Asia| Sep 22 2025

Asia| Sep 22 2025Economic Letter from Asia: Of Politics and Policy

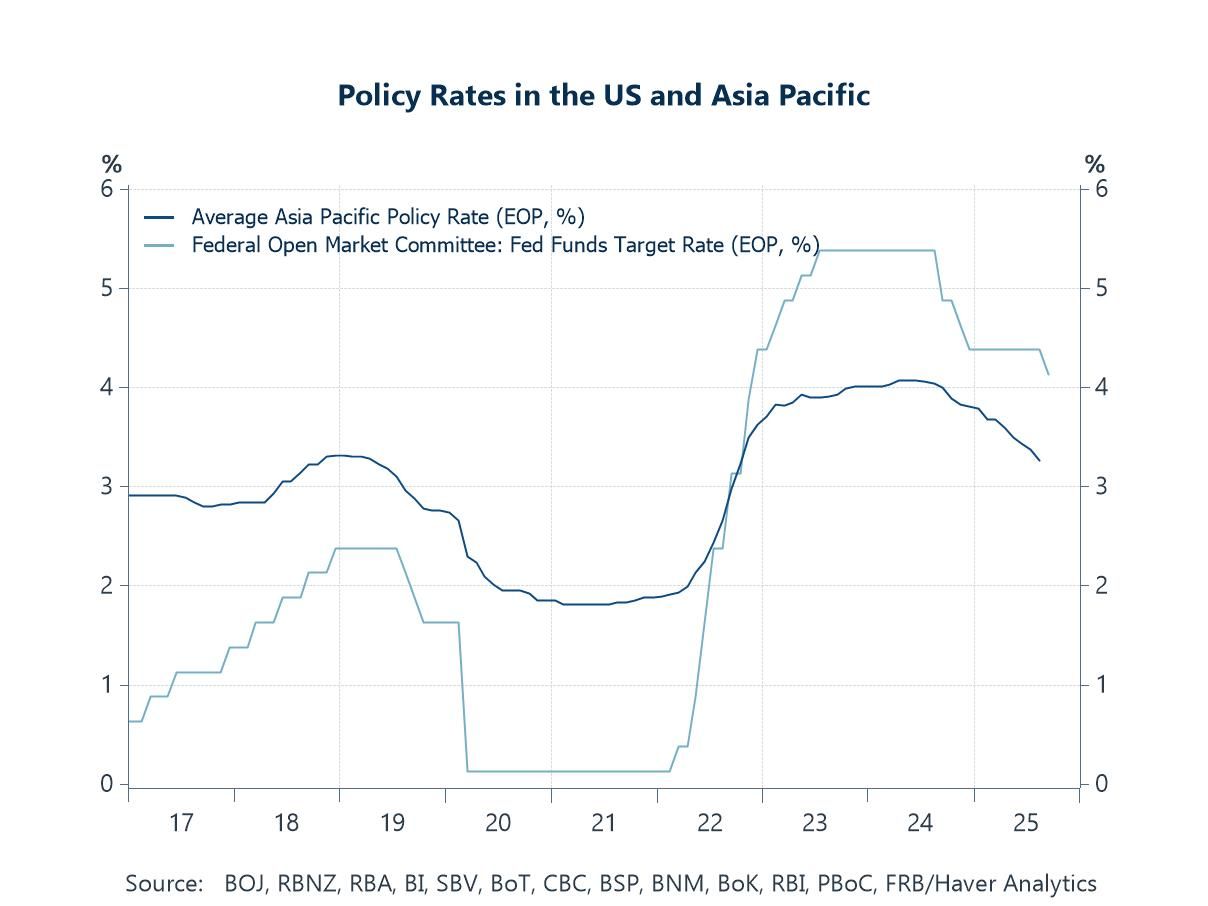

Following last week’s decision by the Fed to lower US interest rates, we examine Asia’s economic outlook, with particular focus on Japan, Indonesia, and Thailand. The Fed’s first rate cut of the year—while signalling more to come—has cleared the path for further easing from Asia’s central banks. Still, many regional central banks had already loosened policy despite wider yield differentials, responding to sluggish domestic demand, the growth drag from new US tariffs, and muted inflation pressures (chart 1). Across Asia, moreover, political turbulence risks distracting governments from tackling deeper structural challenges.

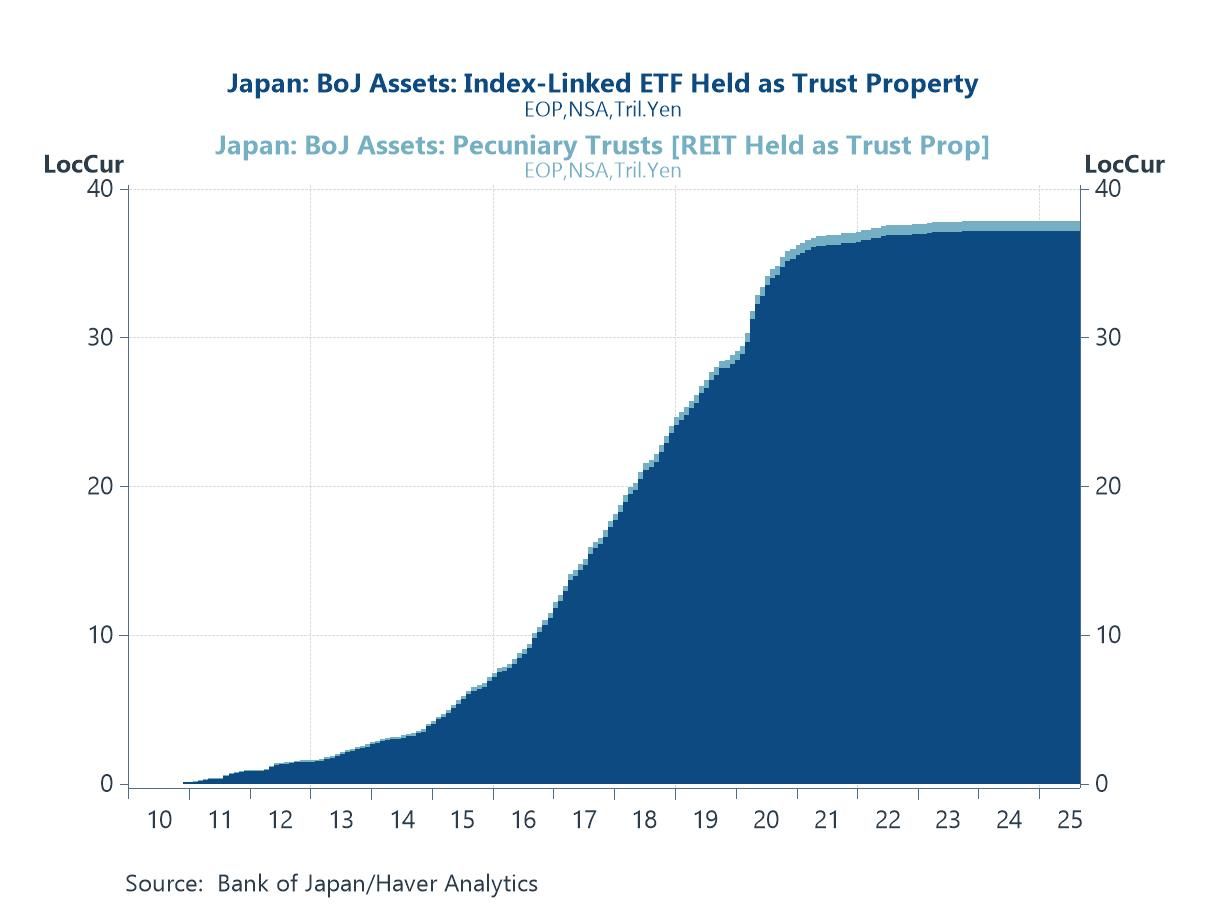

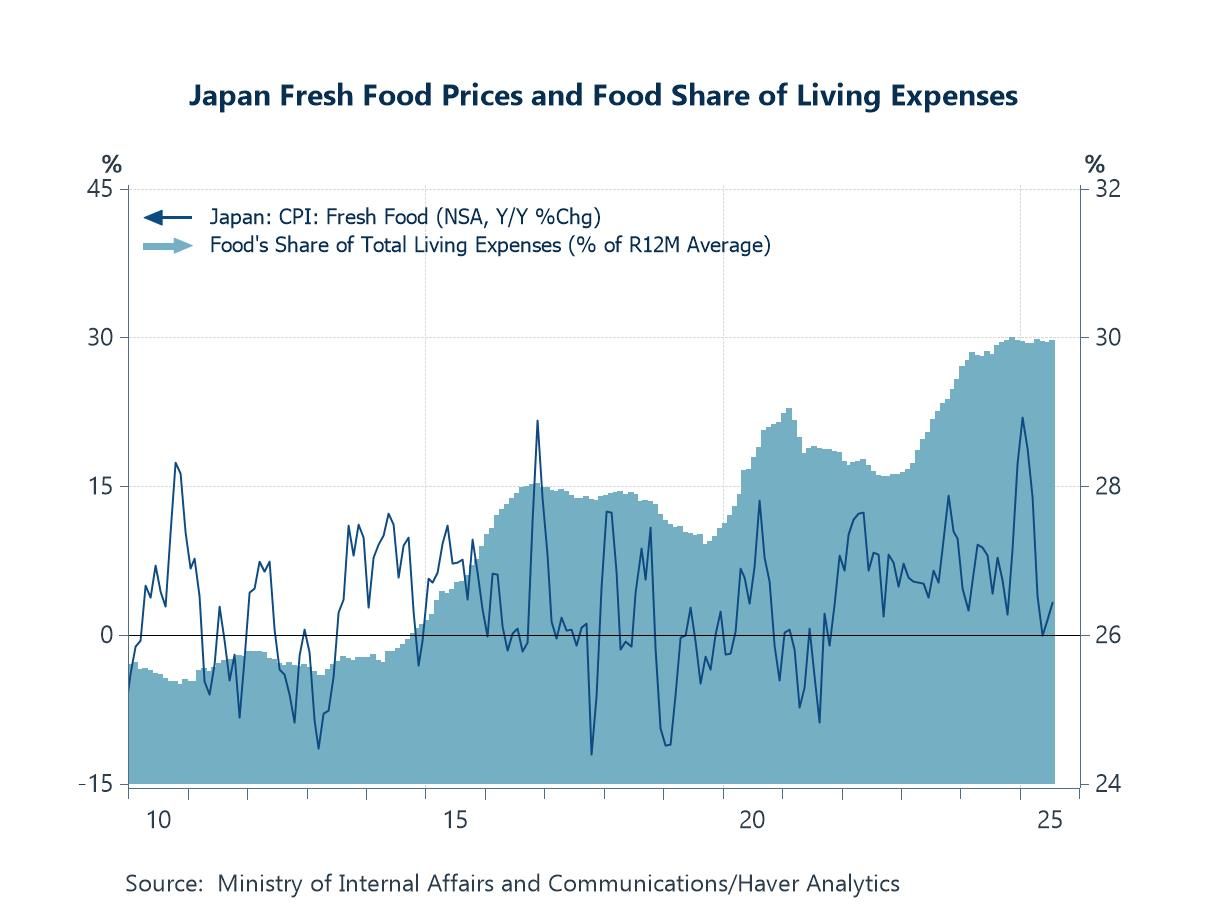

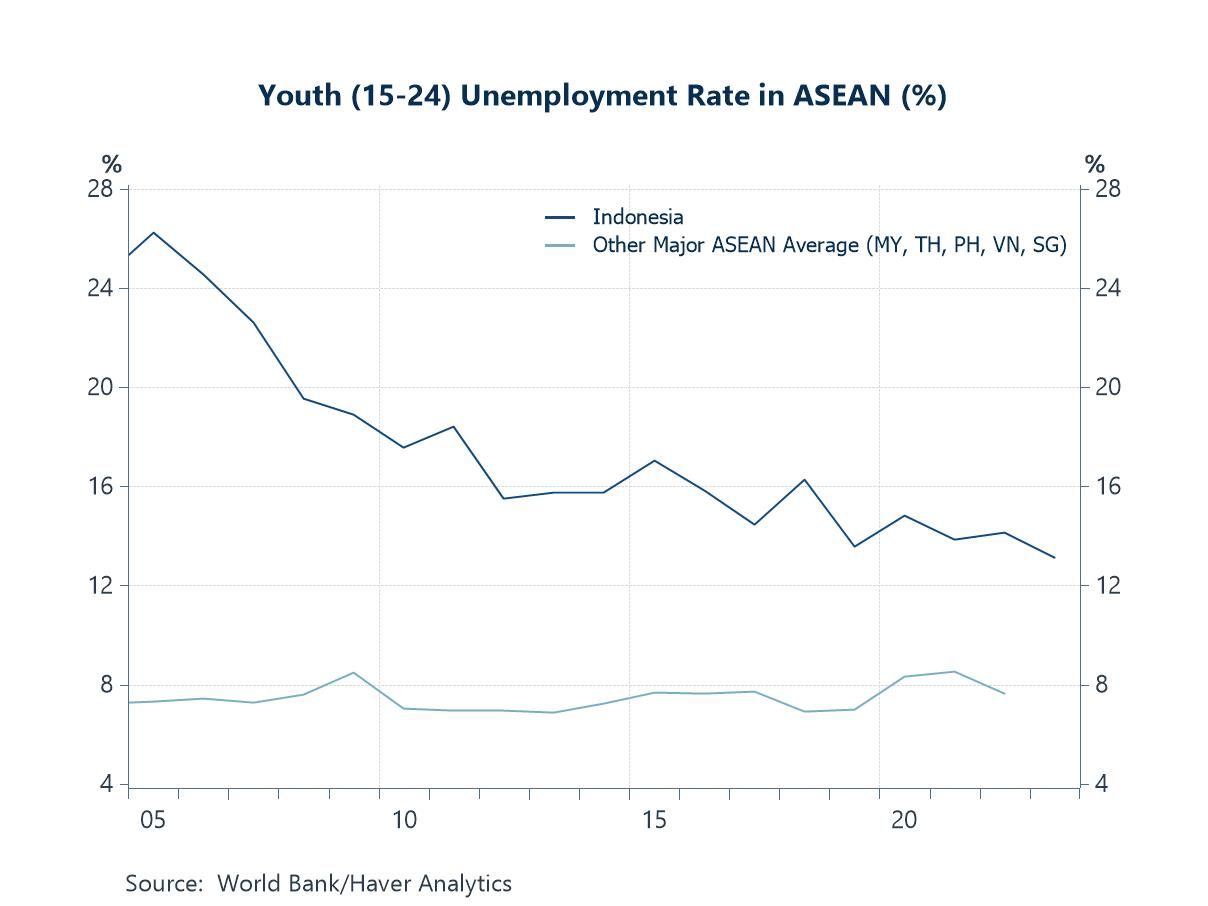

In Japan, the BoJ kept its policy rate unchanged as expected last week but announced the gradual unwinding of its large ETF and J-REIT holdings, a move likely to tighten liquidity (chart 2). On the political front, investors are watching the LDP’s two-week leadership contest, which culminates in an October 4th vote, with elevated food costs and broader inflation still pressing concerns (chart 3). Indonesia remains in focus as well, with investor concerns over fiscal discipline heightened by the recent removal of its long-serving Finance Minister. Long-standing issues, such as persistently high youth unemployment, continue to weigh as well (chart 4).

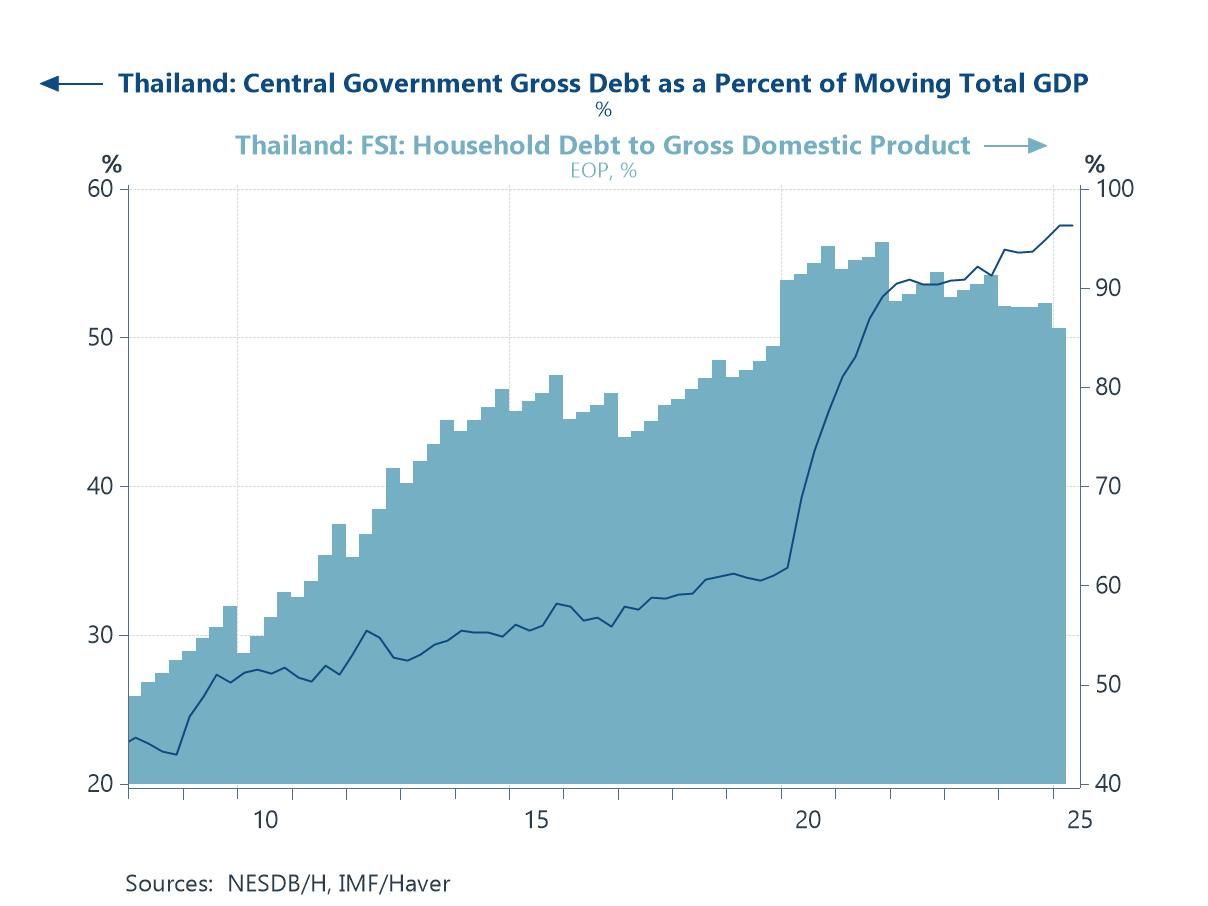

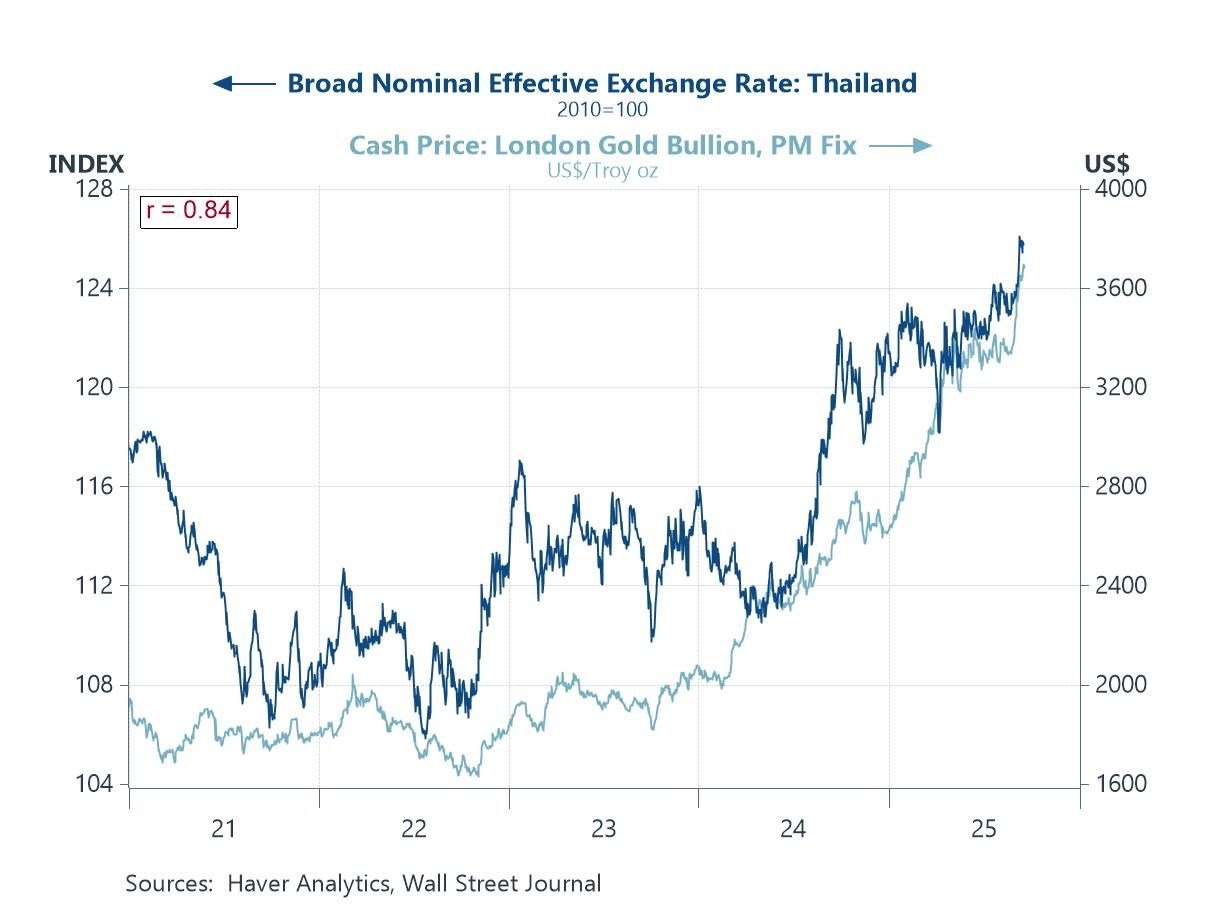

Thailand faces its own political uncertainty, with elections expected within four months after Prime Minister Anutin’s appointment. The interim push for near-term policy wins risks delaying structural reforms on household and public debt (chart 5). Meanwhile, the baht’s recent sharp appreciation—driven partly by surging gold prices (chart 6)—is straining exports and tourism, prompting the Bank of Thailand to explore measures to ease the currency’s gains, including taxing gold and encouraging US dollar-denominated trades.

Post-Fed reactions, implications As expected, the Fed cut its policy rate by 25 bps at its September meeting, marking its first reduction of the year after months of anticipation. The updated “dot plot” suggests two additional cuts may be on the horizon, though these projections remain data-dependent. The Fed’s move follows several rounds of easing by Asian central banks (chart 1), which cut rates despite wider US differentials to shore up weak domestic demand or offset risks from US tariffs. Contained headline CPI, driven by softer demand and the absence of broad supply shocks, has given the Asian policymakers room to ease. Looking ahead, further rate cuts across Asia—except in economies such as Japan, which maintain a tightening bias—remain possible. This is especially likely as the growth effects of the latest US tariff hikes, effective August 7th, have yet to be fully felt. If the Fed delivers additional easing later this year, it could further strengthen the case for Asian central banks to loosen policy again.

Chart 1: Policy rates in the US and Asia Pacific

Japan Last week also brought several key monetary policy decisions in Asia, including in Japan. As widely expected, the Bank of Japan (BoJ) kept its policy rate unchanged at 0.5% but signalled that further hikes remain possible later this year. More significantly, the BoJ announced it would begin selling its substantial holdings of exchange-traded funds (ETFs) and Japan real estate investment trusts (J-REITs), targeting annual sales of roughly 330 billion yen and 5 billion yen, respectively (see chart 2). This marks the start of unwinding purchases that began in late 2010 under the Asset Purchase Program (APP) and expanded significantly with the launch of Quantitative and Qualitative Easing (QQE) and its subsequent iterations. While the BoJ emphasized its intention to avoid disrupting markets, the start of asset sales effectively tightens liquidity and may exert downward pressure on asset prices.

Chart 2: Bank of Japan’s ETF and REIT holdings

Japan’s upcoming leadership contest is also drawing increasing attention following Prime Minister Ishiba’s recent resignation, announced in response to the ruling Liberal Democratic Party’s (LDP) heavy losses in the recent upper house elections. Investors are now focused on the party’s two-week leadership race, culminating in a vote on October 4th. The winner is expected to become Japan’s next prime minister given the LDP’s size. Also worth watching is the continued rise of populist rhetoric, both within the leadership campaign and from outside the party—a trend mirrored across parts of Asia amid heightened political uncertainty. For Japan, pressing issues remain, including stubborn inflation and its impact on the rising cost of living, particularly as food prices have steadily taken a larger share of household expenses over the last few years (chart 3).

Chart 3: Japan fresh food prices and food share of living expenses

Indonesia Political developments in Indonesia are also drawing investor attention, following recent widespread protests. More recently, concerns intensified after the replacement of the country’s longstanding former Finance Minister, raising questions about fiscal discipline. These concerns have been heightened amid scrutiny of the costs of Prime Minister Prabowo’s free school meals programme and the spending cuts it has necessitated elsewhere. More broadly, Indonesia continues to struggle with persistently high youth unemployment, which remains far above that of its Southeast Asian peers (see chart 4) and is a key factor contributing to the recent unrest. These long-standing challenges are further compounded by recent waves of layoffs and a structural mismatch between education outcomes and labour market needs.

Chart 4: Indonesia’s youth unemployment vs. Southeast Asian peers

Thailand Turning to Thailand, investors are closely watching the approaching parliamentary race. Current Prime Minister Anutin, who only recently took office following former Prime Minister Paetongtarn’s ouster, has pledged to dissolve parliament within four months, paving the way for fresh elections. In the meantime, Anutin has taken steps to solidify his credibility on delivering near-term promises. These include signing a binding Memorandum of Agreement (MoA) with the People’s Party that commits to dissolving the House within four months and bars his Bhumjaithai Party from forming a majority government. Despite the political noise, Thailand’s structural challenges—such as rising household debt and deteriorating public finances—remain unresolved, and the heightened focus on politics risks further delaying progress on longer-term reforms.

Chart 5: Thailand government and household debt

At the same time, recent financial market developments—most notably gold’s meteoric rise this year—have driven the baht higher, reflecting the strong price correlation between the two (chart 6). The surge in gold exports, much of which is traded in baht, has added to the currency’s strength. While a stronger baht might seem like good news, it poses challenges for an economy reliant on tourism and exports, as currency appreciation typically weighs on both sectors. In response, the Bank of Thailand is exploring measures to curb the baht’s gains, including imposing a gold tax and encouraging gold trading in US dollars.

Chart 6: The Thai baht and gold prices

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief