U.S. Small Business Optimism Fell in September

by:Sandy Batten

|in:Economy in Brief

Summary

- First decline in three months.

- Uncertainty rose to the fourth highest levels in series history,

- Percentage expecting economy to improve fell for the third time in the past four months.

- Percentage reporting supply chain disruptions jumped 10 points in September.

- This survey was conducted in September. Whatever impact the federal government shutdown will have will appear in the October survey.

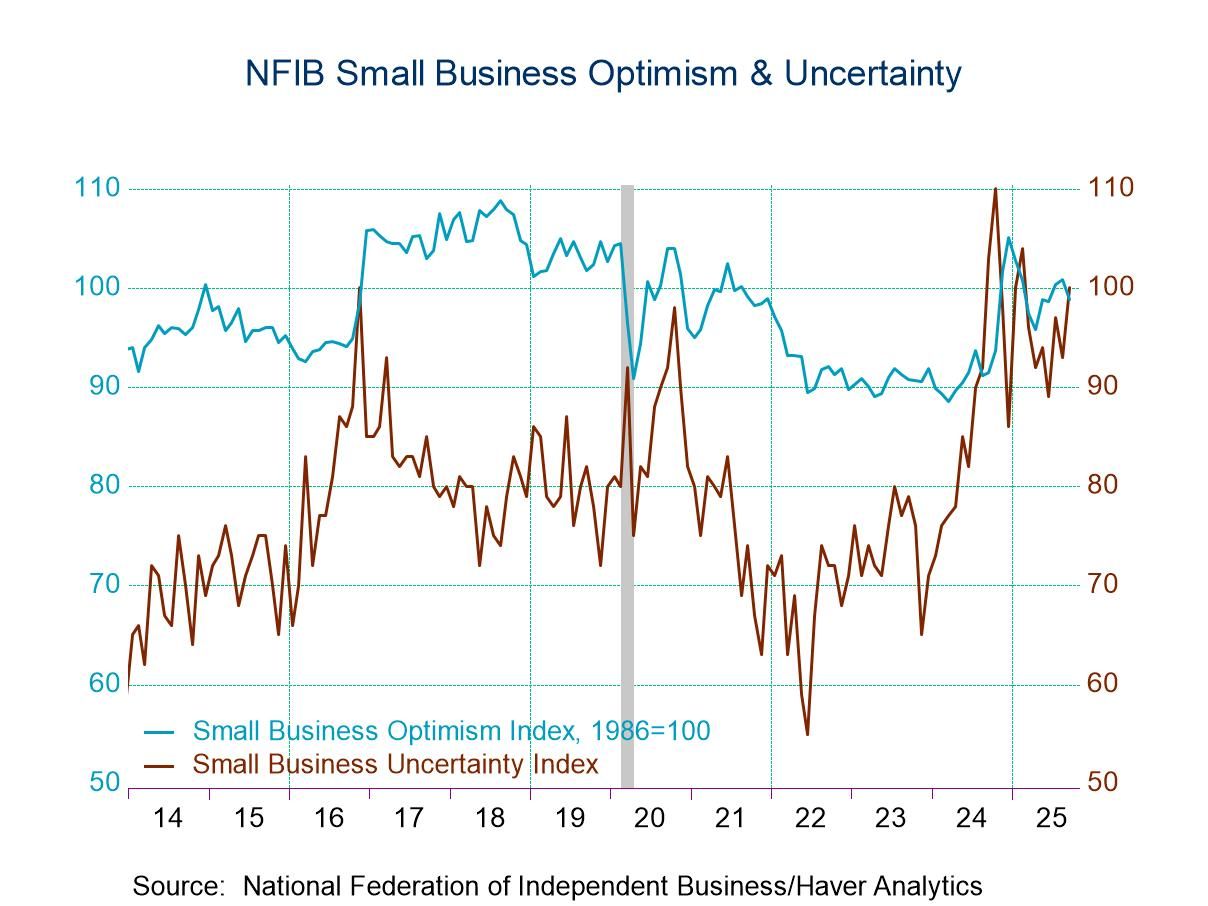

The NFIB Small Business Optimism Index fell 2 points (-2.0% m/m, +8.0% y/y) to 98.8 in September from 100.8 in August, according to the Small Business Economic Trends survey conducted by the National Federation of Independent Business. This was the first monthly decline in three months. Market expectations were for a smaller decline to 100.5. Still, the index remained above the survey’s 52-year average. Five of the indexes 10 components fell in September while two increased and three were unchanged. A decline in those expecting better business conditions in the next six months and an increase in reports of excess inventory contributed most to the drop in the Optimism Index in September. The Uncertainty Index rose 7 points from August to 100 in September, the fourth-highest reading in over 51 years.

The quality of labor and taxes were tied as the single most important problem that small firms face in this survey. However, inflation rebounded 3 points to 14%, and 64% of small business owners reported that supply chain disruptions were affecting their business to some degree, up 10 points from August.

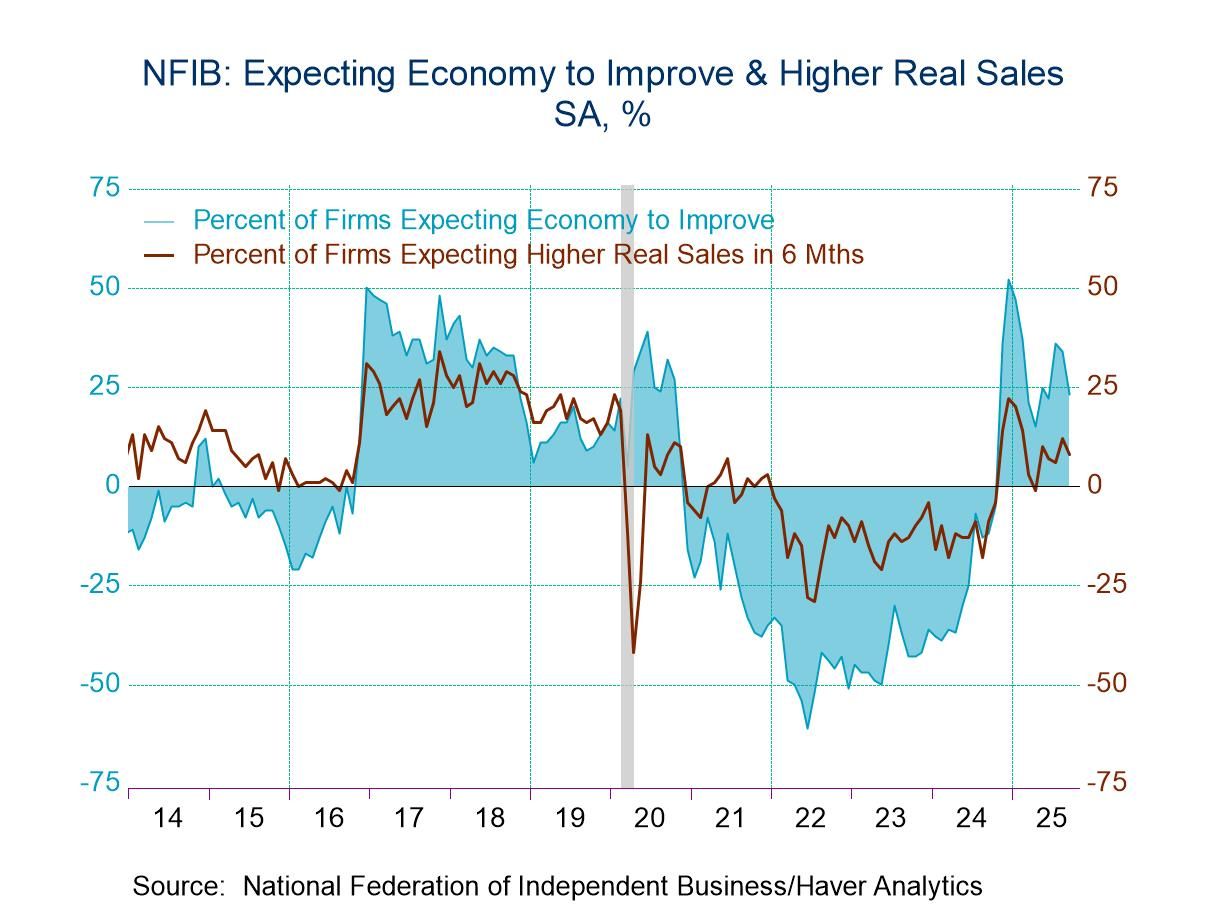

The sample continues to think that, on balance, the economy will improve over the next six months. However, that view was held by a smaller share of respondents with the net balance falling 11 points to 23% in September from 34% in August and 36% in July. Firms were also less optimistic about their sales outlook with the net balance expecting higher sales in six months falling to 8% in September from 12% in August. A net negative 7% of respondents viewed current inventory stocks as “too low” in September, down 7 points from August. This was the largest monthly decline in the survey’s history.

A net 11% of respondents thought that now was a good time to expand their business, down from 14% in August and the lowest reading since May. Plans to increase capital expenditures were unchanged at a net 21%, still low by historical standards.

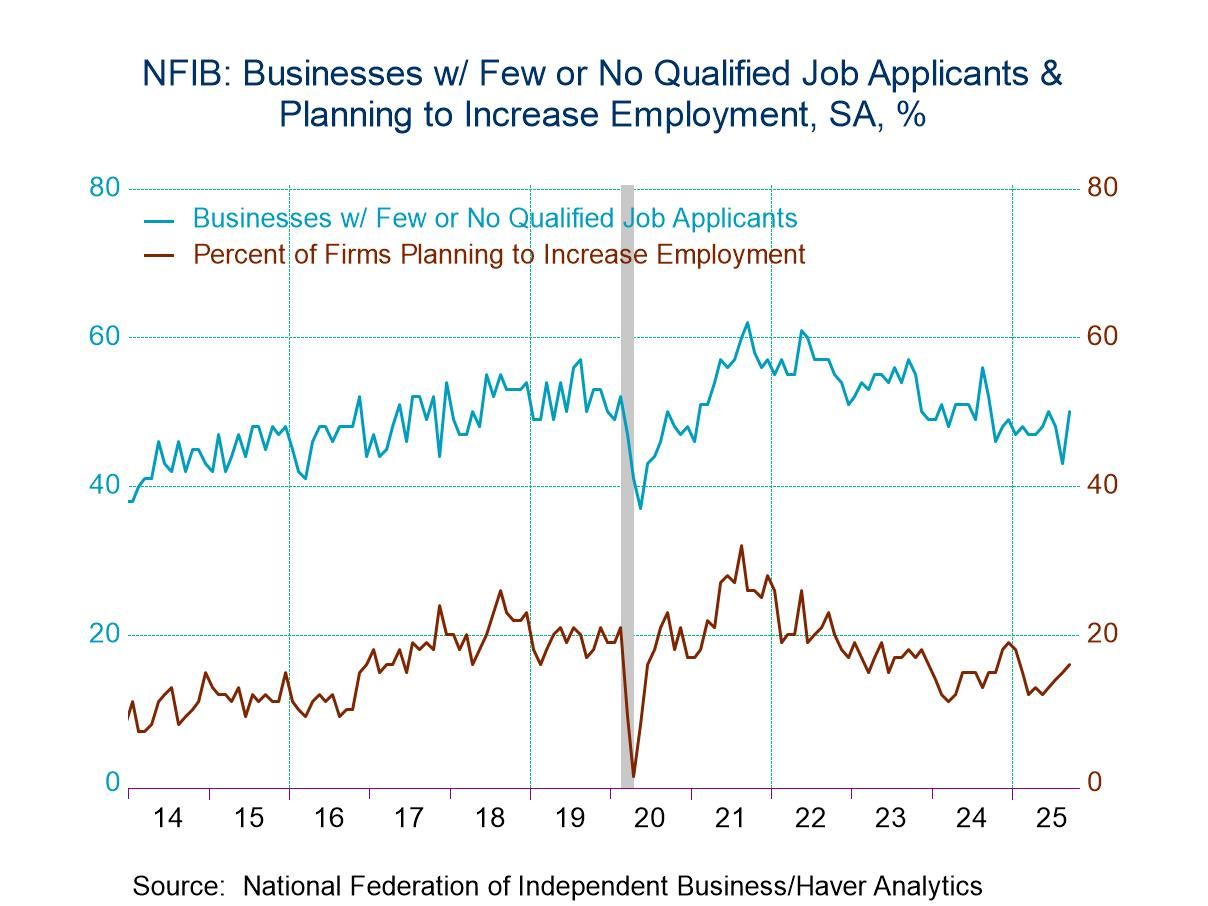

Labor market indicators were a little mixed. The percentage of respondents reporting few or no qualified applicants for openings jumped to 50% in September from 43% in August. This tied the June reading as the highest since last September. Moreover, wages gains increased. The net balance of respondents who have increased wages over the past three months rose for the second consecutive months to 31%. By contrast, the net balance of respondents with positions that they were not able to fill was unchanged at 32%, its lowest reading since December 2020. And the net balance of respondents expecting to increase wages over the coming three months slipped to 19 from 20 in August.

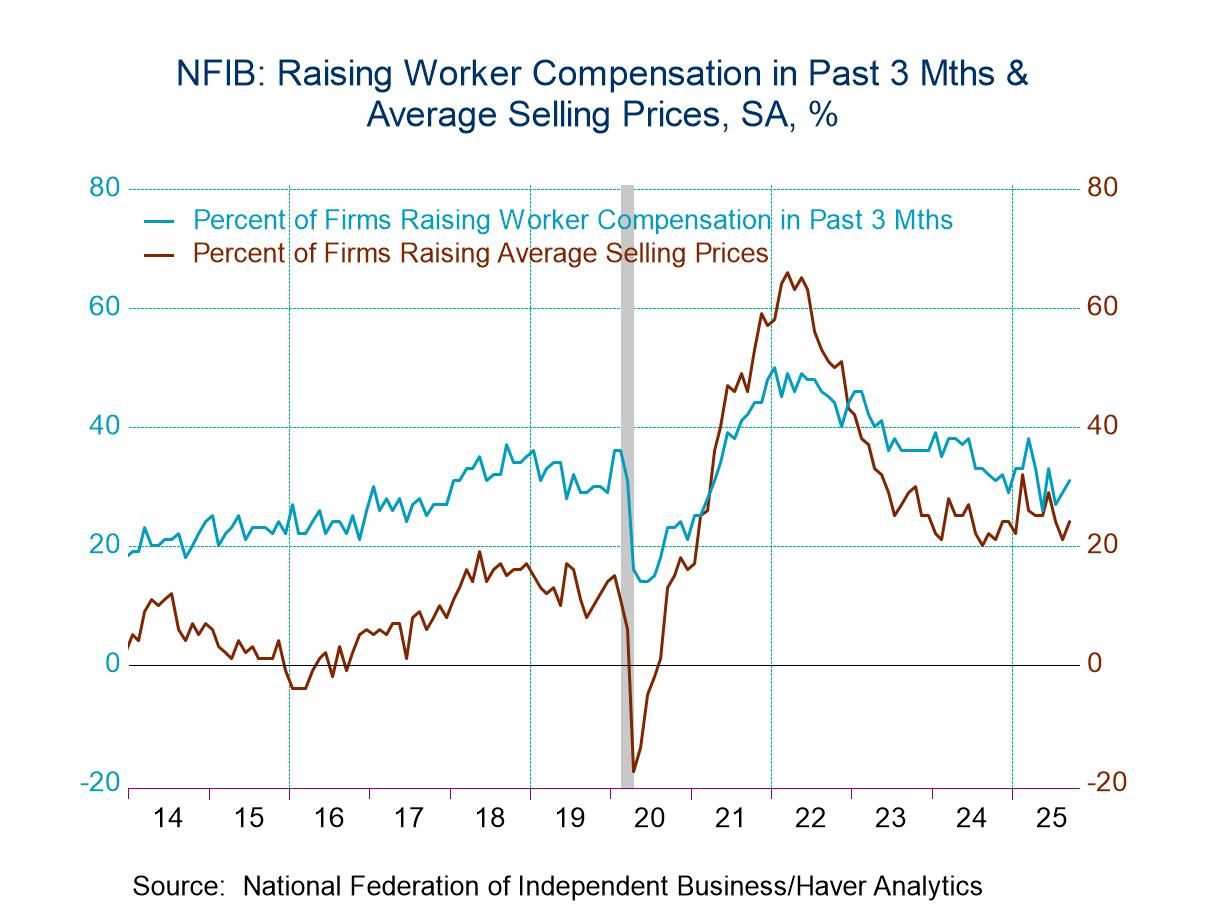

Inflation concerns re-intensified in September. The net balance of respondents who have raised selling prices increased to 24% in September from 21% in August, while the net balance planning to raise prices jumped to 31% from 26%. Also, the percentage considering inflation to be the single most important problem increased to 14% from 11%.

According to the Small Business Administration, there are 33 million small businesses in the United States, which employ 62 million workers. The NFIB surveys anywhere from 500 to 2000 respondents each month and the typical firm employs 10 people and reports gross sales of about $500,000 a year. The NFIB figures can be found in Haver’s SURVEYS database.

Understanding the Fed’s Balance Sheet is the title of today’s speech by Fed Chair Jerome H. Powell and it can be found here.

Sandy Batten

AuthorMore in Author Profile »Sandy Batten has more than 30 years of experience analyzing industrial economies and financial markets and a wide range of experience across the financial services sector, government, and academia. Before joining Haver Analytics, Sandy was a Vice President and Senior Economist at Citibank; Senior Credit Market Analyst at CDC Investment Management, Managing Director at Bear Stearns, and Executive Director at JPMorgan. In 2008, Sandy was named the most accurate US forecaster by the National Association for Business Economics. He is a member of the New York Forecasters Club, NABE, and the American Economic Association. Prior to his time in the financial services sector, Sandy was a Research Officer at the Federal Reserve Bank of St. Louis, Senior Staff Economist on the President’s Council of Economic Advisors, Deputy Assistant Secretary for Economic Policy at the US Treasury, and Economist at the International Monetary Fund. Sandy has taught economics at St. Louis University, Denison University, and Muskingun College. He has published numerous peer-reviewed articles in a wide range of academic publications. He has a B.A. in economics from the University of Richmond and a M.A. and Ph.D. in economics from The Ohio State University.

More Economy in Brief

Global

Global