UK Inflation Drifts Lower as Unemployment Rises

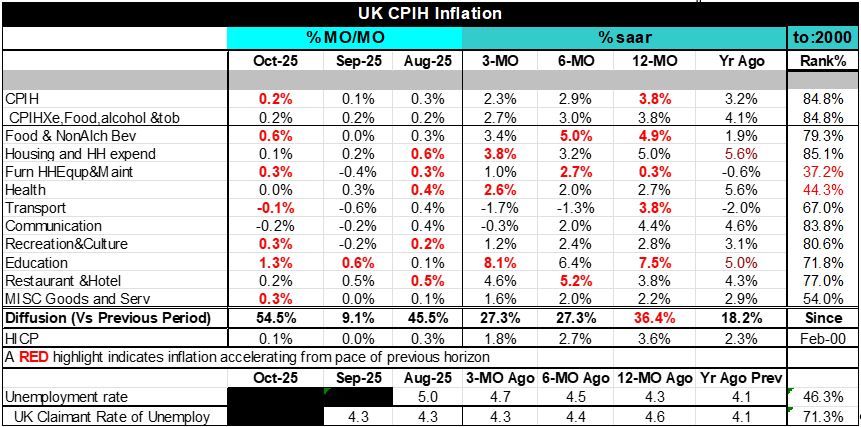

UK inflation gives the BOE a greenlight on rate cuts. UK inflation is still excessive at 3.8% over 12-months for the CPI-H and its core metric. But over six-months both of those drop; the headline drops to a pace of 2.9% and the Core drops to 3.0%. Over three-months inflation drops even lower to a headline pace of 2.3% and a care pace of 2.7%. Both are still above the 2% target but look much less dangerous.

Stauch inflation fighters still will not like the results. But with the unemployment rate a year ago at 4.2% and now up to 5% (as of August) and with a one-half-of-one percentage point rise in the unemployment rate in the last six-months it becomes hard to hold the line on monetary policy. The BOE’s rate changes have mirrored those of the Fed in the US, but with the official; unemployment rate at 4% now and short-term inflation readings around 2 ½ percent and unemployment rising it would be hard for the central bank, especially given the turbulent UK political scene, to squeeze the economy further. IN the UK inflation is deflation whereas in the US inflation is stuck, possibly rising and facing the potential of pressure form tariffs.

Inflation diffusion checks in below 50% (the level that marks equal tendencies for inflation to accelerate or decelerate across broad categories) for 12-months, 6-months, and 3-months. Over recent months, month-to-month inflation has been contained in terms of broad categories with two of three months showing monthly diffusion below 50%.

It is hard to make any optimistic case for economic activity and if UK activity is going to slow, it is much easier to make a case for inflation containment to progress further. While the more up to date claimant count unemployment rate has been steady, the lagging overall rate has a clear uptrend that has to be viewed as worrisome.

Like the Fed I would surely like to see more progress on inflation in the UK and I do not view current circumstances as optimal to cut rates. But the situation is simply slippery. And monetary policy is made in the real world under conditions or uncertainty. And real-world conditions surely pave the way for some continued rate cutting unless data and trends shift.

In October, the CPI and Core rose by just 0.2% month-to-month with inflation rising in six of ten major categories month-to-month and after seeing only one category accelerate month –to- month in September and a split of five/five in August.

Still, make no mistake about it, inflation is still too high. The question of the bet by the central bank will be on the future. When UK inflation is ranked on Year-over-year monthly observations back to early 2000, inflation is below its median year-to-year rise in only two of ten categories and ranked on the same period the freshest unemployment rate has been lower about 46% of the time marking the current (rising) rate of unemployment as slightly below its median for this period. But the claimant rate that has stabilized at a lower level is nonetheless higher on this period, less than 30% of the time, which means the stability in the claimant rate is not as reassuring as it seems. It would appear that policy dialogue in the UK is about to shift.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global