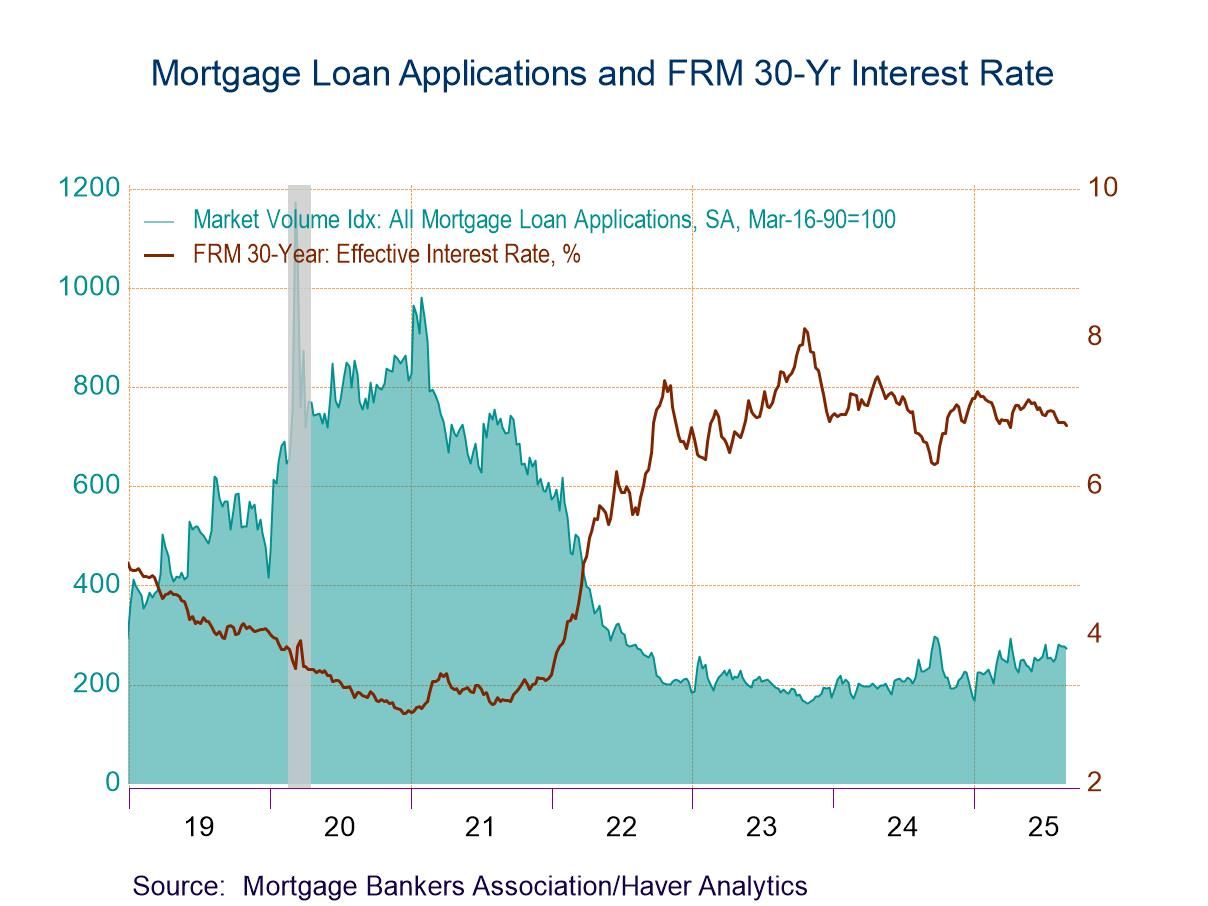

- Purchase applications dropped while loan refinancing edged up.

- Fixed-interest rate on 30-year loan holds at a 4-month low.

- Average loan size edged up.

USA| Sep 03 2025

USA| Sep 03 2025U.S. Mortgage Applications Declined in Latest Week

Global| Sep 03 2025

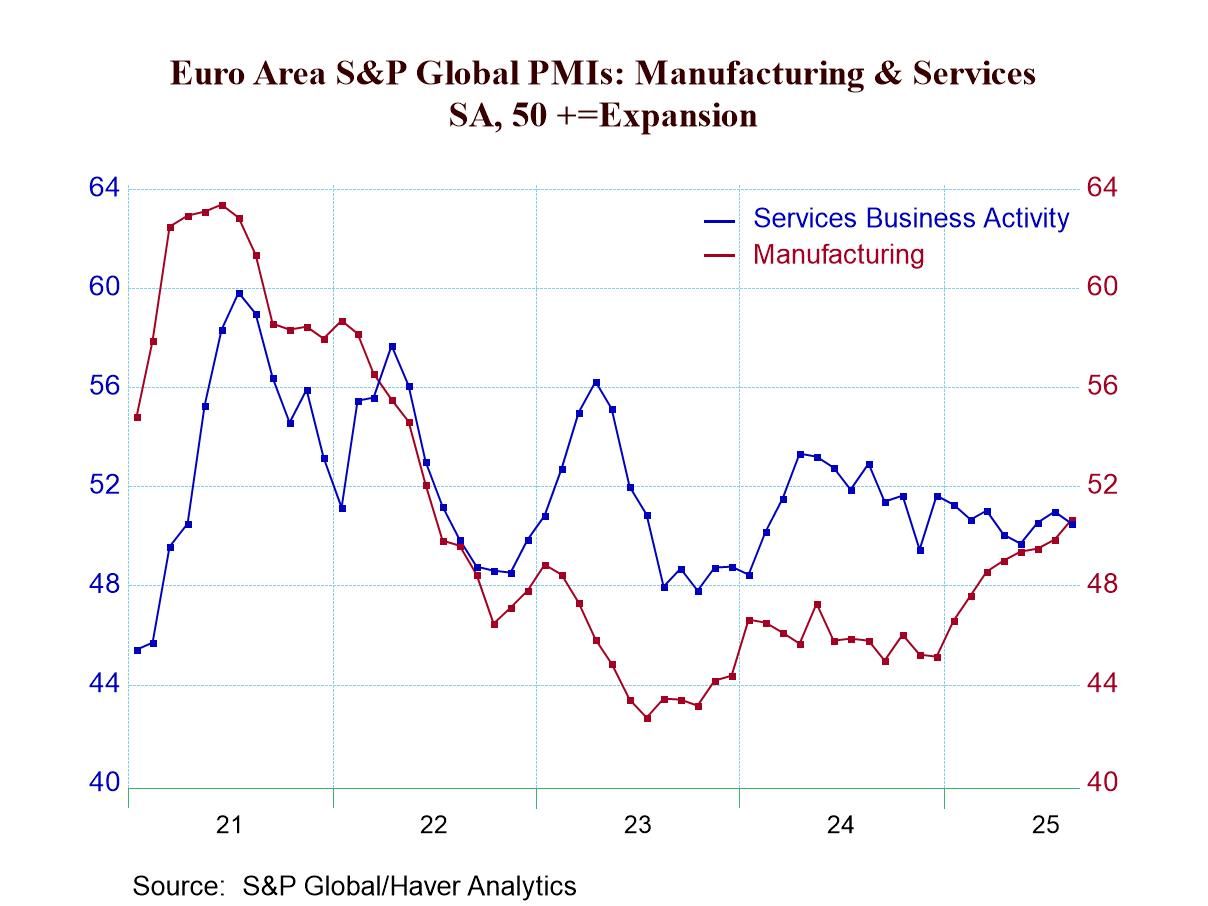

Global| Sep 03 2025S&P Composite PMIs Improve in August

The S&P composite PMIs in August have advanced broadly with only four of 25 reporters showing weaker conditions in August compared to July. In July 13 of these same reporters showed worsening conditions and in June 12 reporters showed worsening conditions. August is a marked turnaround for this survey. One caveat is that the U.S .data in this report continued to use the preliminary services estimate because the final U.S. estimate is not yet available.

Over three months compared to six months, 9 of 25 reporters show worsening conditions. Over six months compared to 12 months, 12 of 25 reporters showed worsening conditions. Over 12 months compared to a year ago, 15 reporters out of 25 showed worsening conditions. There has been a progression in terms of the breadth for reporting countries that are showing improvement in addition the overall average. It has improved slightly from 51.7 over 6 and 12 months to 51.9 over 3 months. The medians have improved from 51.1 over 12 months to 51.5 over 6 months to 51.6 over 3 months, a slightly clearer progression toward better results. Still, both of them are on fairly thin margins of improvement. However, June to August the averages and medians show a little bit more movement and a little more progression to better readings.

The statistic that is perhaps most encouraging is the one about the percentage of reporters that are weaker in August; only 16 were weaker compared to July; in July 52% were weaker compared to June, but in June 48% were weaker compared to May. Looking at the broader progressive period, 39.1% are weaker over 3 months, 52.2% are weaker over 6 months compared to 39.1% weaker over 12 months. The proportion of reporters weakening over these horizons is moderate on the order of 40% to 50%- tending to readings below 50%.

The queue percentile standings show only 8 reporters out of 25 have standings below their median since January 2021.

The chart on top depicts separately the services business activity index for the euro area versus the euro area manufacturing PMI. While the services readings have been relatively stable - perhaps trending slightly to weakness from earlier in the year - manufacturing PMIs have been improving consistently and strongly. At first it was thought that this was manufacturing activity that was ramping up to try to create output to export before U.S. tariffs went into effect, but since the tariff deadline has come and gone, manufacturing has continued to stay strong and to further strengthen. This is an unexpected and impressive trend.

USA| Sep 02 2025

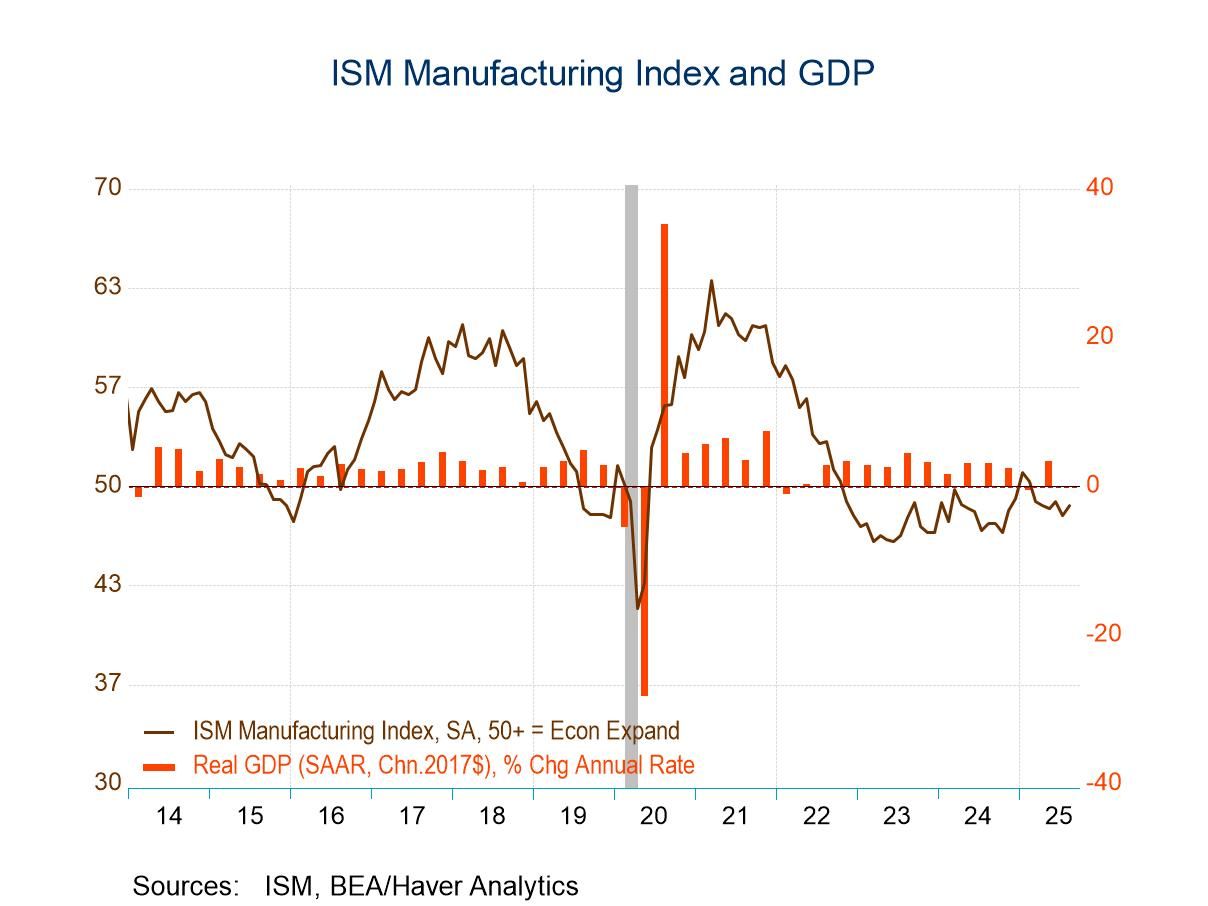

USA| Sep 02 2025U.S. ISM Manufacturing PMI Increases in August; Prices Ease

- Improvement fails to recover all of July decline.

- New orders gain offsets production decline.

- Price index falls to six-month low.

by:Tom Moeller

|in:Economy in Brief

USA| Sep 02 2025

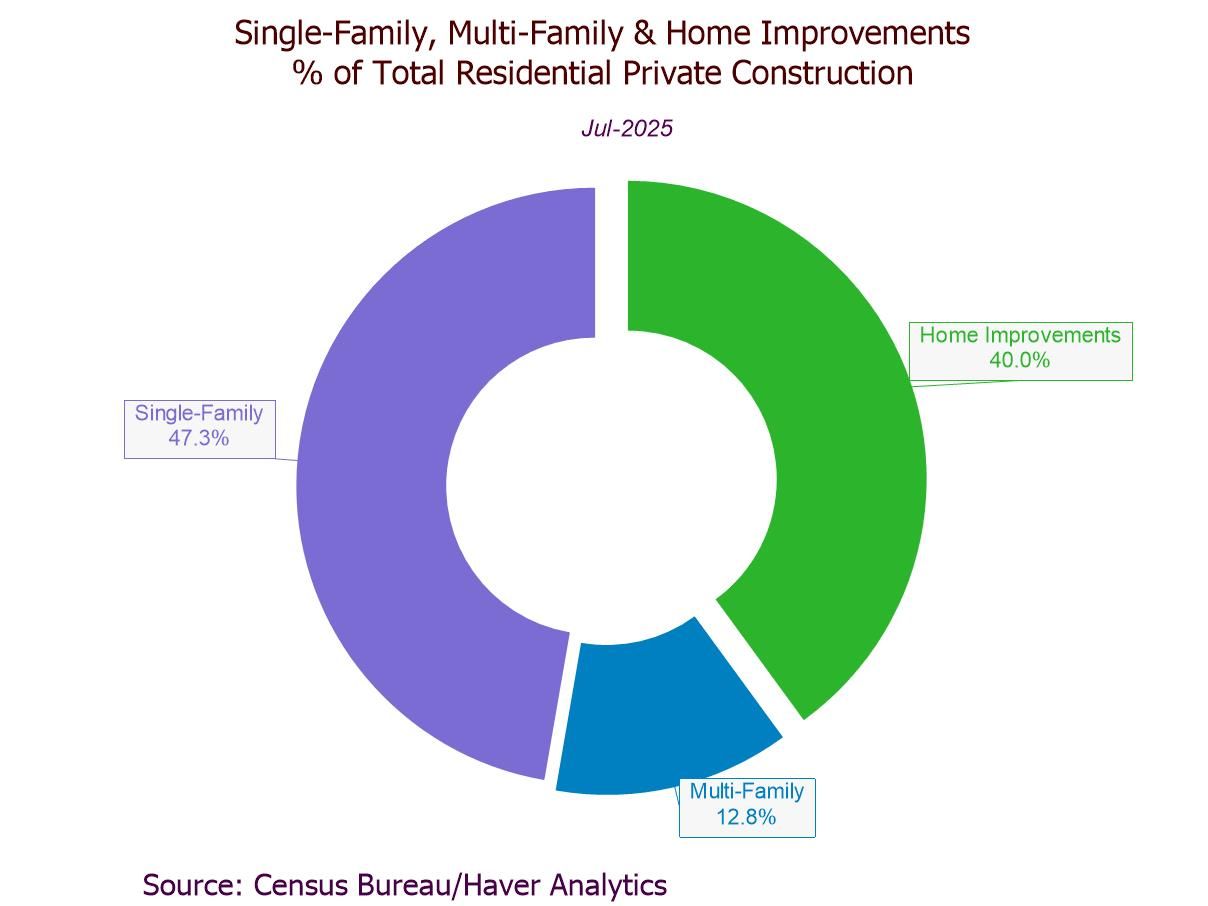

USA| Sep 02 2025U.S. Construction Spending Eases in July

- Headline: -0.1% m/m, the third straight m/m fall; -2.8% y/y, the sixth straight y/y slide.

- Residential private construction +0.1% m/m, up for the first time since December.

- Nonresidential private construction -0.5% m/m, the third consecutive m/m decline.

- Public sector construction +0.3% m/m, led by a 1.8% rebound in residential public building.

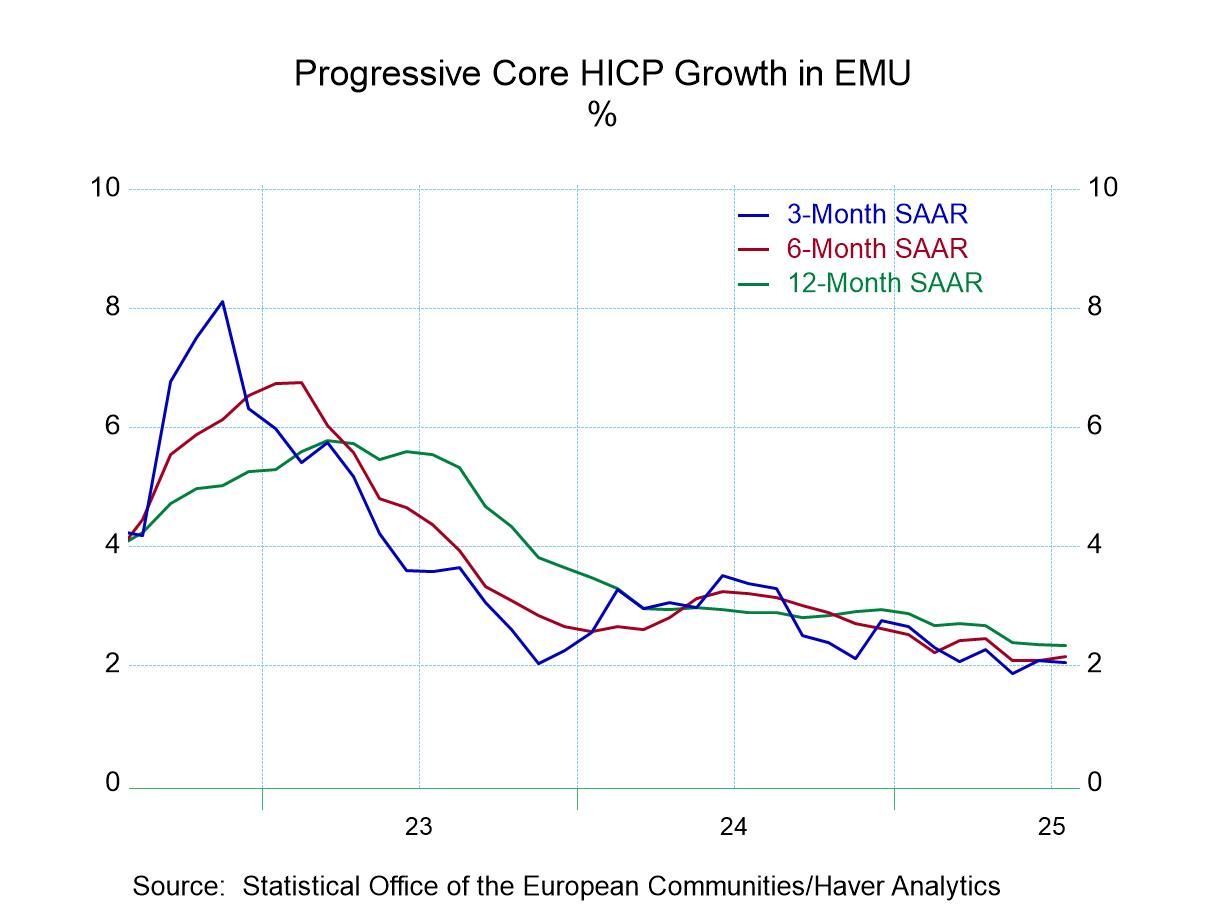

Global| Sep 02 2025

Global| Sep 02 2025Inflation in Europe Shows Mild Pressure

Inflation in August was well behaved; the headline series with the monetary union posted a gain of 0.2% after 0.3% gains in each of the previous months. Still those increases mean that the three-month inflation rate is at 3% compared to 2.1% over 12 months. Stop headline inflation has grown moderately hot in the monetary union.

Across countries the largest EMU members has so well-behaved inflation in August, with Germany up 0.2%, France up 0.1%, and Italy and Spain both unchanged. However, inflation in the previous two months was a bit stronger leaving three-month inflation rates for France, Italy, and Spain over 2%. Over six months only Italy is over 2% and that's barely, and over 12 months only Spain is substantially above the 2% mark.

Core inflation in the monetary union is where the elusiveness and stubbornness is for the three large economies that report core inflation. Germany actually reports ex-energy inflation. Italy and Spain report core inflation. They're all showing increases of 0.3 and 0.2 over the last two months. Over three months German ex-energy inflation is running at a 2.4% annual rate with Italy's core at 2.7% and Spain's core at 3.8%. Over 12 months German ex-energy inflation is up at a 2.6% annual rate, compared to a 2.4% annual rate for Spain’s core and Italy’s core that that is nearly on the money at a 2.1% annual rate.

The 12-monht inflation rate is marginally worse for headline and core rates across this group of countries in August compared to July. For the EMU, the headline is the same at 2.1%. Even though shorter measures show some pressure building, 12-month inflation is marginally lower in August 2025 than in August 2024 for headline and core measures in the large countries.

However, there has been no sense of controlled inflation recently as all averages are clearly excessive with the average five-year reading at a low of 3% for core inflation in Italy to a five-year average high of 4.5% in Germany. This legacy for inflation is still a problem for some although central bankers around the world are trying to dismiss it as a past event; however, no one's quite sure whether inflation is really over the hump and going back to normal for good.

Asia| Sep 01 2025

Asia| Sep 01 2025Economic Letter from Asia: A Friend in Need

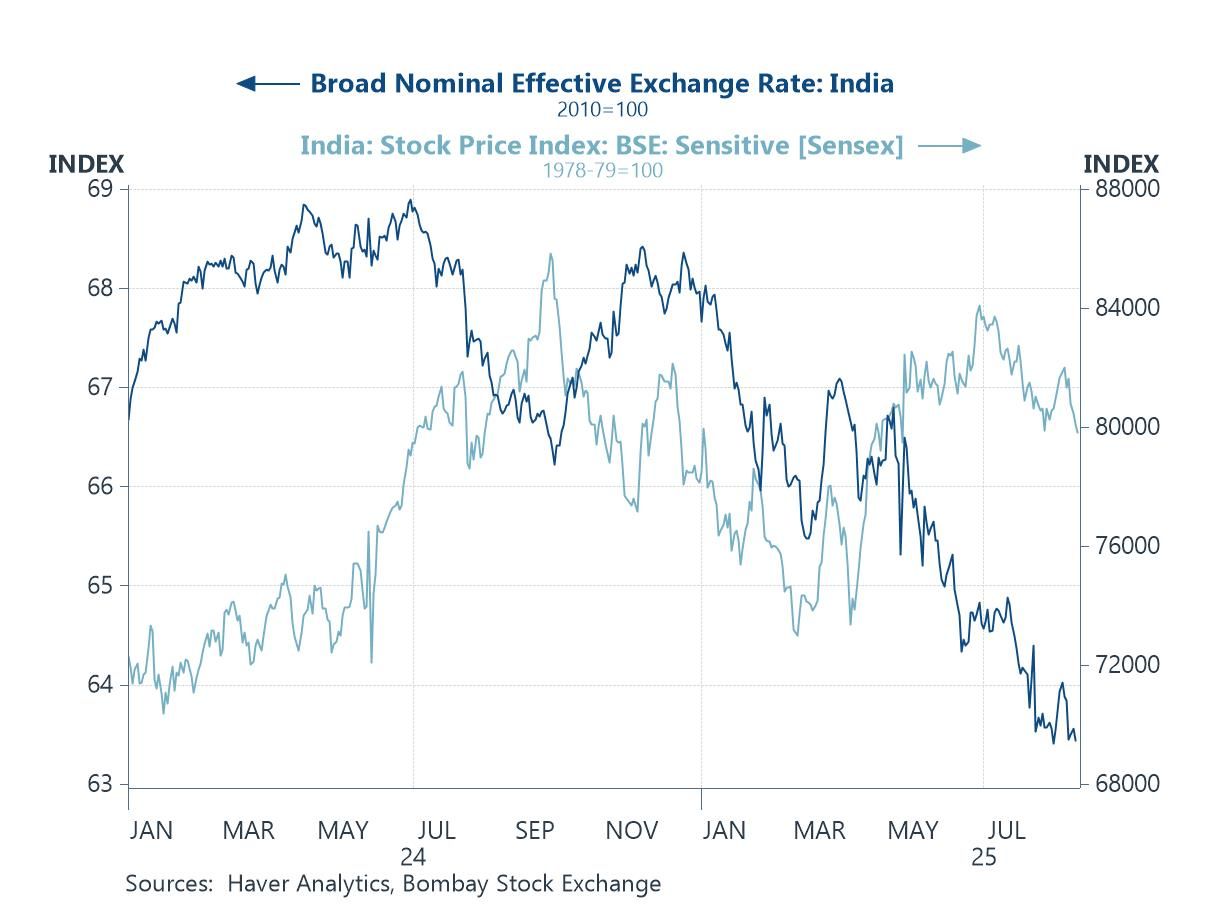

This week, we dive deeper into developments concerning India and China, while noting the recently improving relationship between the world’s two most populous countries. In India, market sentiment understandably soured (chart 1) after US President Trump followed through on earlier threats to raise additional tariffs to 50%, in response to its purchases of Russian oil. While these tariffs would render much of its exports to the US uncompetitive, a small source of interim relief comes from current exemptions, such as for pharmaceuticals and electronics, India’s major export categories to the US (chart 2).

Turning to China, overcapacity remains a concern for many of its major Western trading partners. Persistently rising export volumes amid falling export prices can signal overcapacity, though they are not definitive evidence. Nonetheless, indications of overcapacity — for example, in China’s transportation exports (chart 3) — continue to raise concerns. Europe has responded with significant tariffs on Chinese EVs, but Chinese producers have offset these by onshoring production in Europe or switching to hybrid vehicles, while continuing to expand export volumes despite declining prices (chart 4).

Amid rising US trade pressure, China and India have drawn closer as partners of circumstance despite their often-thorny history. Prime Minister Modi’s attendance at China’s Shanghai Cooperation Organization (SCO) summit, starting Sunday — his first visit to China in seven years — is a strong signal of improving ties. While this engagement may help foster trade and investment between the two countries, underlying challenges remain. India’s substantial trade deficit with China (chart 5) could worsen if imports increase, and mutual direct investment — which has been subdued in recent years, perhaps due to previously frosty relations — may require further policy support to rebound (chart 6).

India President Trump followed through on his earlier threats by imposing an additional 25% tariff on India, raising the total additional tariff rate to 50% as of last week and in response to India’s purchases of Russian oil. Indian markets reacted sharply, with equities falling and the rupee weakening, as shown in chart 1. Given the scale of the new tariffs — which render much of India’s exports to the US uncompetitive — calls for government and monetary policy support have intensified. Authorities are already bracing for the immediate impact, including first-round effects such as rushed efforts to re-route trade, seek alternative markets, and limit losses through layoffs. On the fiscal side, Prime Minister Modi announced consumption tax cuts last week to cushion the blow, and the crisis may also present an opportunity to finally reform India’s notoriously complex tax system.

- of10Go to 10 page