German Exports Wither and Imports Drop

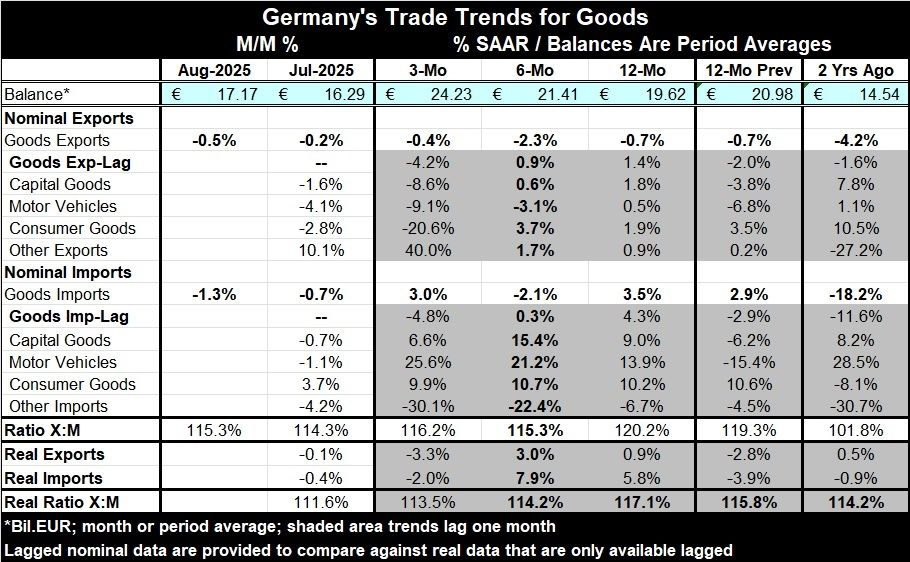

Germany shows signs of withering domestic demand in the face of weaker foreign demand. German exports weakened in August, falling by 0.5% month-to-month. The drop in German exports to the U.S. was being highlighted at a 2.5% month-to-month decline, but its exports to EMU members were down by 2.2% as well and exports to non-EMU members of the EU were lower by 3.1%. In fact, German exports outside the EU area rose by 2.2% largely on exports to China.

Exports to the U.S. vs. European trends The German website highlights a large drop in German exports to the U.S. from August 2024, a period over which German exports to the U.S. are off by some 20%. This is a much sharper drop than the German overall result that shows a decline of less than 1% over the past year for total exports. However, on the near-term comparison, German exports to the U.S. seem to be behaving a lot like German exports to its closer European neighbors.

World trade The Baltic dry goods index shows a sharp recovery in world trade volume (in dry goods; excluding tanker volumes) from a dip in early-2025. From early 2025 to date, trade volume readings on the Baltic index are among some of the stronger readings since 2022.

German orders imports, demand German orders data had also flagged weakness in external orders. Overall orders show weakness, but domestic orders remain strong and are accelerating. Still, the recent (August) IP report showed declines on the month and growing output weakness - despite strong domestic real orders. In today’s trade report, we are seeing some weakness in Europe and among the EU’s non-EMU members plus trade weakness with the United States. This is partly compensated for by strength elsewhere and a part of that is German exports finding some demand in China. All the geographical references are up to date through August.

Overall German trade patterns However, German overall trade showing German domestic import strength with real and nominal imports rising solidly and even strongly over 12 months and six months but giving some ground over three months. German nominal and real export trends are showing some growth except over three months but at that, the pace generally is weaker than the pace for imports.

Prospects: Looking ahead, prospects are uncertain. We have not seen a full year of U.S. tariffs yet and trade flows over the past year are distorted by lead and lag effects as exporters saw the U.S. tariffs coming and generally tried to squeeze as much into the U.S. ahead of the tariff imposition as possible. That activity beefed up pre-tariff growth and has sapped strength from post-tariff growth rates. Firms in the U.S. are now saying they have mostly run down their pre-tariff inventories. So in the U.S., we should begin to see pricing based in where tariffs are and we should also begin to see trade flows settle into new longer-run patterns. One caveat is that in the wake of all this tariff gyration and other U.S. policy shifts the dollar has gotten weaker. A weaker dollar could weigh against German export recovery in the future as well as weigh on the rest of the EMU.

The German economic scene The German trade, orders and industrial productions reports all seem to tell a common story of some new weakness in demand for German exports that incudes much of Europe and the United States. Germany’s own domestic demand, as revealed by real orders and imports, seems to be still stable. But Germany is an economy that relies on its international sales. Weakness in foreign orders and in German exports are not to be brushed off lightly. As a testament to that, industrial production is declining and showing progressive weakness despite solid German exports and strong real domestic orders. During this stretch ahead, we will watch export and demand trends closely in Germany and in Europe; we will also monitor closely what central banks are doing.

Fed policy will set the tone The Fed may be in a broader easing mode, but then there are also signs of growing restiveness or resistance to the notion of further Fed rate cuts because of stubborn U.S. inflation. Inflation became entrenched above target and stopped falling even when the Fed funds rate was higher, so some are wary of further cutting- especially with the brunt of tariff effects lying ahead.

While many are poised for a Fed easing cycle ahead, and that is one thing weighing on the dollar, that cycle is something that may not develop. Another rate cut from the Fed seems to be in the cards. After that, I think all bets are off. That could change the dynamics and the outlook for ECB policy as well. Global policy is in flux and much of it centers on policy in the U.S. But Europe, with a war on its doorstep and an increasingly adventuresome Russia, also faces important challenges and decisions. Nothing from here on out will be simple.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia