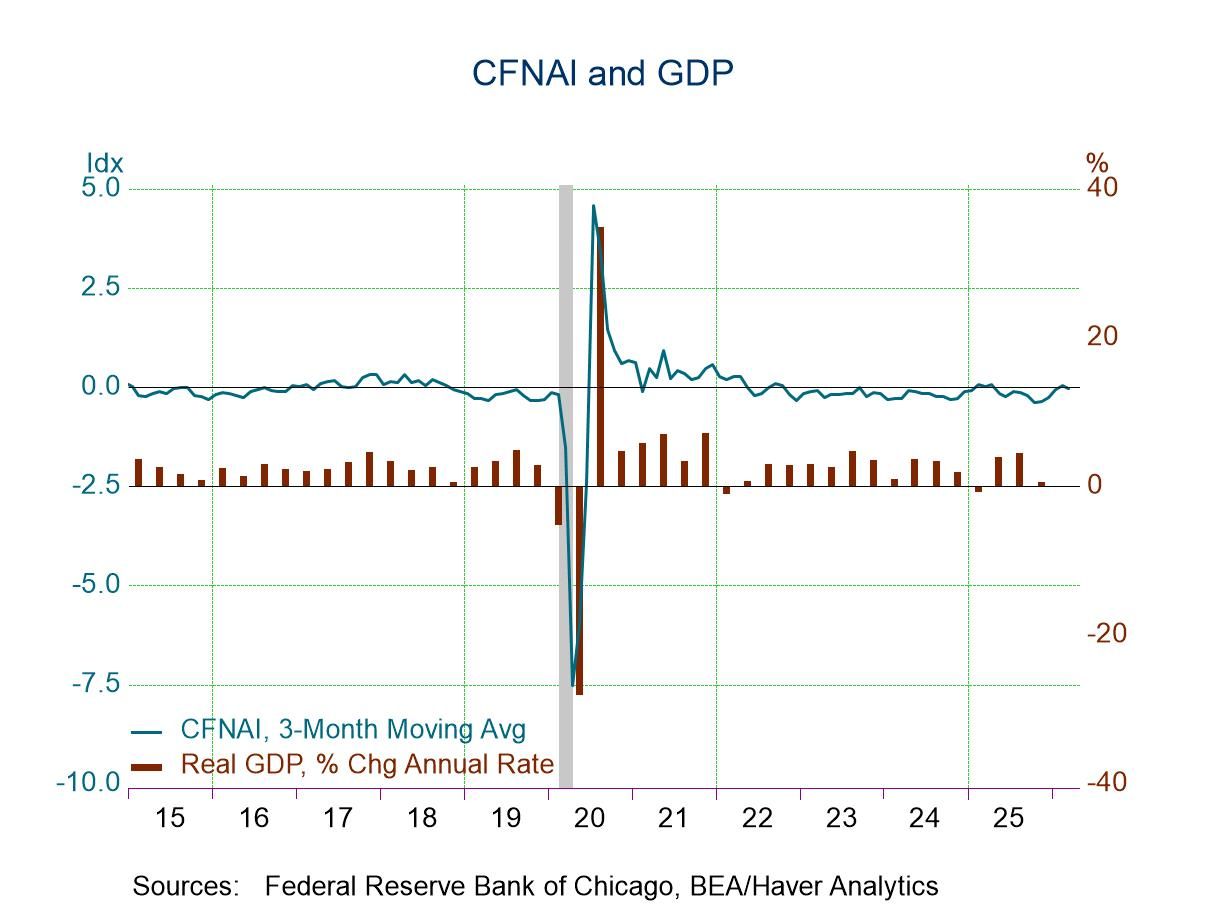

- The monthly reading fell to -0.20 in March from an upwardly revised +0.03 in February.

- The three-month average slipped from +0.03 to -0.03.

- Despite the slip in March, the index points to near-trend economic growth and is well above recession territory.

USA| Apr 23 2026

USA| Apr 23 2026Chicago Fed National Activity Index Slipped in March

by:Sandy Batten

|in:Economy in Brief

USA| Apr 23 2026

USA| Apr 23 2026U.S. Initial Unemployment Claims Rose in the Week of April 18

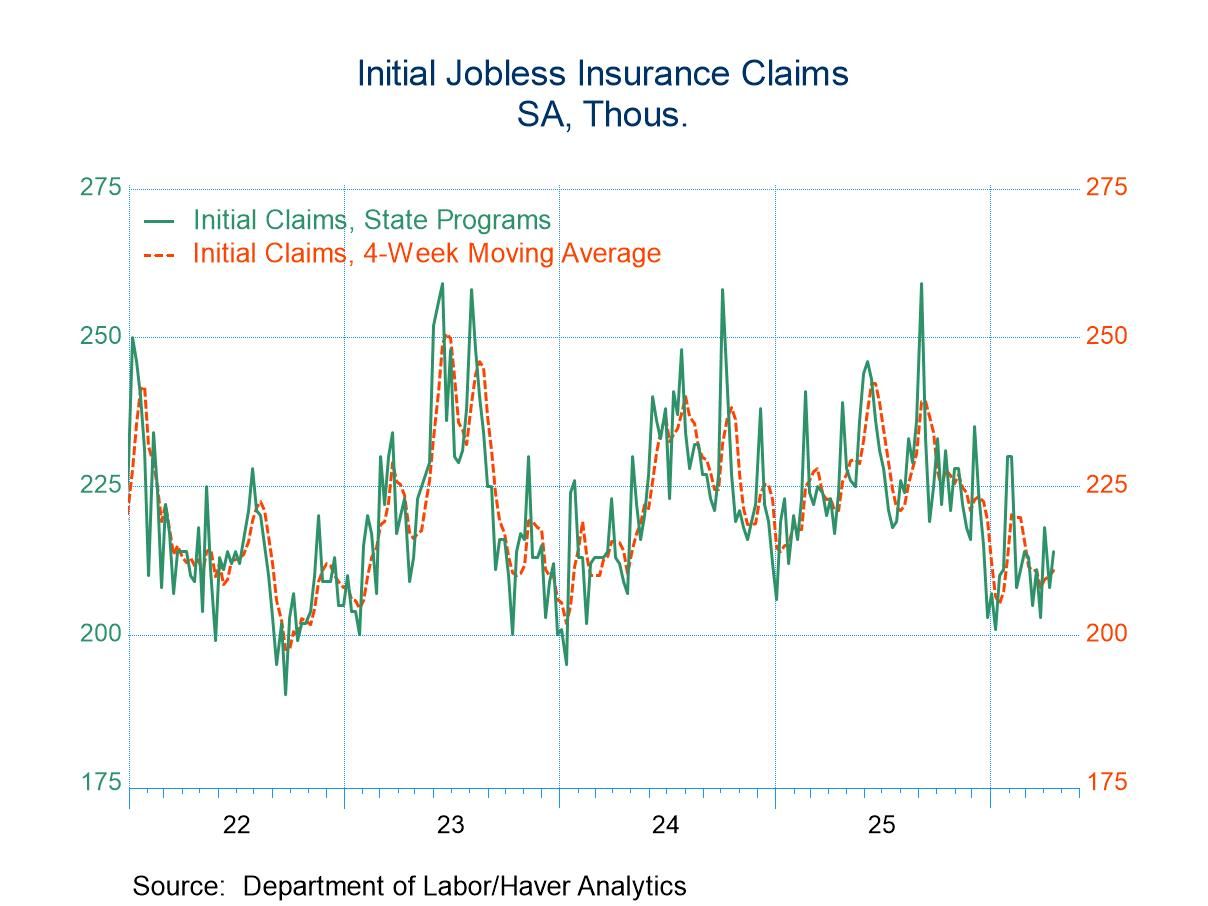

- New claims rose by 6,000 to 214,000.

- Continuing claims rose by 12,000 to 1.821 million.

- The insured unemployment rate remained at 1.2%.

Global| Apr 23 2026

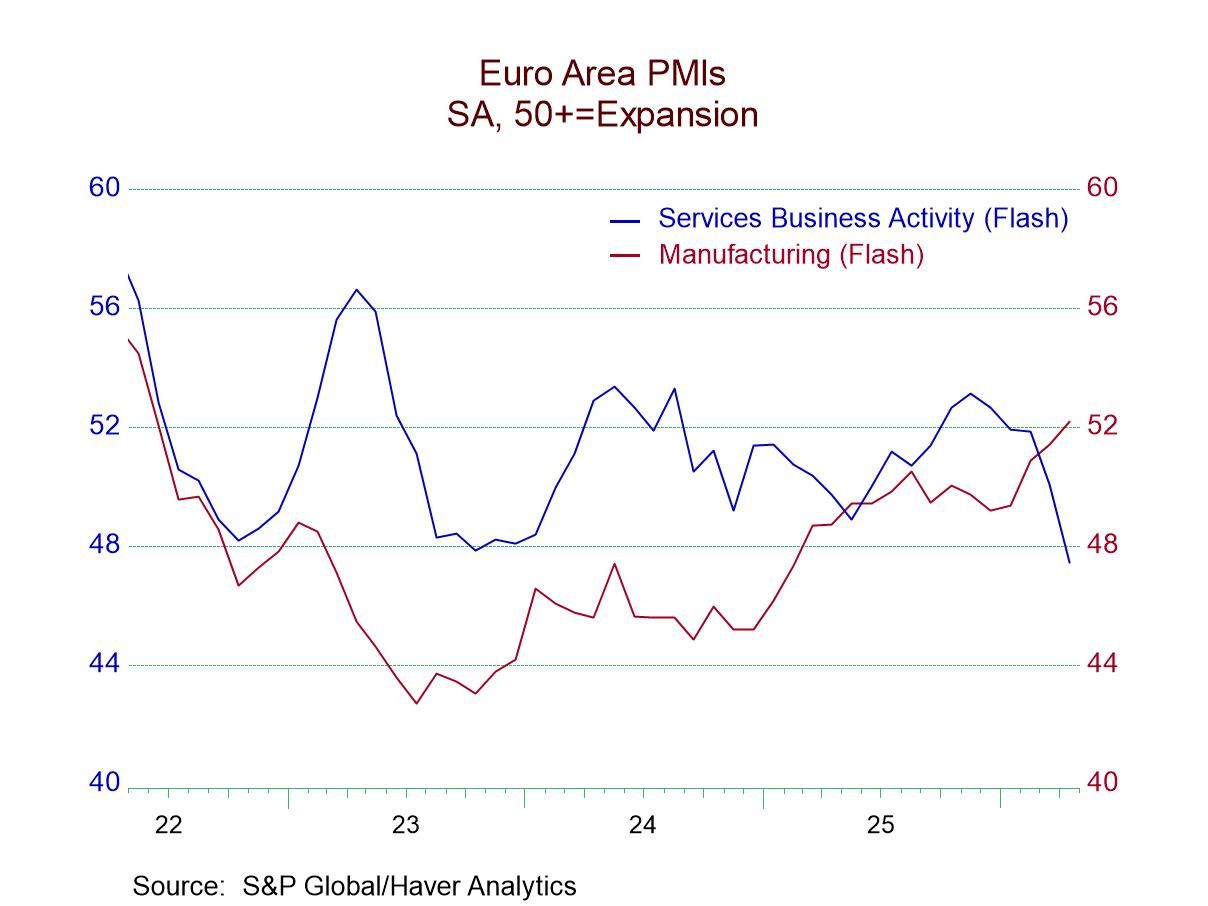

Global| Apr 23 2026S&P PMIs Show Mixed Fortunes

Manufacturing looks strong while service sectors weaken S&P's April flash PMI readings show some very mixed results. For the United States, India, Australia, and the United Kingdom, there is a strengthening in the readings month-to-month for services, manufacturing, and the composite.

For Japan, France, and the European Monetary Union as a whole, there is improvement in the manufacturing sector on the month but a weaker services reading and a weaker composite overall.

Germany is the only responding area in the table showing weakness all around—in all three sectors—a weaker composite, a weaker manufacturing sector, and a weaker services sector in April. For Germany, this follows a weaker composite and service sector in March as well.

Most reporters—France, the United Kingdom, Japan, Australia, and India—had weaker readings for all three metrics in March: the composite, services, and manufacturing. The March exceptions were the United States, Germany, and the European Monetary Union; in each case, the exception was that the manufacturing sector improved month-to-month, while the composite and services both weakened.

This has been a period of weakening—in March and April—since the war in Iran began. The 48 separate sector readings produced 30 readings that were weaker month-to-month in March and April. Among the 16 composite readings, 12 reported weaker conditions month-to-month. In March, the immediate aftermath of the outbreak of war brought instantaneous step backs across the PMI readings, while April, responding to at least a military success in the area, has shown a significant bounce back that is now more common than further weakness.

The sequential data over three months, six months, and 12 months are based only on completed data; therefore, they're up to date through March. On that basis, we have triple sector weakness in the U.S., India, and Australia, with only Japan and the United Kingdom showing triple-sector improvement over three months. However, if we look at six months compared to 12 months, we have triple sector strength in the Monetary Union, Germany, France, the United Kingdom, Japan, and Australia. India and the U.S. each show only one stronger sector over that comparison—services in India’s case and manufacturing in the U.S. case.

Ranking Peculiarity The ranking data take the current flash data and compare them to the history of observations back to January 2022. What is quite surprising is that, on that timeline, the manufacturing sectors of all the countries in the table—except for Australia and India—show manufacturing standings in their respective 80th to 90th percentiles. Meanwhile, services standings are typically in the 30th percentile or lower.

Odd Impact of War If the war in Iran has an impact on something, we would expect that to fall on the goods trade sector. We would expect this to have an impact on manufacturing although it's the opposite thing that's happening. Manufacturing is showing a revival, while services sectors are showing weaker performance across these countries generally. India is an interesting case, with manufacturing only in its 32nd percentile; however, India’s raw diffusion reading for manufacturing is the strongest raw diffusion reading in the table. What India's ranking is telling us is that India had been extremely strong over the period since 2022, and now compared to that past standard, it's relatively weaker. However, it's still strong in absolute terms, showing a great deal of strength based on its pure diffusion value, just not in comparison to historic performance.

USA| Apr 22 2026

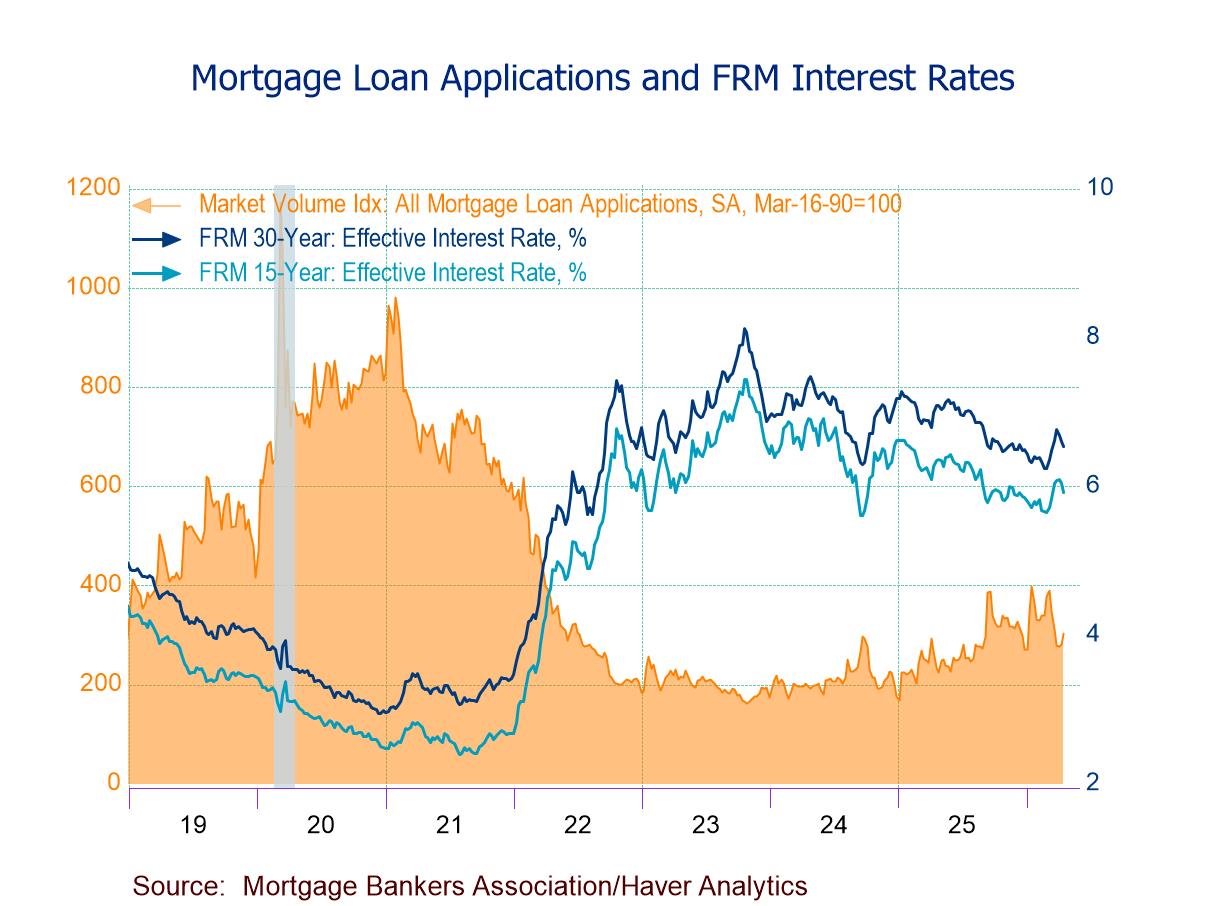

USA| Apr 22 2026U.S. Mortgage Applications Up 7.9% in the April 17 Week, Largest Gain Since Late February

- Purchase applications +10.1% w/w, biggest increase since the Jan. 9 week; refinancing loan applications +5.8% w/w, second consecutive rise.

- Effective interest rate on 30-year fixed loans down 7bps to 6.53%, a five-week low.

- Average loan size up for the third straight week, highest level since the March 13 week.

Belgium| Apr 22 2026

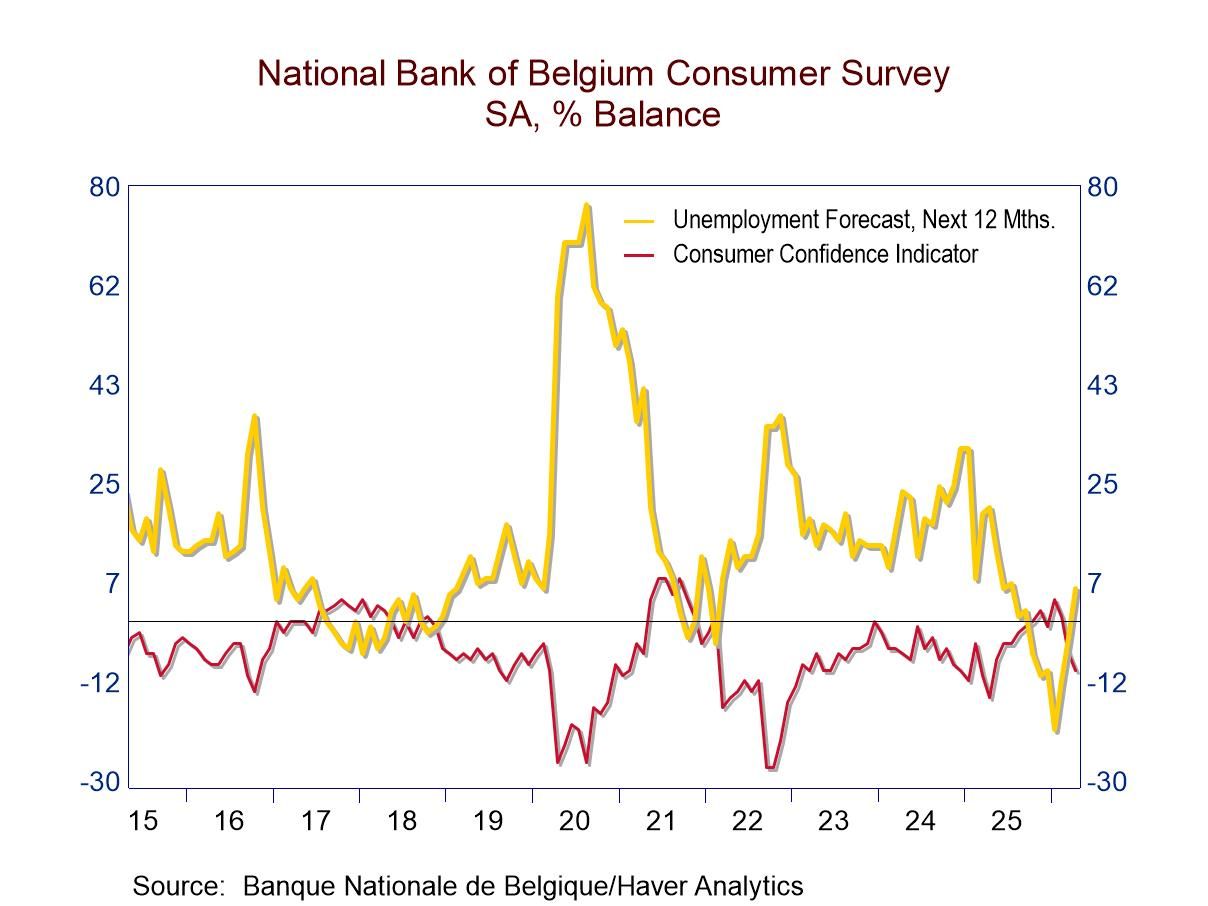

Belgium| Apr 22 2026National Bank of Belgium Consumer Survey for April

The National Bank of Belgium consumer survey for April registered -9, compared to a reading of -6 in March and +1 in February. Since the war in the Middle East began, confidence readings have declined steadily. However, the April consumer confidence reading of -9 still shows improvement from its level of -14 recorded 2 months ago. The index has a 37.8 percentile standing based on data back to 1991, which places it below its historic median: the median ranking occurs at a percentile standing of 50.

The responses to the survey are mixed and some of them are quite negative; however, a few also are quite upbeat. For now, the main message is that the survey is mixed. While most confidence readings tend to the weak side, there are a few that are actually quite encouraging.

Economic Situation A survey on the economic situation shows improvement for the next 12 months; its April reading rose to -43 in April from -45 in March. However, with the onset of war, the March reading had fallen to -45 from -25 in February, so the month-to-month uptick in April is really small potatoes. The 12-month change in the outlook for the economic situation over the next 12 months is a tick better in April 2026 than it was in April 2025. Continuing the back and forth on its “bad but not that bad” swing, the queue reading of the index on data back to 1991 has only a 1.8 percentile standing, marking it as weaker than its current level less than 2% of the time and ending the back-and-forth on whether the reading is poor or not. It is very weak.

The assessment of the economic situation over the last 12 months deteriorated to -57 in April from -42 in March, and it also worsened compared to its level of a year ago. In addition, its standing is in the bottom 8% of its historic queue data.

Prices Price trends give us some of the clearest and most negative views. Prices over the next 12 months improved slightly from March, moving to a reading of 50 in April from 53 in March. Still, the April reading of 50 is higher than its reading of 35 one year ago, and its standing is in the top 1% of all observations on data back to 1991. Those are dismal statistics. Price trends for the last 12 months are shown to have been slightly more stable but still with readings that had been historically worse, only about 15% of the time, marking the past inflation environment as having been poor as well.

Unemployment The consumers’ unemployment forecast went up in April to a reading of +6 from -3 in March; it had deteriorated to -3 in March from -11 in February. A rising unemployment response reflects deterioration. People are assessing the possibility of unemployment as getting higher, although at +6 the April reading is substantially reduced compared to what it was a year ago at +21. The standing for the unemployment forecast is only in its 16.7 percentile of its historic queue of data, meaning that the likelihood of unemployment has been lower than this, only about 16% to 17% of the time.

Major Household Purchases If you look at the environment to make major household purchases, the responses of consumers become slightly more convoluted since the question as to whether it's favorable to buy at present deteriorated sharply in April to -44 from -23 in March; that was a sharp deterioration from -20 a year ago. Ranking the current -44 reading on data back to 1991, this is the weakest or the worst favorability for spending on this timeline. So that particular sequence of data doesn't fit really well with the unemployment responses, although being unemployed and finding it's a favorable time to buy goods are different things; both do speak to the economic environment which we can see is somewhat touch and go.

The outlook for making major purchases over the next 12 months deteriorated slightly over the last few months, with a reading of -19 compared to -17 a year ago. That current reading has a 24.3 percentile standing, placing it in the lower quartile of its historic queue of data. This underlines that the spending environment has been poor throughout the last year compared to historic experience since the 1990s.

The Financial Situation of Households The financial situation of households over the next 12 months deteriorated slightly in April to -5 from -3, and it had deteriorated in March to -3 from -2 in February. Even so, the April reading of 5 was stronger than -8 recorded one year ago. Still, if we let the ranking on data back to 1991 be the arbiter of whether the assessment of conditions is weak, the 10.6 percentile standing for the financial situation ahead and the 12.2 percentile standing for the financial situation of households over the last 12 months both indicate decisive weakness.

The Current Situation The next reading is a bit of a surprise given the drumbeat of weakness that we see from the data above. The current situation appraisal did backtrack in April to 21 from 25 in March, but it's only slightly weaker than a reading of 22 in February. The April 2026 reading of 21 is slightly weaker than a reading of 25 one year ago. However, the April reading has a percentile standing on data back to 1991 at its 74.5 percentile, putting it right at the border of its top 25th percentile.

So, the current situation is appraised as a top 25-percentile standing, but the environment for making purchases over the next 12 months has a lower 24-percentile standing; and the current situation has a favorability for buying which is the worst that we've seen in the entire period. However, expectations of unemployment remain low. To round out this situation, the favorability to save over the next 12 months has a ranking in its 86-percentile, making it a top 15-percentile reading. The favorability to save at present has a 58-percentile standing, placing it above its historic median and slightly better than average. What we have are crosscurrents.

On balance, you see the consumers view their situation as having a lot of crosscurrents. In terms of the thing they fear the most, unemployment conditions are not considered to be at risk and the economic situation is appraised to be in the upper tier of where it has been since the 1990s even though the favorability of spending is the worst experience for consumers on that same timeline. But the inflation readings are unambiguously bad—and worsening.

It would appear from these crosscurrents that the Belgian consumer is ripe for being pushed one way or the other if events were to markedly either improve or to deteriorate.

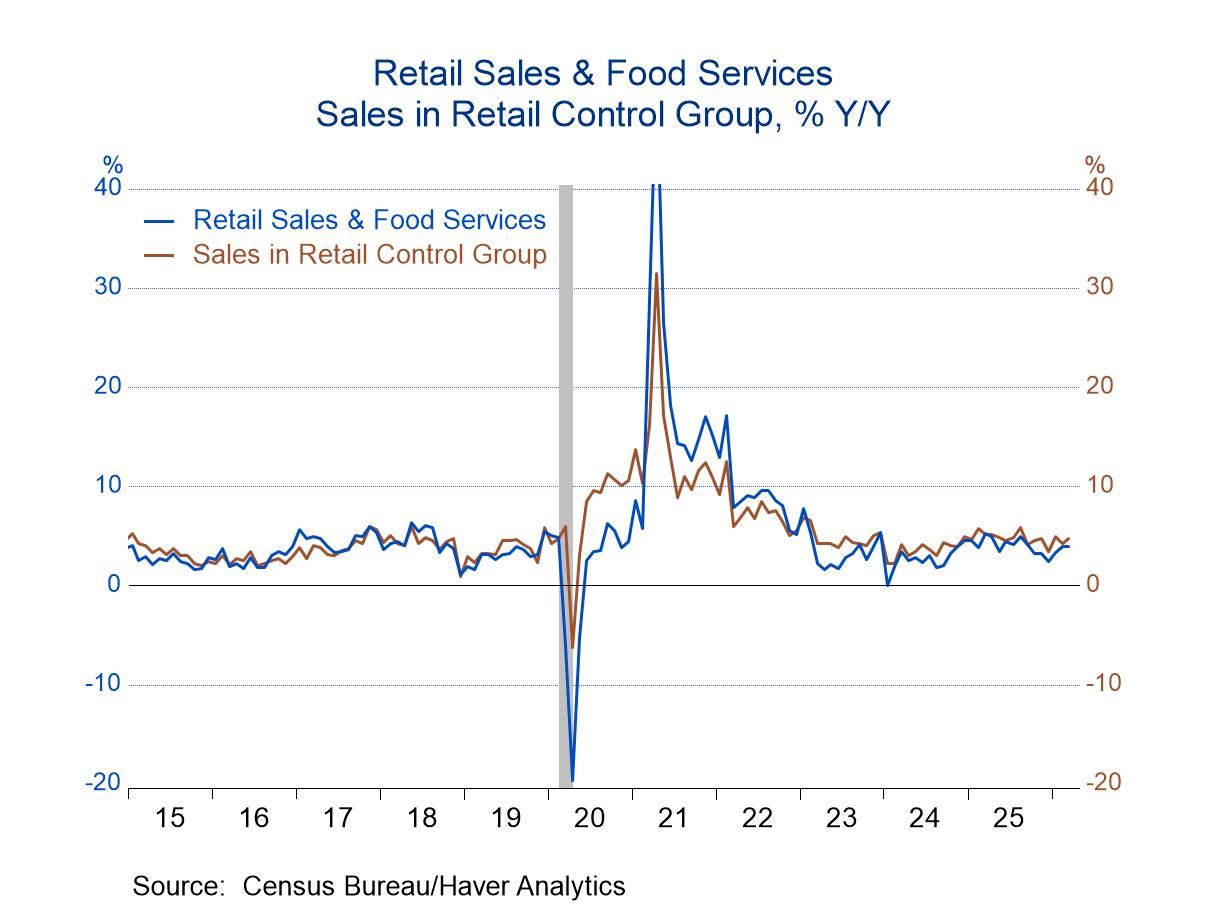

- Total sales jumped 1.7% m/m in March with small upward revisions to January and February.

- Gasoline sales surged 15.5% m/m in March, but even excluding that increase, the remainder of retail sales rose 0.6% m/m.

- Excluding autos, sales soared 1.9% m/m in March with small upward revisions to January and February.

- Sales of the retail control group that is used to construct PCE rose 0.7% m/m in March and 1.2% q/q for all of Q1.

by:Sandy Batten

|in:Economy in Brief

USA| Apr 21 2026

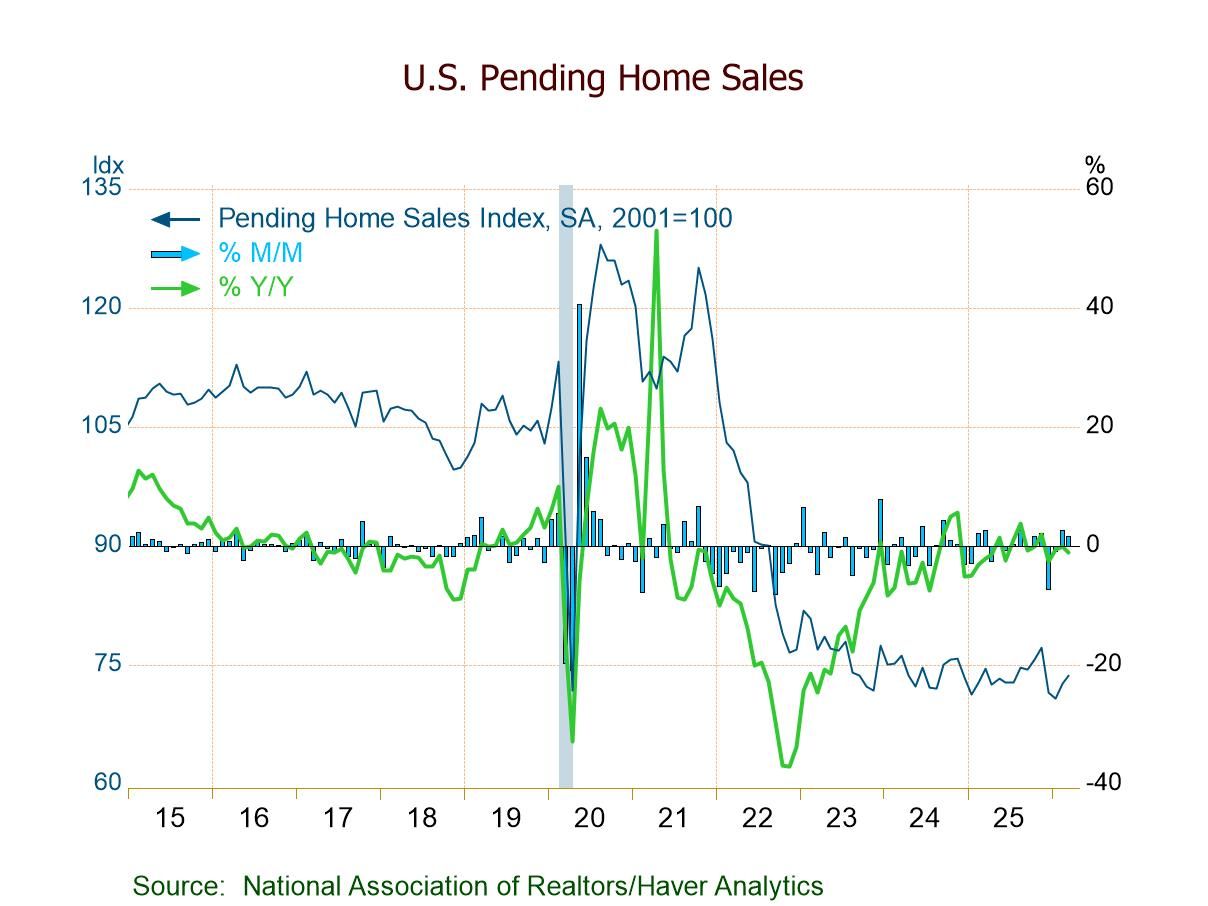

USA| Apr 21 2026U.S. Pending Home Sales Up for Second Consecutive Month in March

- PHSI +1.5% m/m (-1.1% y/y) to 73.7 in Mar., highest level since Nov.

- Home sales m/m up in the Northeast (+4.4%) and South (+3.9%); down in the Midwest (-1.3%) and West (-2.6%).

- Home sales y/y down in the Northeast (-6.5%), Midwest (-3.1%), and West (-1.7%); up in the South (+2.3%).

France| Apr 21 2026

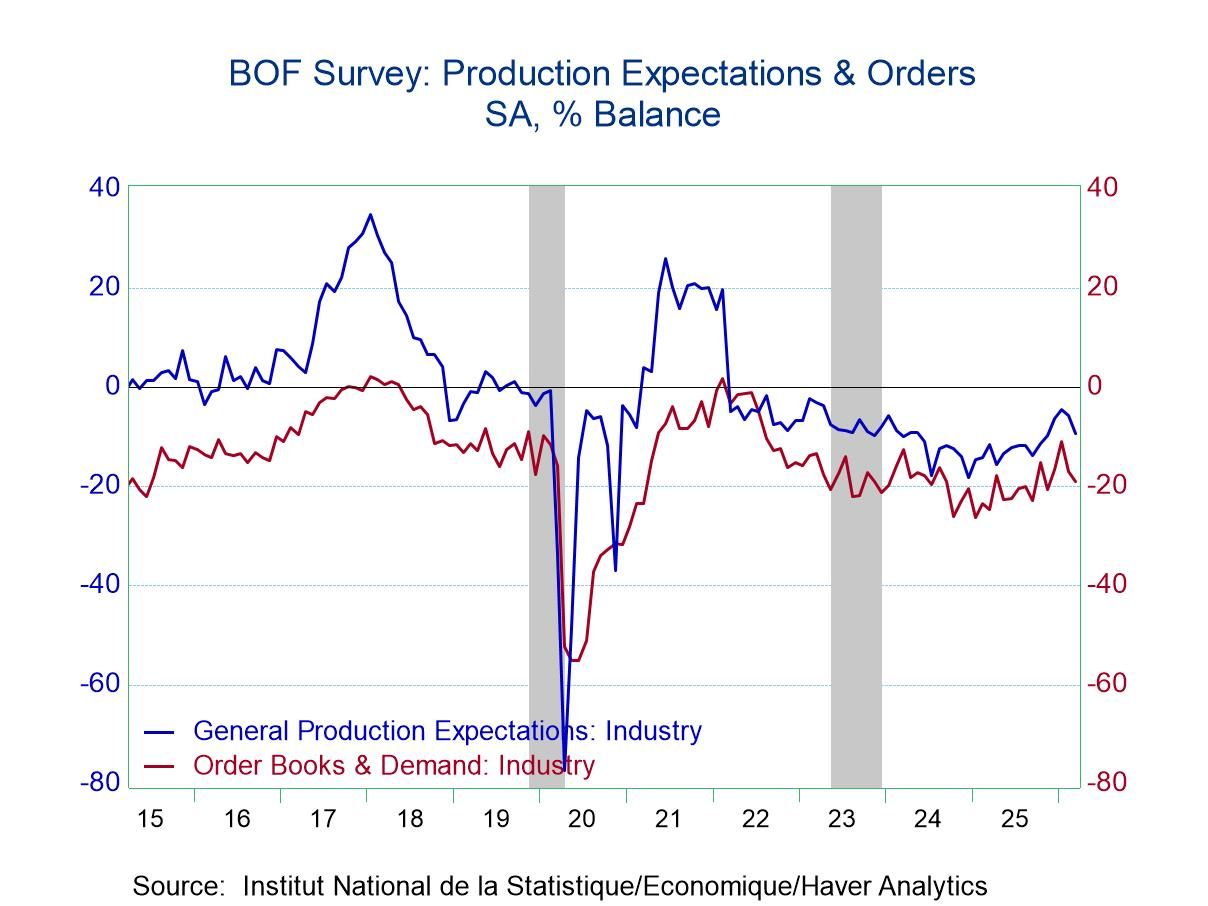

France| Apr 21 2026Bank of France Survey Advances in March

The overarching survey indicator for March stepped up despite enhanced global challenges. The March headline index rose to 99.3 from 98 in both January and February.

The March level of the headline compares to a 12-month average of 97.2. Nearly all the components in March are above their 12-month averages. The exception is the output change, which is substantially weaker than its 12-month average. Expected production, at 3.1 in March, is just a tick below its 12 month average of 3.2. Finally, expected employment in March is tied with its 12-month average.

In addition, only 3 readings weaker month-to-month in March were output change, expected production, and expected employment.

On the month, output change is a weak reading, falling by 3.5 points month-to-month; it may be the clearest example of the report showing weakness ahead, affected by upcoming global issues related to the war and rising oil and energy prices.

In addition to output change, expected production slipped to 3.1 in March from 4.8 in February. There was also a step back in expected employment, a modest one to 0.8 in March from 1.0 in February.

But order books showed a 10.2 reading in March, up from 5.6 in February. Changes in new foreign orders and total orders both showed more strength in March than in February, with foreign orders at 5.5 in March compared to 5.2 in February. The change in total orders, at 10.2 in March, was much stronger than 5.6 in February. Inventories registered 0.6 in March, up from -0.3 in February.

However, capacity space is being used up as capacity use rose to 77.0 in March from 76.6 in February.

The employment metric at 2.6 in March was much stronger than its zero reading in February.

On balance, the components indicate the sector is moving ahead as the headline gain suggests in March. But the major question mark is probably the strength in orders—which we take to be forward-looking compared to the setback in output change.

The index in March has a 64.1 percentile standing. Only three components in March ranked below their respective 50% marks (below their medians). The strongest readings generated standings in the 90th and mid-80th-percentile levels. These included finished inventories, the change in total orders, and order books. The lagging components, below their median values, were output change, expected production, and capacity utilization.

The French industrial readings are surprising for their resilience.

- of2725Go to 15 page