Asia

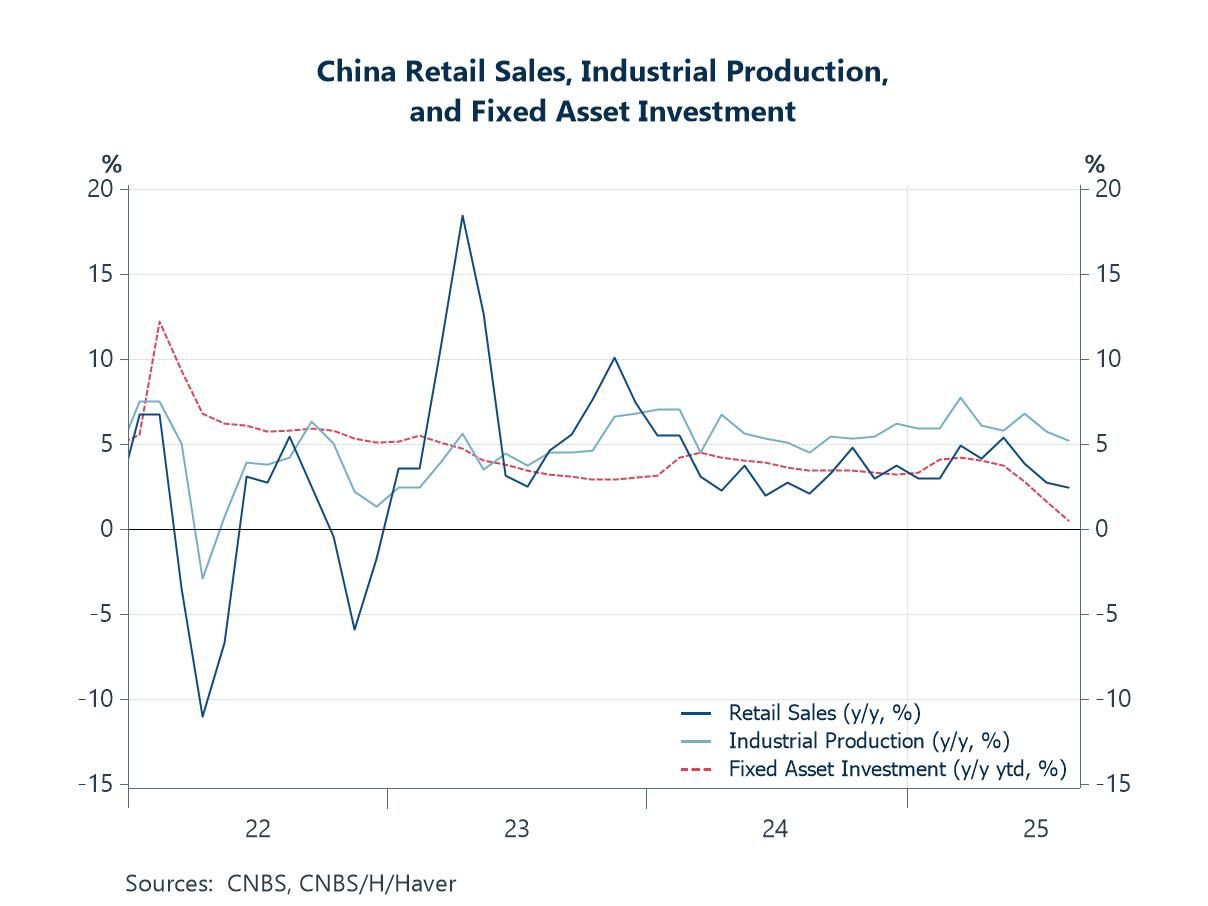

AsiaThis week, we examine a broad set of key developments, from China’s disappointing August data and structural economic challenges to a flurry of central bank decisions across Japan, Taiwan, and Indonesia. China’s latest data disappointed again, reinforcing concerns that US trade tariffs are starting to bite as the front-loading boost fades (chart 1). More broadly, China continues to struggle with its transition toward a more consumption-driven economy (chart 2). Recent figures show little sign of this pivot, with trade remaining resilient while consumption still lags.

In Japan, the Bank of Japan (BoJ) will decide on interest rates during a central bank-heavy week, following key decisions from the Fed and the Bank of England (chart 3). The BoJ is widely expected to hold its policy rate steady for now as the country navigates a period of political uncertainty after Prime Minister Ishiba’s recent resignation. Still, there has been some good news: the Cabinet Office estimates that Japan’s output gap turned positive for the first time in two years, although figures differ across methods and sources (chart 4).

Turning to Taiwan, uncertainty remains in the semiconductor sector as US tariffs loom. However, major Taiwanese producers’ substantial US investments may position them for exemptions (chart 5). Finally, in Indonesia, Bank Indonesia’s policy decision is also due this week on Wednesday. While the door to monetary easing remains open, the timing of any move is unclear. Meanwhile, Indonesian asset prices fell again after the removal of one of its long-serving Finance Ministers (chart 6), with her successor’s plans raising renewed concerns about fiscal discipline.

China China’s latest monthly data releases disappointed again, showing a further slowdown in growth. This has strengthened investor concerns that US trade tariffs are finally starting to weigh on the economy as earlier front-loading effects fade. Year-on-year growth in retail sales and industrial production fell to their lowest levels in about a year, while fixed asset investment was nearly flat (chart 1). Property prices also extended their multi-year decline. In response to the weakening outlook, calls for additional policy support have grown, though several measures have already been announced. For instance, domestic consumption may get another boost as the government’s new personal consumer loan interest rate subsidy program takes effect this month. If realized, this would follow the one-off lift from the earlier durable goods subsidy program.