Asia

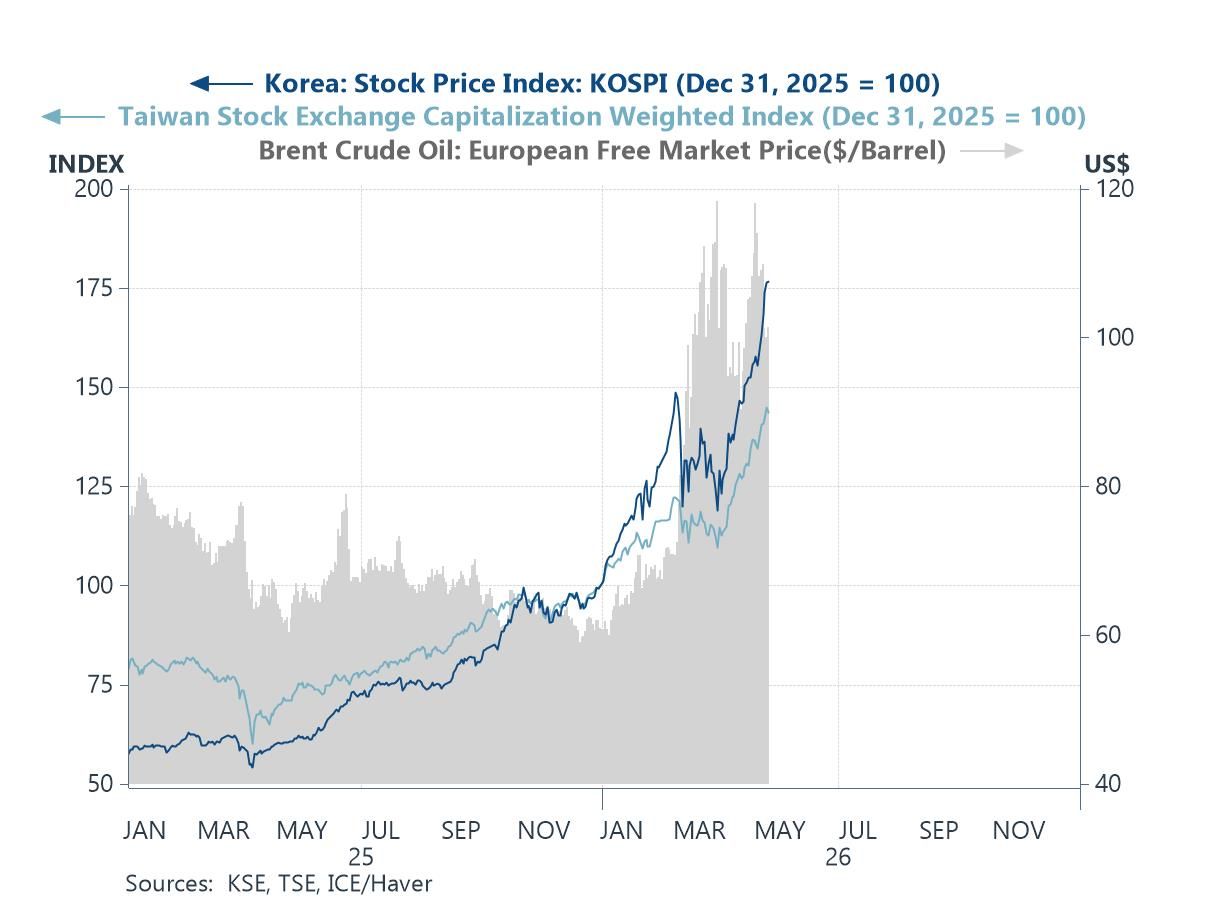

AsiaIn this week’s Letter, we track the dual drivers of AI optimism and the ongoing Middle East conflict, and how they continue to shape market prices and investor expectations. AI-related enthusiasm has remained a key support for equity markets, particularly in highly exposed indexes in Taiwan and South Korea, while continued oil supply bottlenecks stemming from the closure of the Strait of Hormuz have kept crude prices elevated (chart 1). These dual forces are also evident in the latest Blue Chip Economic Indicators survey. Year to date, all Asian economies have seen upward revisions to inflation forecasts, while the most AI-exposed advanced Asian economy, Taiwan, has recorded a particularly large upgrade to real GDP growth expectations (chart 2). Looking more closely at the monetary policy implications of higher oil prices, this month’s survey shows an increasing share of panellists expecting central banks to resume or extend tightening cycles, marking a modest shift from last month’s results (chart 3). This shift is already partially reflected in recent data, with average inflation across Asia edging higher and several central banks already opting to tighten policy in response (chart 4).

Looking ahead, attention will likely centre on the Trump–Xi summit taking place in Beijing later this week. While any potential for additional Chinese mediation efforts regarding the Middle East conflict will be closely watched, developments on the US–China trade front should not be overlooked given the range of unresolved issues (chart 5). Finally, despite recent headline focus on the Middle East, China has continued to post steady export growth, while also managing to temper excessive domestic producer competition. Together, this has supported a combination of firmer external demand and more stable pricing dynamics—an “all-win” outcome for now (chart 6).

AI vs. the Middle East conflict The divergence between AI-driven equity market optimism and the persistence of elevated crude oil prices amid the ongoing Middle East conflict remains striking. On the one hand, equity markets—particularly in AI-heavy economies such as Taiwan and South Korea (chart 1)—have largely shrugged off concerns over energy supply disruptions. Investors remain focused on the upside potential from the current AI buildout cycle, driven by the rising computational demands of increasingly capable AI models. More recently, attention has shifted toward the scalability and broader applications of physical AI, including humanoid robots, and their potential implications for manufacturing, healthcare, and even household use. On the other hand, crude oil prices remain well above pre-conflict levels. The latest development is the US rejection of Iran’s most recent peace proposal, underscoring that a swift resolution to the US-Iran conflict remains unlikely.