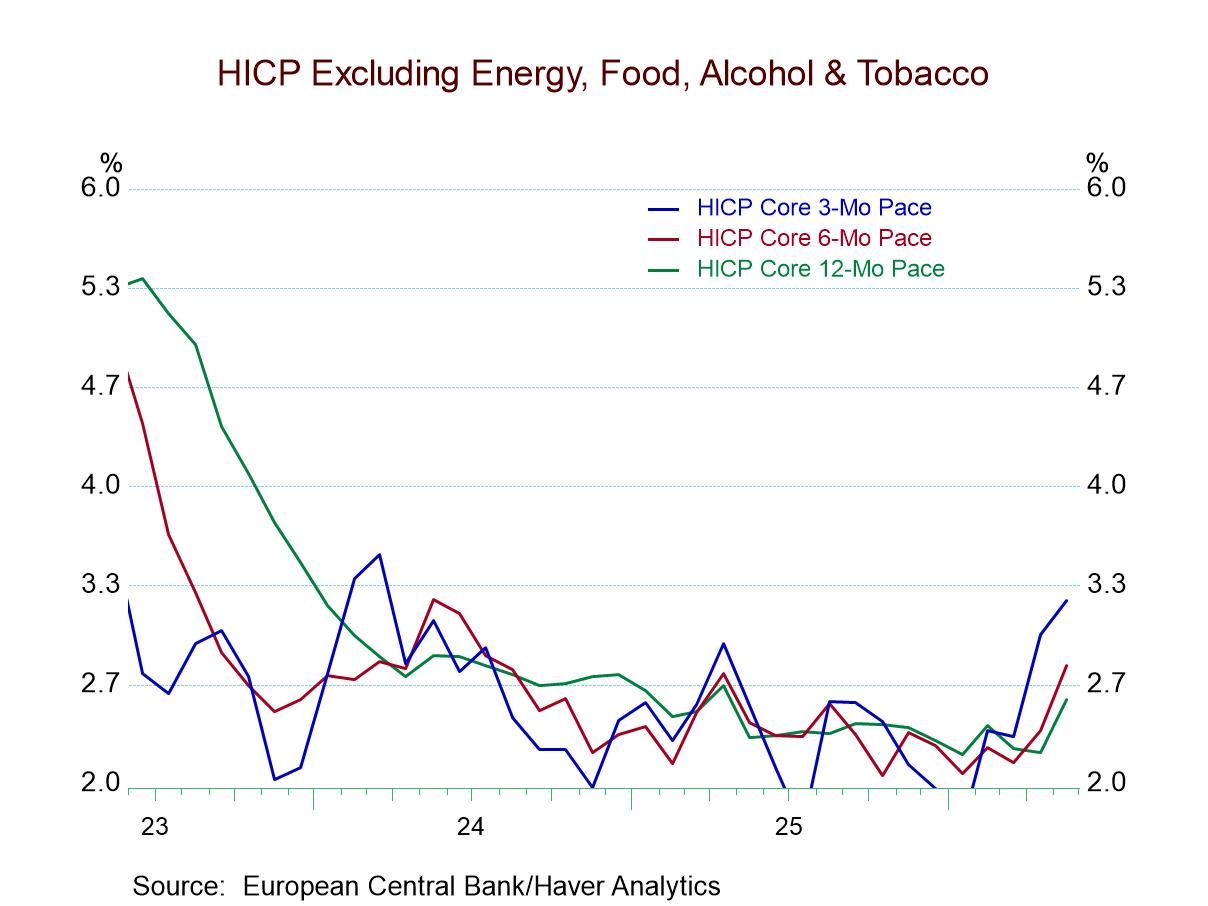

The chart shows European Monetary Union inflation using seasonally adjusted data to produce 12-month, 6-month, and 3-month compounded annual rates of change for the core, yielding a clear picture of acceleration. The core rate is supposed to be relatively less affected when energy prices spurt. However, in this case, the increase in energy prices is so large that it is being passed on across commodity classes because of its impact on transportation costs, an effect that is ubiquitous.

Every product must be brought to market, and apart from that, products have different intrinsic exposures to energy as a direct or indirect input, either because it's a chemical, it uses plastic, or it's more insulated as a service. However, the impact on transportation costs is broad.

The table shows year-over-year inflation monthly, and there you can see that the headline is moving up more than the core. However, the core rate is moving up, and at 2.5%, it's far enough above the ECB's 2% target for it to be considered too strong. The headline rate in May at 3.2% is considerably higher and stronger, but it's also more affected by energy prices and therefore it may represent something the ECB could view with a bit more flexibility. However, the strength in the core is going to cause the ECB more problems.

Along the bottom of the table, we look at the details on inflation to see the incidence of acceleration of inflation over three-month and six-month periods to give trends a bit of breathing room to develop. For both the headline and the core, the breadth of inflation is rising. Headline and core measures both are rising in nearly two-thirds of the categories (62.5%).

We take a broader look to see where inflation ranks historically on data back to 2001. The headline measure has inflation at the 88.5 percentile, while core is at the 86.2 percentile. Both demonstrate considerable strength in May. Looking at the details by category by stepping back one month to April, we find that one of the highest standings for inflation is in transportation, which is no surprise given what's going on with energy prices. Communications products, however, have a high inflation at their 98.7 percentile. Personal care products have a standing on their 92nd percentile, another high standing. Inflation for recreation and culture has a relatively low standing in its 36th percentile, and house furniture and maintenance prices have only a 16.4 percentile standing.

There are differences in inflation rates and inflation pass-throughs from energy effects. But the dispersion of inflation is only about a top one-third phenomenon—high but not extreme. That suggests that the impact on inflation, while significant, is not—at least not yet—dominant. We'll be watching indicators like this to get some idea of how impactful and broad the effects of inflation from the Middle East conflict are and how they will develop. For now, the impact is substantial and still seems to be in full swing.

Asia

Asia