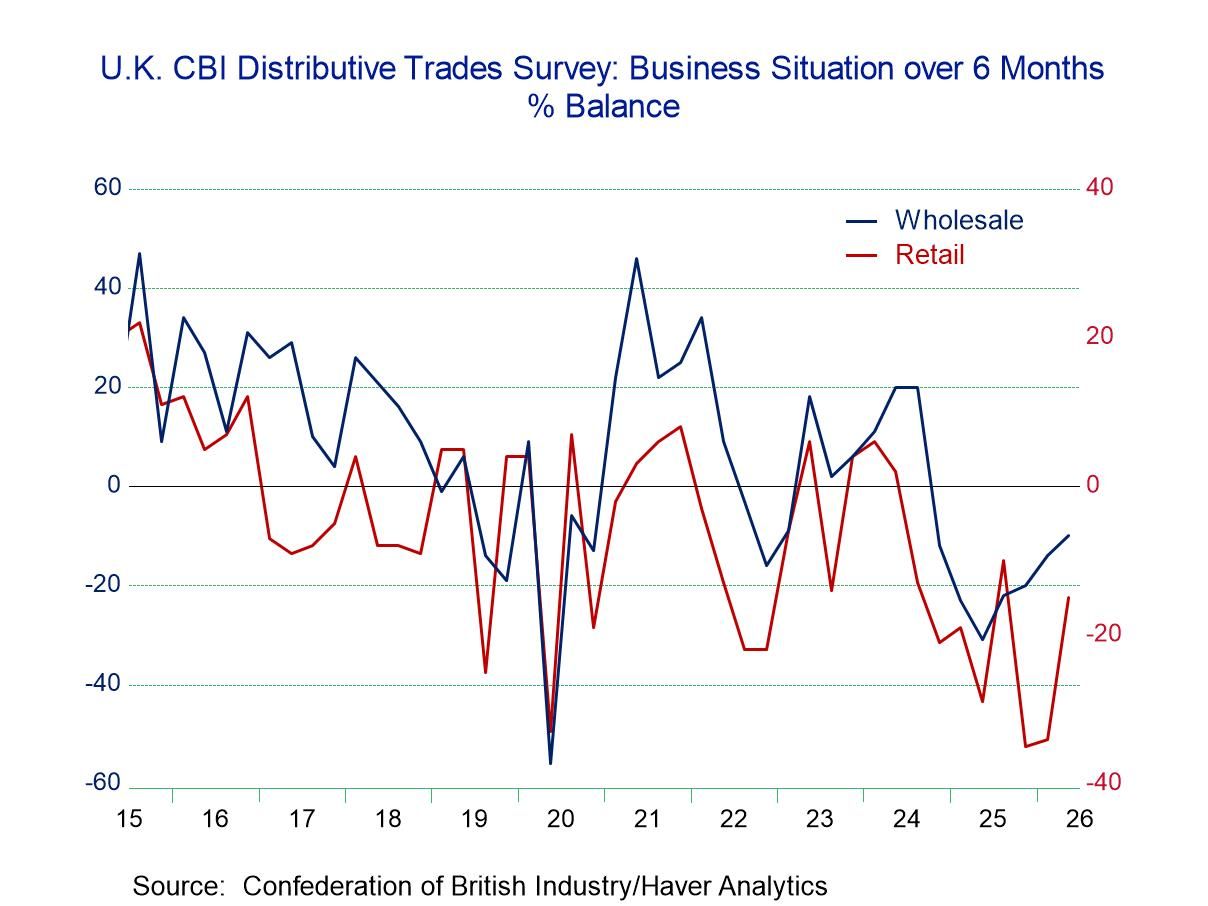

The U.K. distributive trades survey in retaliating for the second quarter of 2026 shows some improvement in the business situation expected over the next six months as that reading rose to -15 from -34 in the first quarter, putting it only slightly weaker than its third-quarter 2025 reading of -10. Still, it is a very weak reading.

The employment reading also improved in the second quarter to -30 from -40 in the first quarter. That reading, however, is still lower than its -19 reading in the fourth quarter and its -14 reading on the third quarters of 2025.

Capital spending plans on the quarter for the year ahead registered -52 in the second quarter, compared to -46 in the first quarter; this reading has steadily deteriorated.

Imports have improved slightly in the second quarter, with the reading at 7 compared to 10 in the first quarter and 13 in the fourth quarter.

The expected selling price compared to what it registered a year ago is at 42, compared to 40 in the first quarter; they compared to even stronger values at the end of last year. Expected employment in the second quarter fell sharply to -44 from -23 in the first quarter, and this reading has steadily and strongly deteriorated, particularly in the second quarter itself.

Comparing the trailing 4-quarter to 8-quarter averages shows clear deterioration across the board, except for prices. That clarifies the overall story and trend for retailing.

The retail rankings are uniformly weak, with the exception that the selling price has a 43.6 percentile standing, which is still below its historic median ranking. However, the standings for imports, capital spending, and employment are all below the 10th percentile, with the business situation coming in an 11.4 percentile standing. The expected selling price has a 63.6 percentile standing, well above its historic median (the median occurs at a ranking of 50%). Meanwhile, employment, looking ahead, has only a 2.9 percentile standing, clearly not much of a vote of confidence in the outlook for the economy.

The wholesaling portion of the distributive trades report also registers weak standings, but they are higher than those seen in retailing, with the business situation at an 18.6 percentile standing, imports at a 25.7 percentile standing, and employment at a 17.1 percentile standing, while capital spending plans are at a very weak 5.7 percentile standing. All these metrics are generally stronger than for retailing; they're still poor readings and generally below their respective medians. The only exception is the selling price with a 77.9 percentile standing, which is only a vote of confidence for inflation. The expected selling price compared to a year ago has a 44.3 percentile standing, while employment expectations compared to a year ago are at a 35-percentile standing.

Similarly, in wholesaling as for retailing, the comparison of 4-quarter to 8-quarter averages shows across the board deterioration, except for prices. The distributive trades sector for retailing as well as for wholesaling is fading.

Summing up The United Kingdom distributive trades survey is telling us clearly that it is a weak environment for the distributive trades. The standings of the current readings are weak, and the outlook and forward-looking portions of the survey are weak as well. The economy continues to fight inflation that has been over the top for some time, and inflation is still above target, keeping the BOE inflation-vigilant. Global conditions are mixed with the cutoff of goods shipments through the Straits of Hormuz impacting economies globally. The second quarter survey is a depressing statement on the state of the outlook for the U.K. economy.

Asia

Asia