Global| Jan 06 2026

Global| Jan 06 2026S&P Total PMIs A Mixed Bag As 2025 Ends

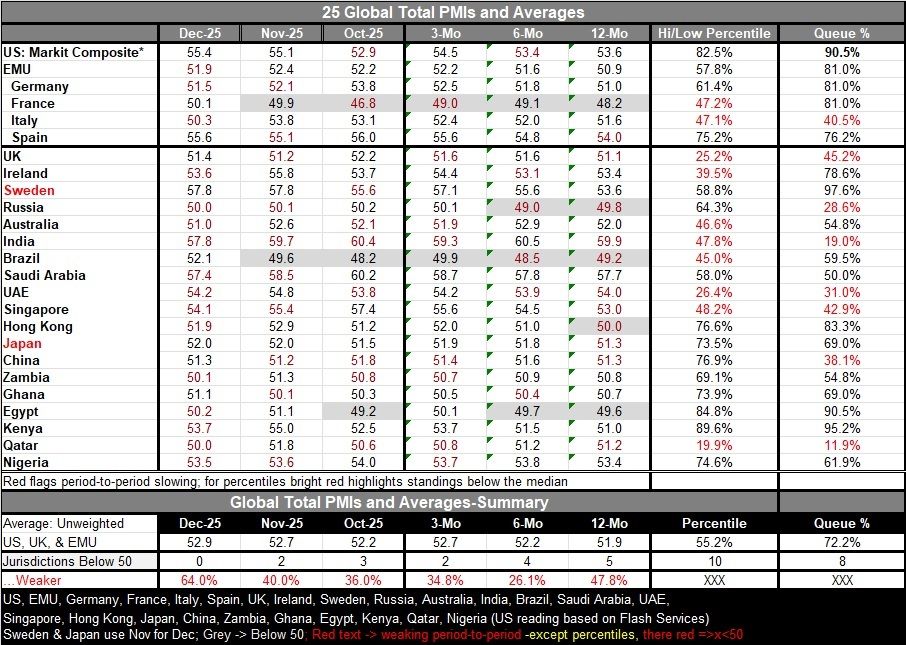

The S&P total or composite PMIs demonstrated a tendency to weakness in December as 64% of the 25 reporting countries reported weaker readings in December than in November. However, even with that bit of bad news on the table, the number of jurisdictions that reported PMI readings below 50 indicating economic contraction had gone to zero, indicating that there were no contracting jurisdictions in December. That's an improvement from two contracting in November and three in October. In those previous months, for example, in October, only 36% of the reporting entities were weaker month-to-month; in November, only 40% were weaker month-to-month so the step up to 64% weaker month-to-month in December was a big step-up in weakness; however, it comes after a period when conditions had generally been improving and now that has stopped.

Sequential trends: 12-months to 6-months to 3-months Sequential data that look at performance over three months, six months and 12 months compared to earlier periods show that, over three months only 34.8% of the jurisdictions were weaker compared to six-months. Over six months only 26.1% were weaker compared to 12-months. However, 12-months was a period of treading water because over 12 months compared to 12-months ago, about 48% of the reporters were weaker indicating that conditions over the past year had been largely unchanged. But over shorter periods of time conditions had been improving.

Contraction is less common At the same time, sequential data showed that there has been an improvement in terms of the number of jurisdictions that are showing contraction because there were five of them over 12 months, four of them over six months and only two of them over here months.

Standings/rankings The queue percentile standings show eight jurisdictions below 50% which means that on data from January 2021, only eight of the twenty five reporters are below their median result for that period. Egypt, Kenya, Sweden, and the United States have percentile standings in their 90th percentile marking them as very strong composite standings compared to where they have been over the last five years. There were also strong rankings in a relative sense in Western Europe with the European Monetary Union in its 81st percentile, Germany in its 81st percentile, France in its 81st percentile, and Hong Kong in its 83rd percentile, indicating strength spread across various areas but concentrated in Europe. On the weak side, there are extremely weak readings that are offered by Qatar that has an 11.9 percentile standing, in India that has a 19-percentile standing, the UAE with a 31-percentile standing, and China with the 38th percentile standing. These are relative standings that is they are not a ranking of the PMI values compared to other countries, but rather comparing to each individual country over the whole time series of values since January 2021 with its own performance. China, for example, has a 51.3 composite reading for December 2025, and while that's roughly a lower 1/3 reading compared to where it's been historically, it isn't a particularly weak reading compared to what other countries are reporting in December 2025. China, for example, ranks 17th out of 25 countries (approx. bottom one-third position) reporting data in December 2025. In the case of China, its timeseries and cross-section standing are very similar in ranking terms.

Summing up The bottom line for the PMI data at the end of 2025 is that conditions are still only moderate. There has been a sizable improvement through the year. However, there is some backing off occurring both in manufacturing and in services as the year has drawn to a close. Some of that may reflect the delayed reaction to the tariffs that the United States put in place. U.S. economy itself faced some adverse shocks at the end of the year. However, based on data we have in hand, it looks like the economy managed them fairly well and continues to grow reasonably robustly. Looking ahead to 2026, the U.S. economy will be riding tailwinds because of fiscal changes that are already agreed to and just taking effect. Inflation, globally, is largely moving sideways but largely doing it at a pace that is higher than central bank targets and that is going to be a major question mark for the year ahead. Will inflation calm down, or speed up, and what do central banks intend to do to deal with inflation for the year ahead?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief