U.S. Philadelphia Fed Factory Index Turns Negative in October; Prices Weaken

by:Tom Moeller

|in:Economy in Brief

Summary

- Current General Activity Index reverses earlier improvement.

- Inflation reading increases.

- Future General Activity Index rebounds to five-month high.

The Current Activity Diffusion Index from the latest Manufacturing Business Outlook Survey (MBOS) conducted by the Federal Reserve Bank of Philadelphia, declined to -12.8 during October after rising to +23.2 in September. The survey covers the third Federal Reserve District. A reading of 7.5 for October had been expected in the Action Economics Forecast Survey. A lessened 12.4% of firms reported increases in general activity in October, down from 32.9% in September, while 25.2% reported declines after 16.7% did in September. Responses to this month's survey were collected from October 6 to October 13.

Haver Analytics calculates an ISM-adjusted current activity diffusion index from five key components using the methodology along the lines of the national ISM index. This reading fell to 53.5 in October from 55.0 in September. It remained up from an April low of 43.6.

In the latest survey, the shipments index fell to 6.0 from 26.1 in September. A greatly lessened 24.1% of respondents reported higher shipments while a steady 18.1% reported lower. The inventories measure dropped to 5.4 from 15.0. Working higher, the new orders index strengthened to 18.2 in October after rising sharply to 12.4 in September. A lessened 34.5% of respondents reported higher new orders while a diminished 16.2% reported declines. The unfilled orders measure rose to -2.2 this month after declining to -6.6 in September. The delivery times reading improved to 6.6 this month after falling to -3.4 in September, but remained below the high of 13.6 in June.

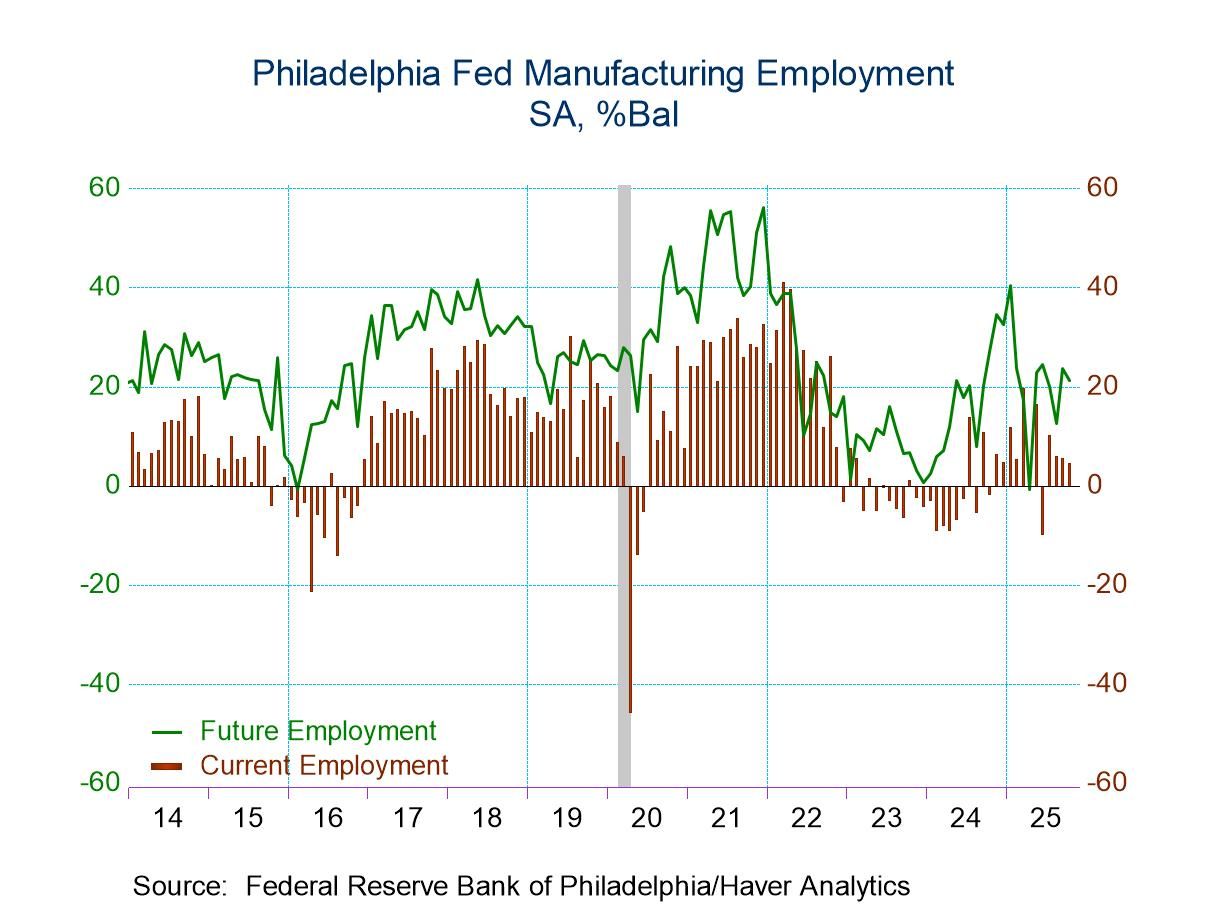

Working lower, the employment index eased to 4.6 in October after falling to 5.6 in September. It was down from a high of 16.5 in May. A lessened 11.6% of respondents reported increases in employment in October while a lower 7.0% reported declines. The average workweek index fell to 12.8 in October after surging to 14.9 last month. A greatly lessened 13.8% of respondents reported longer hours while a notably fewer 1.0% reported a decline.

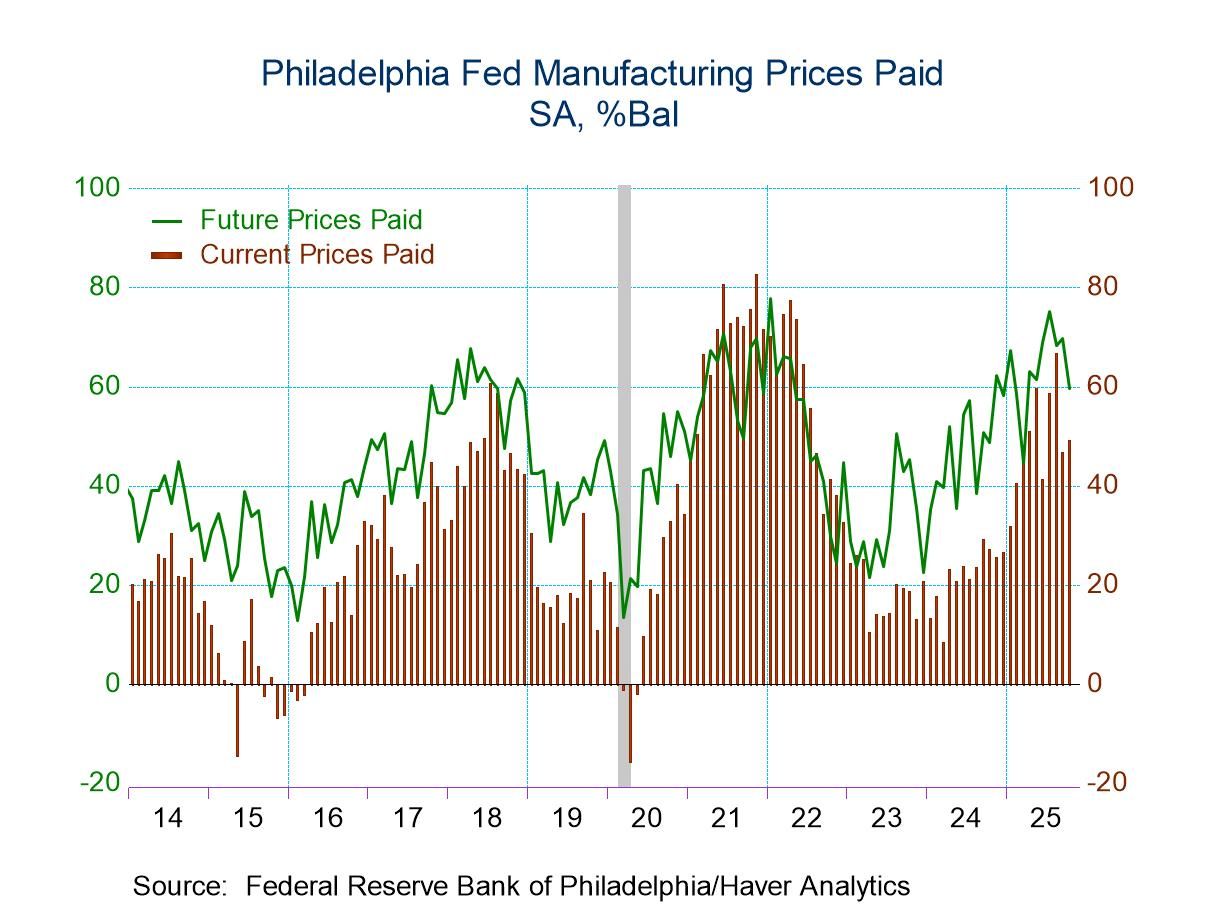

Inflation measures increased in October. The prices paid index rose to 49.2 in October after falling to 46.8 in September. A fairly steady 49.2% of respondents reported increases in prices in October while a lessened none of respondents reported decline. The prices received index strengthened to 26.8 after declining to 18.8 in September. A higher 27.5% of respondents reported increases in prices received while a steady 0.7% reported declines.

The Future Activity Index over the next six months increased to 36.2 in October after rising to 31.5 in September. It was a five-month high. A lessened 47.4% of respondents expected an increase in activity while a roughly halved 11.2% expected a decline. Component declines were mixed. New orders rose as well as the shipment series increased sharply . Delivery times, the inventory index and expected unfilled orders improved but the future employment index fell as well as future hours worked. Future capital expenditures strengthened. The future prices paid index as well as the future prices received measure declined.

The Manufacturing Business Outlook Survey (MBOS), conducted by the Federal Reserve Bank of Philadelphia, is a monthly survey of manufacturers in the Third Federal Reserve District. Participants indicate the direction of change in overall business activity and in the various measures of activity at their plants. The diffusion indexes in the MBOS represent the percentage of respondents indicating an increase minus the percentage indicating a decrease. The series from the survey dating back to May 1968 can be found in Haver's SURVEYS database. The expectations forecast figures are from the Action Economics Forecast Survey in AS1REPNA.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief

Global

Global