Asia| Jun 16 2025

Asia| Jun 16 2025Economic Letter from Asia: India Rising

This week, we focus on India’s economic developments, which continue to demonstrate resilience amid persistent global headwinds. In Q1, GDP growth accelerated to its fastest pace in a year, surpassing expectations. Services remained the primary growth driver, bolstered by gains in construction and manufacturing (chart 1). Despite widespread global downgrades, the World Bank still expects India to be the fastest-growing major economy in 2025.

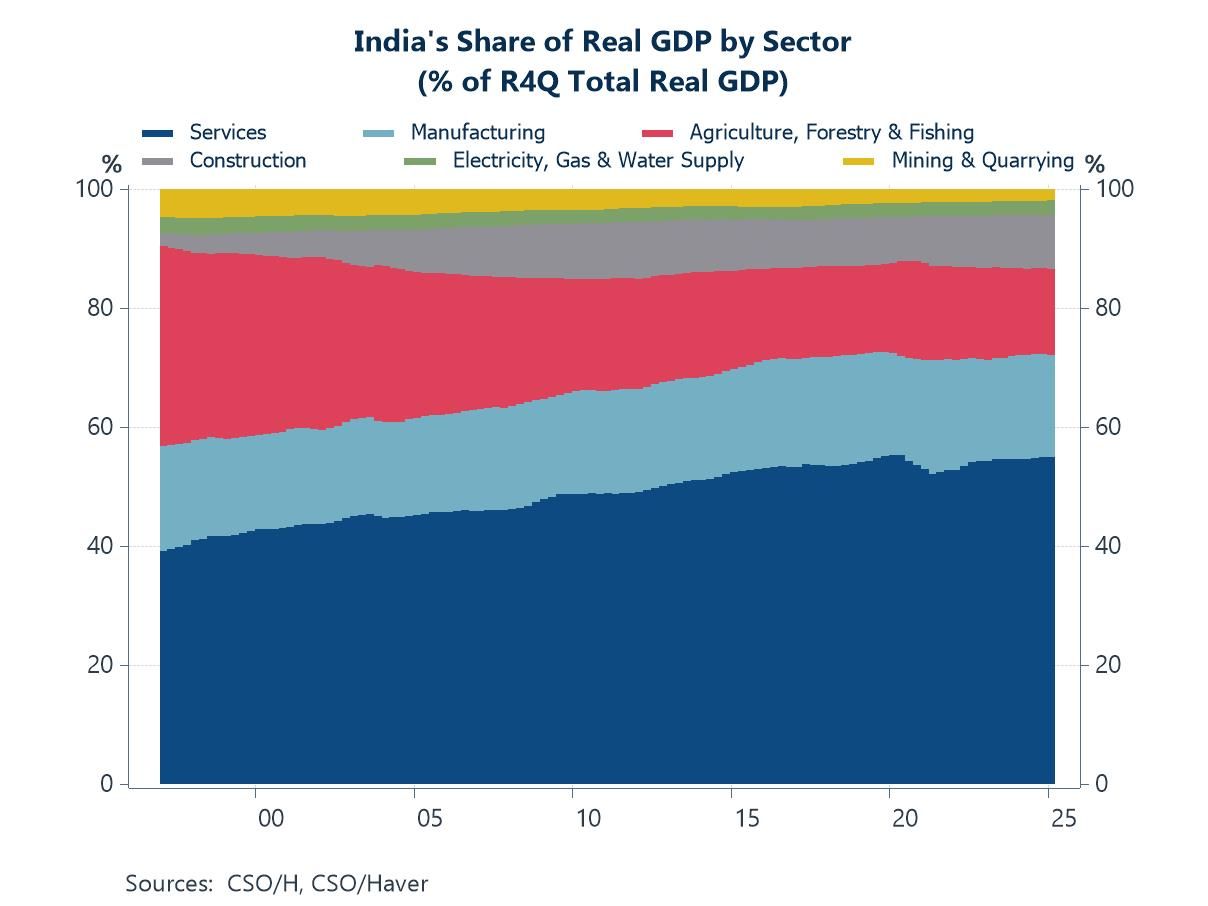

While services have long underpinned India’s growth, the country is gradually pivoting toward manufacturing, including higher-end, IP-intensive sectors. Progress has been made—such as attracting iPhone production—but manufacturing has yet to significantly shift the composition of GDP, which remains heavily weighted toward services (chart 2). India’s rising role as a “China Plus One” destination has enhanced its global appeal, though the shift has drawn criticism from former US President Trump, who favours bringing manufacturing back to the US.

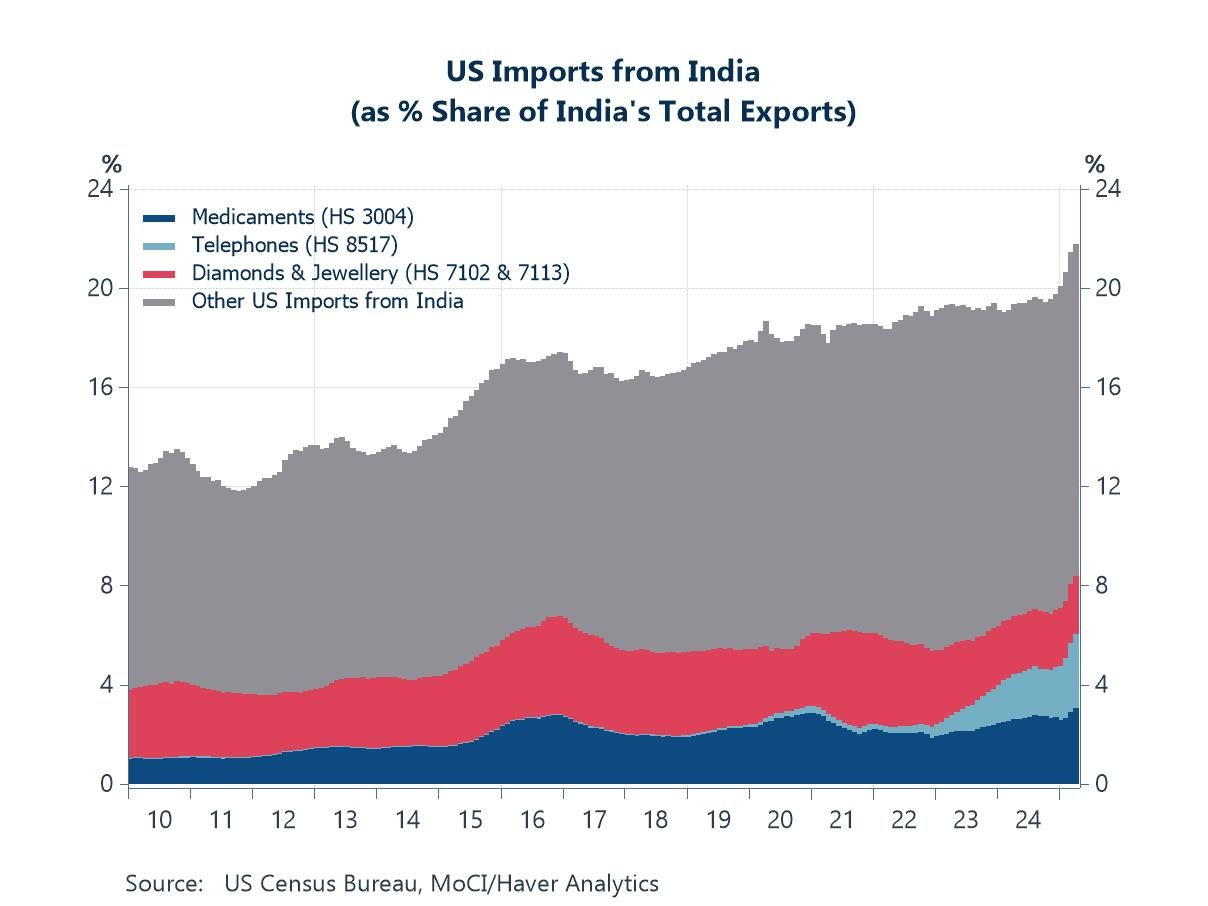

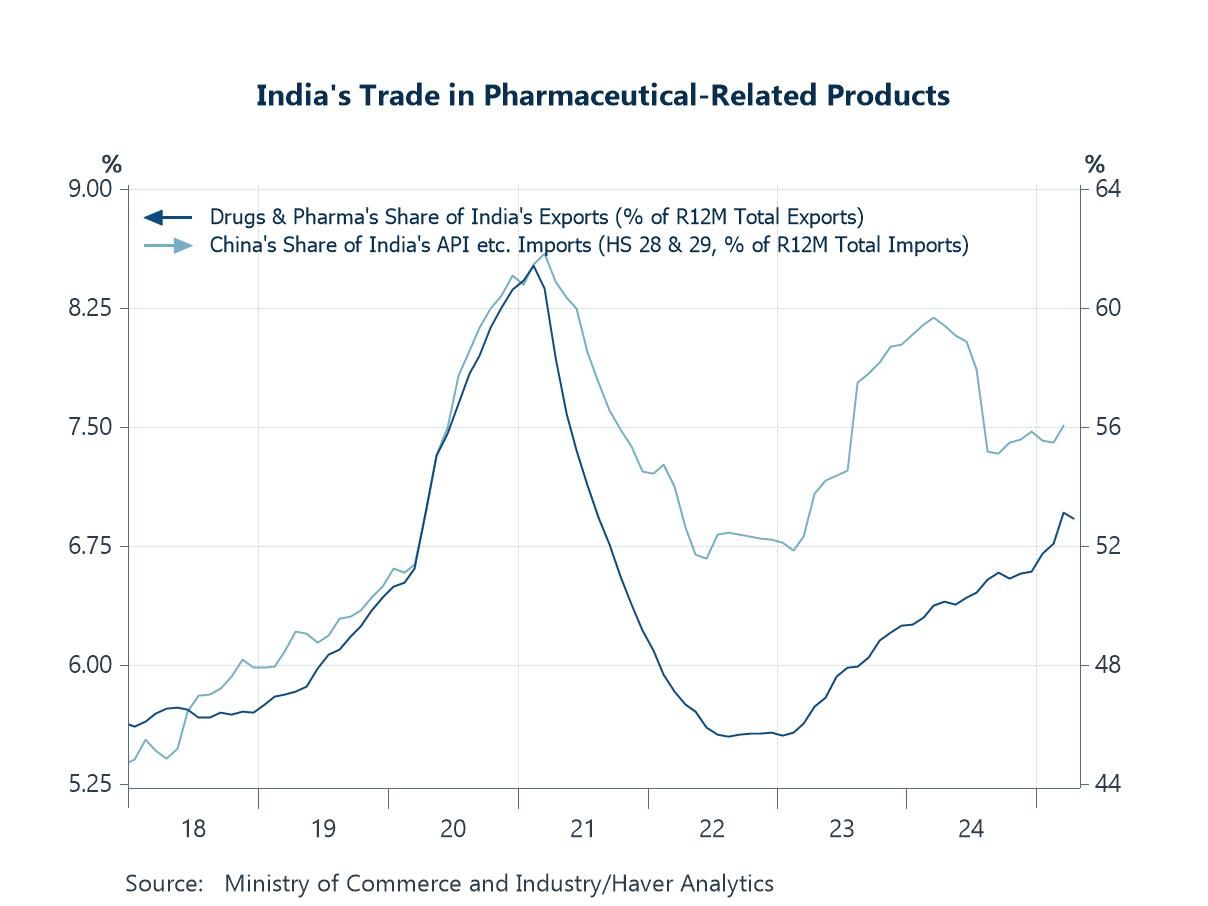

India’s strategic ties with both the US and China require a careful balancing act. The US is India’s top export destination, with major exports including pharmaceuticals, jewellery, and smartphones (chart 3). At the same time, India relies heavily on China for critical inputs such as Key Starting Materials (KSMs) and Active Pharmaceutical Ingredients (APIs), both vital to its pharmaceutical sector (chart 4). As a result, India is seeking to deepen trade relations with the US while avoiding actions that might provoke China. Trade negotiations with the US are reportedly progressing, with an interim deal possible ahead of Trump’s July 9 tariff deadline.

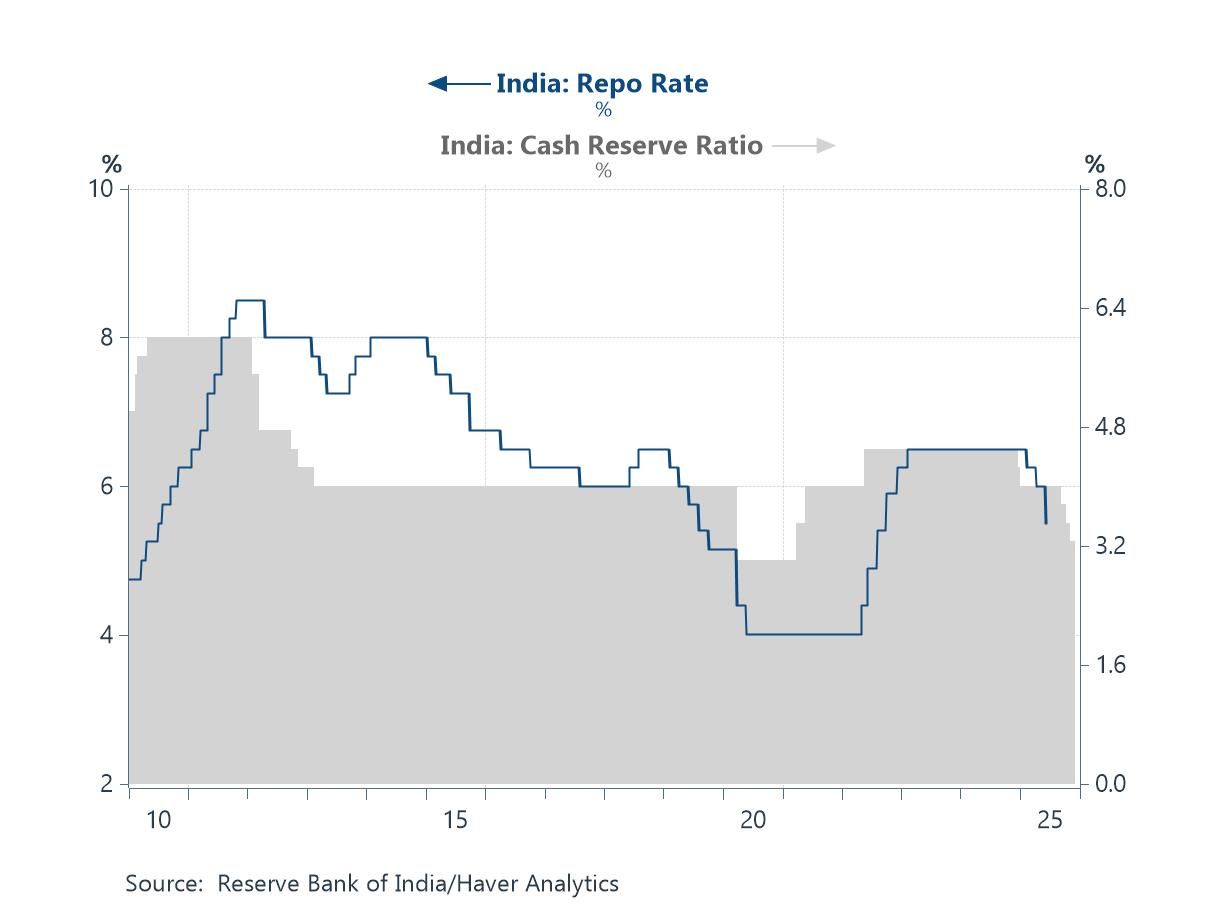

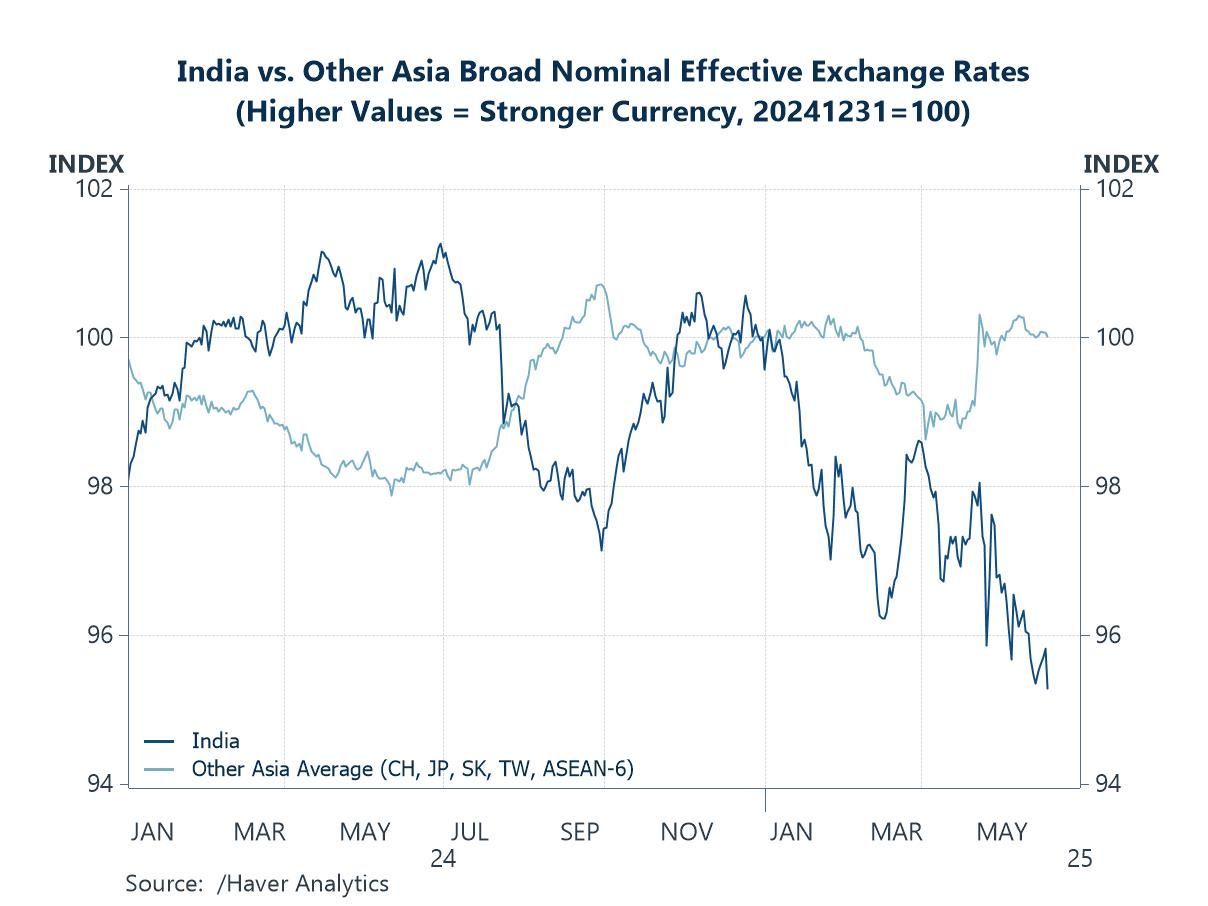

On the monetary front, the Reserve Bank of India cut policy rates by 50 bps in June and announced a phased 100 bps reduction in the Cash Reserve Ratio (CRR), in response to falling inflation and risks of weaker demand (chart 5). As a partial consequence, the rupee has underperformed its Asian peers—though the primary pressures stem from persistent foreign outflows and narrower interest rate differentials (chart 6).

India’s economic developments India’s economy grew faster than expected in calendar Q1, with growth accelerating to 7.4% y/y—exceeding economists’ expectations and marking the fastest growth rate in a year. By sector, and based on gross value added at basic prices, services remained the primary growth driver, as shown in chart 1. However, contributions from the construction and manufacturing sectors also improved. More broadly, many investors and economists continue to view India as one of the few economies expected to deliver robust growth this year. This remains a rare distinction, given the growth-dampening effects of US tariffs and the associated retaliatory actions. That said, recent US-China breakthroughs on trade-related agreements have eased much of this latent risk.

Despite enacting widespread forecast downgrades in its latest projections just last week, the World Bank still expects India to post the fastest growth among major economies in 2025. Nonetheless, India’s outlook has been somewhat dampened by weaker export potential and slowing investment amid rising global trade barriers. Similarly, panellists in our recent Blue Chip Economic Indicators survey continued to rank India as the top-growing major economy among those covered.

Chart 1: Drivers of India’s real GDP growth

Over the years, India has positioned itself as a services-oriented economy, a strategy that initially offered a degree of insulation from external shocks. More recently, however, the country has begun shifting its focus toward manufacturing—not only at the low- and mid-range levels but also in high-end, intellectual property (IP)-intensive sectors. In support of this pivot, India has been gradually improving its IP protection framework. Nonetheless, it remains on the US Trade Representative’s 2025 Priority Watch List, partly due to what has been described as “inconsistent” progress on IP protection and enforcement. In more traditional forms of manufacturing, India has made several high-profile strides, including securing production capacity for iPhones. However, despite such headline-grabbing developments, the shift has yet to meaningfully alter the structure of India’s GDP (chart 2), which remains heavily services-dependent—likely due to the limited scale of manufacturing gains thus far.

India has also emerged as a key beneficiary of the “China Plus One” strategy, as global firms seek to diversify production away from China amid rising geopolitical tensions, particularly with the US. These concerns—recently reinforced by US policy actions—have helped position India as a partial but increasingly viable alternative. That said, the shift has not been without controversy. The redirection of US-linked manufacturing capacity toward India has drawn criticism from former President Donald Trump, who has advocated for bringing such production back to American soil—even though the current US manufacturing landscape may be ill-equipped to fully absorb it.

Chart 2: India’s share of real GDP by sector

India’s relationship with the US and China Amid ongoing US-China tensions, India finds itself in a complex—but potentially advantageous—position. On one hand, India is heavily reliant on the US as a key export market, with the US currently being its top export destination. On the other hand, India depends on China for critical inputs across several major sectors. Among India’s key exports to the US are pharmaceutical products, jewellery, and, more recently—as mentioned earlier—smartphones (see chart 3). Given this dual dependency, it is unsurprising that India is eager to maintain constructive trade relations with the US. India-US trade talks are reportedly progressing well, with an interim deal likely before President Trump’s 90-day tariff pause ends on July 9.

Chart 3: US imports from India

At the same time, India remains highly dependent on China for low-level inputs, which may temper its willingness to appear too closely aligned with the US or to pursue a trade deal perceived as unfavourable to China. This strategic caution stems from India’s reliance on key material imports from China, including rare earth elements (REEs), recently spotlighted by China’s export restrictions. REEs are critical to several industries, notably automotive manufacturing. India is also heavily dependent on China for key starting materials (KSMs) and active pharmaceutical ingredients (APIs), both essential to its large and growing pharmaceutical export sector (see chart 4). As a result, India must carefully balance its strategic interests—deepening ties with the US while avoiding actions that could provoke a negative response from China amid rising geopolitical tensions.

Chart 4: India’s trade in pharmaceutical-related products

India’s financial and monetary developments In response to the potentially demand-dampening effects of ongoing US tariffs, the Reserve Bank of India (RBI) cut policy rates by a larger-than-expected 50 bps at its June meeting. The move was supported by a sharp decline in CPI inflation, which fell well below the RBI’s 4% target amid easing commodity prices. However, the central bank warned that it now has “very limited” policy space left to support growth, a concern reflected in its shift in policy stance from “accommodative” to “neutral.” In addition, the RBI announced a 100 bps cut to the Cash Reserve Ratio (CRR), to be implemented in four tranches of 25 bps each from September to November, ultimately bringing the CRR down to 3%. This measure aims to release additional liquidity into the financial system.

Chart 5: India’s policy rate and cash reserve ratio

Lastly, we turn to the Indian rupee, which has underperformed relative to its Asian peers so far this year (see chart 6), despite the broad-based weakening of the US dollar. Weighing on the rupee have been persistent foreign equity outflows—substantial on a year-to-date basis—along with some net FDI outflows and other external pressures. The RBI’s recent interest rate cuts, though necessary to support the domestic economy, have also reduced the rupee’s appeal by narrowing interest rate differentials. Investor sentiment was further shaken during the previous wave of US-China tensions, prompting capital flight from emerging markets, including India. While some of that risk aversion has eased amid a temporary cooling in US-China rhetoric, caution remains warranted, as the US appears poised to announce a new round of unilateral tariffs in the coming weeks.

Chart 6: Indian rupee performance vs. other Asian FX

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief