Asia| Oct 13 2025

Asia| Oct 13 2025Economic Letter from Asia: Gotta be Golden

This week, we highlight recent developments in China and Japan, alongside movements in gold and their relevance to Asia. Investors remained broadly unfazed after China’s “super golden week” holidays, with equities buoyed by AI optimism despite recent weak economic data (chart 1). US President Trump’s Friday threats of additional 100% tariffs, however, dented sentiment, with the escalation underscoring China’s delicate external environment. This week’s trade figures show a continued divergence, with exports to Asia still growing while those to the US slumped further (chart 2), amid a backdrop of subdued domestic inflation. Attention is also on the IMF’s upcoming economic forecasts for China. Past projections, including the IMF’s July WEO and the World Bank’s recent report, suggest sub-5% growth, though late-year stimulus has sometimes lifted growth above expectations (chart 3).

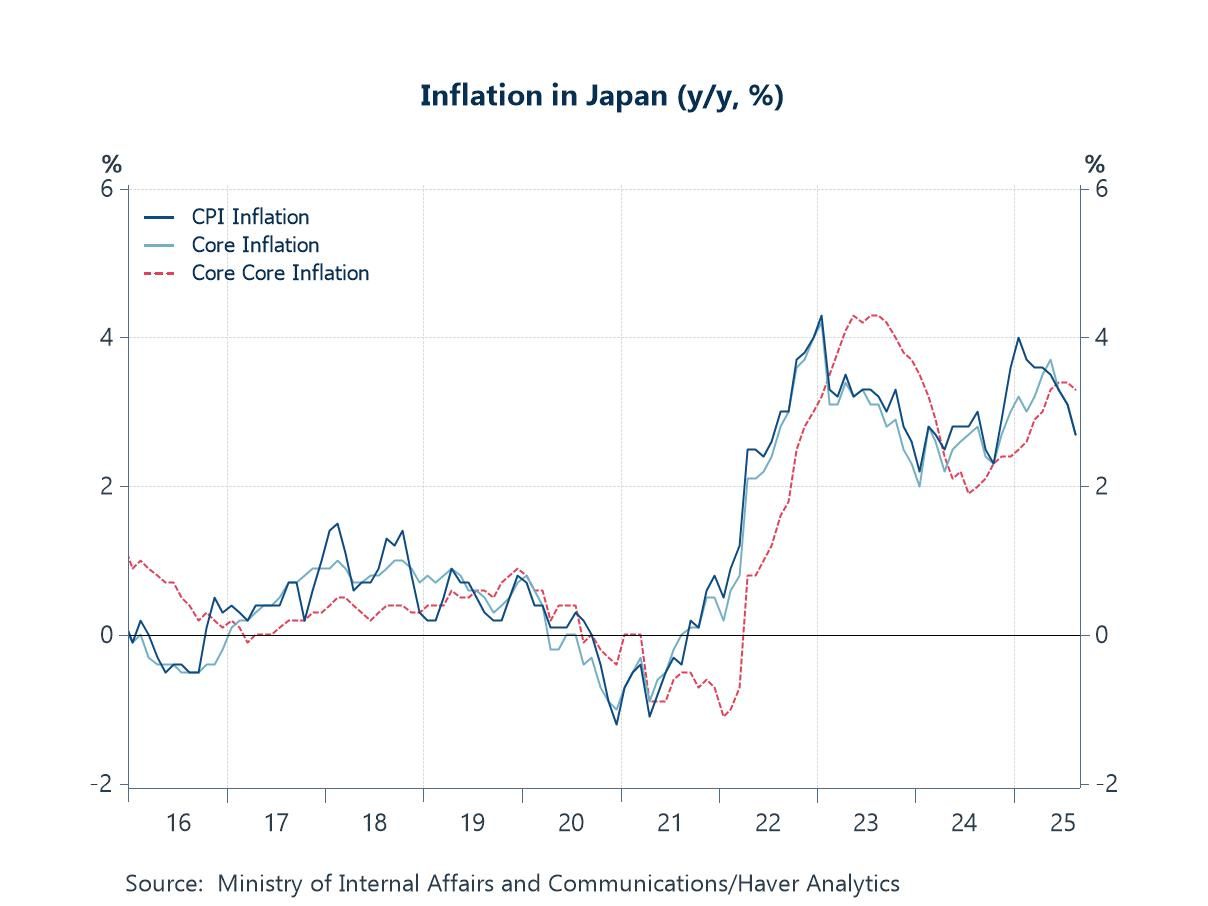

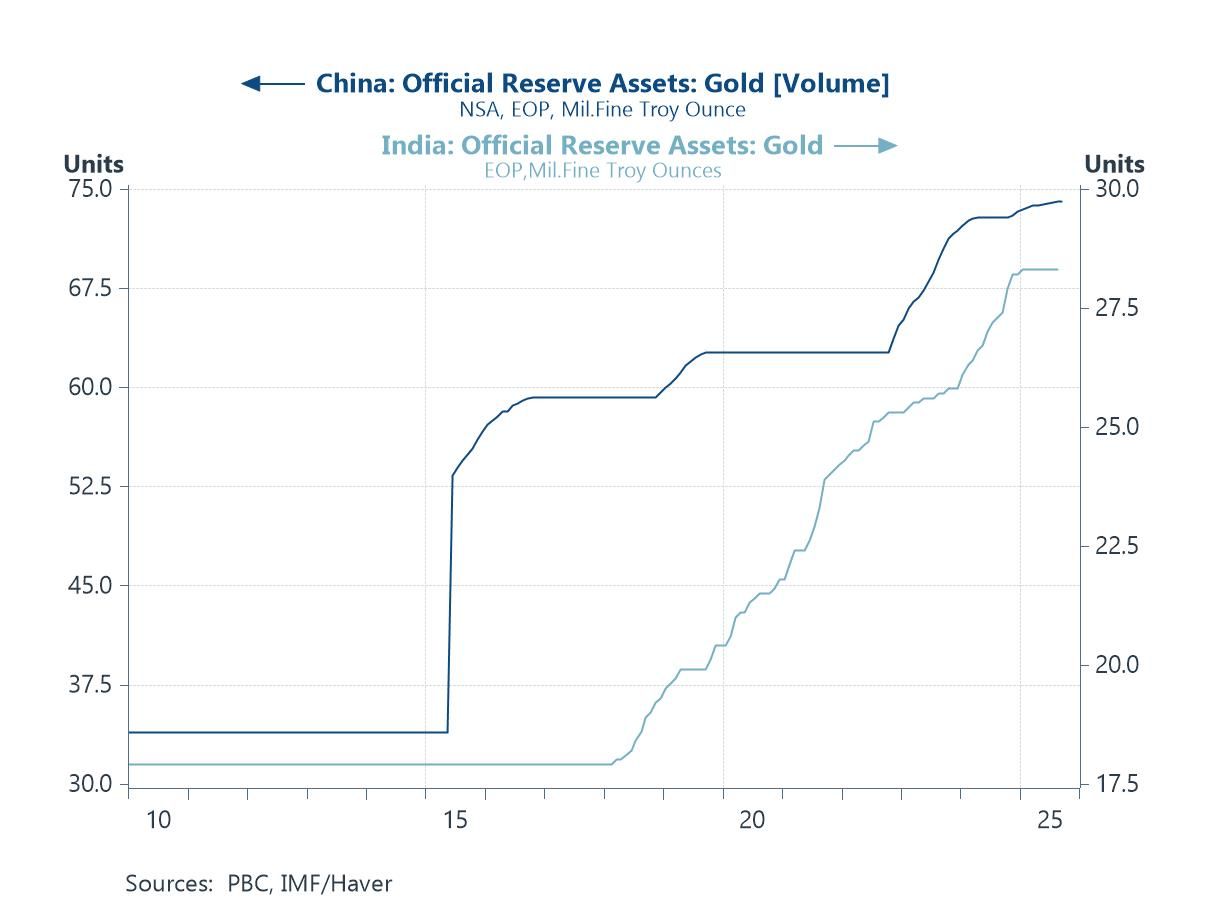

In Japan, Sanae Takaichi’s victory in the LDP leadership race positions her to become the country’s first female Prime Minister. Yet, the exit of long-time coalition partner Komeito has left much uncertain. Nonetheless, markets have priced in Takaichi’s pro-growth stance, with a weaker yen and rallying equities (chart 4), though rising inflation (chart 5) may constrain policy ambitions. As for gold, the precious metal continues to attract attention, with prices surpassing $4,000 per ounce. The rally has strengthened Asian currencies that are usually correlated with the precious metal, such as the Thai baht. A slower-moving but significant driver of the gold rally remains the accumulation of reserves by major Asian central banks, including China and India (chart 6), likely reflecting efforts to diversify away from the US dollar.

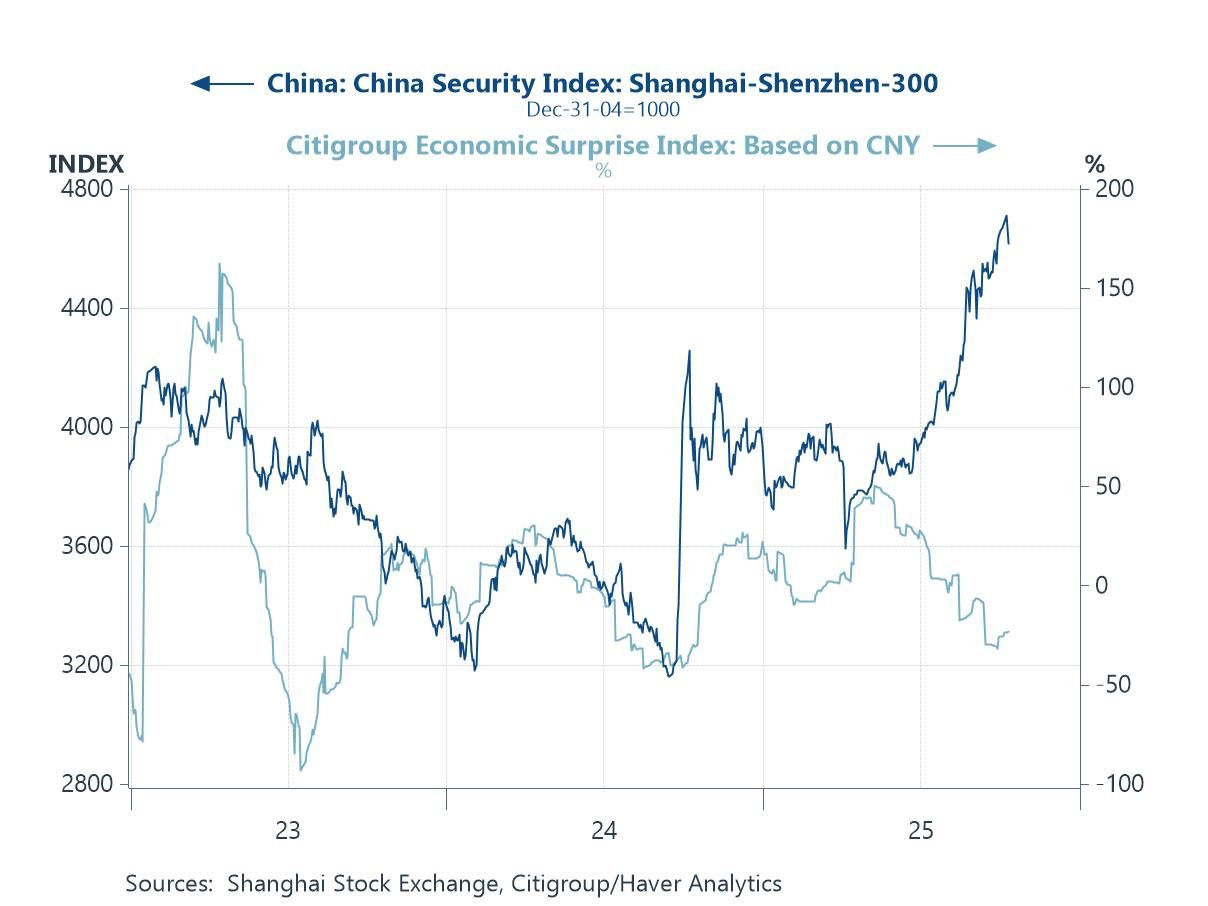

China China has just come out of its “super golden week”, an eight-day stretch of consecutive holidays from October 1st to 8th, resulting from the overlap of the National Day and Mid-Autumn Festival breaks. This extended holiday period was closely watched for a potential spike in domestic tourism, retail spending, and broader growth momentum. Preliminary data show that key retail and catering firms recorded a 2.7% y/y increase in sales, a notable slowdown from the 6.3% growth seen during the Labour Day break earlier this year. This suggests that consumer spending was more restrained during the recent holiday period. Given Beijing’s increasing emphasis on consumption-led growth over traditional drivers such as exports and investment, the health of Chinese consumers has become an ever more critical barometer of the economy. Nonetheless, following the reopening of financial markets after the holidays, equity market enthusiasm — buoyed in part by AI optimism — initially appeared undimmed, despite a weaker run of economic data (chart 1).

Chart 1: China equities and economic surprise

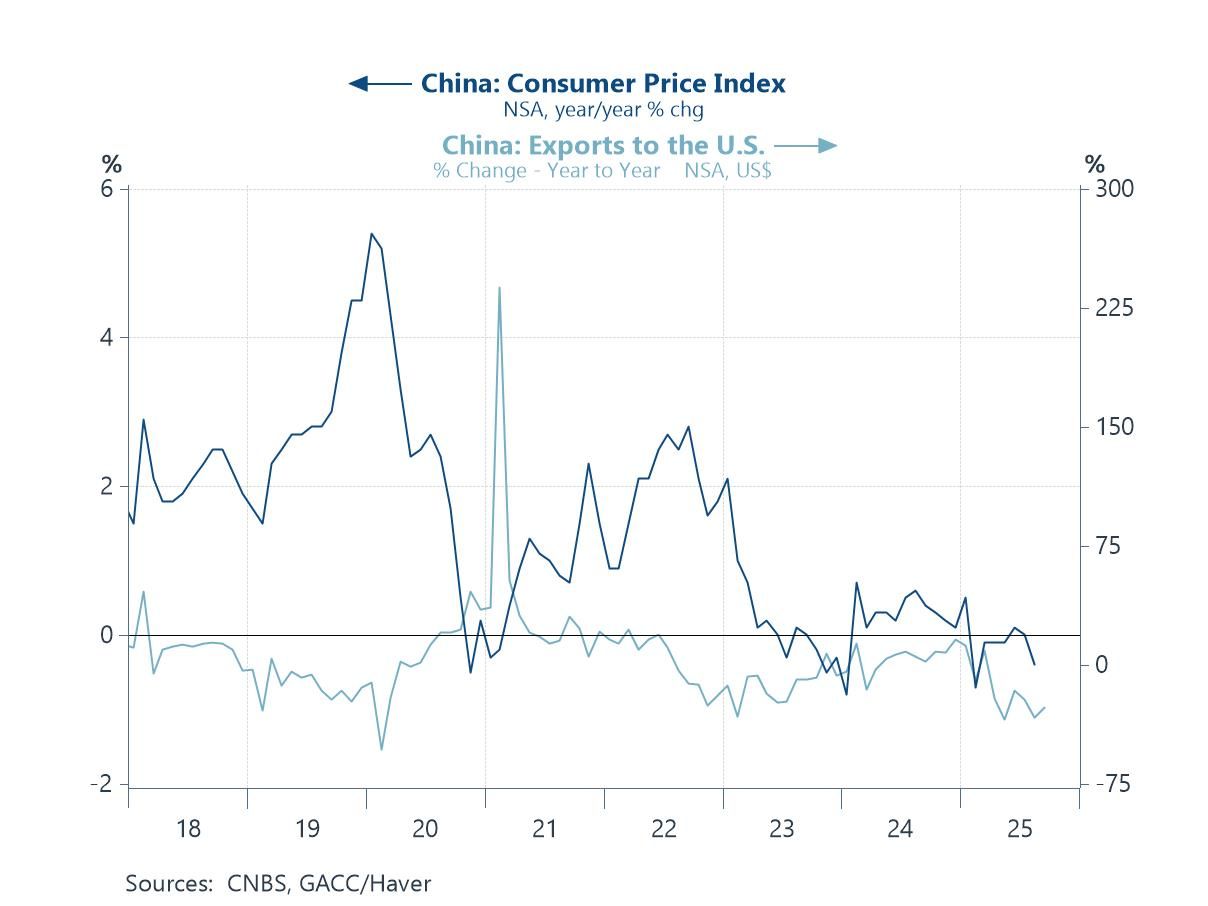

With that said, Chinese equity markets experienced a more recent dent in sentiment following US President Trump’s Friday threat to impose an additional 100% tariff on imports from China. The announcement also included new export controls on critical software, effective November 1st. President Trump cited recent Chinese actions — including sweeping curbs on exports of rare earths and critical minerals — as justification for the move. The flare-up in tensions, however, appeared to ease over the weekend after the US signalled openness to a potential deal on Sunday. These events serve as a reminder that external headwinds for China persist. The latest trade data show a continued divergence, with overall exports rising on stronger trade with Asia, while exports to the US continued to slump. Meanwhile, inflation in China remains subdued (chart 2), reflecting weak domestic demand and persistent oversupply.

Chart 2: China CPI and exports to the US

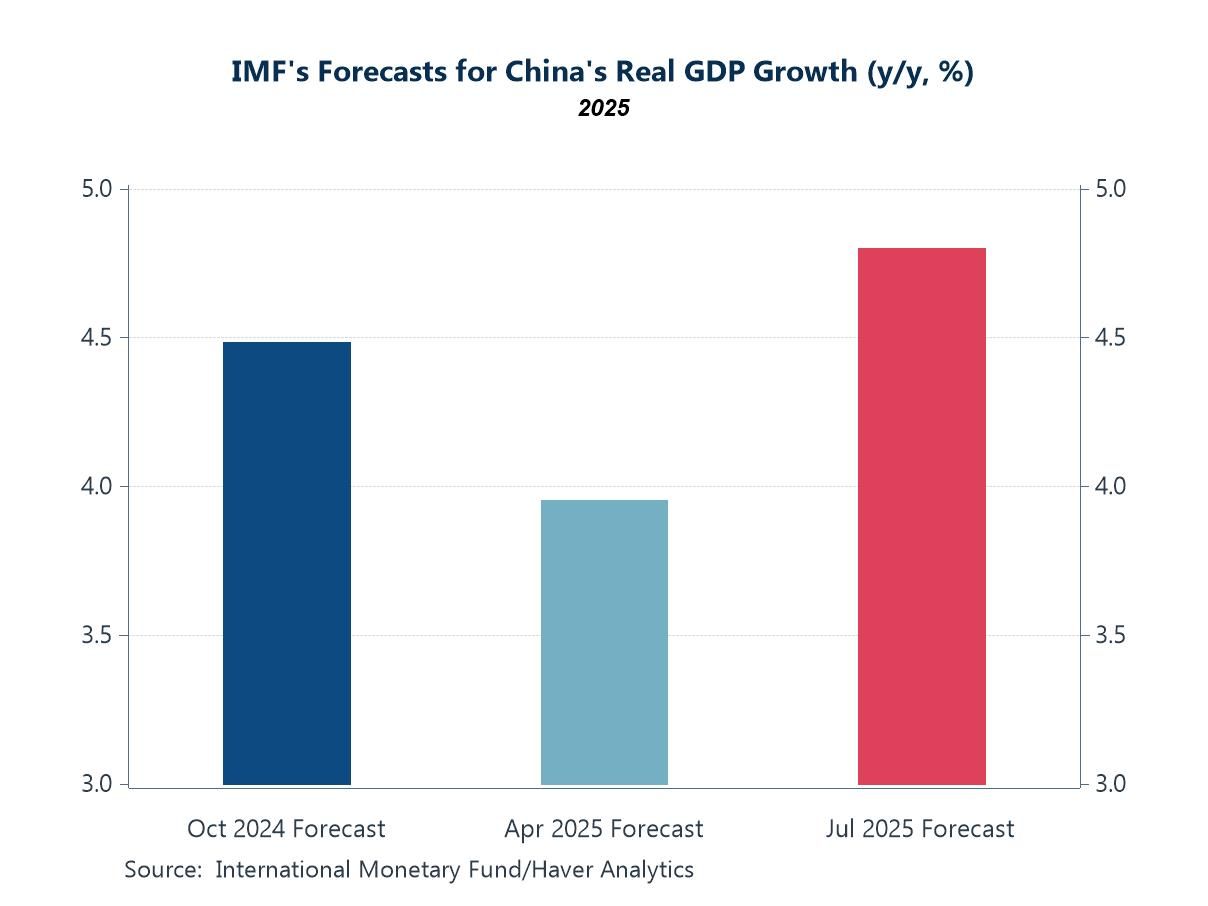

This prolonged lack of inflation has prompted calls from IMF Chief Kristalina Georgieva for a fiscal package aimed at boosting private consumption and reflating the economy. Her remarks come ahead of the IMF’s updated World Economic Outlook, due for release on Tuesday, October 14th. Even before this October update, the IMF (via its July WEO update) and the World Bank (via its October East Asia and Pacific Economic Update) had revised their China GDP forecasts. Both institutions raised their projections for the year from about 4% to 4.8%. Barring the IMF’s forecast update this week, these prior projections suggest that China is unlikely to hit its 5% growth target this year. That said, it is worth noting that China has previously defied expectations of missing its growth target, thanks to late-year stimulus measures that can lift economic growth.

Chart 3: IMF forecasts for China’s real GDP growth

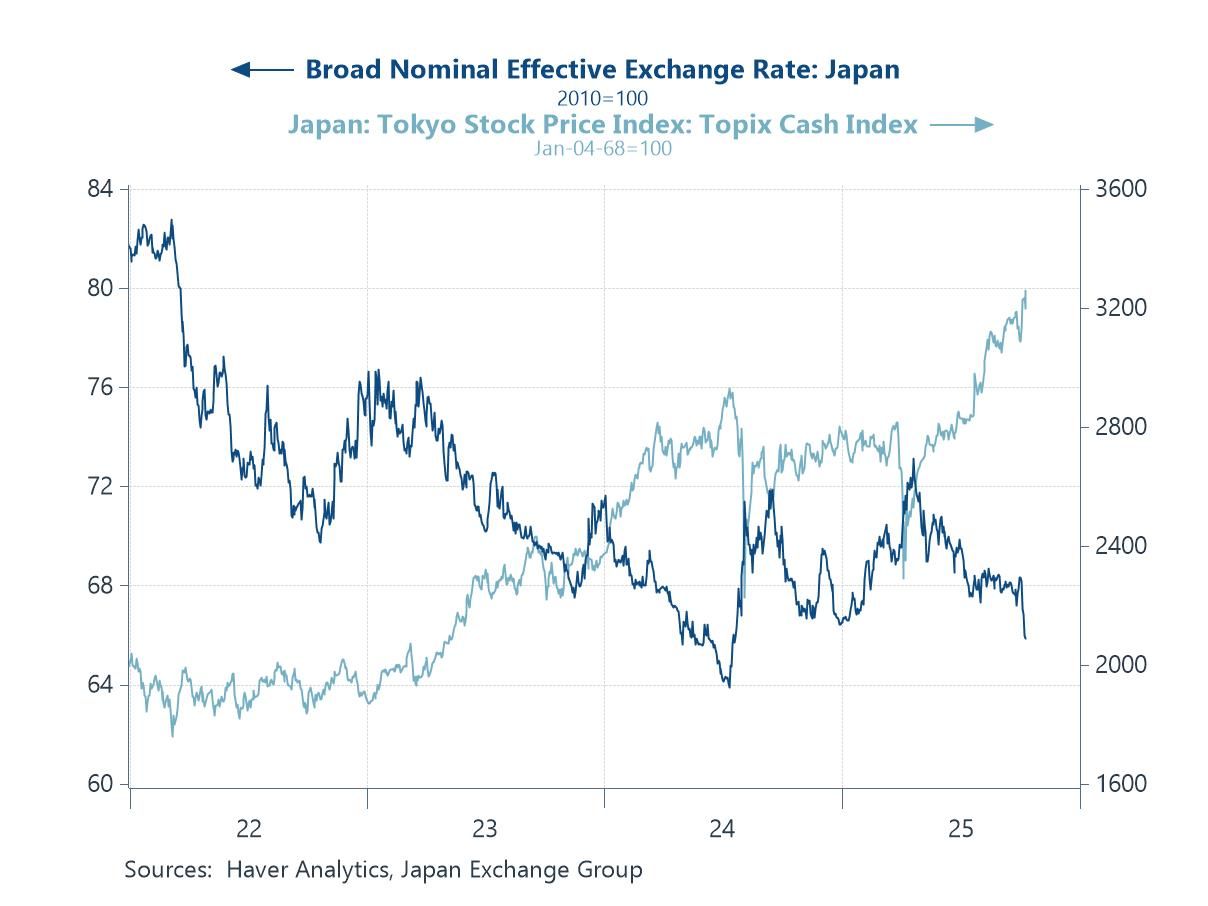

Japan Following Prime Minister Ishiba’s resignation announcement, Sanae Takaichi won the ruling Liberal Democratic Party’s (LDP) leadership race, positioning her to become Japan’s first female Prime Minister. A slim risk remains, however, that this may not occur. Attention now turns to an extraordinary parliamentary session, expected from October 20th, to formally elect the country’s next leader. Much remains in flux — from the composition of Japan’s new cabinet to the shape of its ruling coalition — amid competing policy priorities among potential partners. The latest uncertainty stems from the withdrawal of Komeito, the LDP’s coalition partner for 26 years, leaving the structure and direction of the government less certain. Nonetheless, markets have already begun pricing in potential shifts under Takaichi’s leadership. The yen has weakened sharply, while Japanese equities have rallied (chart 4), reflecting expectations that she will continue the late former Prime Minister Shinzo Abe’s “Abenomics” strategy of fiscal stimulus, loose monetary policy, and structural reform.

Chart 4: Japanese yen and equities

Eyes are also on the shape and scope of a potential supplementary budget that Takaichi may introduce to advance her policy agenda. This could include support grants for local governments and the abolition of fuel levies on gasoline and diesel, among other measures, although delays in forming a cabinet could slow progress. Externally, investors are watching Takaichi’s early engagements with major world leaders, given her stated openness to revisiting the US–Japan trade agreement, even as Japan’s relationship with China continues to evolve. Meanwhile, assessments of the Bank of Japan’s policy path are also likely to shift. Markets may perceive greater resistance to additional tightening if fiscal and monetary policies are aligned to further stimulate growth. However, the desire to maintain loose policy for longer could face constraints if inflation resumes its upward trend following the implementation of more accommodative measures (chart 5).

Chart 5: Japan inflation

Gold Turning to gold, the recent US government shutdown left policymakers and investors largely in the dark due to the absence of key data releases such as nonfarm payrolls. The disruption has also pushed gold prices to record highs, surging past $4,000 per ounce, with multiple implications for Asia. For instance, the Thai baht–gold correlation has driven the currency to appreciate sharply. This poses a challenge for Thai policymakers, as a stronger domestic currency weighs on tourism and exports, two of Thailand’s key growth drivers. More broadly, another factor underpinning gold’s gradual price appreciation over time has been central bank buying. Major central banks, including those of China and India, have been steadily expanding their gold reserves in recent years (chart 6). This trend is likely motivated by a desire to reduce reliance on US Treasuries, among other strategic considerations. Looking ahead, this trend of central bank accumulation is expected to continue, providing ongoing support for gold prices.

Chart 6: China and India official gold reserve assets

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief