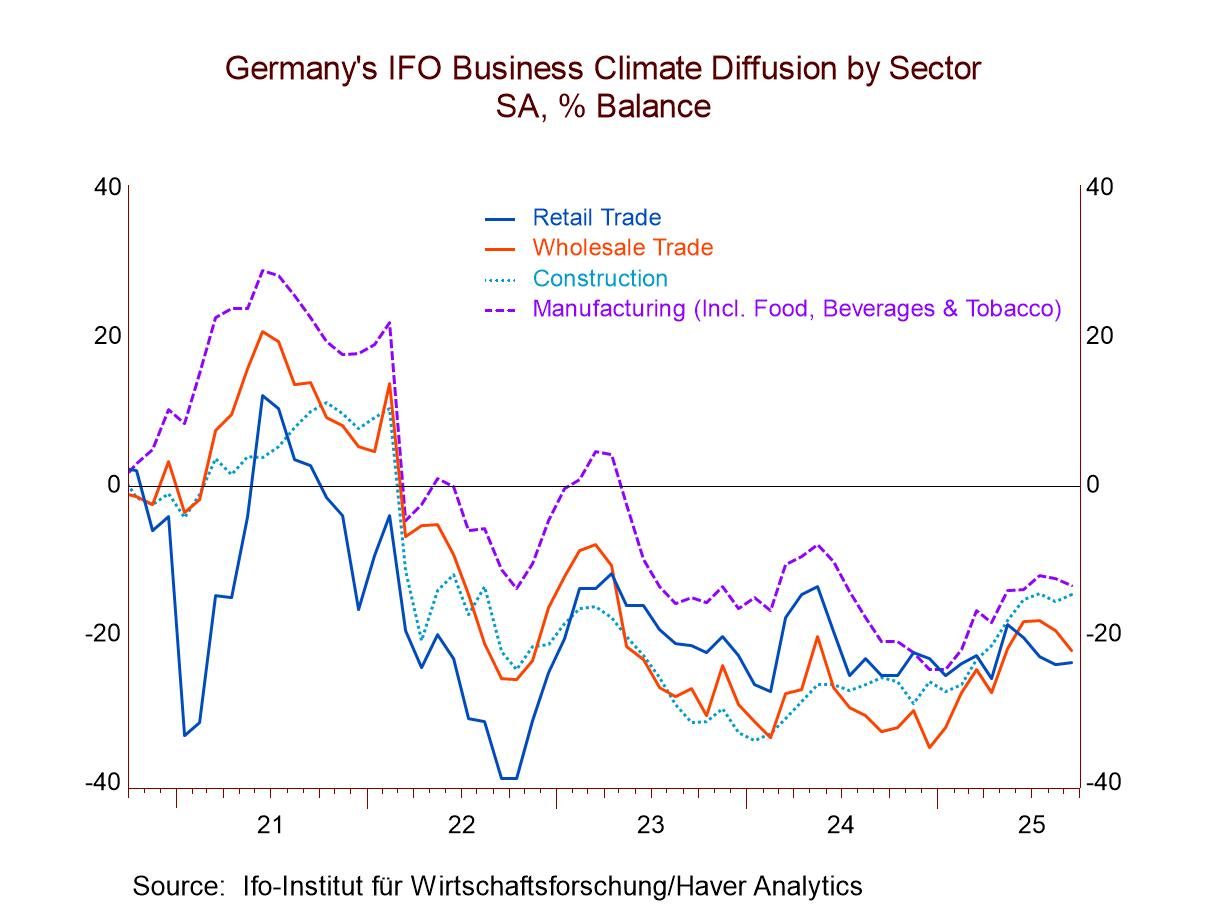

IFO Survey Setback in Germany

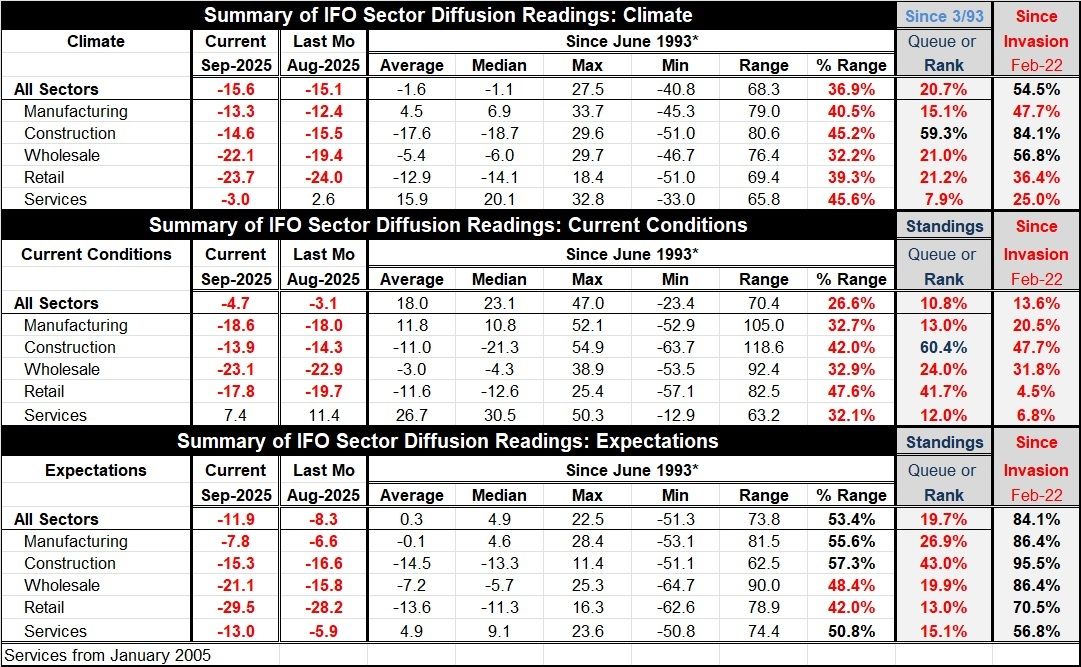

The IFO climate survey deteriorated in September, falling to -15.6 from -15.1 in August. The wholesale reading showed a deterioration, as did manufacturing and then services. Construction and retailing improved slightly. The climate all-sector ranking is at its 20.7 percentile. Even weaker is the ranking for services at 7.9% and the ranking for manufacturing at 15.1%. Only the construction sector has a ranking above 50%, which places it above its median value. Wholesale and retailing both have rankings in the 21st percentile.

Current conditions in September fell to a diffusion reading of -4.7 from -3.1 in August. The slippage was in manufacturing, wholesaling, and services once again with construction improving slightly and retailing improving to -17.8 from -19.7. The queue standing rankings have the all-sector current index in its 10.8 percentile. The individual sectors all have a higher ranking than that. The lower overall ranking reflects the confluence of weak rankings across sectors that is unusual. Manufacturing has a 13-percentile standing, services have a 12-percentile standing, with retailing at a 41.7 percentile standing and once again construction has a standing above its 50th percentile at the 60.4 percentile mark.

The expectations’ all-sector index falls to -11.9 in September from -8.3 in August; that drop is troubling because this is a forward-looking metric not simply a current assessment. The rank standing for expectations is in its 19.7 percentile, about the same ranking as for climate and above the current all-sector ranking. Retailing logs a 13-percentile standing, services are at a 15-percentile standing, and wholesaling at a 19.9, nearly 20-percentile standing. Manufacturing is at a 26.9 percentile standing with construction at a 43-percentile standing. All the metrics are below their 50th percentile in expectations, marking all of them below their historic medians on data back to 1993.

There is a far-right hand column that also presents ranking statistics. These are rankings since February 2022 since the invasion of Ukraine by Russia. For expectations, we see that after the invasion rankings are currently showing a lot of uplift although ominously the services sector, which is the job creating sector has only a 56.8 percentile standing; that compares to the all-sector expectation standing at its 84th percentile. Looking at climate the all-sector index is at 54.5%. That is much stronger than on the full data set back to 1993. The 54.5 percentile standing is supported by strong readings out of construction and wholesaling vs. weak greetings from retailing and services. But these weak rankings are still stronger than for the full sample. Readings for September current conditions on this shorter period remain about the same as for the full sample – except that retailing and services are much weaker.

Overall, the September IFO is disappointing and weaker. The performance of expectations is disturbing. These are going to be developments to watch in the coming months especially to see if expectations make a recovery.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global