Asia| Aug 11 2025

Asia| Aug 11 2025Economic Letter from Asia: Trade-Offs

This week, we look at key economic and trade developments across Asia amid persistent geopolitical tensions and shifting policies. US-India trade talks, once expected to produce a quick deal, have stalled. India now faces up to 50% additional US tariffs—half from revised reciprocal rates and half linked to its continued imports of Russian oil, which make up about 35% of its crude supply (chart 1). Around 20% of India’s exports go to the US, leaving its economy exposed to the impact of these measures. In China, a flurry of economic data releases for July will provide a comprehensive update. Despite resilient numbers of late, doubts persist about the sustainability of growth. Recent retail sales gains have been partly fuelled by a government subsidy program, which is likely a one-off, while the property market continues its multi-year decline. Export growth has endured (chart 2), but largely supported by importers’ front-loading ahead of tariffs,an effect that’s likely to be temporary. The US-China tariff pause may be extended, though talks remain ongoing, and risks of renewed tensions persist. Meanwhile, China’s trade surplus continues to expand as exports shift toward Africa, Southeast Asia, and Europe (chart 3).

On the region’s growth backdrop, Japan’s preliminary Q2 GDP reading and final Q2 figures from Taiwan, Hong Kong, and Malaysia are due. Taiwan’s preliminary Q2 GDP shined, boosted by AI-driven exports (chart 4), while Hong Kong and Malaysia have been treading water. Japan has faced export headwinds from US tariffs, particularly in autos, though recent US-Japan and US-Korea deals reducing auto tariffs may support future growth (chart 5). Monetary policy watchers will focus on the Reserve Bank of Australia, expected to cut rates but signal an end to easing, and the Bank of Thailand, likely to cut rates amid deflation risks (chart 6).

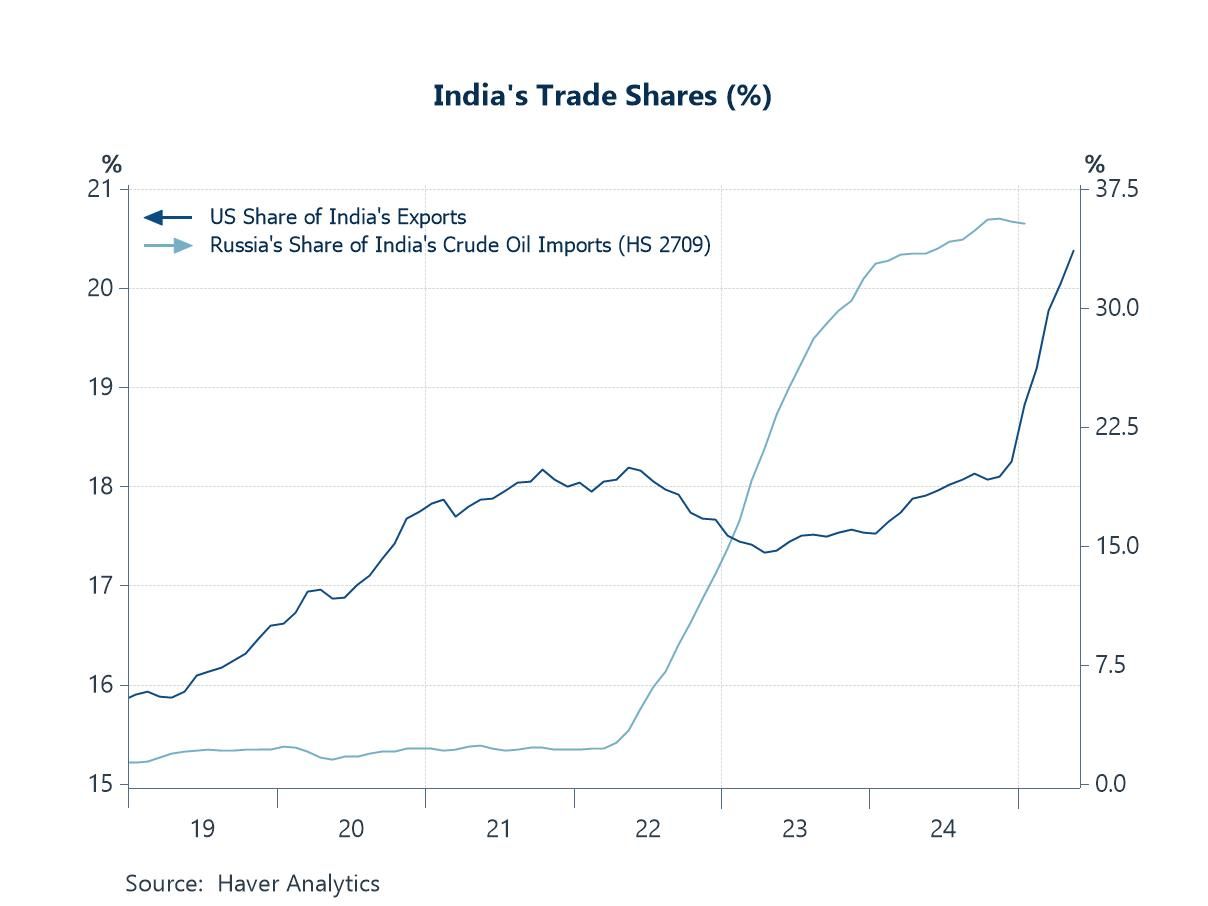

The US-India furore The trajectory of US-India trade talks has not unfolded as initially expected. At one point, these negotiations were considered among the most likely to yield an early deal. However, that has not materialized. In fact, India now appears to be in a potentially worse position than it was around its Liberation Day period, as it faces the prospect of up to 50% in additional US tariffs. Of that, 25% stems from the revised reciprocal tariff rate from the US, while the remaining 25% is linked to India’s continued purchases of Russian oil. India has thus found itself in a bind: on the one hand, it is under pressure to reduce imports of Russian oil—which have grown about 35% of its total crude oil imports, as shown in chart 1—while on the other, its exports to the US, which now make up roughly 20% of its total exports, could be seriously harmed by US tariff measures.

Chart 1: India’s trade shares with the US and Russia

The China docket In China, July data on retail sales, industrial production, fixed asset investment, house prices, and unemployment are all scheduled for release this week, offering a comprehensive update on the state of the world’s second-largest economy. Despite a recent run of seemingly resilient figures, there remain valid reasons for caution and doubts about the sustainability of this momentum. While government and monetary support measures have undoubtedly helped prop up growth, they can only do so much—and only for so long—without structural reforms to address underlying issues. For example, recent retail sales data have often exceeded expectations, but much of that strength has been driven by the government’s durable goods subsidy program. These effects are likely to be one-off, and with budget allocations for such subsidies capped, the retail sales bounce may soon fade in the absence of deeper, structural improvements in China’s consumer base. Persistent weaknesses also remain in other sectors—most notably the property market, where prices have continued to fall, extending a multi-year downtrend. In trade, export growth has held up, as shown in chart 2, despite US tariff measures. However, much of this resilience has stemmed from importers’ precautionary front-loading ahead of potential tariff hikes—an effect that is likely temporary and could soon fade.

Chart 2: China’s exports, retail sales, and residential prices

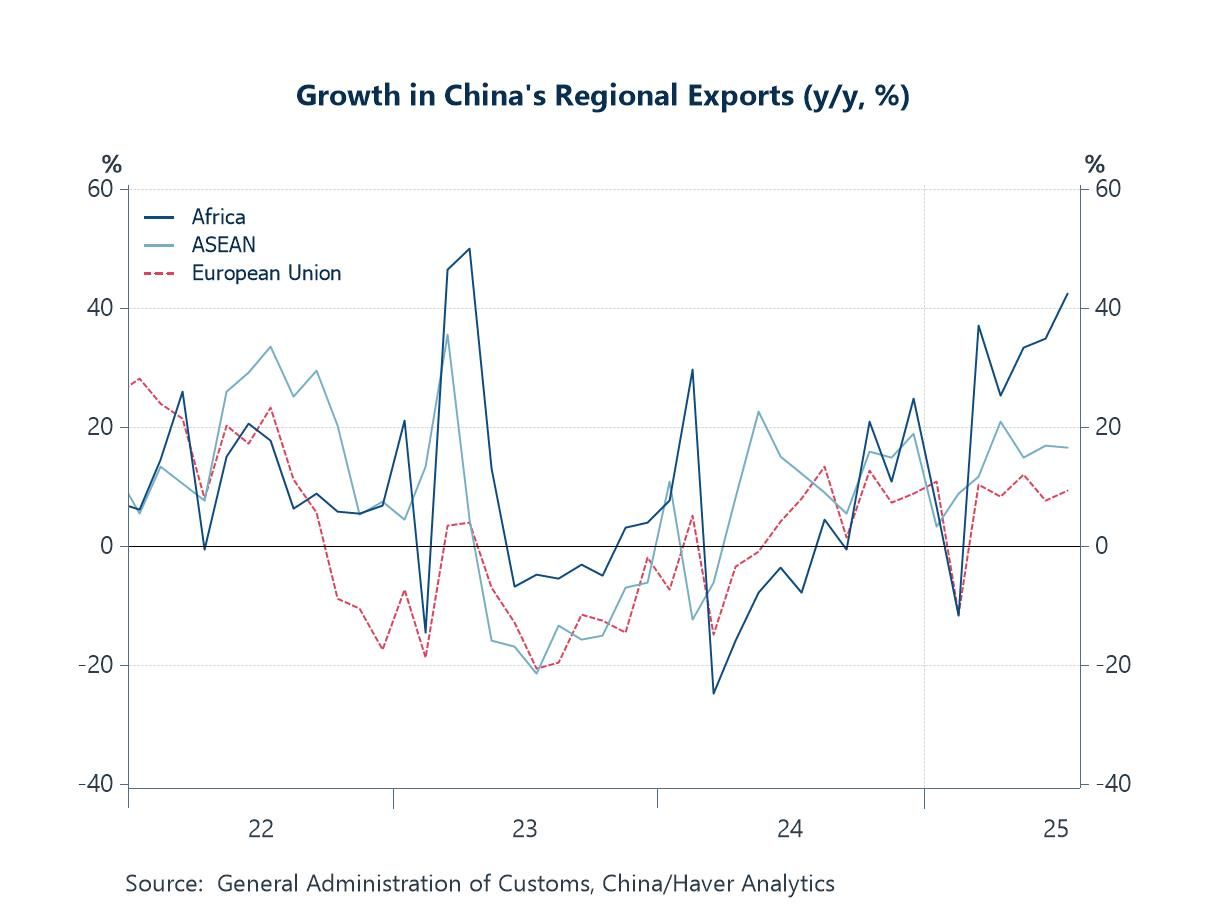

Adding to the discussion on China’s trade situation, while an extension of the US-China tariff pause appears likely (talks are still ongoing) there remains a tail risk of renewed escalation in trade tensions, an outcome that would clearly weigh on the global economy. Nonetheless, the first round of (now-paused) mutual tariffs had already triggered some degree of trade rebalancing, with the US-China trade deficit even narrowing during the current pause. However, China’s overall trade surplus continues to expand, suggesting it may be redirecting exports to other markets such as Africa, Southeast Asia, or Europe, as shown in chart 3—or potentially re-routing trade flows altogether.

Chart 3: Growth in China’s regional exports

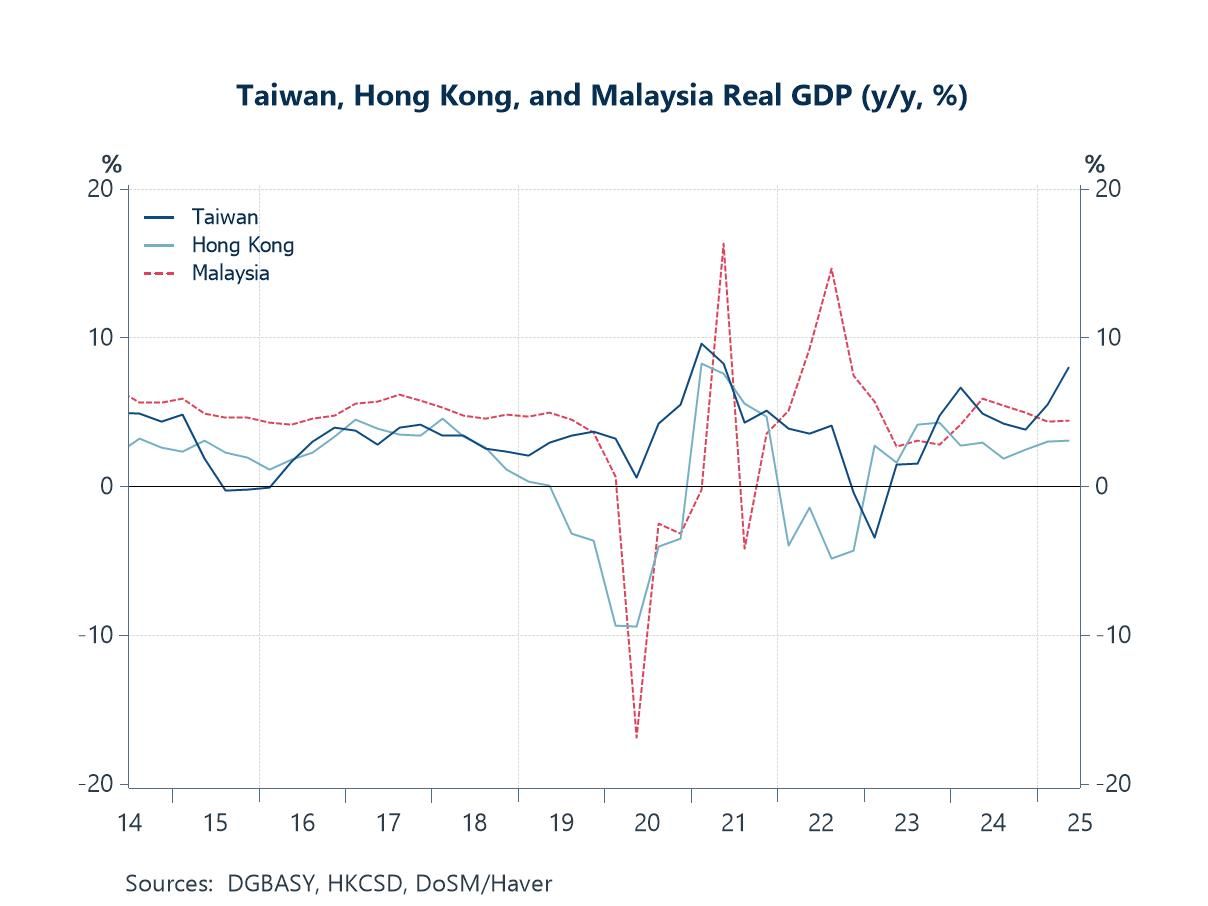

GDP releases ahead Apart from developments in China and the ongoing US-India trade furore, the week is packed with GDP releases—most notably the preliminary reading for Japan (discussed below) and final readings for Taiwan, Hong Kong, and Malaysia. Broadly speaking, while Q2 data will capture part of the impact from the US’s first round of reciprocal tariffs and the subsequent pause, the effects of the updated tariffs—mostly higher than the prior pause rate of 10%—are of arguably greater concern and will only be captured in later data prints. These new rates, announced recently by the US, took effect on August 7. Preliminary Q2 GDP figures for Taiwan have already shown stellar results (chart 4), driven by export strength linked to the ongoing AI boom, while growth in Hong Kong and Malaysia has continued to tread water.

Chart 4: Taiwan, Hong Kong, and Malaysia real GDP

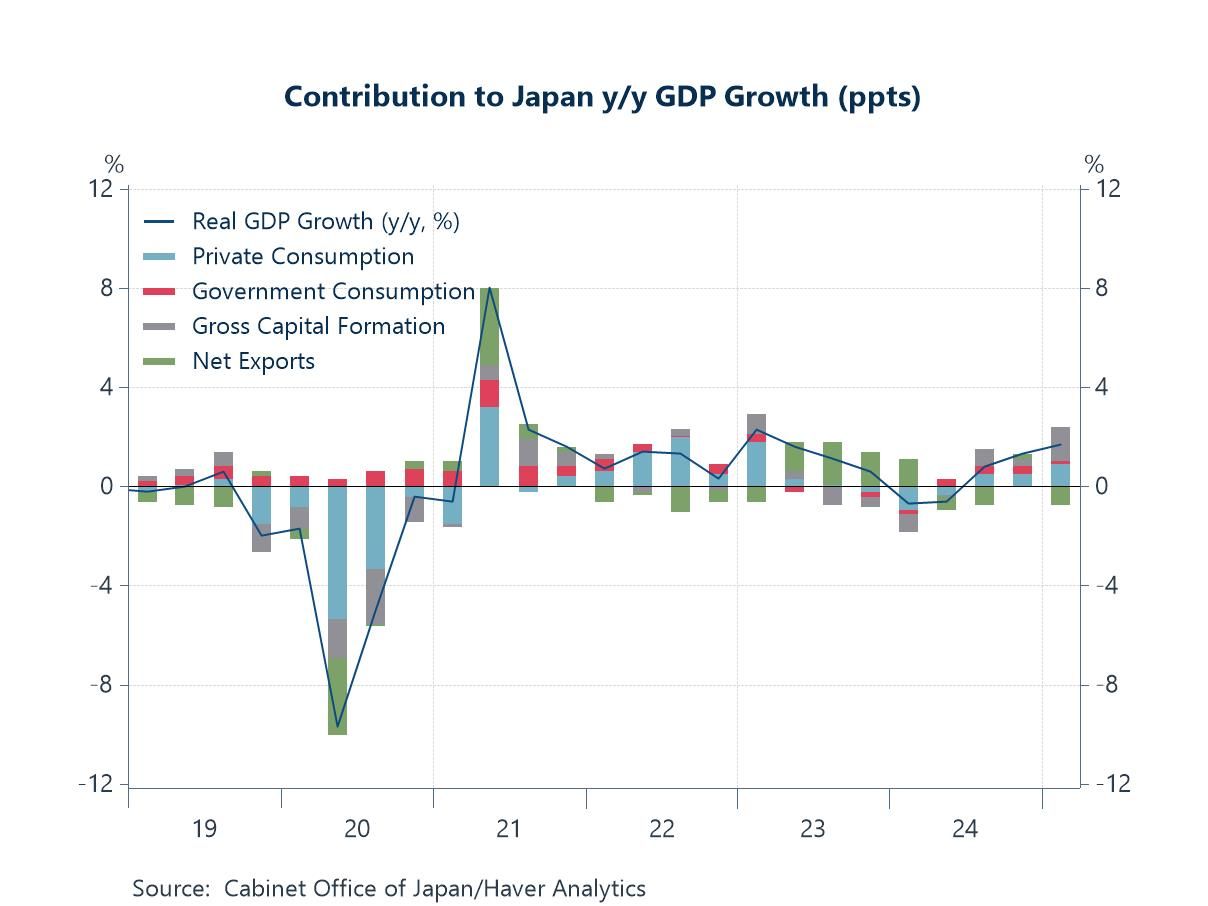

Turning next to Japan, the economy—like many other export-driven Asian markets—has recently felt the weight of US tariffs, which have significantly dampened growth by reducing export volumes, particularly in the automotive sector. These tariffs created headwinds that slowed Japan’s export performance and constrained overall economic momentum (chart 5). However, the recent US-Japan and US-Korea trade agreements, which include reductions in auto tariffs, may provide some relief and bolster future growth. That said, it’s important to note that the positive effects of these tariff reductions will not be reflected in Japan’s preliminary Q2 GDP figures, scheduled for release later this week.

Chart 5: Drivers of Japan’s real GDP growth

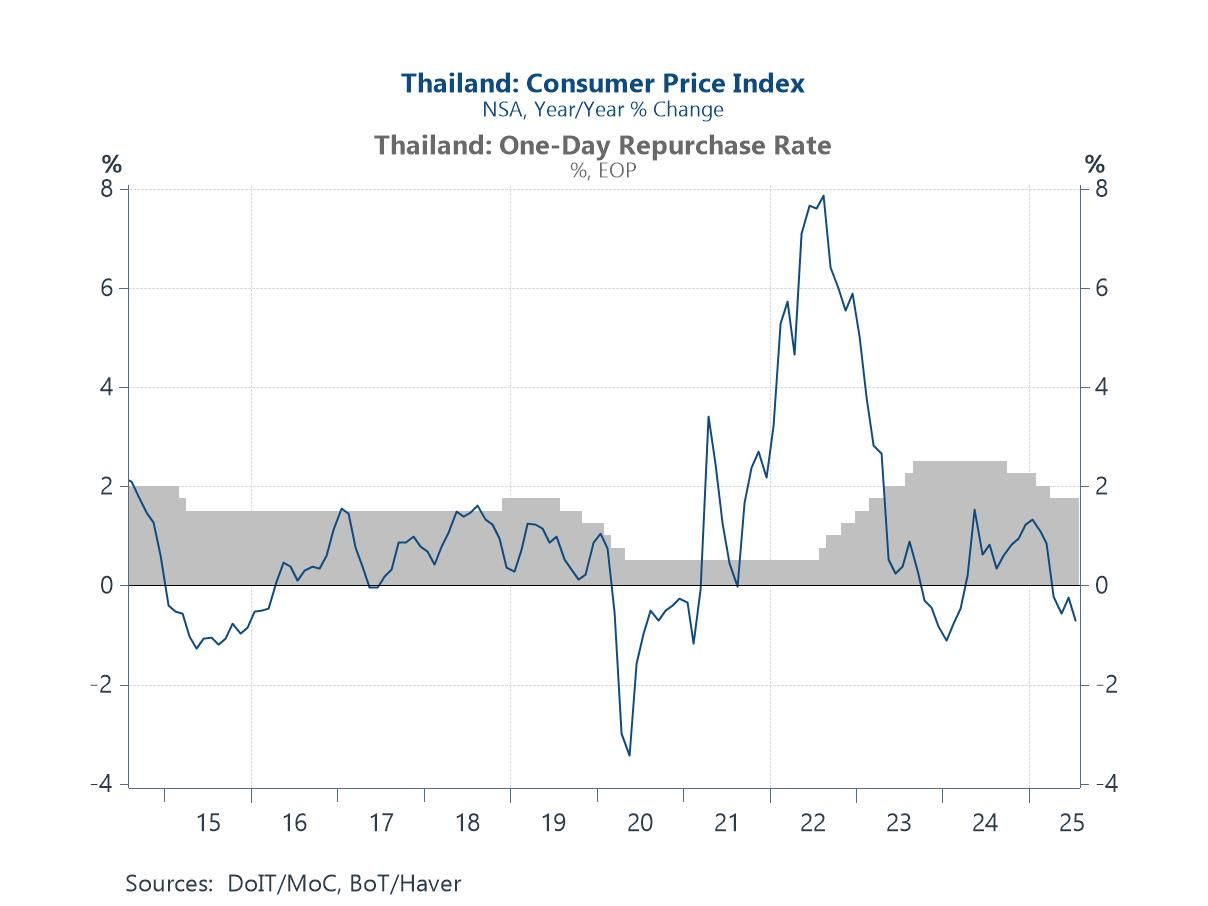

Central bank releases ahead Monetary policy decisions from the Reserve Bank of Australia (RBA) and the Bank of Thailand are also in focus this week. The RBA is widely expected to deliver another rate cut while signalling a likely end to its easing cycle, balancing the risk of resurgent inflation against the continued need to support growth. Meanwhile, a rate cut by the Bank of Thailand has become increasingly likely, following the latest inflation data that showed a deeper dive into deflation (chart 6). This weak price and demand environment may compel the central bank to ease further to bolster growth. Regardless of what happens before October, markets anticipate that the Bank of Thailand will adopt a dovish stance once incoming Governor Vitai—known for his pro-easing views—assumes leadership.

Chart 6: Thailand inflation and policy interest rate

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief