U.S. New Home Sales Surge in August Amid Lower Mortgage Rates

Summary

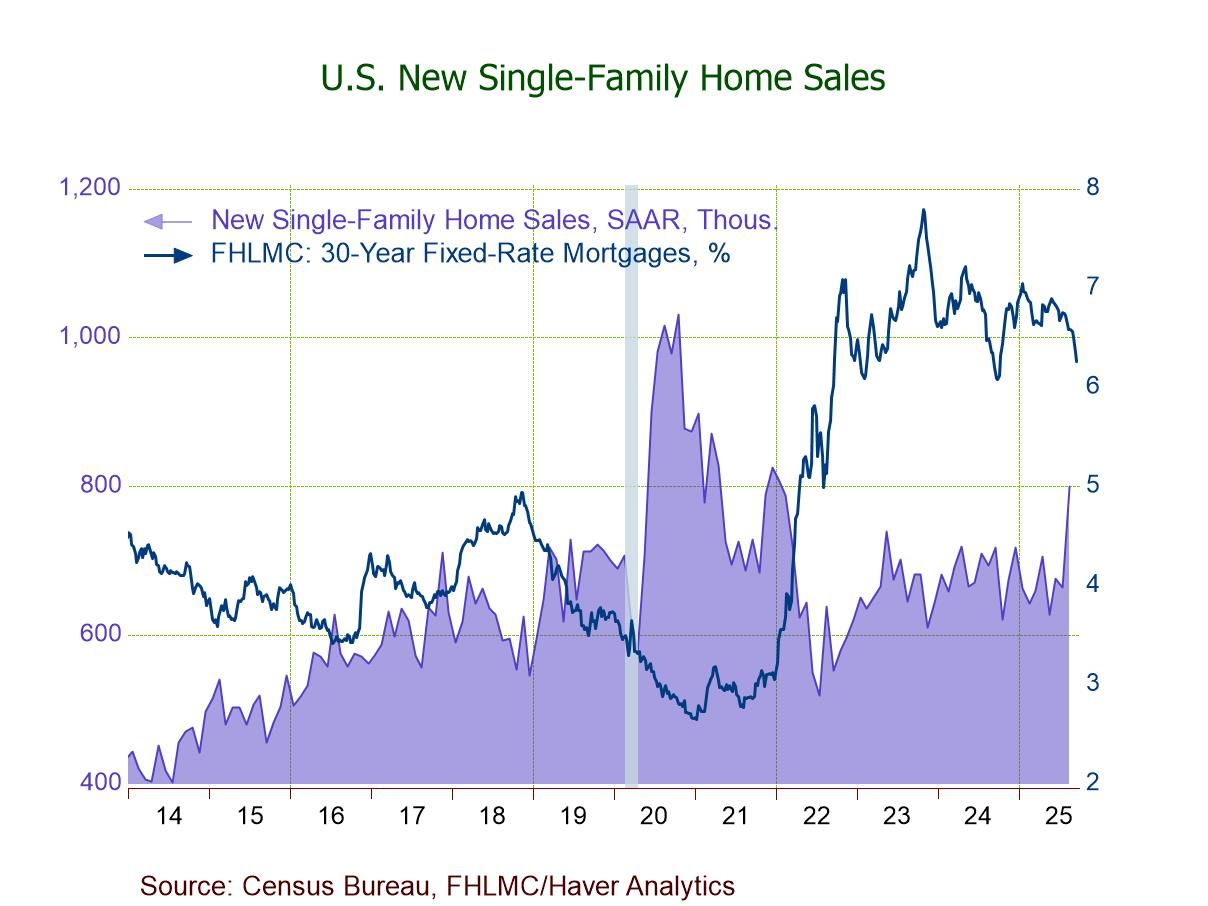

- August sales +20.5% (+15.4% y/y) to 800,000; largest m/m gain in 3 yrs.; highest level since Jan. '22.

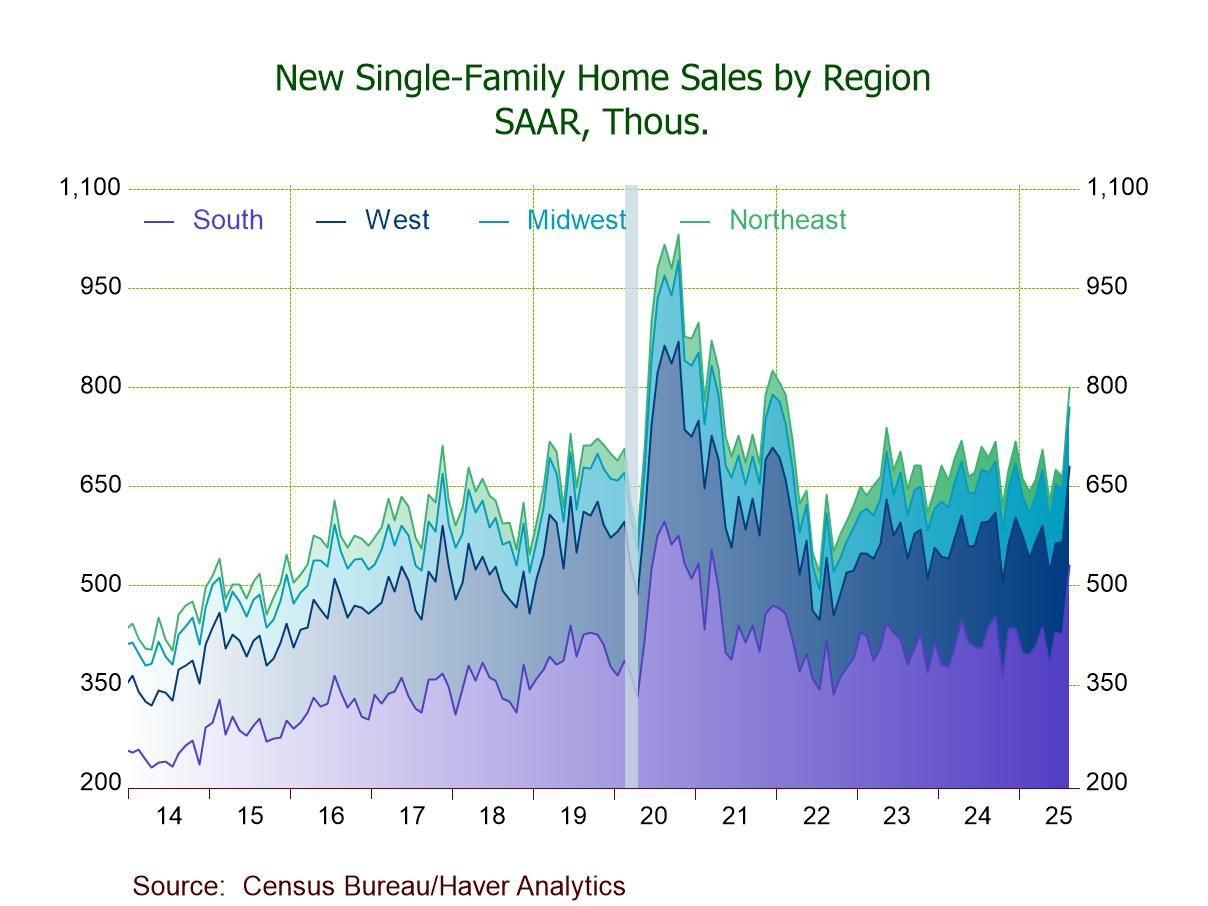

- Sales up m/m in all four regions; sales down y/y only in the West (-5.7% y/y).

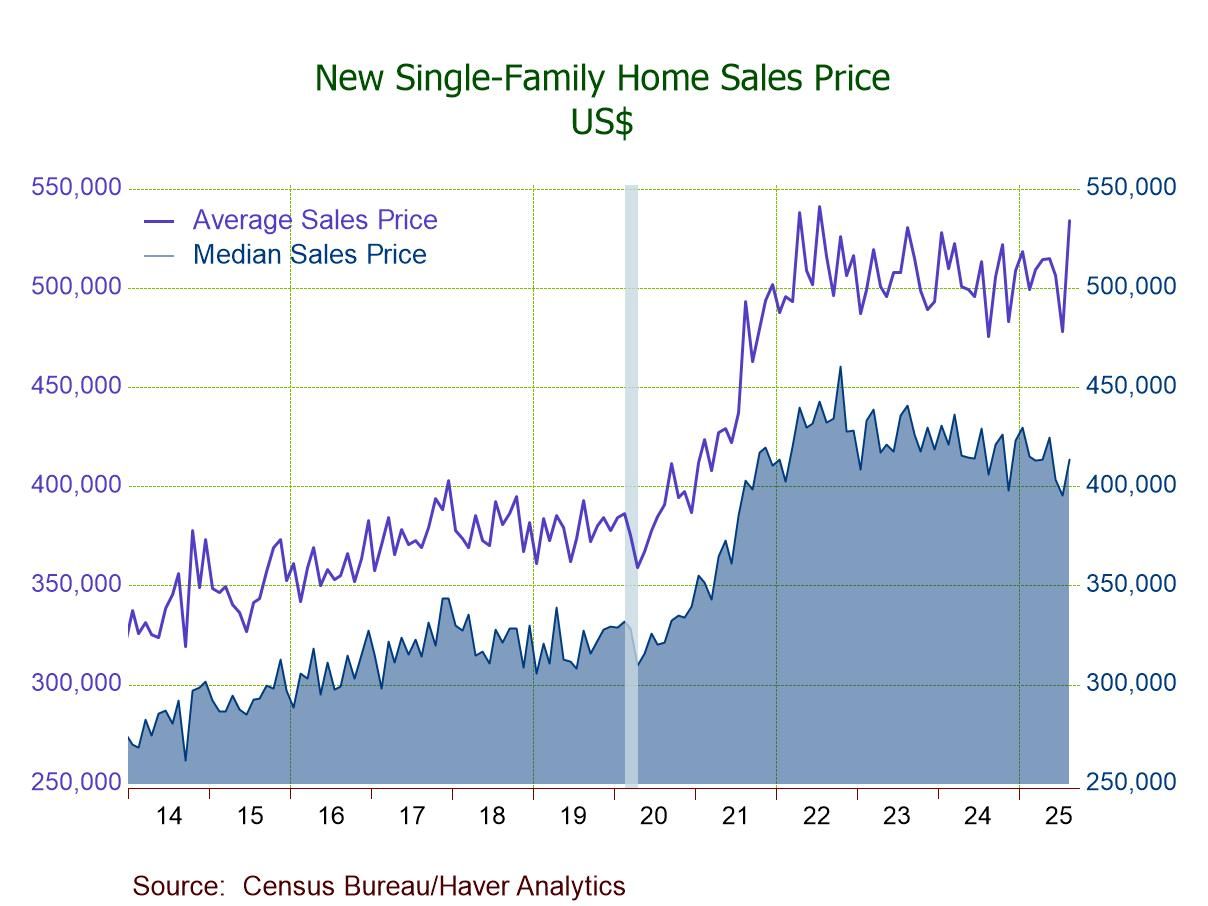

- Median sales price at a 3-month-high $413,500; avg. sales price at a 3-year-high $534,100.

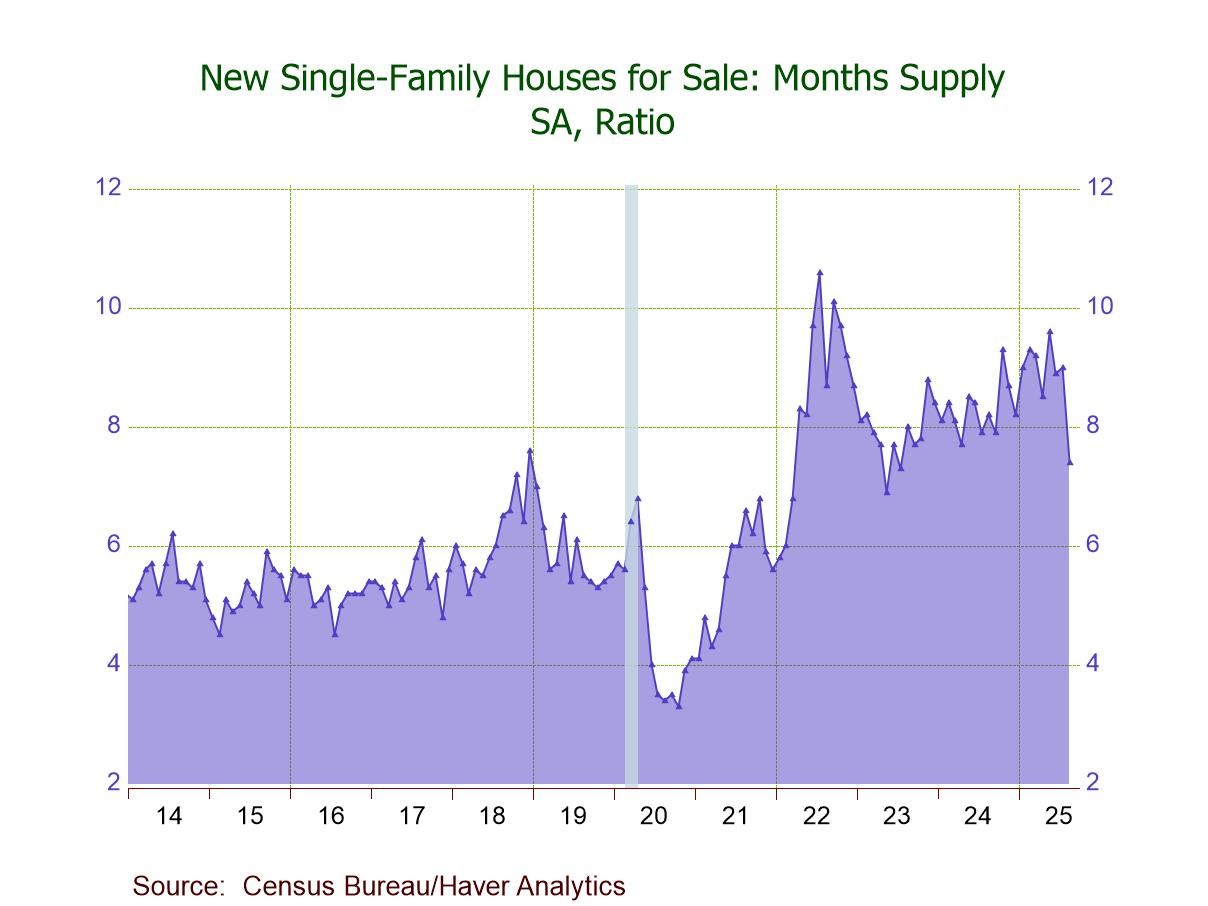

- Months' supply of new homes for sale drops to 7.4 mths., lowest since July '23.

New single-family home sales jumped 20.5% m/m (15.4% y/y) to 800,000 units at an annual rate in August following a 1.8% drop to 664,000 in July (-0.6%, 652,000 initially) and a 7.8% rebound to 676,000 in June (+4.1%, 656,000 previously), data from the U.S. Census Bureau showed. The Action Economics Forecast Survey expected sales of 650,000 in August. The August m/m jump was the biggest since August 2022; the 800,000 level was the highest since January 2022. New home sales had advanced 54.1% since a low of 519,000 in July 2022. The sales gain coincided with a decline in the average 30-year fixed mortgage rate to 6.59% in August, the lowest since October 2024, after a decrease to 6.72% in July; it had subsequently fallen to 6.35% in the September 11 week and 6.26% in the September 18 week, according to Freddie Mac.

By region, month-on-month new home sales rose in August across all four major regions. Sales in the Northeast surged 72.2% (40.9% y/y) in August, the largest m/m gain since January 2024, to 31,000, the highest level since February, following three straight m/m falls. Sales in the South jumped 24.7% (21.0% y/y) to 530,000, the highest level since March 2021, after a 0.7% July decline. Sales in the Midwest gained 12.7% (20.3% y/y) to 89,000, reversing an 11.2% July drop and returning to the June level. Sales in the West rose 5.6% (-5.7% y/y) to 150,000, the highest level since April, following a 5.2% July rise and three consecutive m/m decreases. Notably, the South continued to post the highest new home sales level (530,000) among the four regions, while the West was the only region with a year-on-year decline (-5.7% y/y) in August.

The median sales price of a new home rose 4.7% (1.9% y/y) to $413,500 in August following a 2.1% decline to $395,100 in July ($403,800 initially), registering the first m/m rise and the highest since May. The median sales price had fallen 10.2% since its record high of $460,300 in October 2022. The average sales price of a new home jumped 11.7% (12.3% y/y) to $534,100 in August, the highest since July 2022, reversing two successive m/m declines. The average price was 1.3% below a high of $541,200 in July 2022. These sales price data are not seasonally adjusted.

The number of unsold new homes on the market fell 1.4% (+4.0% y/y) in August, the fourth m/m fall in five months, to 490,000, the lowest level since December 2024, on top of a 1.2% decline to 497,000 in July. The latest figure was 15.0% above a low of 426,000 in July 2023. The seasonally adjusted months' supply of new homes for sale fell to 7.4 months in August, the lowest level since July 2023, after edging up to 9.0 months in July. The latest reading, while above a low of 6.9 months in May 2023, remained below a high of 10.6 months in July 2022.

The median number of months a new home stayed on the market held at 2.7 months in August for the third straight month, after declining m/m to 2.4 months in May. The latest number was well above its record low of 1.5 months in both September and October of 2022 but below a high of 5.1 months in March 2021. These figures date back to January 1975.

New home sales are recorded when the sales contract is signed. New home sales activity and prices are available in Haver's USECON database. The consensus expectation figure from Action Economics is available in the AS1REPNA database.

Winnie Tapasanun

AuthorMore in Author Profile »Winnie Tapasanun has been working for Haver Analytics since 2013. She has 20+ years of working in the financial services industry. As Vice President and Economic Analyst at Globicus International, Inc., a New York-based company specializing in macroeconomics and financial markets, Winnie oversaw the company’s business operations, managed financial and economic data, and wrote daily reports on macroeconomics and financial markets. Prior to working at Globicus, she was Investment Promotion Officer at the New York Office of the Thailand Board of Investment (BOI) where she wrote monthly reports on the U.S. economic outlook, wrote reports on the outlook of key U.S. industries, and assisted investors on doing business and investment in Thailand. Prior to joining the BOI, she was Adjunct Professor teaching International Political Economy/International Relations at the City College of New York. Prior to her teaching experience at the CCNY, Winnie successfully completed internships at the United Nations. Winnie holds an MA Degree from Long Island University, New York. She also did graduate studies at Columbia University in the City of New York and doctoral requirements at the Graduate Center of the City University of New York. Her areas of specialization are international political economy, macroeconomics, financial markets, political economy, international relations, and business development/business strategy. Her regional specialization includes, but not limited to, Southeast Asia and East Asia. Winnie is bilingual in English and Thai with competency in French. She loves to travel (~30 countries) to better understand each country’s unique economy, fascinating culture and people as well as the global economy as a whole.

More Economy in Brief

Global

Global