Asia| Sep 01 2025

Asia| Sep 01 2025Economic Letter from Asia: A Friend in Need

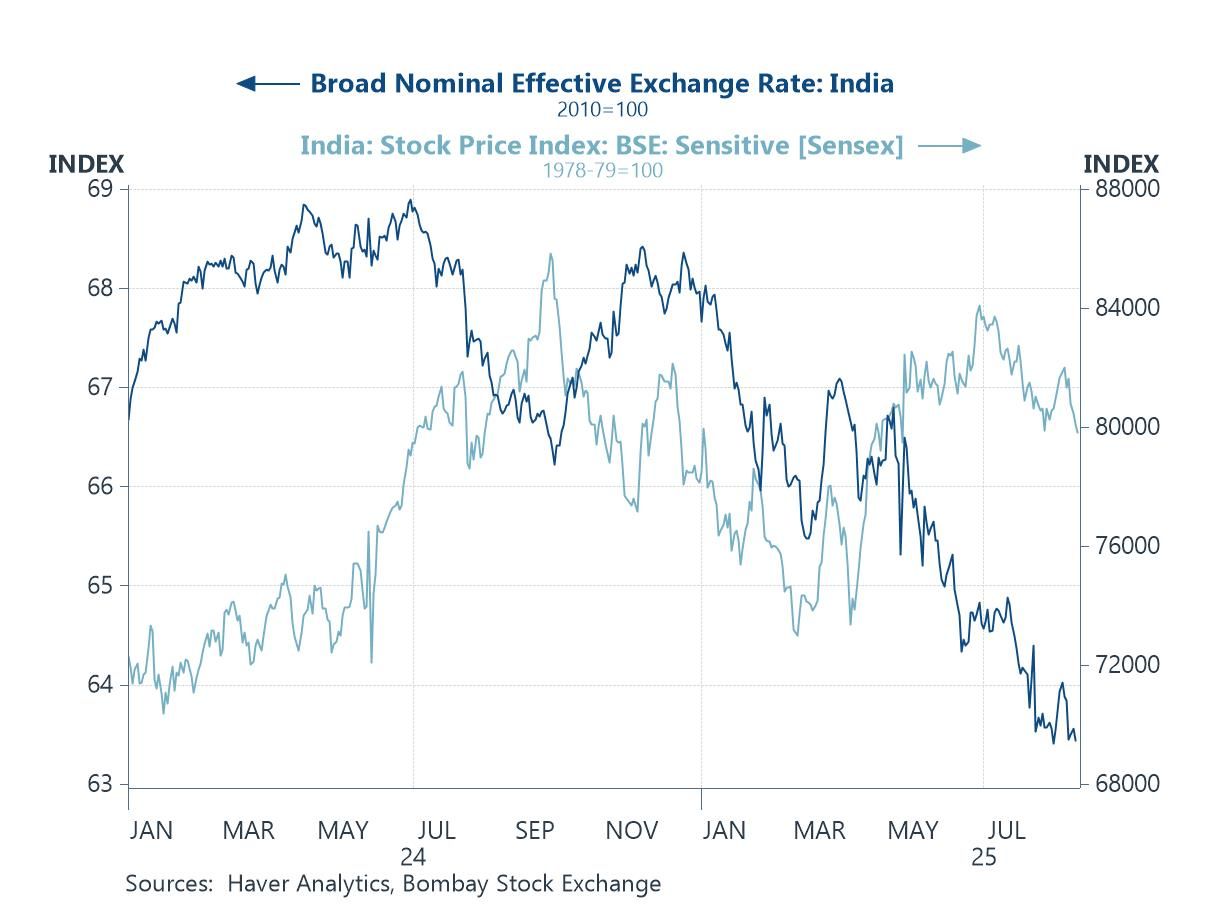

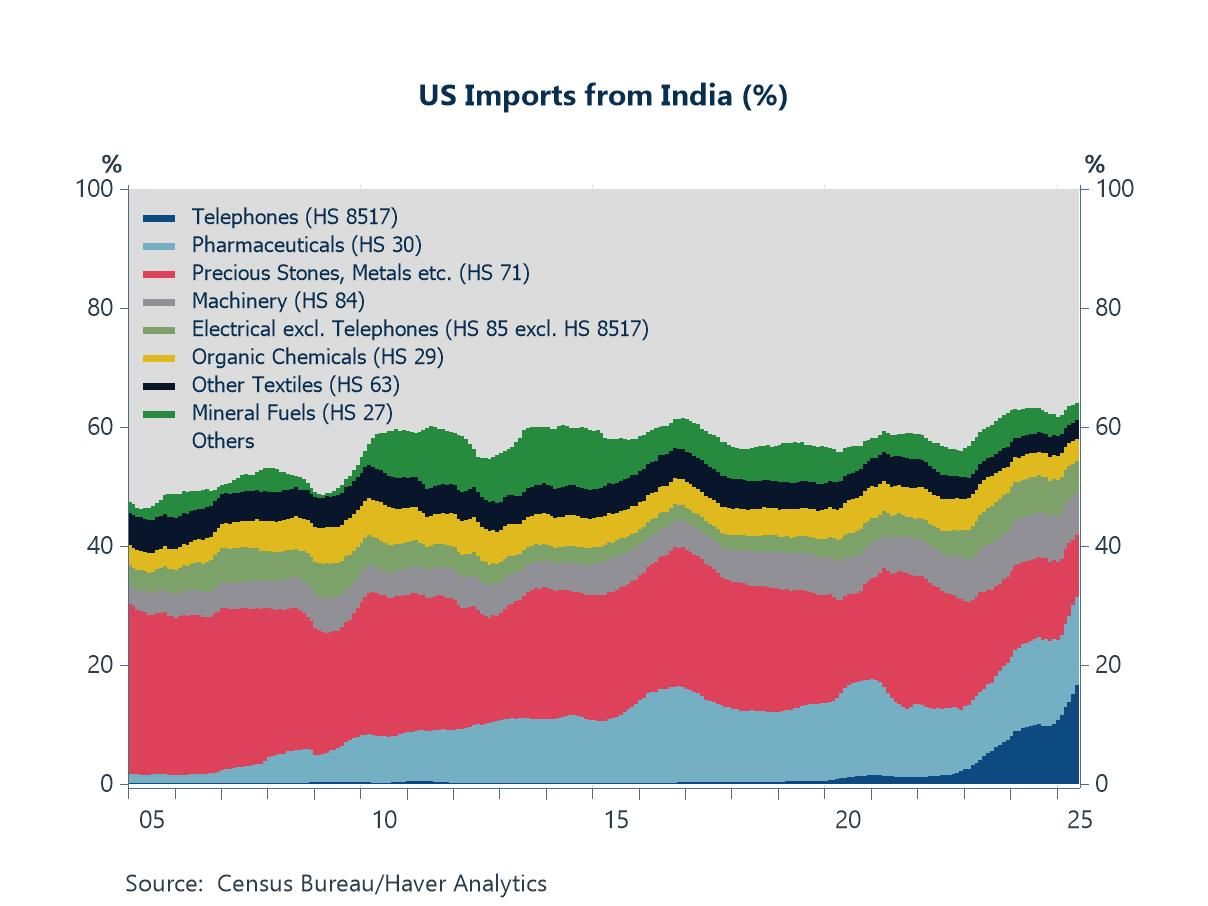

This week, we dive deeper into developments concerning India and China, while noting the recently improving relationship between the world’s two most populous countries. In India, market sentiment understandably soured (chart 1) after US President Trump followed through on earlier threats to raise additional tariffs to 50%, in response to its purchases of Russian oil. While these tariffs would render much of its exports to the US uncompetitive, a small source of interim relief comes from current exemptions, such as for pharmaceuticals and electronics, India’s major export categories to the US (chart 2).

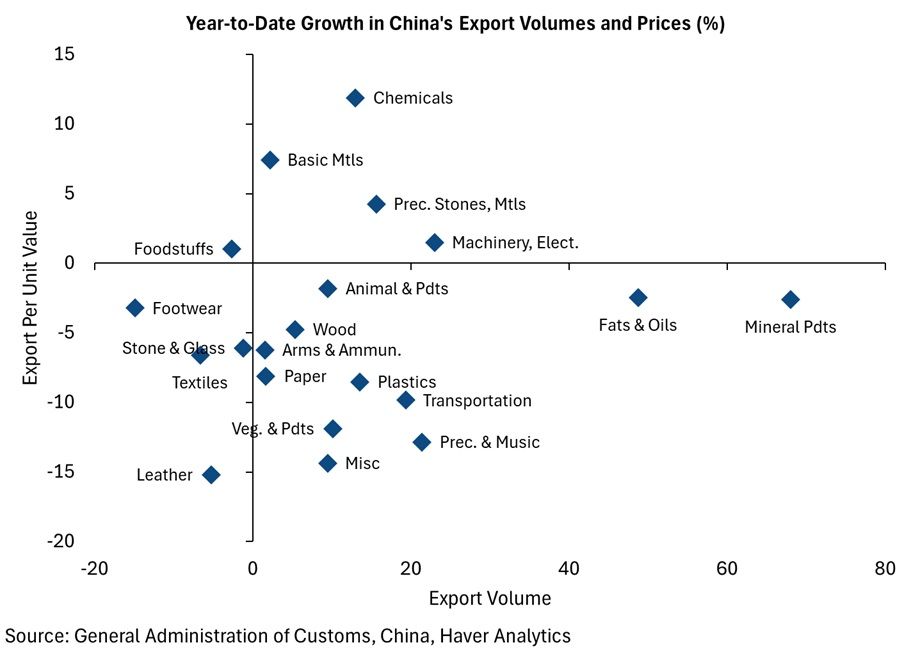

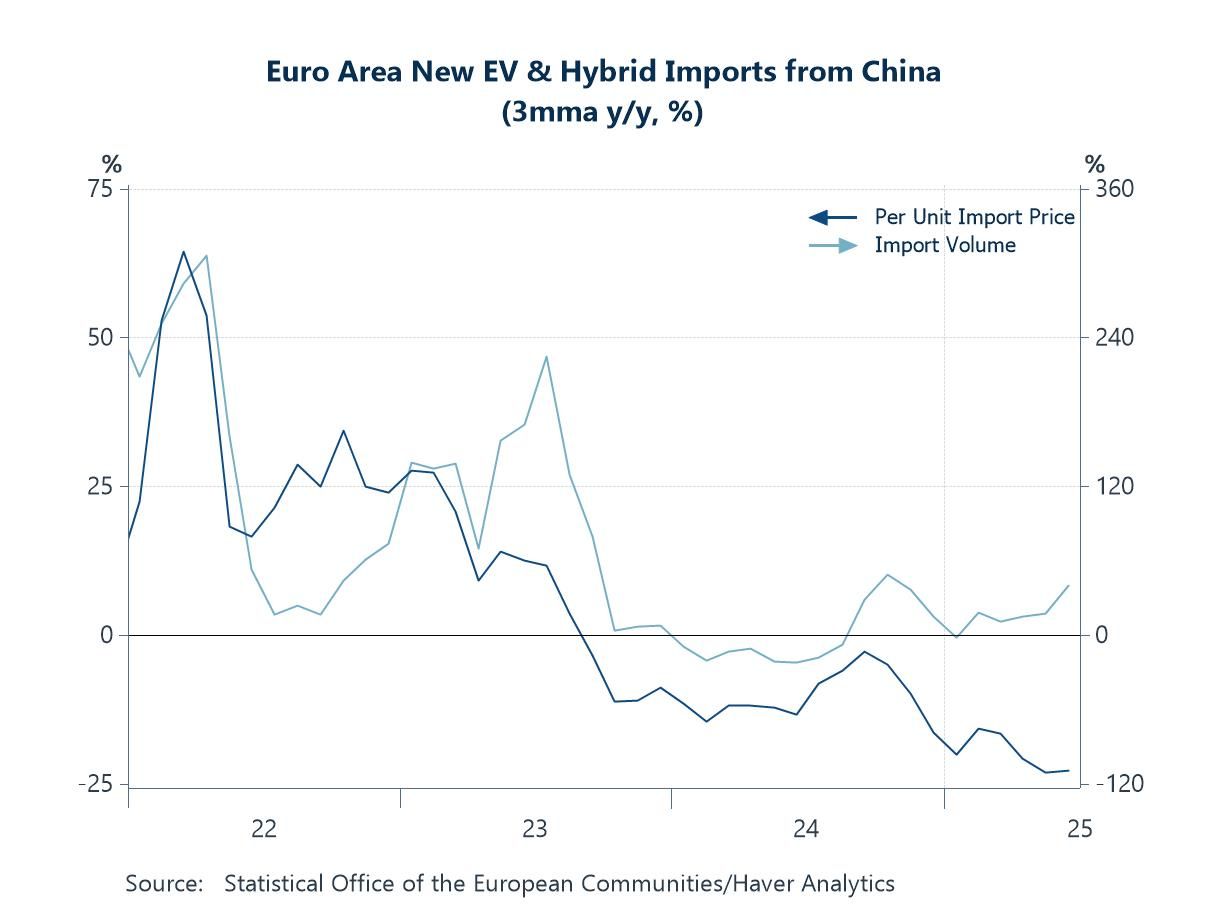

Turning to China, overcapacity remains a concern for many of its major Western trading partners. Persistently rising export volumes amid falling export prices can signal overcapacity, though they are not definitive evidence. Nonetheless, indications of overcapacity — for example, in China’s transportation exports (chart 3) — continue to raise concerns. Europe has responded with significant tariffs on Chinese EVs, but Chinese producers have offset these by onshoring production in Europe or switching to hybrid vehicles, while continuing to expand export volumes despite declining prices (chart 4).

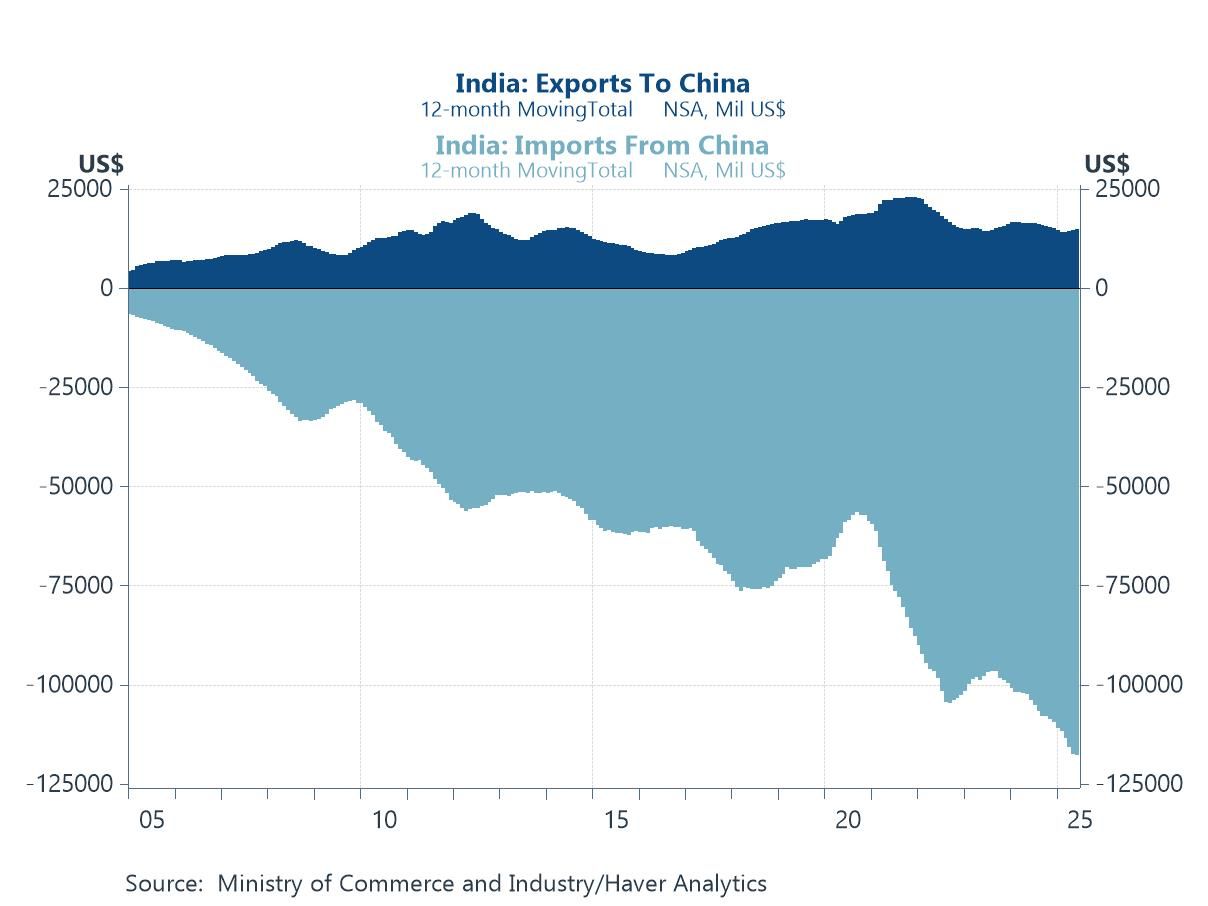

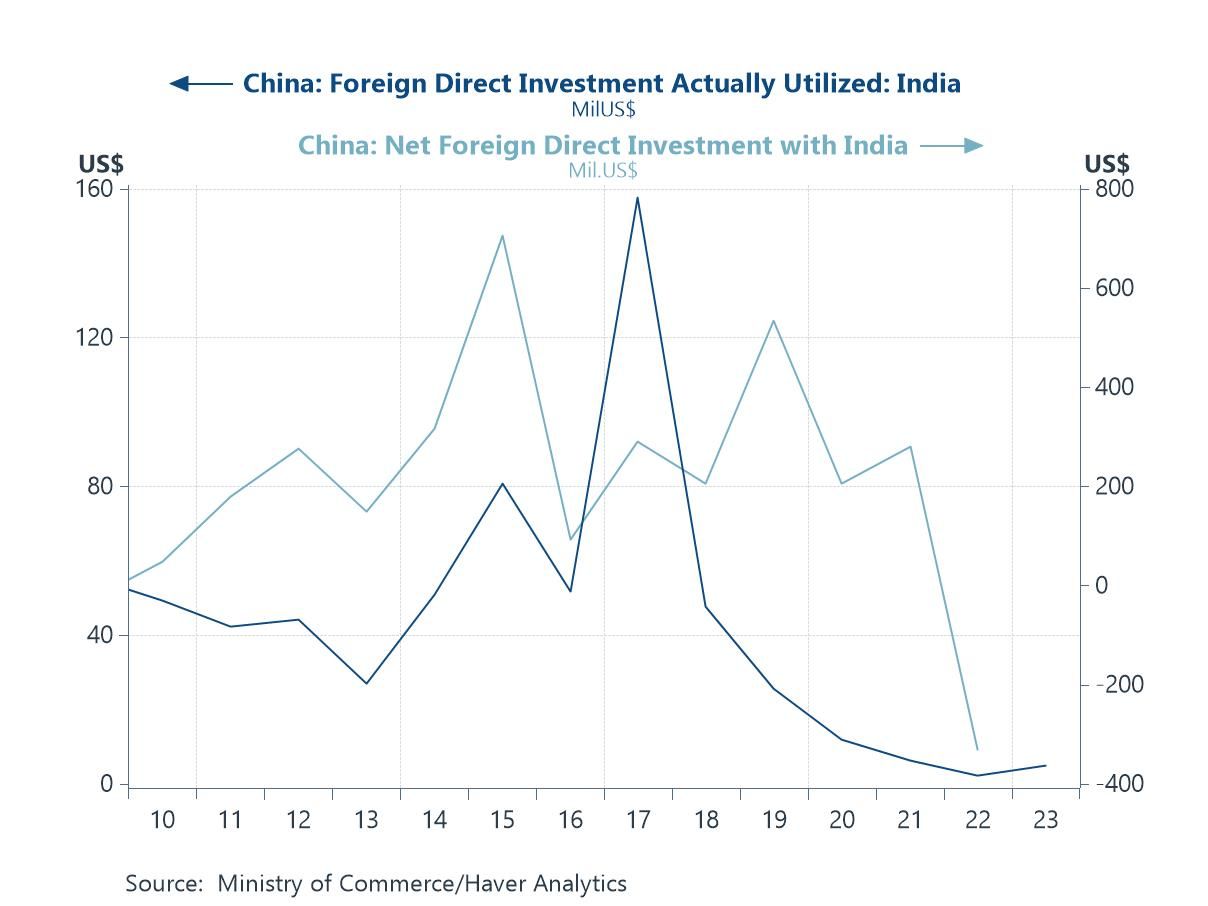

Amid rising US trade pressure, China and India have drawn closer as partners of circumstance despite their often-thorny history. Prime Minister Modi’s attendance at China’s Shanghai Cooperation Organization (SCO) summit, starting Sunday — his first visit to China in seven years — is a strong signal of improving ties. While this engagement may help foster trade and investment between the two countries, underlying challenges remain. India’s substantial trade deficit with China (chart 5) could worsen if imports increase, and mutual direct investment — which has been subdued in recent years, perhaps due to previously frosty relations — may require further policy support to rebound (chart 6).

India President Trump followed through on his earlier threats by imposing an additional 25% tariff on India, raising the total additional tariff rate to 50% as of last week and in response to India’s purchases of Russian oil. Indian markets reacted sharply, with equities falling and the rupee weakening, as shown in chart 1. Given the scale of the new tariffs — which render much of India’s exports to the US uncompetitive — calls for government and monetary policy support have intensified. Authorities are already bracing for the immediate impact, including first-round effects such as rushed efforts to re-route trade, seek alternative markets, and limit losses through layoffs. On the fiscal side, Prime Minister Modi announced consumption tax cuts last week to cushion the blow, and the crisis may also present an opportunity to finally reform India’s notoriously complex tax system.

Chart 1: Indian equities and the rupee

Given India’s heavy reliance on the US for export revenue — and with US importers already pressuring Indian producers to cut prices — profits on both sides are likely to suffer under the newly imposed tariffs. As a partial reprieve, the US has temporarily exempted pharmaceuticals and electronics, two of India’s major export categories, as shown in chart 2. Moreover, significant front-loading of shipments ahead of the tariff hike may temporarily buoy trade data and near-term growth, though India’s longer-term prospects now face renewed headwinds.

Chart 2: US imports from India

China Moving on to China, the economy remains under scrutiny for signs of industrial overcapacity, a concern raised by several Western trading partners. While not conclusive on their own, some common hallmarks of industrial overcapacity include persistently falling prices — often driven by price wars — and a turn to higher exports as producers offload surplus output when domestic demand cannot absorb it. In this context, chart 3 compares year-to-date changes in both export volumes and unit values across major goods categories, offering suggestive — though not definitive — evidence of overcapacity. Notably, sectors such as transportation stand out, which we examine in greater detail in the next section.

Chart 3: Growth in China’s export volumes and prices

Focusing on a more concrete case of China’s overcapacity, electric-vehicle (EV) exports to Europe remain a key flashpoint. Export volumes continue to climb even as unit prices fall year-on-year (chart 4), suggesting that overcapacity persists, with low-cost Chinese EVs pressuring European automakers. This surge has continued despite EU tariffs of up to 45% on battery EVs. Chinese carmakers have offset the impact by promoting plug-in hybrids and onshoring production in Europe to sidestep duties and defend market share. Beijing, however, is not standing idle. Measures to rein in excess capacity and curb destructive price competition — or “break involution” — are underway. These include crackdowns on price wars across multiple sectors and even a dedicated fund to acquire and shutter roughly one-third of China’s loss-making polysilicon industry. Early signs of traction appear in China’s latest industrial profits data, where year-on-year declines narrowed to 1.7% in July as cut-throat pricing eased.

Chart 4: Euro area new EV & hybrid imports from China

China & India relations China and India, facing rising trade pressure from the US, have drawn closer together as partners of circumstance despite their often-thorny history. A clear sign of warming ties was Prime Minister Modi’s attendance at the Shanghai Cooperation Organization (SCO) summit, which began on Sunday in Tianjin — his first visit to China in seven years after skipping last year’s meeting in Kazakhstan. Following talks at the summit, President Xi and Prime Minister Modi affirmed that China and India are partners rather than rivals, pledging to improve trade ties while easing tensions over their Himalayan border dispute. Modi also announced that direct India-China flights will resume after a five-year suspension. Even so, it remains uncertain how much India can expand imports from China without worsening its already sizable trade deficit, as shown in chart 5.

Chart 5: India’s trade with China

The Xi-Modi meeting also raised prospects for renewed investment flows between the two countries. In recent years, mutual direct investment has slowed sharply, likely reflecting strained relations and caution. Stronger political engagement — including Foreign Minister Wang Yi’s earlier visit to India, a precursor to the summit — could help reverse this trend. As shown in chart 6, cross-border investment remains subdued. However, improving ties could pave the way for new projects, joint ventures, and deeper economic integration, potentially unlocking the combined economic potential of both countries given their large populations and other significant factors.

Chart 6: China-India direct investment

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief