Existing Home Sales: A (Faint) Pulse

Summary

-Sales rose for the third time in the past four months… -…but activity remains low by historical standards

Sales of existing homes rose 1.2% in October, marking the third increase in the past four months and leaving a net gain of 4.3% over this span. Although activity has advanced in the past few months, sales remain low by historical standards. They dramatically trail the robust activity that unfolded in response to the low interest rate environment during the pandemic, and they lag noticeably behind the level of sales before Covid.

Interest rates seem to explain both the recent mild stirring in home sales and the still-low level of activity relative to historic norms. An easing in mortgage rates from approximately 7% in the early months of the year to 6.25% more recently undoubtedly gave a boost to the housing market. However, mortgage rates are still approximately 1.4 percentage points above the high in 2018 and almost 2.6 percentage points above the low in 2019, easily enough to keep many potential homebuyers on the sidelines.

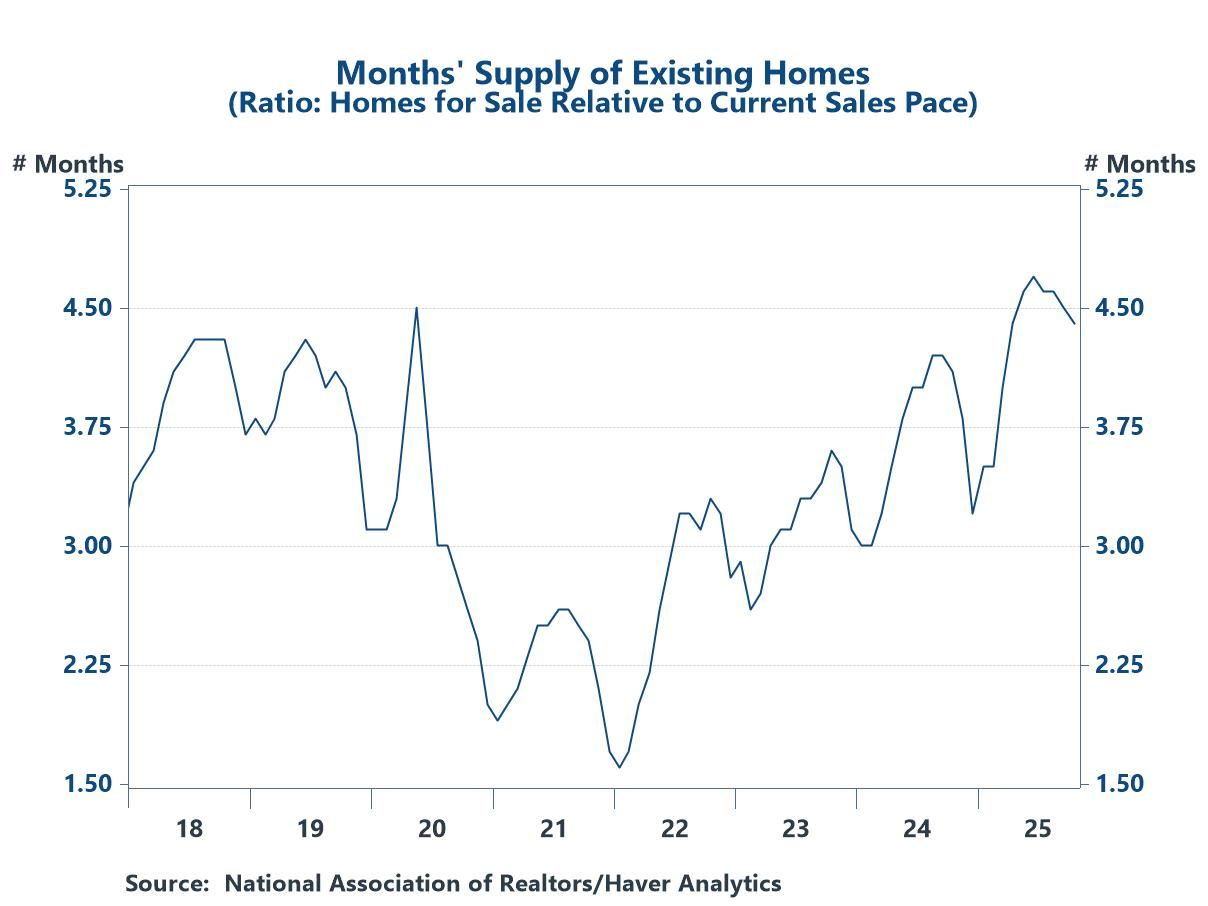

The National Association of Realtors, the source of data on existing home sales, cited a lack of inventory for the slow pace of sales when activity started to soften in 2022. That seems to be less of a problem now. The number of homes on the market has recently climbed to slightly more than 1.5 million, up from a range of 0.85 to 1.3 million from 2021 through much of 2024. When measured relative to the pace of sales (so-called months’ supply) the current level of 4.5 months is comfortable by historical standards. (Months’ supply is the time required to clear housing inventory at the current sales pace.)

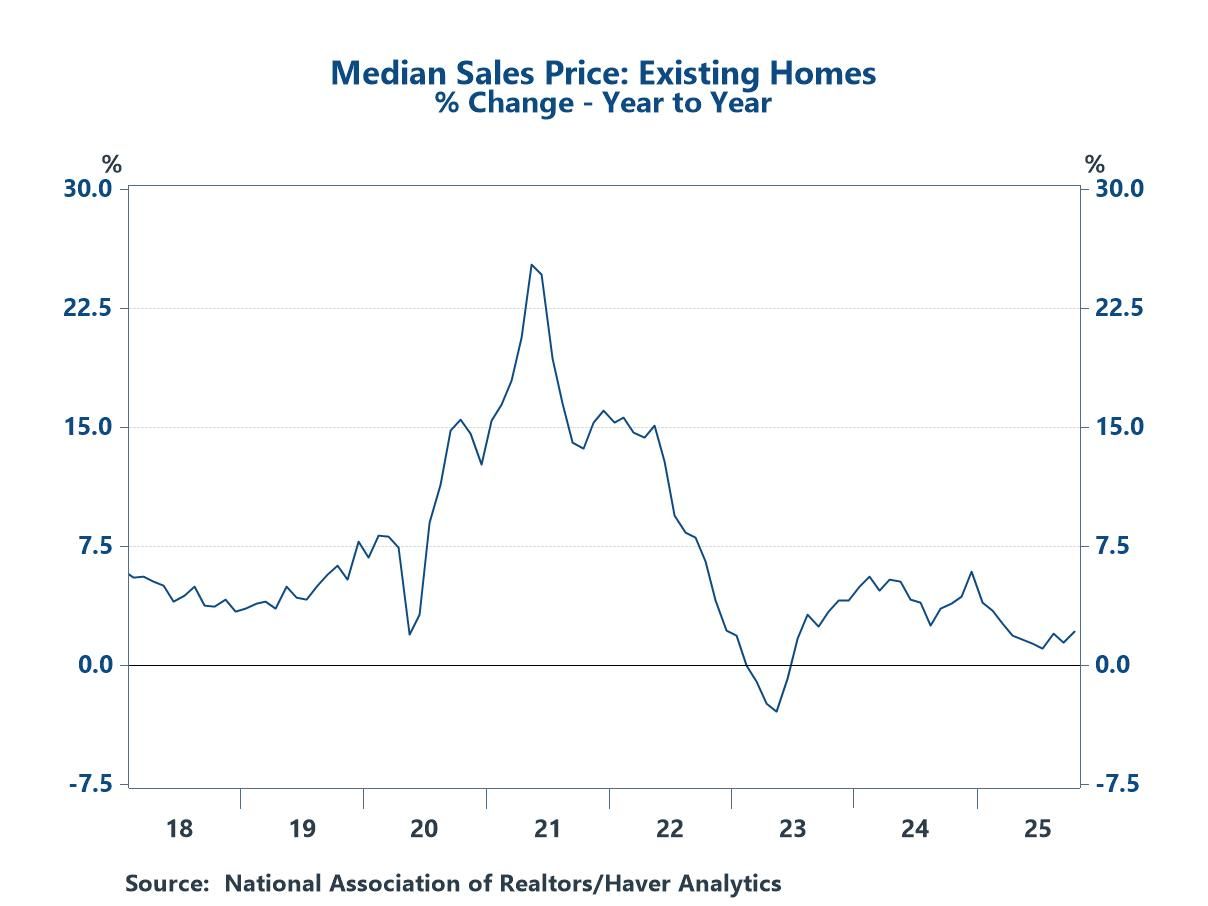

The subdued pace of demand has led to cooling in price appreciation. The median price of existing homes is still increasing, but at a slow pace. The latest year-over-year increase of 2.9% pales in comparison to the double-digit increases seen during the low interest rate environment of 2020-22 and trails the increase of 4.5% last year and the average of 4.7% in 2018-19.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global