CBI’s Distributive Trades Survey Weakens Sharply in December

The new UK Confederation of British Industry (CBI) survey on the distributive trades sector shows a sharp weakening of an already weak survey for December and for the outlook into January of 2026.

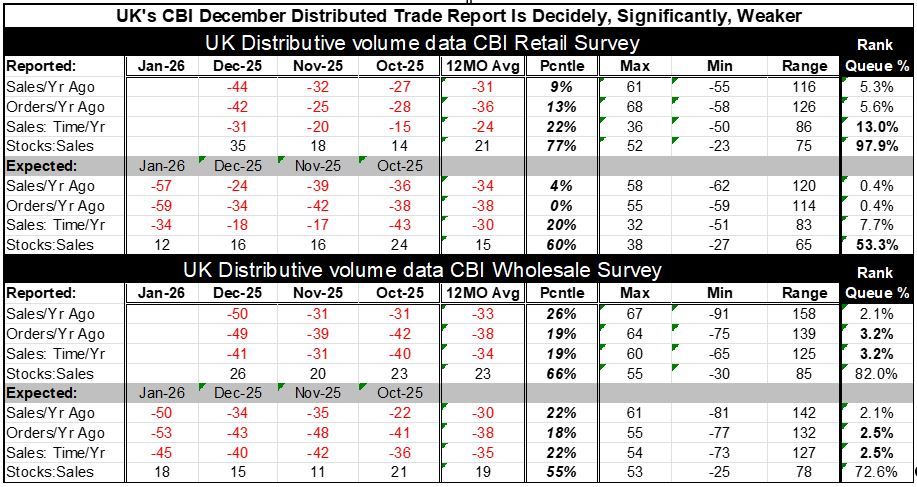

The month-to-month deterioration from November was widespread across metrics for retailing as well as for wholesaling for the current month as well as for the outlook. The monthly degradation is without exception across the board - omitting the inventory metric which is a different animal in any event since inventory building is sometimes involuntary.

The Retail survey Current conditions: In December, the retail survey for sales compared to a year ago, orders compared to year ago, and sales for the time of year (a seasonal adjustment metric), all worsened month-to-month. The November readings were weak and in December sales compared to a year-ago worsened by 12 points, Orders compared to a year ago worsened by 17 points month-to-month and sales for the time of year worsened by 11 points. These metrics for December are below their respective 12-month average by 6 to 13 points, as well for these categories. The rankings tell a stark story, year-on-year sales have been lower only 5.3% of the time, Year-on-year orders have been weaker only 5.6% of the time, while time of the year sales have been lower only 13% of the time. These are all extremely low-ranking metrics.

Expected Conditions: In January expected conditions have weakened month-to-month by amounts ranging from 33 points to 16 points depending on the metric. And sales and orders compared to a year ago as well as sales for the time of year each are weaker than their respective 12-month average readings by amounts ranging from 4 points to 23 points. The rankings on expectations are even worse than for the current metrics. Expected sales compared to a year ago rank lower less than 1% of the time, the same is true of orders. While sales for the time of year have been weaker 7.7 percent of the time.

Wholesale survey The rankings for wholesaling are even lower than for retailing across the current and expected metrics. The month-to-month degradation for the current readings ranges from 7 points to 17 points weaker while the reading degradation monthly ranges from 5 points to 16 points. Wholesale sales and orders compared to a year ago and sales for the time of year each rank below the 5% mark. The expectations for January shows expectations for the three categories each are at a 2.5 percentile standing or lower.

Summing up The distributive trades survey has all but crashed and burned in December. Over the last 26 years the average of the three current metrics’ rankings has been lower only 18 times. The average outlook ranking for the month ahead has been weaker only 5 times in the last 26 years (over 313 months). On a relative basis the expected sales/orders performance is more depressed than the Current results for January. The pooled rankings show current ranking over the past 26-years weaker only 5.8 percent of the time with expectations lower only 1.6 percent of the time. These are very weak metrics. It is surprising that the BOE is walking on eggshells to cut rates with mixed support for rate cuts amid such weakness. There is already a GDP decline in the monthly data for October. UK and inflation is still too high, but it is breaking lower at a relatively fast pace. Will the UK be the first economy down after Covid?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global