Global| Nov 12 2025

Global| Nov 12 2025Global Money Supplies Deliver Growth-Rate Plateau

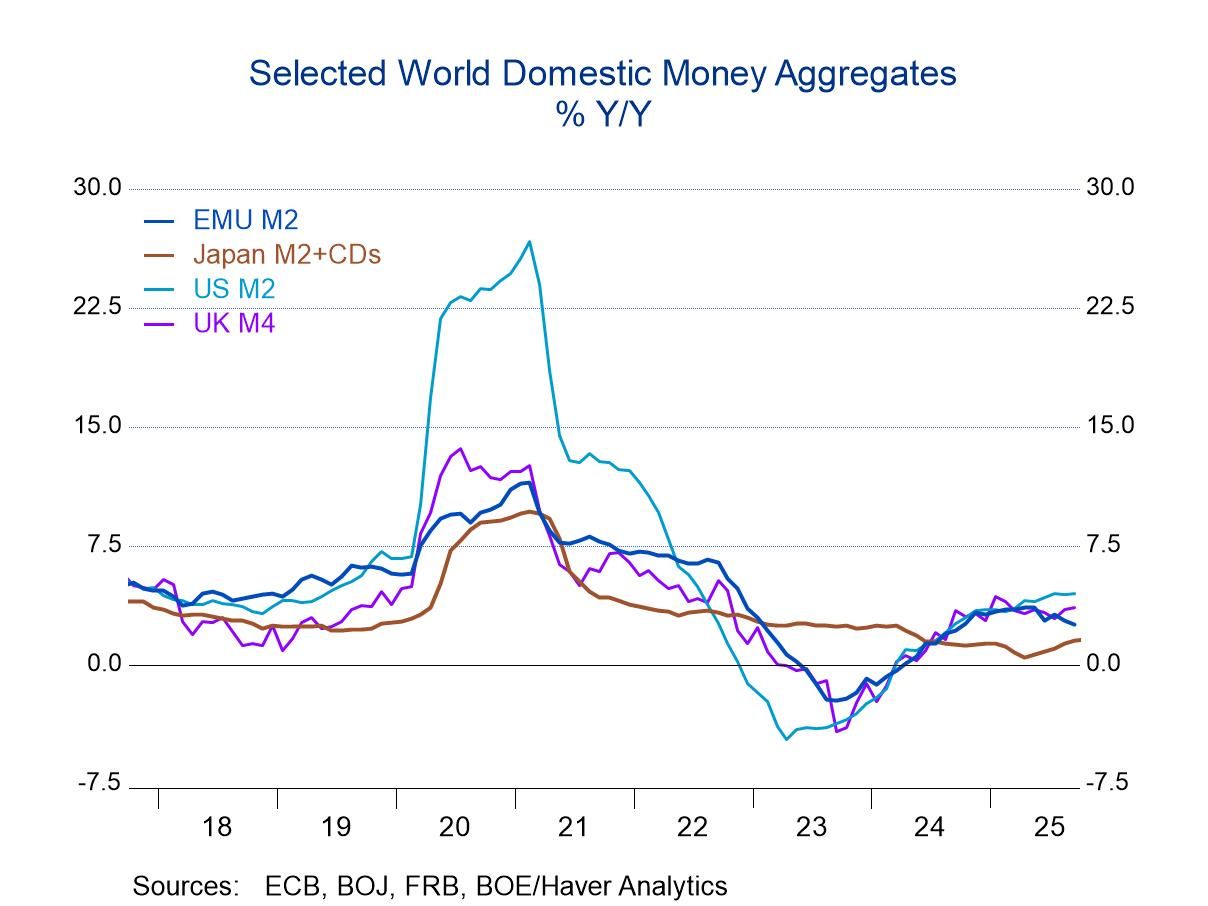

Global money supply growth boomed during COVID. Then growth ‘busted,’ decelerating sharply with the United States, the United Kingdom, and the European Monetary Union all showing monetary contraction to some degree throughout 2023. The only country to buck this trend was Japan which had a more modest boost in money supply during COVID and then more modest growth rates that decelerated and continued to gravitate toward near zero growth, until recently, when Japanese money supply started to accelerate very slightly.

Euro Area Recent trends show nominal money growth in the euro area decelerating slightly from a 2.5% growth rate over 12 months to growth rates around 2% or a bit lower over three months and six months. Monetary union private credit has also decelerated from a growth rate of 2.4% over 12 months to 1.7% over six months and to a 1.3% annual rate over three-months.

United States, United Kingdom, and Japan Nominal money supply growth in the U.S. remains fairly steady, growing 4.5% over 12 months and an annual rate of 5 to 5.4% over three months and six months. The U.K. nominal money supply growth is 3.5% over 12 months, 2.8% at an annual rate over six months and 3.6% at an annual rate over three months. Japan's M2 plus CDs has been stepping up its growth from 1.6% over 12 months to a 2% pace over six months to 4% at an annual rate over three months. Nominal money supply growth is mostly fluctuating between steady and stronger across these monetary center countries.

Real balances in EMU Real money balances, however, are looking significantly weaker. In the European monetary Union, real M2 grows 0.3% over 12 months and then its growth rate slips to -0.6% at an annual rate over both three months and six months. Private credit in the euro area rises by 0.1% over 12 months, declines by 0.5% at an annual rate over six months, and declines at a 1.3% annual rate over three months. Real credit is weakening.

More real balances In the U.S., real money supply growth is fluctuating, growing at 1.4% over 12 months, stepping up to 2.3% over six months and back to a 1.4% annual rate over three months. U.K. real money balances are simply shrinking at a -0.6% annual rate over 12 months and a -0.7% annual rate over three months. In Japan, real money balances are actually accelerating; real money growth is -1.3% over 12 months, which rises to plus 0.4% over six months with an annual rate of 2.9% at an annual rate over three months.

Global monetary growth conditions Global monetary conditions simply don't show a great deal of change over the last year. The perception is that nominal money growth has been relatively stable; however, we can see that real money growth and real credit growth are declining in the euro area and in the U.K. Real balances are growing at a relatively modest rate but also accelerating in Japan. On the whole, money supply doesn't seem to be playing a significant role in charting a new path for monetary policy- except perhaps in Japan.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief