EMU Trade Surplus Expands But Stays on Lower Trend Pace

In the wake of U.S. tariff implementation, we, of course, look for evidence of the impact of that action on global trade performance. In the July trade report for the EMU, there is little direct evidence of a draconian impact on trade in the EMU that coincides with changes in U.S. trade policy. Of course, the EMU picture is of the external trade of that community with the world and not just the United States. But such dire predictions had been made of the impact of U.S. tariff policy that it is very worthwhile to note that such cataclysm has not appeared. Has there been some trade impact? Certainly! Has there been some increases in uncertainty? Yes. But nothing has brought global trade to a screeching halt. In fact, the Baltic Dry goods index shows a rise in trade volumes since early 2025. The current level is comparable to or higher than 2024 and last persistently stronger in 2022.

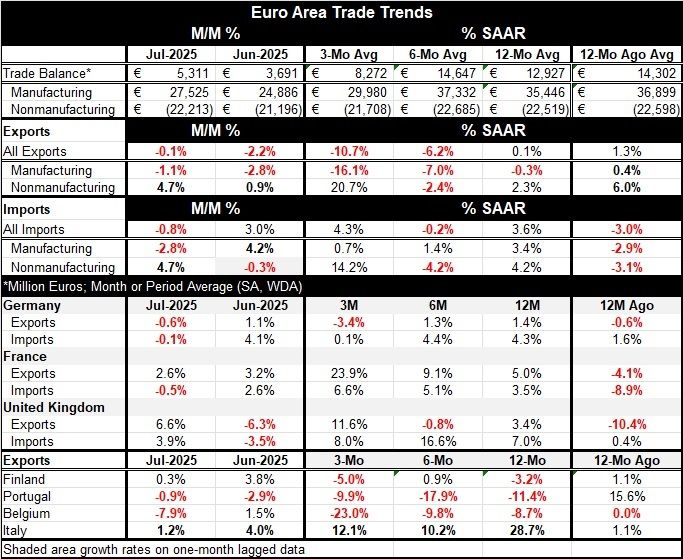

The euro area trade surplus at 5.3bln euros is higher in July than in June but is much weaker than its 3-month, 6-month, and 12-month averages. In round numbers, the 3-month average is €8bln, the 6-month average is €15bln and the 12-month average is €13bln. So, July runs at less than half the pace of the 12-month average. That may be evidence of U.S. tariff impact.

The overall balance sees disproportionately large-looking effect because it is smaller…smaller than what? Well, the manufacturing surplus is at 27bln euros in July, up by 3bln euros from June, about 3bln euros below the 3-month average of 30bln euros and about 8bln euros below the 12-month average. An eight billion drop on a level of 35bln seems smaller than and eight billion euro drop on 13 bln…but eight billion euros are eight billion euros- but that is only 2.2% of total exports. How we view relativity is important. Is that the draconian U.S. tariff impact?

The nonmanufacturing deficit in the EMU is almost unchanged by month or on any average (at minus 22bln euros).

Growth rates for manufacturing exports show contraction and a worsening trend from 12-months to 6-months to 3-months. This is not so for nonmanufacturing exports that log a strong double-digit rise over three months. EMU manufacturing imports show very steady slow growth with modest decay… not so for nonmanufacturing imports that log strong double-digit gains over three months.

Country level trends By country, German exports show growth rate erosion, French exports show acceleration, Italy shows a slowdown but at a still-strong double-digit pace for three months. Finland, Portugal, and Belgium show exports in a state of decline or weakness- mostly decline. The United Kingdom, not an EU member, shows an erratic trend but with 3-month export growth in double digits. There is some export weakness here to be sure but nothing that looks very severe.

On the import side, German imports melt down to a 3-month low annualized pace of +0.1%. French imports speed up to a 6.6% pace over 3 months. The U.K. looks at positive- if irregular- import growth.

The global scene The global economy and the firms that operate in that broader sphere are buffeted by many trends. Macroeconomic growth shifts, central banks change posture based on policy objectives, there is war in Ukraine due to Russia’s actions and a severe contentious hot spot in the Middle East. Mix in some pollical instability in France… And of course, there have been a number of significant policy shifts in the U.S. as the Trump administration tries to carve out a new international order that it feels will be fairer to the U.S. Agree or not, that is the picture. So far, there has been a lot more complaining and many more dire predictions than there have been dire outcomes.

Global inflation remains as it has been over target but barely changing speed. Growth is still in gear. Global stock markets are performing well. Commodity prices are not inflamed but gold has stepped up. It would be hard to tell a story about all the concerns that have been expressed referencing or supporting these concerns with economic or market data. The most severe shift we can put our finger on is in the U.S. labor market where surprising weak job growth has appeared but was subsequently made less surprising by the admission that job growth had been overstated over the previous year by a significant amount. So where’s the new risk?

U.S. job growth has slowed because of closing its border, and that slowing seems much more severe than the impact on U.S. economic growth. But the Fed has the labor market as part of its dual mandate and so the jobs slowdown is putting Fed policy on edge for a change and will probably result in a Fed rate cut this week with more to come. That would have international repercussions. And U.S. inflation is not low and has been over target for over four years. What such a shift means for global inflation stability is worth asking. But that question is now a live one in the U.S. where the President is pushing for more cuts and has been willing to get aggressive in his treatment of Fed officials to get what he wants.

This is a factor in the global economy. What happens with U.S. monetary policy matters. The treatment of the U.S. central bank and its role as an independence policy maker also matters a great deal to the global economy – in part because the Fed is a trend-setter. So far, the impact of all these shifts in U.S. policy has been modest. Will it remain so? Or is there a build-up of forces that markets have yet to reckon with? Many remain concerned that we have not yet seen the full impact of the Trump administration’s policies on the economy and on markets- let alone the global knock-on impacts. It is definitely something to keep an eye on.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global