Global| Nov 06 2025

Global| Nov 06 2025Charts of the Week: Uneven But Unbroken

by:Andrew Cates

|in:Economy in Brief

Summary

Recent financial market developments have been shaped by a renewed bout of volatility, with heightened concerns about stretched AI valuations triggering a big correction across parts of the tech sector. This comes against a backdrop of lingering uncertainty in Washington, where the US government shutdown has continued to delay the release of several key economic reports, clouding visibility on near-term momentum. Still, the broader macro signals offer a mixed but nuanced picture. Global manufacturing PMIs have continued to hold up, hinting that underlying industrial momentum remains resilient (chart 1). The latest US Senior Loan Officer Survey points to a stabilisation in credit conditions—banks remain cautious, but the most intense phase of tightening may have now passed (chart 2). In China, the October PMIs reflected renewed softness in manufacturing alongside a still-steady services sector, tentatively suggesting that growth may be rebalancing, albeit at a weaker aggregate pace of growth (chart 3). Australia’s inflation and labour market data, meanwhile, have complicated the case for near-term policy easing, with the RBA opting to stay on hold this week as core inflation remain sticky. In Argentina, currency weakness persists even as equity markets rally, highlighting the policy and market tension surrounding President Milei’s reform agenda (chart 5). And finally, at a more structural level, latest global emissions data serve as a reminder that energy, manufacturing, transport, and households remain the principal sources of CO₂—illustrating how the climate and energy transition will continue to shape the macro landscape well beyond the current economic cycle (chart 6).

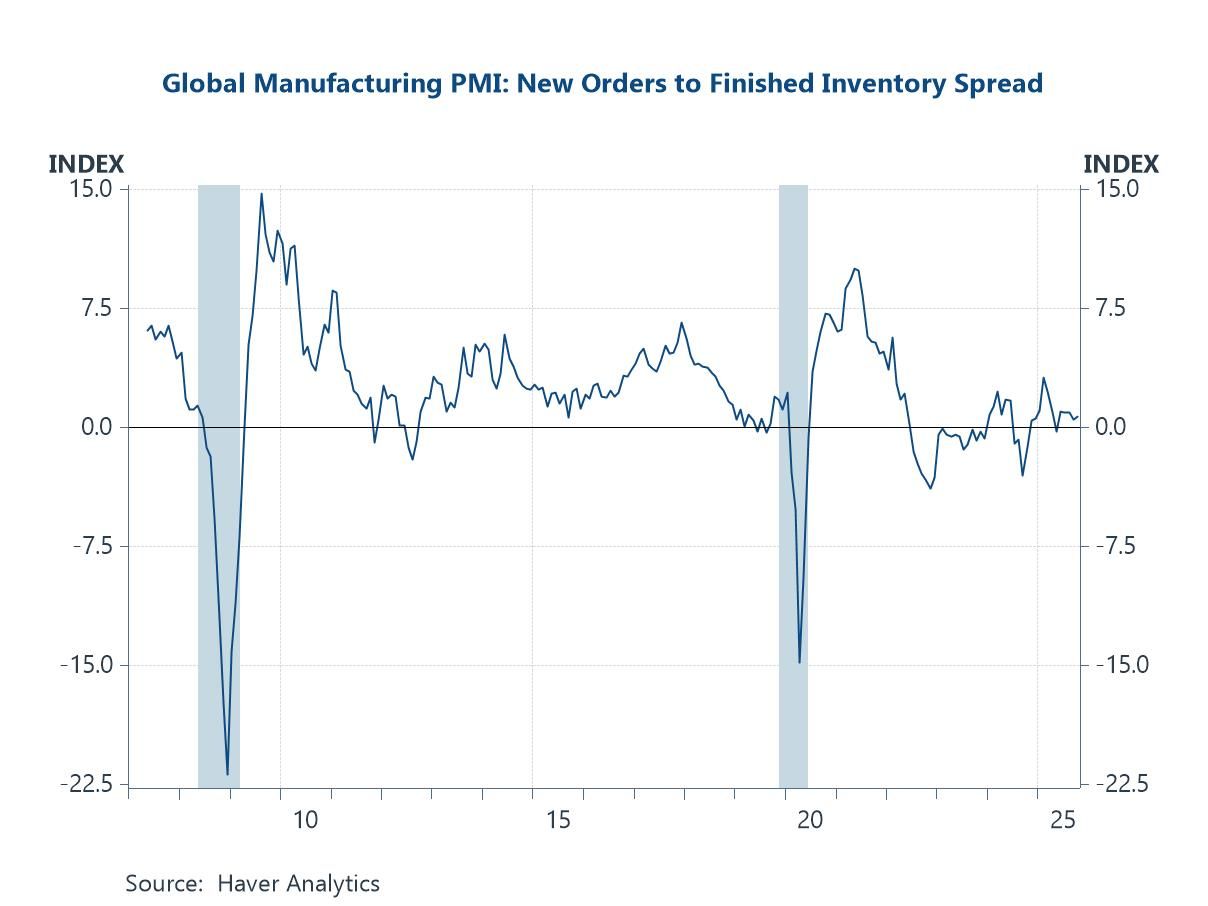

The global growth cycle The new orders-to-inventory spread in the global manufacturing PMI is often been viewed as one of the most reliable forward-looking indicators of the global economic cycle. When new orders are rising relative to inventories, it typically signals that demand is firming, production pipelines are beginning to refill, and industrial momentum is building. Conversely, when inventories accumulate faster than orders, it often foreshadows a slowdown. As the chart shows, this spread has been holding up relatively well in recent months, suggesting that despite ongoing headwinds—US tariff policies, uneven global demand, and geopolitical uncertainty—the underlying pulse of global manufacturing remains resilient.

Chart 1: Global Manufacturing PMI: New Order to Inventory Spread

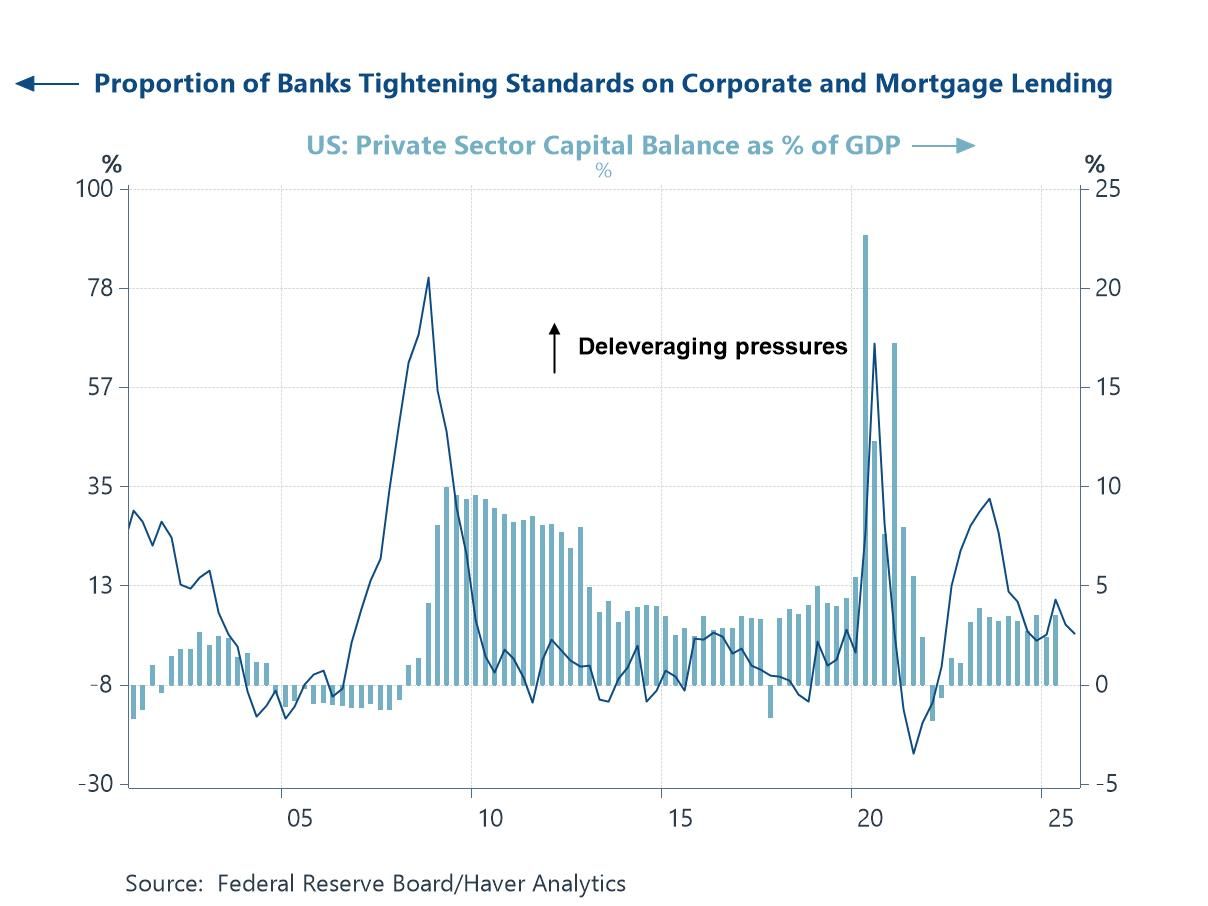

US credit standards The latest Senior Loan Officer Opinion Survey (SLOOS) from the Federal Reserve suggests that credit conditions remain tight but are no longer worsening, marking a tentative stabilization after several quarters of tightening. Banks reported modest easing in standards for some categories of corporate and commercial real estate loans, though mortgage lending remains constrained. Demand for business credit continues to soften, reflecting both higher borrowing costs and a cautious corporate outlook. Historically, periods of widespread tightening—like those seen in 2008 and 2020—have coincided with sharp rises in the private sector savings balance (a proxy for deleveraging), as firms and households retrench simultaneously. The current configuration, shown in the chart, indicates lingering deleveraging pressures, but not a collapse in credit availability.

Chart 2: US bank lending standards versus the private sector savings balance

China Moving to China, the latest official and Caixin PMI releases for October painted a mixed picture of activity. Both manufacturing indices softened, suggesting that the industrial rebound which underpinned much of China’s recent growth may be losing some traction. The official non-manufacturing PMI, by contrast, edged higher, hinting at continued resilience in construction and public-sector-linked services, while the Caixin services measure—which tends to reflect smaller, private-sector firms—slipped modestly. The divergence underscores China’s two-speed recovery: industrial production and exports have carried the economy, while household spending and smaller enterprises remain subdued. If manufacturing momentum fades in the coming months, the economy could face a renewed loss of balance, with fewer reliable growth engines. Still, overall performance this year has surpassed expectations, and the government’s 5% growth target remains within reach, provided activity holds steady through year-end. Looking ahead, marginal policy support and improved external sentiment—helped by selective tariff relief from the US—could offer limited, though welcome, cushioning.

Chart 3: China’s official and private sector PMIs

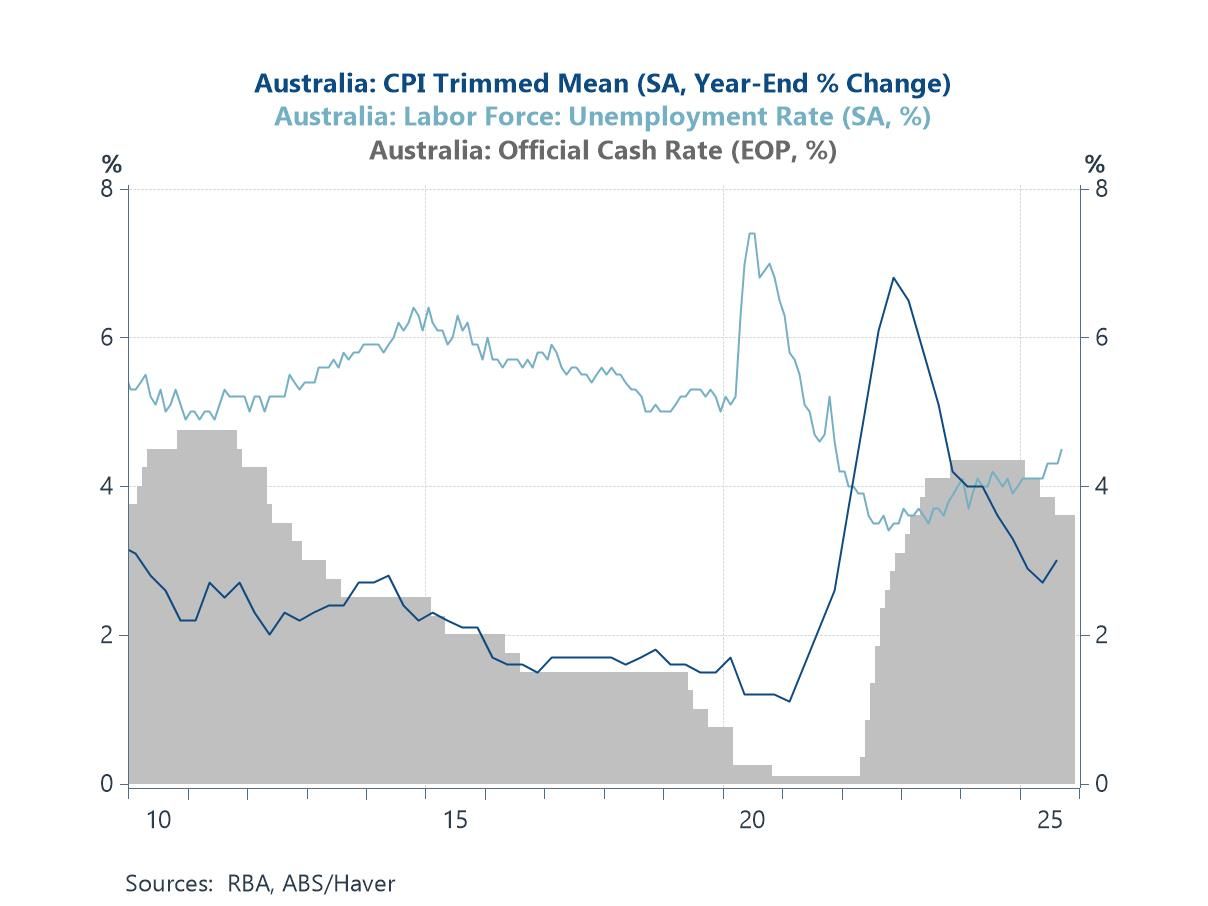

Australia In Australia, the RBA left the cash rate unchanged at its November meeting, maintaining a cautious stance amid a still-complex inflation and growth backdrop. The case for further easing has become less compelling as core inflation (trimmed mean CPI) remains above target and labour market conditions—while gradually softening—continue to show resilience. The unemployment rate has edged higher but remains low by historical standards, consistent with lingering wage and services price pressures. Recent data also hint at a tentative pickup in activity, supported by strong population growth and stabilising commodity exports. Against that backdrop, the RBA has stressed that the path for policy remains finely balanced, with a strong focus on incoming inflation data and global financial conditions. While downside risks persist—particularly from China’s slowdown and weak global trade—the persistence of domestic price pressures means the bar for renewed rate cuts remains relatively high.

Chart 4: Australia’s inflation, unemployment rate, and RBA policy rate

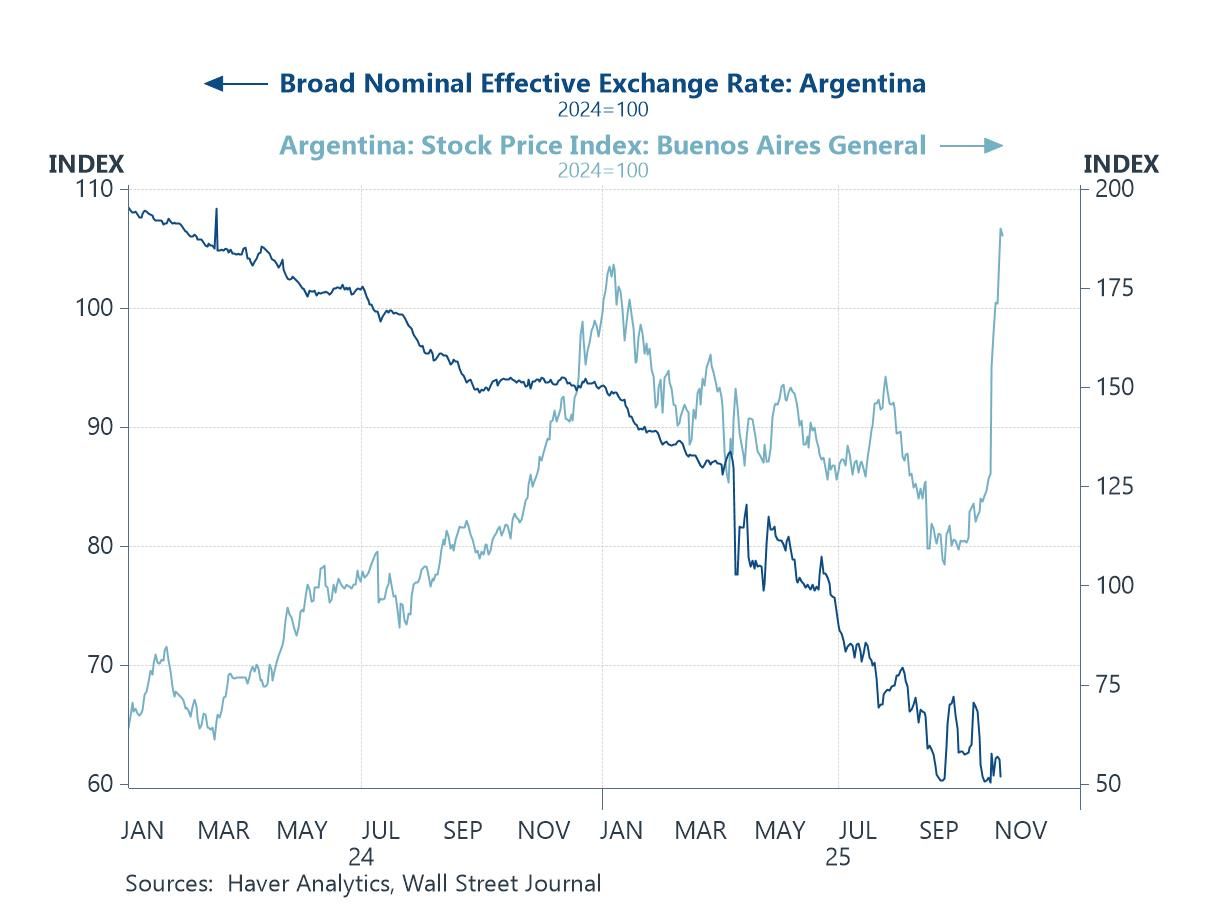

Argentina Turning to Argentina, markets continue to digest the implications of President Milei’s midterm election victory amid deepening economic and financial imbalances. The peso’s broad nominal effective exchange rate has remained under heavy pressure, extending its long-running slide as investors weigh the challenges of implementing fiscal consolidation and monetary reform in a fragile political and social environment. In stark contrast, the Buenos Aires stock index has surged to record highs, reflecting optimism that Milei’s reformist agenda—anchored in deregulation, privatisation, and fiscal restraint—may eventually stabilise the economy and attract renewed capital inflows. The divergence between a falling currency and soaring equity prices highlights the tension between near-term macro risks and longer-term reform hopes. Going forward, investor confidence will hinge on the government’s ability to deliver credible policy execution while managing the inflationary fallout from ongoing peso weakness.

Chart 5: Argentina equities and peso

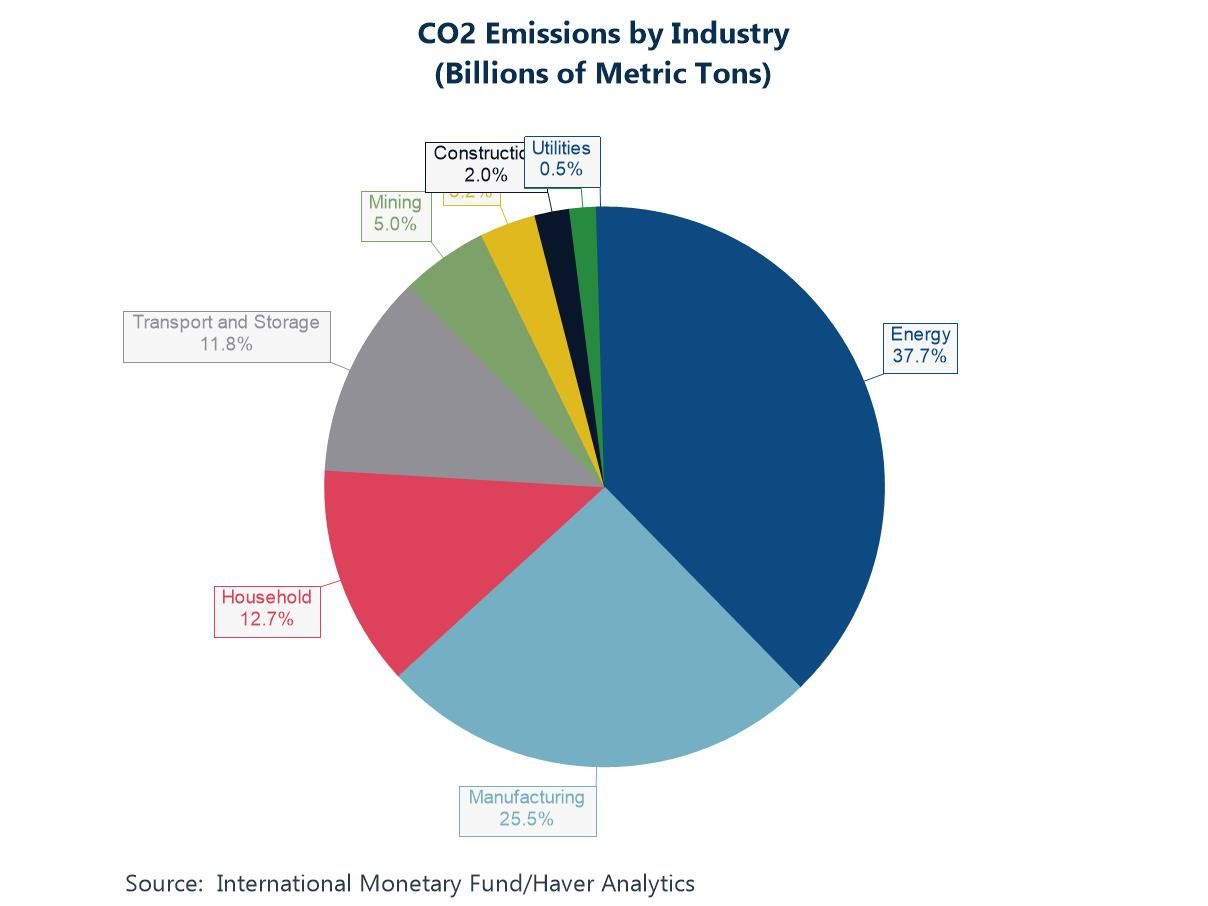

Global CO2 emissions Shifting focus to more structural issues, the chart underscores how decarbonisation challenges remain deeply concentrated in a few heavy-emitting sectors. Energy production alone accounts for nearly 40% of global CO₂ emissions, with manufacturing, households, and transport together contributing another 50%. This composition highlights the complex trade-offs of the energy transition: the very sectors that underpin modern living standards—power generation, industrial output, mobility, and housing—are also those most difficult to decarbonise. Climate change is therefore not just an environmental issue but a structural economic one, shaping investment, infrastructure, and pricing systems for decades to come. The tension between sustaining growth and cutting emissions will remain a defining challenge for policymakers, particularly as clean technologies face constraints in scaling fast enough to offset rising global demand for energy-intensive goods and services.

Chart 6: Global CO2 emissions by industry

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief