Global| Jan 07 2026

Global| Jan 07 2026Inflation in the Euro Area Is Warm but Well-Behaved at Year-End

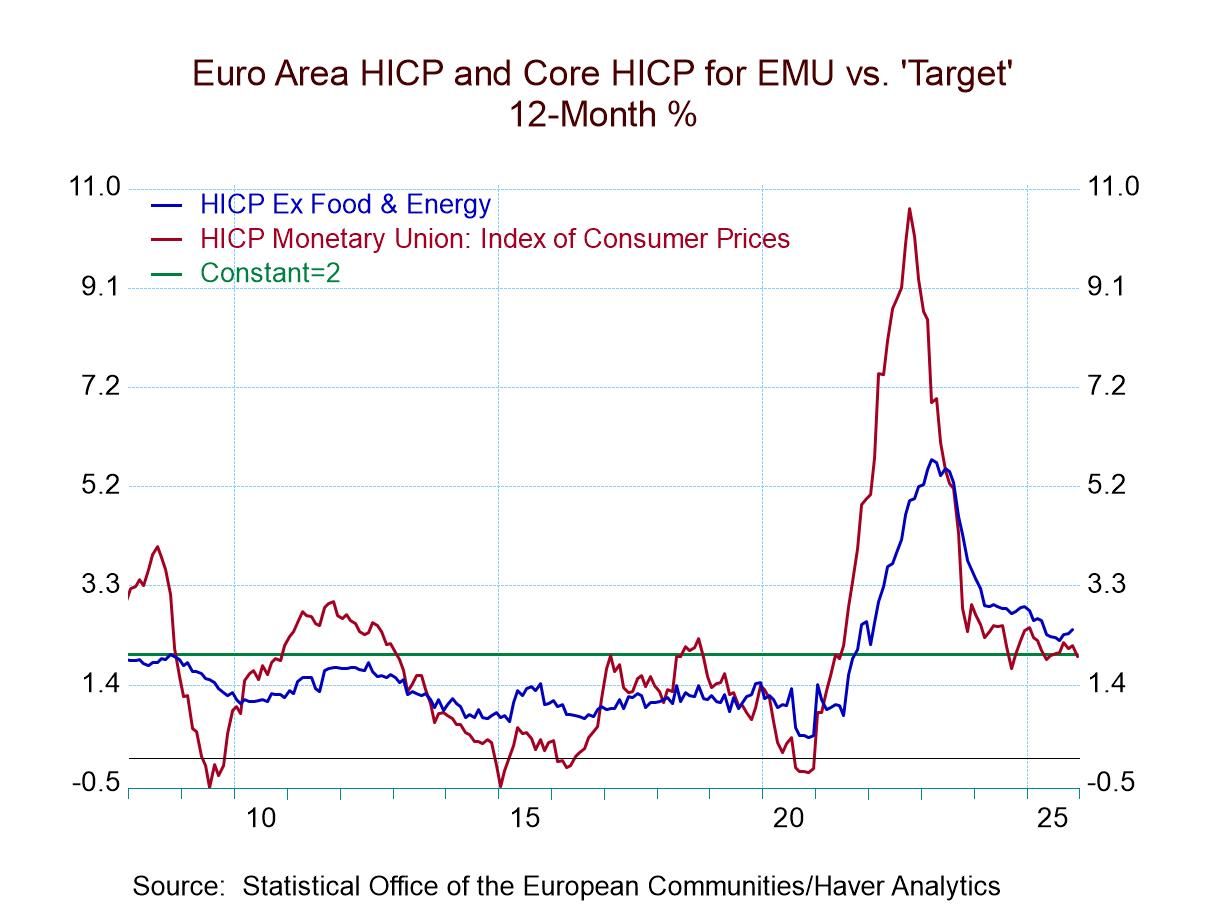

Inflation in the euro area as 2025 draws to a close has pretty much behaved. The HICP gauge for the European Monetary Union, that's targeted at a pace of 2% is closing the year with a 12-month pace of 2% which is exactly what the ECB is looking for. Success is at hand! Congrats to the ECB!

It’s like the super bowl playoffs: a victory, but more games lie ahead However…oh yes there is almost over an ‘however’ or ‘none-the-less’ or some other insidious phrase inevitably is inserted to introduce a caveat… and that is this: over six months the headline pace is at 2.4% at an annual rate, and over three months the pace is at 2.2% at an annual rate. Still, the year-over-year inflation rate is how central banks normally are judged and it has come in right on target, and the ECB can claim a large measure of victory for that even as it faces the challenge for 2026.

Visiting 2% or setting down roots? At the same time, inflation is only closing in on the 2% target over other horizons. It has not generally proven itself to be stable at 2%, having spent most of its time at a pace above 2% for the past year as the chart shows.

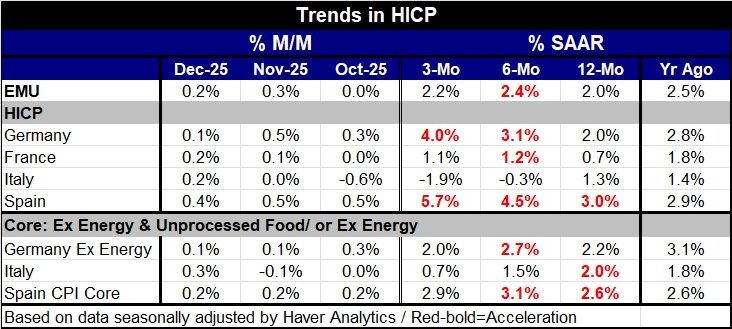

So far so good... The monthly numbers have been encouraging with the December gain in the HICP at 0.2%. Germany logged a gain of 0.1%, month-to-month, France and Italy had gains of 0.2%, while Spain is at 0.4%. Spain, where inflation had been pretty-well contained, has now moved over to the rogue side of the ledger. Spain posted inflation at 3% year-over-year, at a 4.5% annual rate over six months, and at a 5.7% annual rate over three months. Other monetary union countries showed more disciplined patterns. For example, France has a 0.7% gain year-over-year with a 1.2% annual rate gain over six months, and a 1.1% annual rate gain over three months. All of them, of course, are gains well within the ECB's desired result for the union as a whole. Italy shows a tendency toward deflation at a 1.3% HICP gain over 12 months that shifts to a decline of 0.3% at an annual rate over six months, and to a decline of 1.9% at an annual rate over three months. The other troublesome country among the Big-Four economies in EMU is Germany where the 2% headline achievement over 12 months is right on top of the target the ECB seeks; however, it gets there with a 3.1% annual rate increase over six months and a 4% annual rate of increase over three months. Both of those gains, of course, are over the line and indicate accelerating inflation even as German inflation ends the year at 2% and is ‘seemingly’ compliant.

Core inflation is a slightly different animal Germany gives us an early look at inflation excluding energy. Italy and Spain give us core measures to look at early in the year. The December results show ex-energy inflation in Germany at 0.1% month-to-month, Italian core inflation at 0.3%, and Spanish core inflation at 0.2%. This followed a batch of similarly well-behaved numbers in November for these three countries (see Table). The core sequential inflation rates are generally better behaved for these three countries than for their headline rates. Germany's metric excluding energy comes in at 2.2% for the year but it accelerates at a 2.7% pace over six months and then it's back down to 2% over three months. Italy shows a compliant 2% pace over 12 months, then it slides to a 1.5% annualized over six months and slips further to a 0.7% pace over three months, echoing the deflation trend that we see in Italy's headline pace. For Spain, the core also exhibits accelerating inflation trends to join what it reports for the headline as the year-over-year core pace is at 2.6%, the six-month rate steps up to 3.1% annualized, and stays in that neighborhood at a 2.9% annualized rate over three months.

EMU inflation overall is ‘good’ but short of ‘solid’ So, my assessment of inflation in the euro area is that it's certainly better than the performance we've seen in the United States, the United Kingdom and Japan. In Japan, policymakers are still walking on egg-shells trying to come to grips with accelerating inflation but wary because they are still emerging from a long stretch of deflation that they don't want to plunge themselves back into. The Japanese probably have the most difficult policy challenge of all the major currency central banks. The U.K. whose inflation numbers are not pictured here because it is no longer in the European Union also has some severe inflation trouble and it's facing more severe weakness in its economy, likely putting itself on a path to lower rates sooner than for other major central banks. But within the European Monetary Union, the year ends on target but with pressures percolating in the background and those pressures are almost uniformly to the upside with Italy being the major exception. Geopolitical tensions continue to gnaw around Europe's border with continued hostilities in Ukraine and, as 2026 lies ahead of us, it is clearly going to be a year with many of the same challenges that were faced in 2025 although challenges have a more mature nature. There's an expression that says, ‘the more things change, the more they stay the same.’ And that's probably true for the year ahead, except that even as things ‘stay the same’ they're going to introduce different quirks into the policy process that central bankers are going to have to deal with.

Inflation optimism: is it warranted? There is general optimism about inflation overall and this is largely because most countries have basically done what they can do with fiscal policy and fiscal policy throughout the G7 world is substantially bloated and needs to be reined in. It really can't be used to ignite a new round of inflation. At the same time, demographics have changed. The global economy finds its population aging and an aging population is one that's more prone to save than to spend. And so not only is the population growth slowing but the composition is changing in a way that might make inflation a little easier to corral. Except that an older population may lack productivity. Enter technology… tech changes, particularly with artificial intelligence, may be introducing factors that can increase productivity and also help keep inflation at bay. But at the end of the day, monetary policy around the world has generally been relatively accommodative, fiscal policy - for all of the constraints that it faces - is still not tight, and while demographics may favor a less spendthrift environment, and slower population growth overall, at least in the United States growth has not been damped. All of these issues are going to offer challenges for the future and for central bank policy making. The question is whether central banks, after the inflation surge in COVID, have really corralled inflation and are they prepared to keep it at or around its 2% mark? Or is inflation going to slip through its grasp again because policymakers have other objectives that are going to be put ahead of keeping inflation under control? That would be the big question for 2026. Inflation rarely corrals itself.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief