Asia| Sep 16 2025

Asia| Sep 16 2025Economic Letter from Asia: Decisions, Decisions

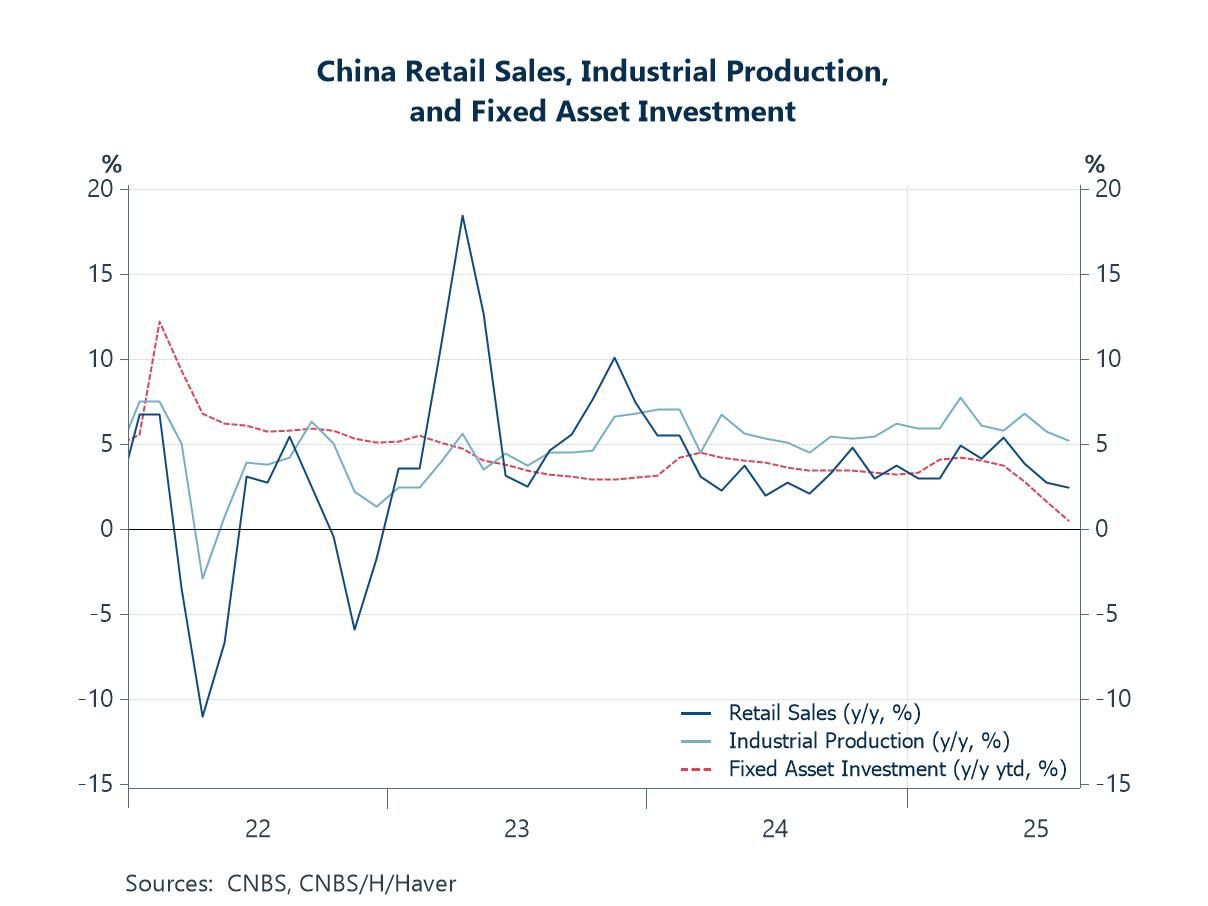

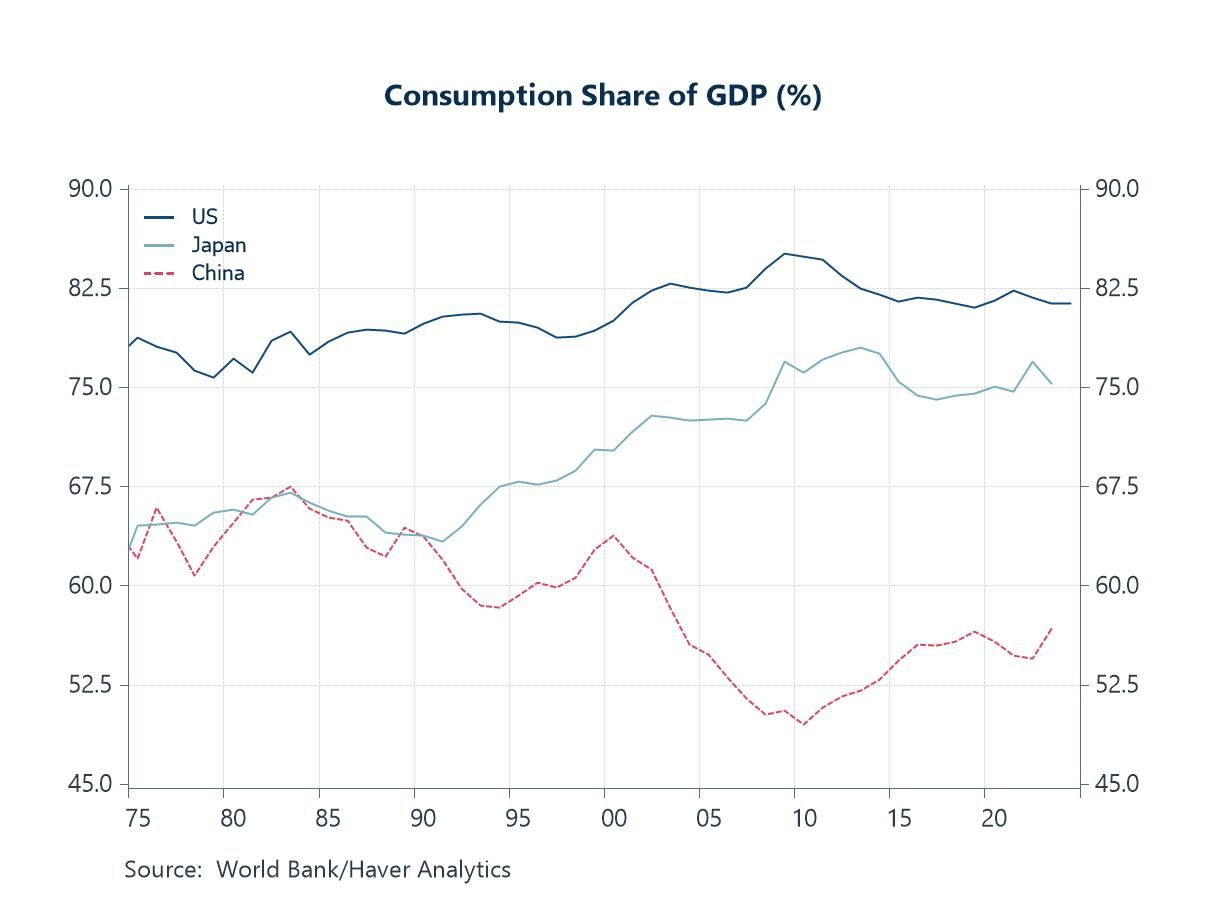

This week, we examine a broad set of key developments, from China’s disappointing August data and structural economic challenges to a flurry of central bank decisions across Japan, Taiwan, and Indonesia. China’s latest data disappointed again, reinforcing concerns that US trade tariffs are starting to bite as the front-loading boost fades (chart 1). More broadly, China continues to struggle with its transition toward a more consumption-driven economy (chart 2). Recent figures show little sign of this pivot, with trade remaining resilient while consumption still lags.

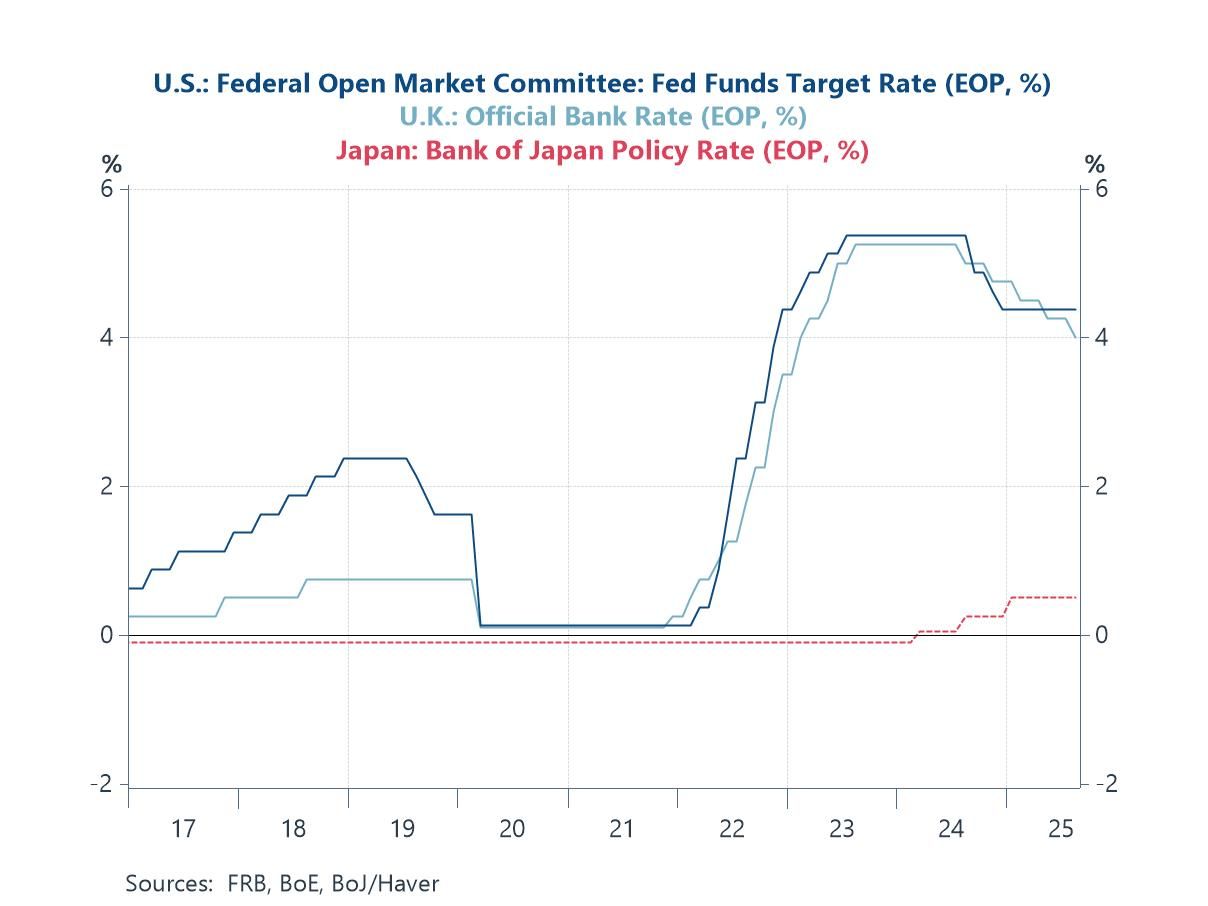

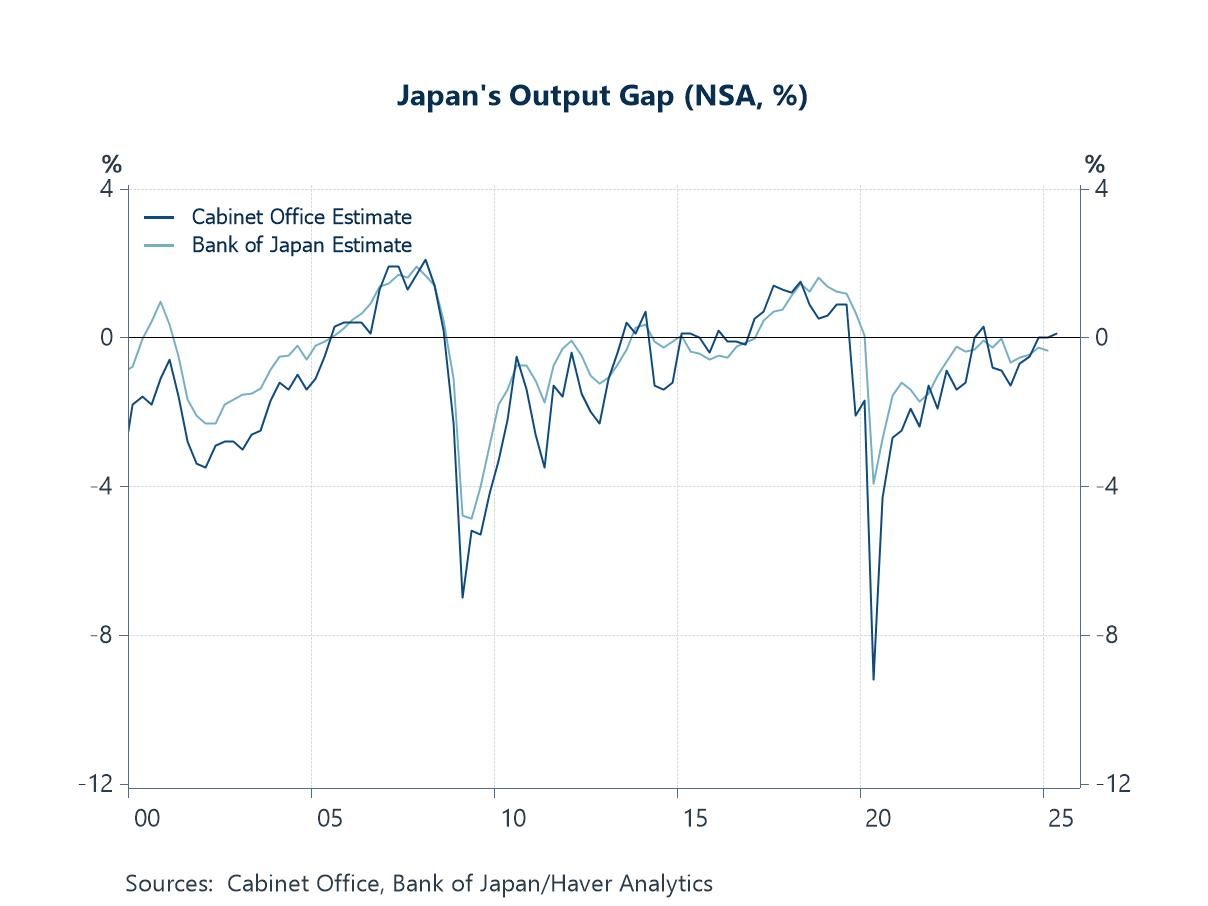

In Japan, the Bank of Japan (BoJ) will decide on interest rates during a central bank-heavy week, following key decisions from the Fed and the Bank of England (chart 3). The BoJ is widely expected to hold its policy rate steady for now as the country navigates a period of political uncertainty after Prime Minister Ishiba’s recent resignation. Still, there has been some good news: the Cabinet Office estimates that Japan’s output gap turned positive for the first time in two years, although figures differ across methods and sources (chart 4).

Turning to Taiwan, uncertainty remains in the semiconductor sector as US tariffs loom. However, major Taiwanese producers’ substantial US investments may position them for exemptions (chart 5). Finally, in Indonesia, Bank Indonesia’s policy decision is also due this week on Wednesday. While the door to monetary easing remains open, the timing of any move is unclear. Meanwhile, Indonesian asset prices fell again after the removal of one of its long-serving Finance Ministers (chart 6), with her successor’s plans raising renewed concerns about fiscal discipline.

China China’s latest monthly data releases disappointed again, showing a further slowdown in growth. This has strengthened investor concerns that US trade tariffs are finally starting to weigh on the economy as earlier front-loading effects fade. Year-on-year growth in retail sales and industrial production fell to their lowest levels in about a year, while fixed asset investment was nearly flat (chart 1). Property prices also extended their multi-year decline. In response to the weakening outlook, calls for additional policy support have grown, though several measures have already been announced. For instance, domestic consumption may get another boost as the government’s new personal consumer loan interest rate subsidy program takes effect this month. If realized, this would follow the one-off lift from the earlier durable goods subsidy program.

Chart 1: China retail sales, industrial production, and fixed asset investment

Touching on broader structural issues, beyond the near-term challenges of US trade policies, it remains uncertain whether China can make substantive progress in its transition toward a consumption-led economy. The shift away from one driven by exports — increasingly constrained by Western trade barriers — and investment, which has become less efficient, is proving difficult. As of 2023, consumption accounted for about 57% of China’s GDP (chart 2), far below the levels seen in developed economies such as the US, where consumption has consistently exceeded 80% for decades. A transition is possible, though not without challenges. Japan managed a similar shift during the 1990s and 2000s, though largely by way of declining investment rather than rising consumption, as part of its “lost decades.” For China, the question is whether it can navigate this adjustment without inflicting significant economic pain. Recent resilient export data suggest that, for now, the economy is still leaning heavily on its traditional growth drivers rather than moving decisively toward consumption.

Chart 2: US, Japan, and China consumption share of GDP

Japan Looking ahead, markets face a busy week with a flurry of interest rate decisions from major economies. The most closely watched will be the Fed on Wednesday, followed by the Bank of England on Thursday and the Bank of Japan on Friday. The Fed’s outcome will likely set the tone and influence subsequent central bank moves. In Japan, the recent upgrade to Q2 GDP could justify further policy tightening. However, renewed political uncertainty following Prime Minister Ishiba’s resignation, along with lingering risks from looming US semiconductor tariffs, are likely to keep the Bank of Japan on hold for now, with markets instead eyeing a potential hike later in the year. That said, Japan’s political situation remains fluid. Depending on the outcome of the upcoming elections and the composition of the next government, market expectations around prospective BoJ policy are likely to shift accordingly.

Chart 3: US, UK, and Japan policy rates

There has, however, been a small sliver of optimism in Japan recently, although upcoming risks, such as those mentioned earlier, could threaten these positive developments. One encouraging sign is that, according to Cabinet Office estimates, Japan’s output gap finally turned positive in calendar Q2 2025 for the first time in two years, as shown in chart 4. A positive output gap is significant for Japan, which has experienced a negative gap for most of the past few decades. It indicates that the economy may finally be operating above its potential rather than underperforming. That said, the output gap is estimate-based, and discrepancies can arise between different methods and sources, as illustrated by the differences between the Cabinet Office’s and the Bank of Japan’s estimates in the chart.

Chart 4: Japan’s output gap

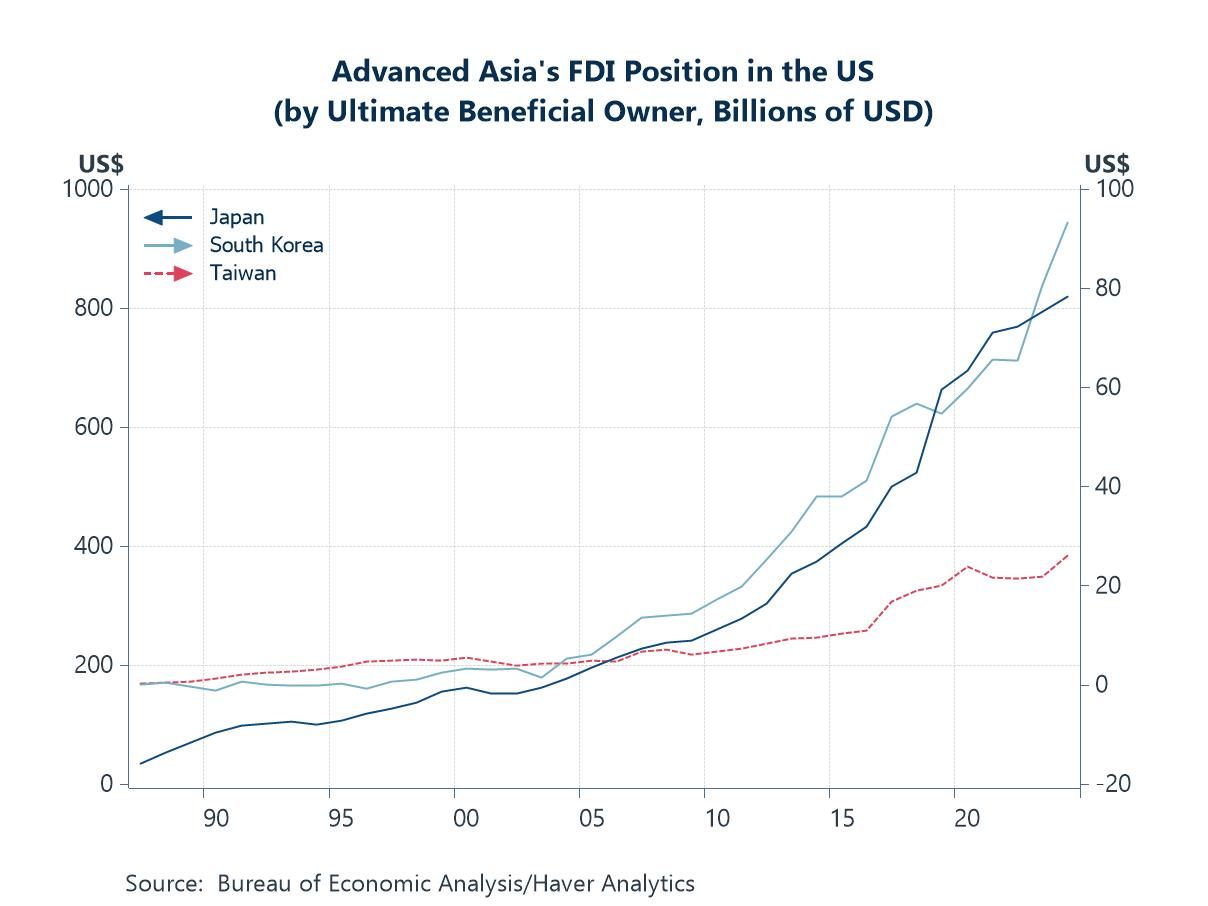

Taiwan and semiconductors Turning to Taiwan, developments from the Trump administration remain in focus, with sectoral tariffs on semiconductors still looming — though exemptions may be granted to firms shifting production to the US or committing to new domestic investments. In this context, major Taiwanese semiconductor producer TSMC may be well-positioned to receive exemptions, given its substantial US investments, including its multi-phase Arizona projects totalling $165 billion. Taiwan, along with other advanced Asian economies such as Japan and South Korea, has already ramped up direct investments in the US (chart 5). Recent trade agreements are expected to further boost these inflows, whether for onshore production or other purposes. This week, Taiwan’s central bank is also set to announce its interest rate decision, with rates widely expected to remain unchanged for a sixth consecutive quarter.

Chart 5: Advanced Asia’s FDI position in the US

Indonesia Indonesia also has a central bank decision due this week, adding to the central bank-heavy calendar. While the door remains open for further monetary easing, the timing of the next move is still unclear. What is clear, however, is the persistence of political uncertainty, even if protests have somewhat subsided. This fresh bout of uncertainty — which has pressured Indonesian asset prices and weakened the rupiah despite central bank intervention (chart 6) — stems from the recent cabinet reshuffle that removed Sri Mulyani Indrawati, one of Indonesia’s longest-serving and most influential finance ministers. Indrawati was replaced by Purbaya, who has since pledged to inject about 200 trillion rupiah ($12 billion) into the economy to improve banking system liquidity, reigniting concerns over Indonesia’s fiscal discipline. That said, more recent readings suggest that a market recovery—particularly in equities—is already underway.

Chart 6: Indonesian equities and the rupiah

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief