart 5: US Effective Tariff rate versus US/China import flows

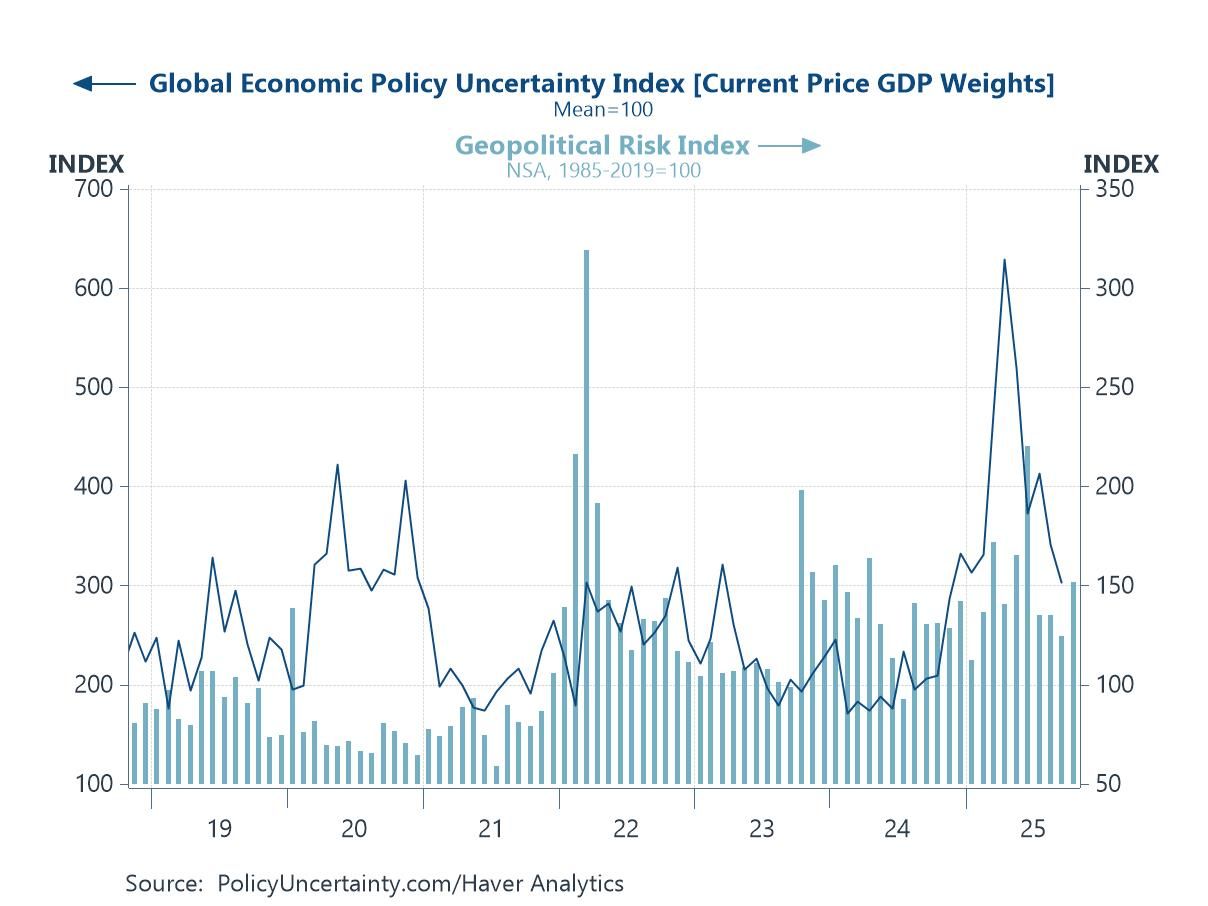

Lingering uncertainties If there has been one constant through 2025, it has been uncertainty itself. Both global economic policy uncertainty and geopolitical risk indices have remained at historically high levels, underscoring an environment shaped by unpredictable policy shifts, heightened conflict risks, and volatile leadership transitions. Trade tensions between the US and China, renewed instability in the Middle East, and political fragmentation across Europe have all contributed to a pervasive sense of unease. For businesses and investors, this has meant navigating a world where the policy outlook can change overnight — from tariffs and fiscal surprises to shifting regulatory regimes. Yet despite this turbulence, financial markets have shown remarkable resilience, helped by disinflation, easier monetary policy, and continued technological investment. In short, 2025 has been a year in which uncertainty has become the new normal — less an episodic shock, more a defining structural feature of the global economic landscape.

Chart 6: Global policy uncertainty versus geopolitical risk

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief