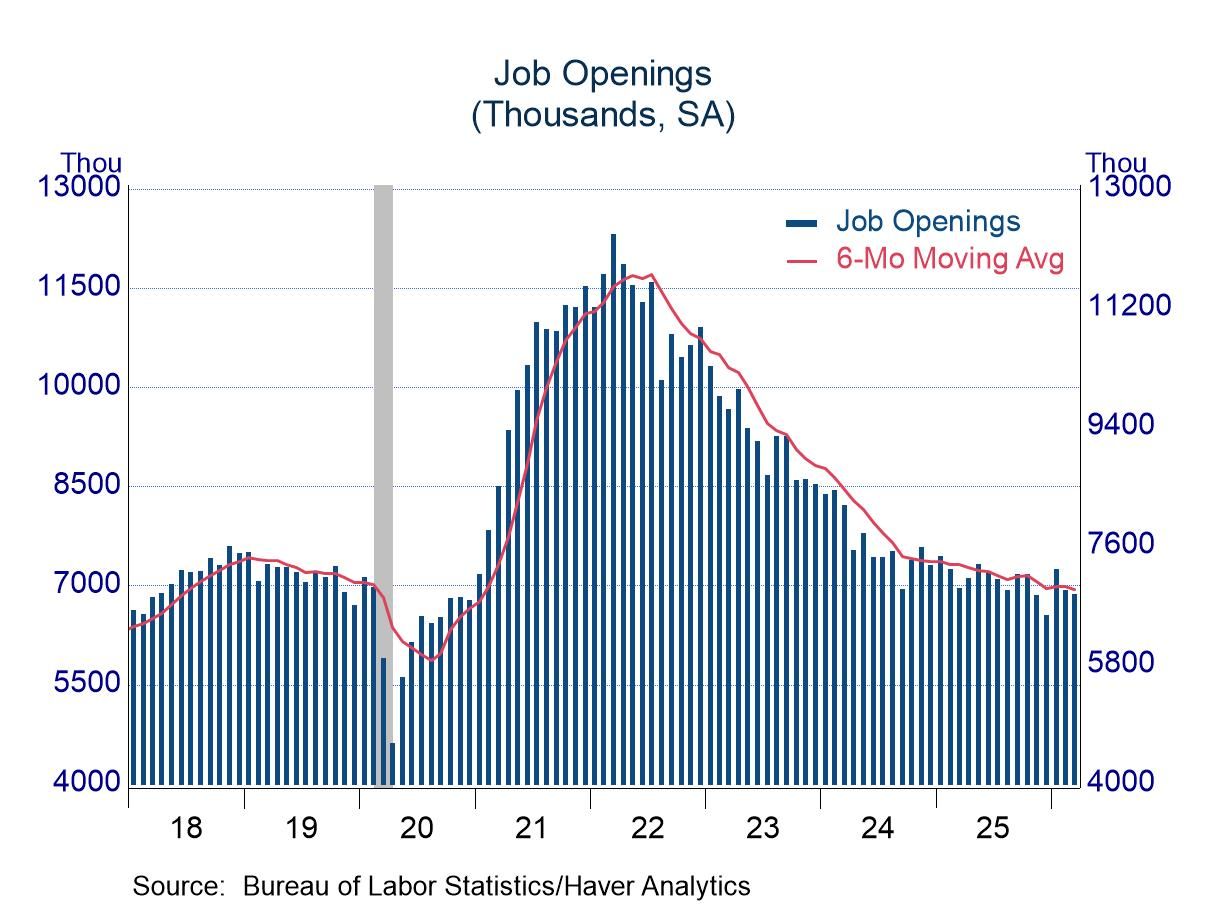

- Job openings were little changed...

- ...but hirings and layoffs picked up.

USA| May 05 2026

USA| May 05 2026Job Openings and Labor Turnover (JOLTS): Mixed Results in March

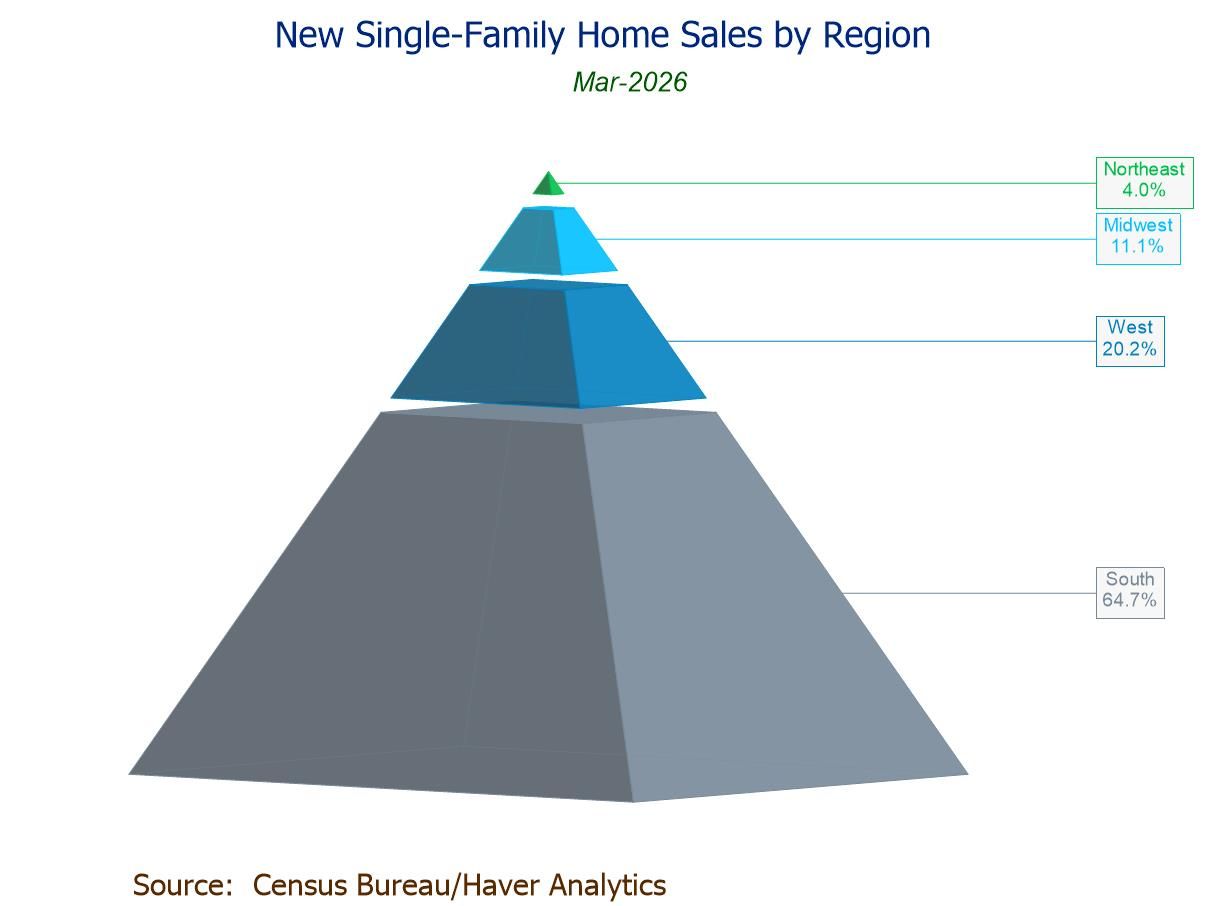

- Sales +7.4% m/m (+3.3% y/y) to 682,000 in Mar., a 3-month high; +8.9% m/m (-1.1% y/y) to 635,000 in Feb.

- Sales m/m up in the Northeast and South, down in the Midwest and West; sales y/y up in all regions except the West (-12.7% y/y).

- Median sales price -5.3% m/m to $387,400, lowest since Jul. ’21; avg. price -3.4% m/m to $503,100, lowest since Jul. ’25.

- Months' supply: 8.5 mths. in Mar., a 3-month low; 9.1 mths. in Feb.

USA| May 05 2026

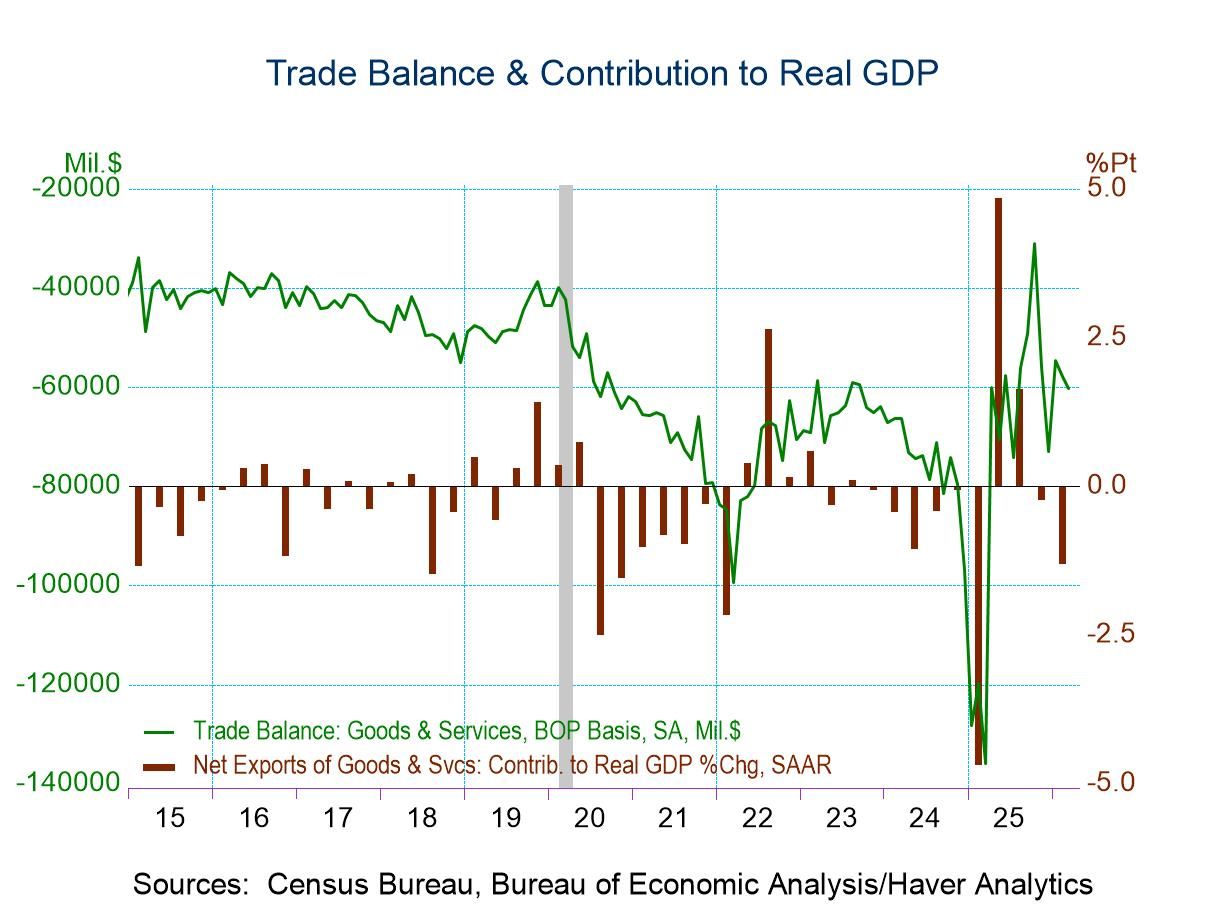

USA| May 05 2026U.S. Trade Deficit Widened in March

- The deficit in goods and services widened to $60.3 billion in March from $57.8 billion in February,

- Exports rose 2.0% m/m, led by a 33% monthly jump in petroleum exports.

- Imports increased 2.3% m/m, led by an 11.2% m/m jump in auto imports.

- The goods deficit widened to $88.7 billion while the services surplus widened to $28.4 billion.

by:Sandy Batten

|in:Economy in Brief

Asia| May 05 2026

Asia| May 05 2026Economic Letter from Asia: Everybody’s Changing

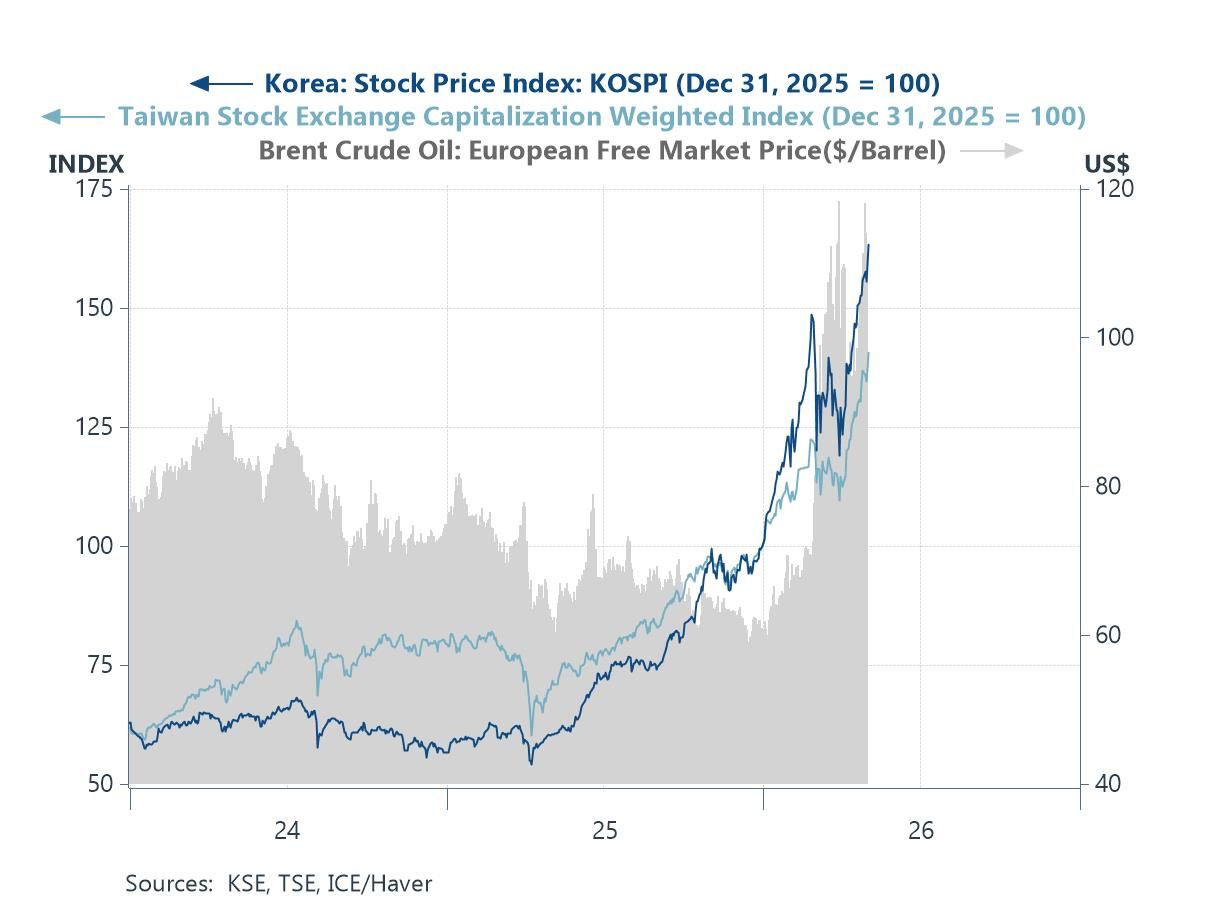

In this week’s Letter, we take another pulse on recent key developments relating to, and affecting, Asia. The week has once again begun on a hopeful note, following reports that the US will guide neutral vessels through the Strait of Hormuz, signalling a partial easing of trade flows through the waterway. Asian markets, including South Korea and Taiwan, were further buoyed by persistent AI-related optimism (chart 1). A full tally of central bank decisions since February highlights a growing divergence across the region. While most central banks have opted to hold back on tightening, a subset has already moved to raise policy rates in response to inflation pressures stemming from higher oil prices (chart 2). A cross-country comparison of consumer inflation reinforces this divergence, with more pronounced CPI increases in economies such as Australia and the Philippines, where central banks have recently hiked rates (chart 3).

In the meantime, amid the absence of oil flows through the Strait, many Asian importers have begun sourcing supplies from alternative producers, including the United States (chart 4). At the same time, major oil exporters affected by disruptions in the Strait of Hormuz have been forced to scale back crude production significantly due to storage constraints (chart 5). Looking ahead, attention turns to a three-pronged week featuring regional PMIs, additional central bank decisions (chart 6), and further Q1 GDP releases.

Early-week optimism Asian markets began the week on an optimistic footing, supported by developments in the Middle East. Reports that the US will guide neutral vessels through the Strait of Hormuz have lifted expectations of a partial resumption in trade flows through what has been a severely constrained passage. That said, while any reopening of oil and broader shipping routes is a key factor in easing the supply shock stemming from the conflict, the situation remains far from resolved. Uncertainty persists over both the scale and durability of any recovery in shipping activity. Elevated tensions between the US and Iran—underscored by exchanges of fire as US forces escorted vessels through the waterway on Monday—continue to leave the outlook vulnerable to renewed disruption. Nonetheless, ongoing AI-related optimism has continued to underpin equity markets. Asia stands to benefit disproportionately given its central role in the global AI supply chain, helping keep equity prices elevated across key markets such as South Korea and Taiwan (chart 1).

USA| May 04 2026

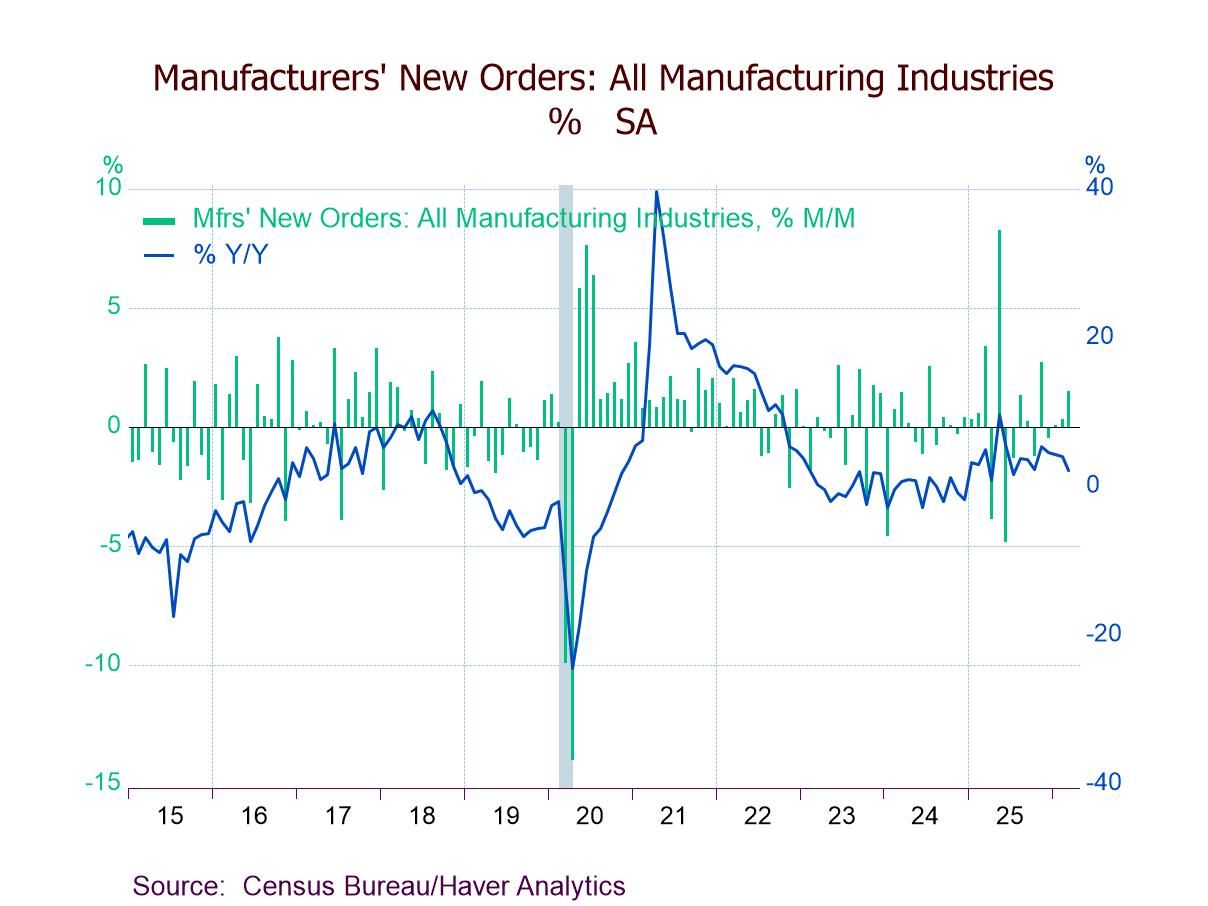

USA| May 04 2026U.S. Factory Orders Exceed Expectations in March

- Factory orders +1.5% m/m (+2.1% y/y) in Mar.; 9.5% above the Jan. ’24 low.

- Durable goods orders +0.8%, first m/m increase since Nov.; nondurable goods orders +2.1%, largest of four straight m/m gains; shipments +1.4%, fourth successive m/m rise.

- Transportation orders +0.8%, driven by m/m surges of 30.9% in ships & boats and 17.8% in defense aircraft orders.

- Computers & electronic products +3.6%, fastest of seven consecutive m/m rises.

- Unfilled orders +0.1%, eighth straight m/m increase.

- Inventories +0.6%, biggest of five consecutive m/m gains.

Global| May 04 2026

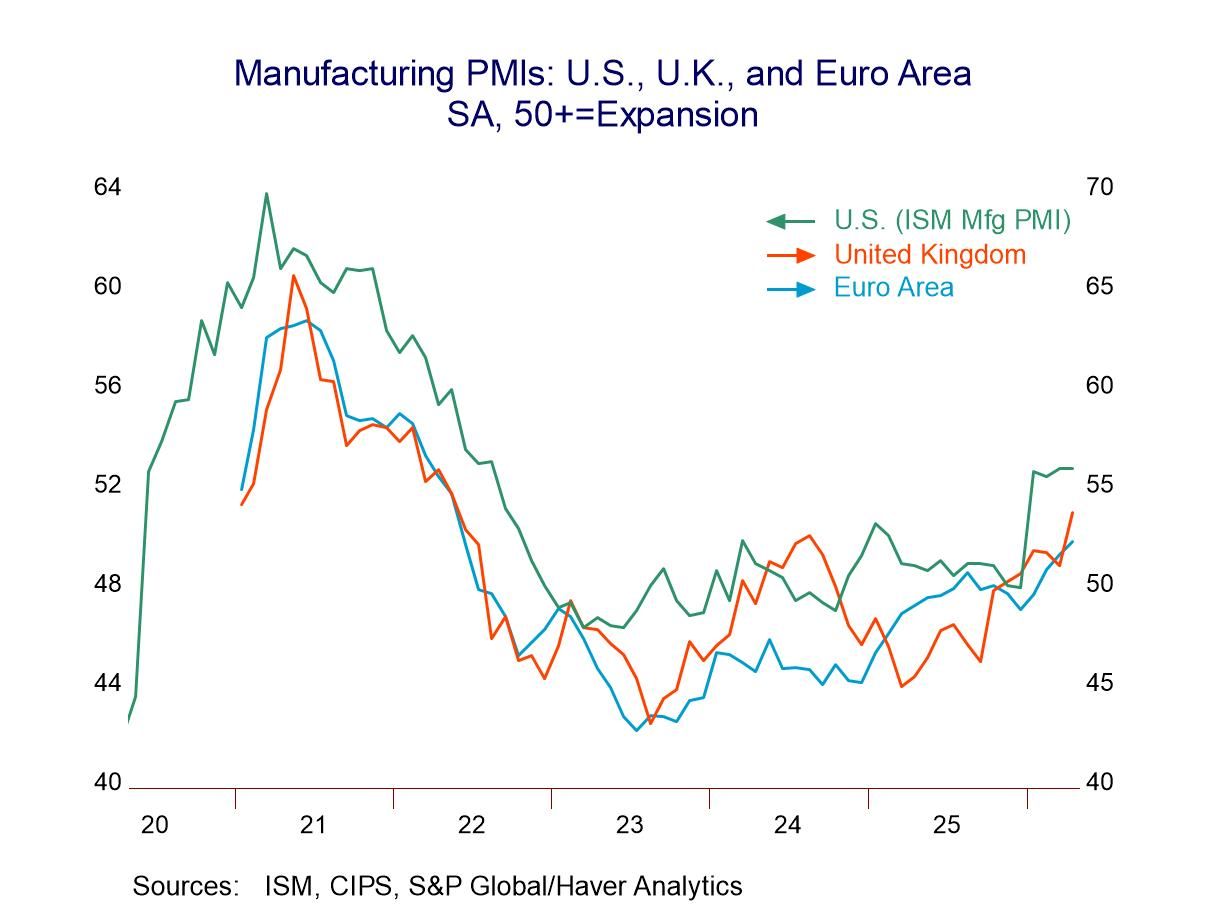

Global| May 04 2026Global MFG PMIs Sweep Higher: Damn the Torpedoes!

You may recognize the excerpted headline quote as ‘borrowing’ from U.S. Admiral David Farragut. It is a famous quote from a U.S. Civil war battle in which he charged ahead in his ship regardless of the risk. This month the global manufacturing PMIs themselves are charging ahead regardless of the rise of inflation, the war in Ukraine, the war in Iran, the closure or impedance in the Strait of Hormuz, and the mucking up of oil and nonoil supply lines. Full speed ahead!

Trend... The chart shows an ongoing recovery in manufacturing. It also shows that conditions are only ‘better’ and not ‘strong.’ Yet when we rank these individual PMIs against their historic results back to January 2022, the median rank across these 18 reporters is 90.8%, signaling that they have been higher less than 10% of the time back to 2022. Of course, 2022-2023 represented low points for manufacturing after COVID. There was a strong recovery from COVID and then the sucker-punch from the invasion of Ukraine by Russia. Nonetheless, on that timeline, recovery is still in progress and—so far—not even the war in the Middle East and other geopolitical turmoil, including a real donnybrook within NATO, has sidetracked it, despite the impact on oil prices. That may not last, but it is the current situation.

A test for central banks With inflation rising, central banks are being put to the test. They failed the post-COVID test and waited too long to hike rates. We did get recovery but inflation, too. Will they do that again? Or will they hike rates sooner? Will they try not to make the same mistake and make, instead, a new mistake by getting too tight too soon? Markets simply do not know. But in the U.S. and U.K., there are five years of missing monetary inflation targets, and in other key countries the inflation targets also have been broadly missed, even if headline inflation recently had dipped into the target range in the last few months or so. Central banks are facing a challenge after their last challenge was not met with success and after a relatively long period—a solid legacy—of missing on the promises they made to the public on inflation.

Solid PMI trends: The sequential, as well as the current, monthly data show how widespread change has been tilted in a positive direction. While conditions are broadly better, the current month’s median reading is only at a PMI value of 52.4. So, manufacturing conditions are only slightly above breakeven (a PMI of 50), but they have been weak for so long that this is an exceptionally strong reading compared to the last four and half years of results.

Some examples: The weak manufacturing readings on the month by ranking are for Turkey, Russia, India, and Indonesia. However, these are own-PMI comparisons, and India is one of the strongest readings in April on a cross-section basis (compared to other countries in April, rather than to its own history) having the third strongest manufacturing reading in April. Malaysia, South Korea, Taiwan, and Japan each have the strongest readings (or nearly so) since January 2022; as a result, Taiwan and Japan also rank one and two among 19 reporter readings in April. South Korea ranks sixth. But Malaysia has been so weak; it still ranks only 11th despite a 99.2% high-low standing.

In Sum: The bottom line is that recovery has not been derailed—yet. But this is only an April report. Given time, this rebound could be untracked. It is only a rebound from the lows. So, the expansion is still at risk, even with global labor markets still tight based on unemployment readings. Economic growth is a slippery slope; the trend is only your friend until it turns on you.

USA| May 01 2026

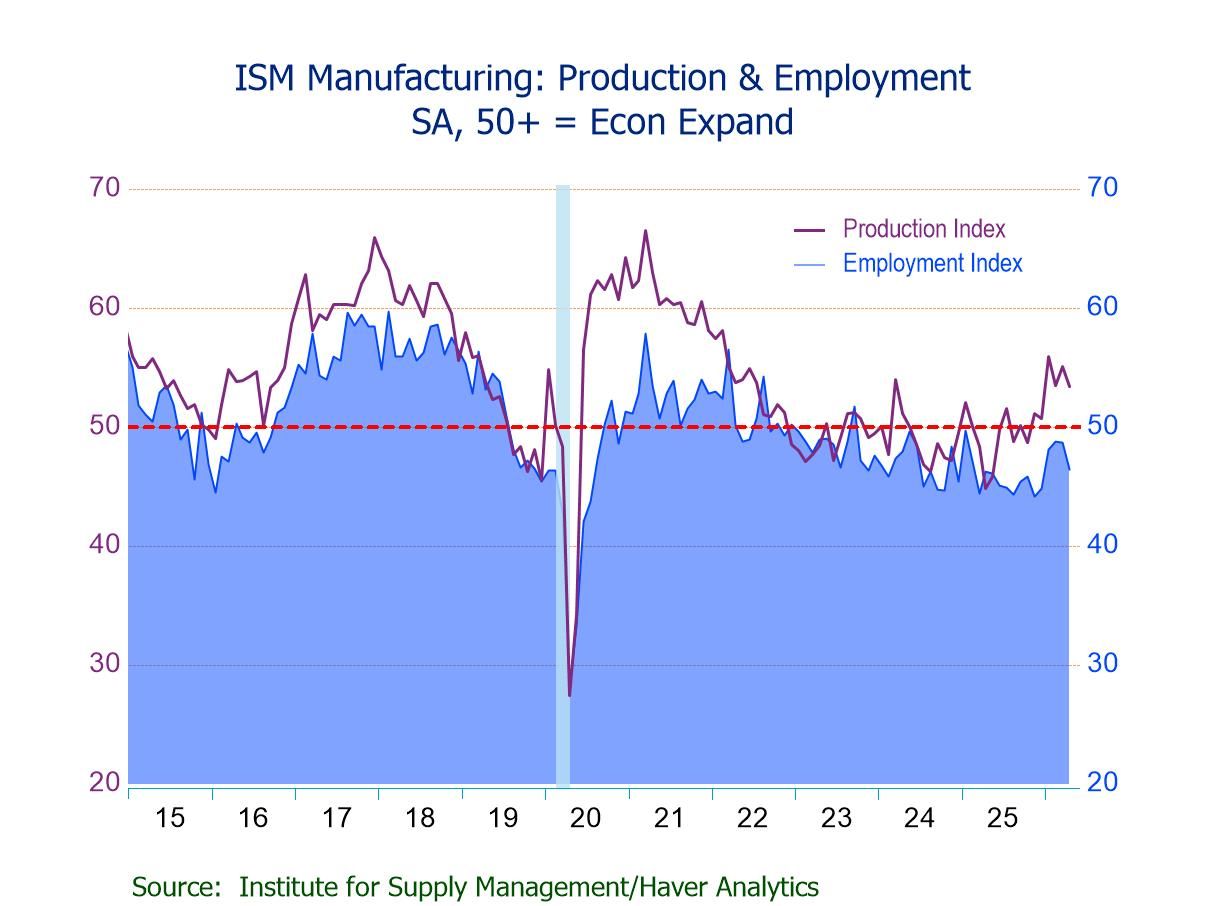

USA| May 01 2026U.S. ISM Manufacturing PMI Steady in April; New Orders and Production Growing; Employment Contracting

- ISM Mfg. PMI at 52.7 in Apr. and Mar.; fourth consecutive month of expansion.

- Production (53.4) expands for the sixth straight mth.; new orders (54.1) for the fourth successive mth.

- Employment (46.4) contracts for the 31st straight mth.; at a four-month low.

- Prices Index (84.6) highest since Apr. ’22; prices rising for the 19th consecutive mth.

- Exports (47.9) contract; imports (50.3) still grow but at a three-month low.

Europe| May 01 2026

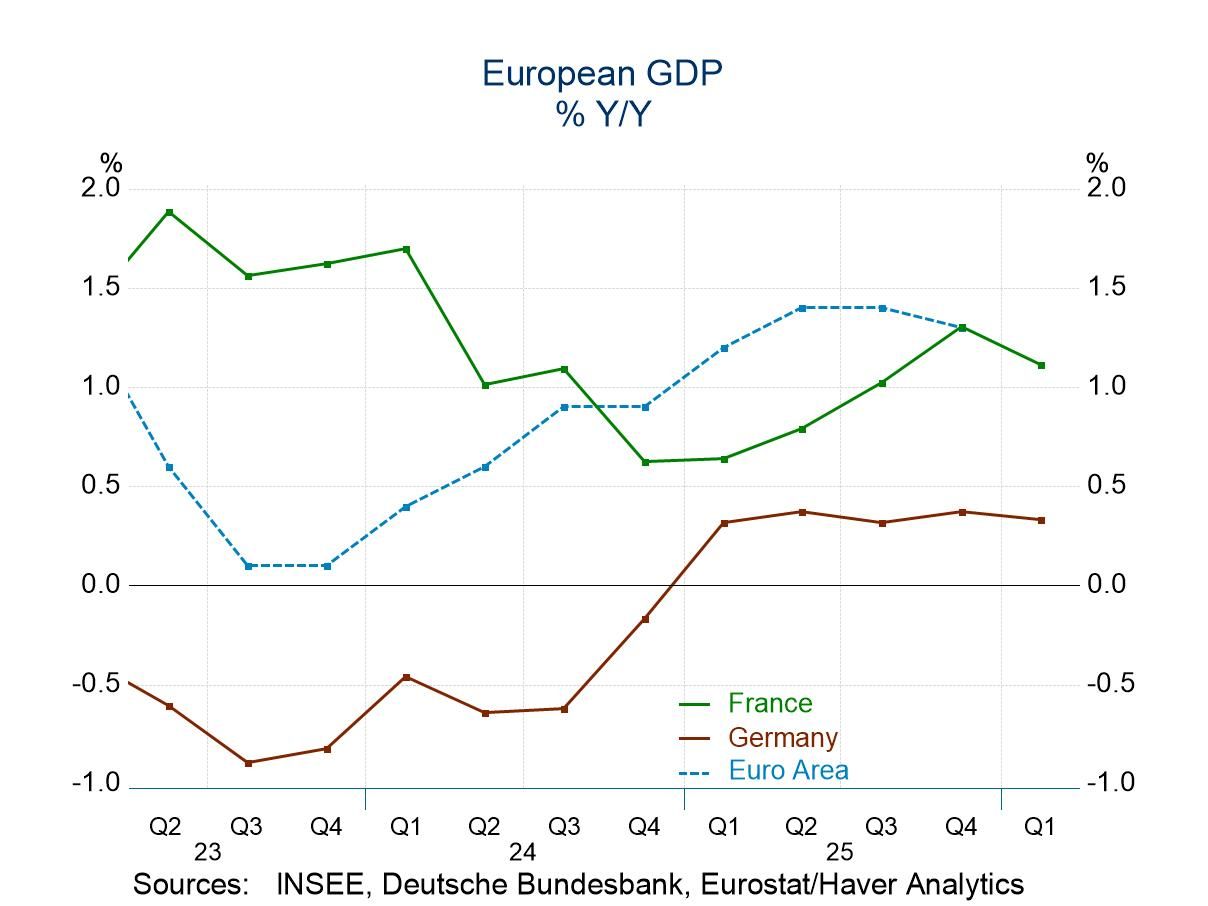

Europe| May 01 2026GDP Remains Weak in EMU

GDP growth in Europe in the first quarter of 2026 continued to be weak. First-quarter annualized growth at 0.6% followed a fourth-quarter annualized growth rate at 0.8%. Year-over-year growth in the monetary union logged a 0.8% annual rate; that represents a slowdown from earlier quarters where the growth rates were generally above 1% and more on the order of 1.5% at an annual rate.

Early GDP reporters in EMU Among the 8 early reporters of GDP in the first quarter, in the table, only three posted growth pickups compared to the previous quarter. Those were Belgium, with a growth rate in the first quarter annualized at 0.8%, up from 0.2% in Q4 2025; Germany, where the growth rate picked up to 1.3% in the first quarter from 1.0% in Q4; and Ireland, with a dubious acceleration of growth to a -7.8% annualized rate, improving from -14.5% annualized in Q4.

Big country, small country The table also looks at growth divided into the four largest economies in the monetary union versus the rest of the monetary union. There we see a growth rate of 1% for the four largest economies, a slowdown from 1.3% in the fourth quarter. For the rest of the monetary union, the growth rate held at 0.5% in the first quarter, the same rate logged in the fourth quarter.

Median growth The median growth rate among these reporters was 0.6%, the same as for the weighted growth rate in the EMU, while the median in the fourth quarter was 1.5% compared to a weighted growth rate for the monetary union at 0.8%.

Ranking the growth rates vs. their own histories The ranking data on the far-right column rank growth in the first quarter on its year-over-year growth pace. On a historic profile, we see only three monetary union reporters with growth in the first quarter at a rate that exceeds median on data back to the 1990s. Those economies are Italy with a 52.2 percentile ranking, Spain with a 53.3 percentile ranking, and Portugal with a 65.2 percentile ranking. For the monetary union as a whole, the growth rate rank is 28.3%, placing it at a ranking between its lower 1/4 and lower 1/3. The median for the monetary union among these early reporting countries is a 32.6 percentile growth rate, and these compared to the United States where the growth rate has a 60.2 percentile standing.

Other data sources report that growth in the services sector has been extremely weak, while there actually has been some resilience in manufacturing. That is somewhat surprising given the Middle East War that affects the world trade and global supply chains. New disruptions because of war in the Middle East are a new fact of life. However, war itself sometimes is a stimulant to some forms of growth. These sector trends will be for us to watch, but for right now growth rates are not impressive and they're certainly not gaining momentum.

- of2725Go to 12 page