Global

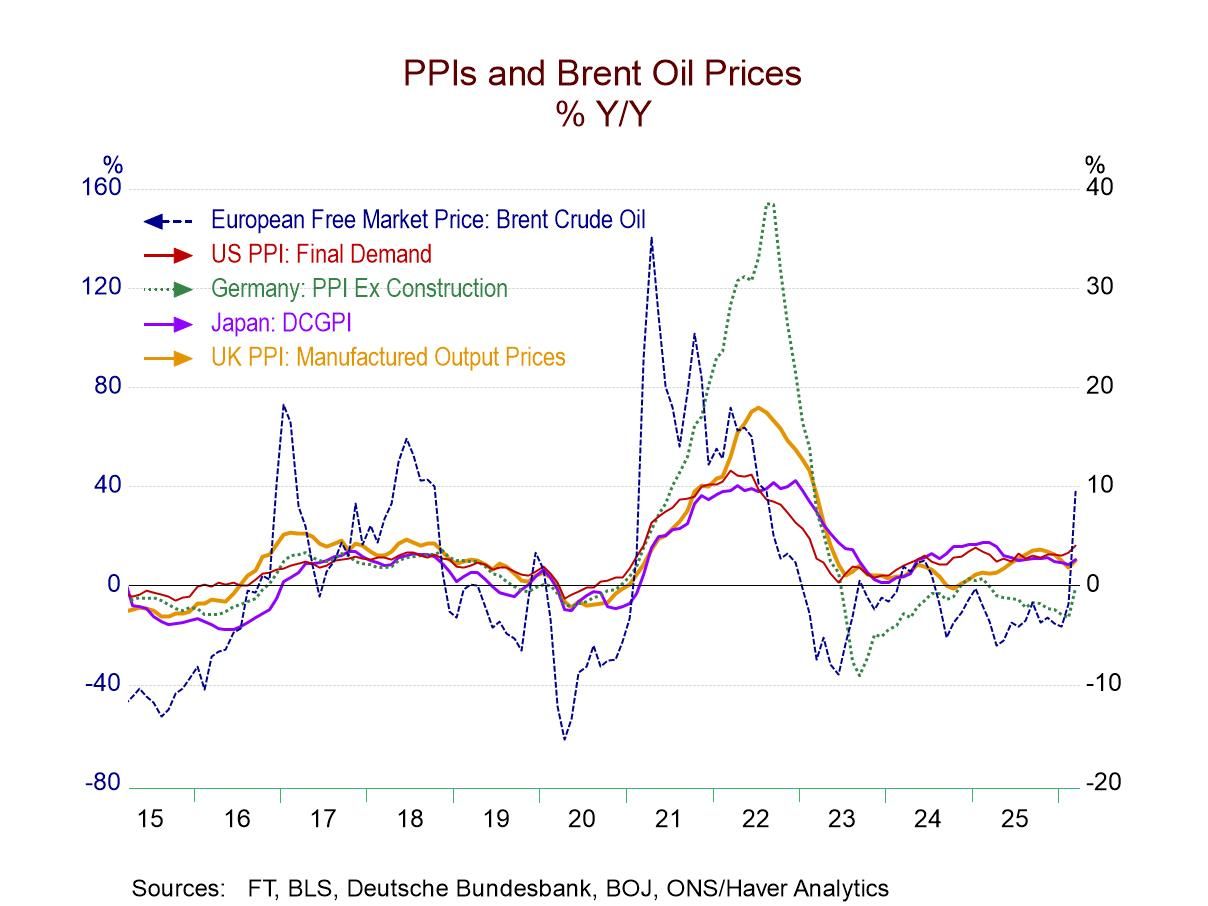

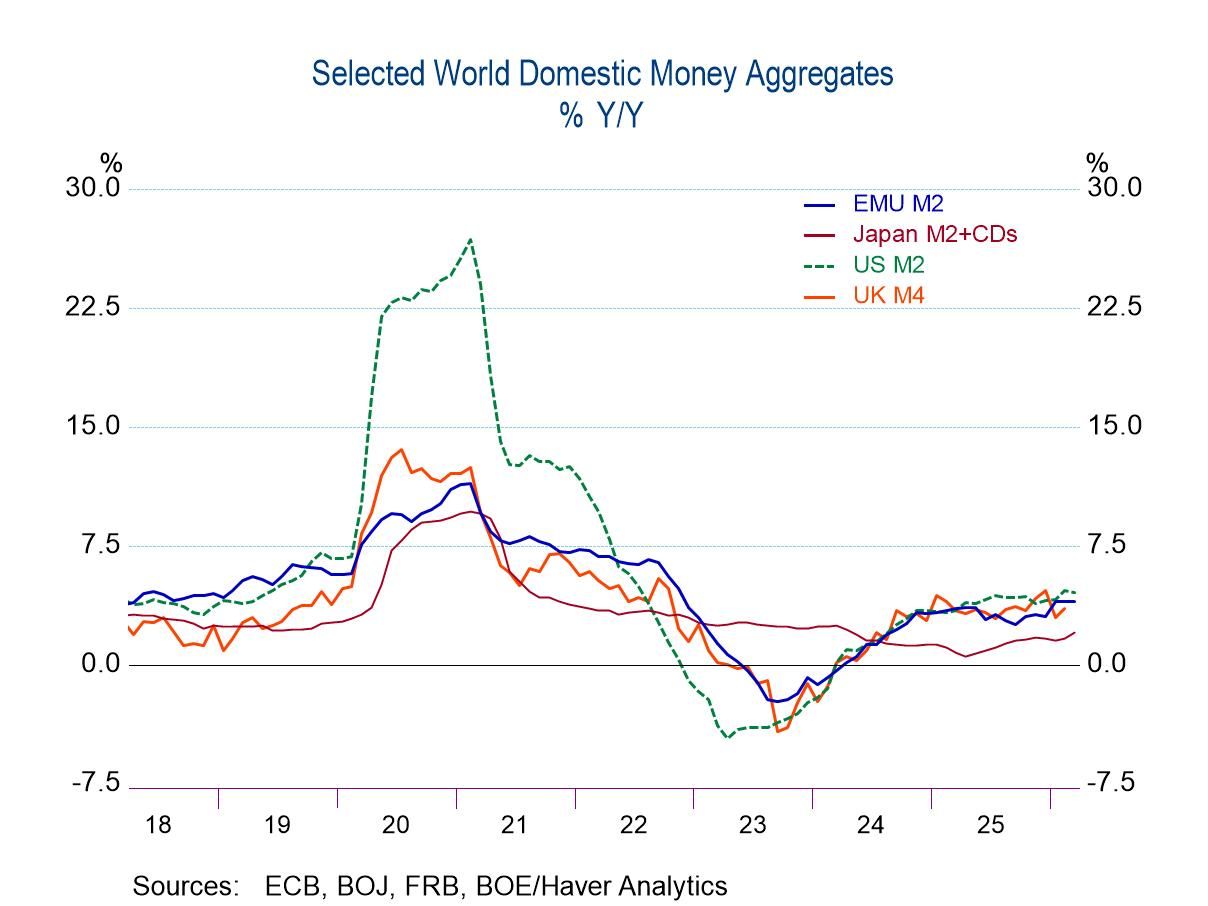

GlobalGlobally, money supplies are accelerating. Three- and six-month money growth rates equal or exceed the year-on-year pace everywhere, and the 12-month growth rates accelerate over the recent 12 months compared to the 12-month pace of one year ago—except for the United Kingdom, where data lag by one month. This deviation may amount to the lack of topicality since money, credit, and inflation all are caught in an updraft prompted by rising oil prices. The oil price (Brent) is up at a 468% annual rate over three months, and over 12 months the oil price is up by 31.7%, compared to a 5.5% rise over 12 months one-year ago.

Rising oil prices do NOT create inflation Now we all know that rising oil prices do not create inflation. So, thankfully, the 468% rise in oil prices is not driving up the inflation rate. But unfortunately, it is helping to drive up the price level. So, we are drawing a distinction between the price level and the inflation rate.

The year-over-year change in a price metric, like the CPI, is just that: the year-on-year gain. We often refer to this as ‘THE’ inflation rate. But that is only if the price level was at—and continued to rise at (about)—that same pace. Inflation is an ongoing rise in the price level. No one in their right mind thinks oil prices are going to rise by 468% year-over-year persistently. But of course, oil is a cost to producers and a price to consumers. It is a price that must be paid and cost that must be borne. The question is how much this bump-up in oil prices will contribute to the prices of the items we track in our various national price indexes in the future. Here I will refer to the CPI as the price index. And then we ask if that one-time rise in the relative price of oil will continue to bump up prices by the same amount month-after-month in the future. If it is, it is creating inflation. If not, it is creating a realignment of relative prices. The rise in relative prices is real. It may be painful to some and remunerative to others. The effects are complex.

But the spike in oil prices is not inflation. Even though we are tracking an unknown price rise that is continuing to waffle, I will speak of it as though we know the ultimate rise and speak of that as a one-time surge.

Expressed in this way, you should be able to see the oil price spurt as painful and as something that may be a temporary boost to inflation. If the price stays high, it will boost the price level based on the pass-through by commodity. After the oil price spurt, prices may be higher, but inflation will go back to ‘where it was.’

But all that happens if and only if monetary policy does not accommodate—does not monetize—the rise in oil prices. Unfortunately, we see money supplies are accelerating. Central banks have stepped up their rate of printing money as oil prices have risen, in order to stabilize interest rates. Printing more money, or increasing the money stock faster, is inflationary.