Global| Dec 11 2025

Global| Dec 11 2025Charts of the Week: The Downside Risks

by:Andrew Cates

|in:Economy in Brief

Summary

As 2025 draws to a close, the global economy enters 2026 with a surprisingly resilient backdrop: equity markets are still trading near cycle highs, volatility is subdued, and consensus forecasts have been drifting upward in recent months—helped by a robust US economy, firmer momentum across Asia, and optimism that AI-related investment will continue to lift the medium-term outlook (chart 1). Against this relatively constructive starting point, we focus this week on the key downside risks that could challenge the consensus narrative next year: the possibility of monetary-policy miscalibration (chart 2); the gap between elevated policy uncertainty and unusually calm financial markets (chart 3); the risk that financial markets may be overestimating the gains from AI (chart 4); renewed strain in global trade (chart 5); and geopolitical tensions (chart 6). These risks do not dominate the baseline outlook, but they help frame the vulnerabilities that could matter if global conditions deteriorate. Next week, we will turn to the upside risks—the forces that could allow the world economy to outperform again in 2026.

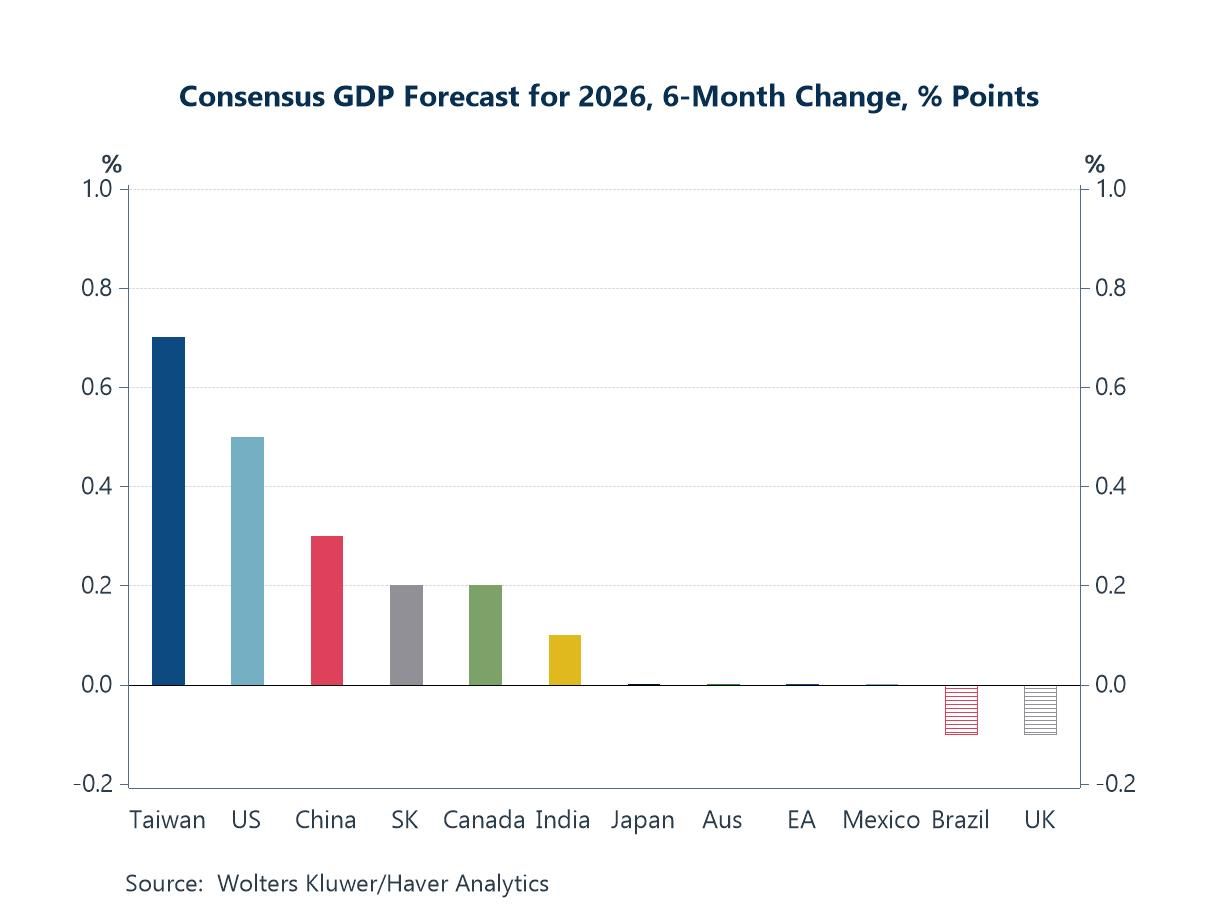

The Blue Chip Consensus Before turning to the risks that could unsettle the global outlook in 2026, it’s worth noting the backdrop against which those risks are emerging. The first chart shows that forecasters have, if anything, become more optimistic in recent months, raising their 2026 GDP projections across many major economies. The upgrades are most visible in Asia’s tech-focused economies, where the semiconductor and AI upturn is lifting expectations, but the US has also benefited from stronger-than-expected momentum and fading concerns that tariffs would deliver a major growth hit. In short, the starting point for the global outlook has improved—making the downside scenarios explored in the next few charts all the more important to test.

Chart 1: 6-month changes in the Blue Chip Growth Consensus for 2026

Policy divergence The second chart highlights one of the central risks to the 2026 outlook: monetary-policy calibration. Even as growth expectations have firmed, forecasters remain convinced that the major central banks still have a little further to go in their easing cycles. For both the Fed and the Bank of England, respondents expect additional rate cuts in early 2026, albeit with growing uncertainty about the exact timing and pace. The broader message is that the heavy lifting on disinflation is now largely done, and what remains are finer calibration risks—where cutting too slowly risks choking momentum, while cutting too aggressively risks undoing progress on inflation. The ECB outlook is far more fragmented. A large share of forecasters sees the next step as a cut—though not necessarily soon—but a meaningful minority lean toward a possible hike. At the opposite pole is the Bank of Japan. Unlike its peers, the BoJ is still expected to tighten policy, reflecting Japan’s firmer growth foundation and a more durable inflation process. This creates a notable US–Japan policy divergence, which has already influenced currency and bond-market behaviour and could become a larger global shock-transmission channel in 2026.

Chart 2: Blue Chip Consensus : The timing of a next policy rate move in the US, Japan and Europe

Source: Wolters Kluwer/Haver Analytics

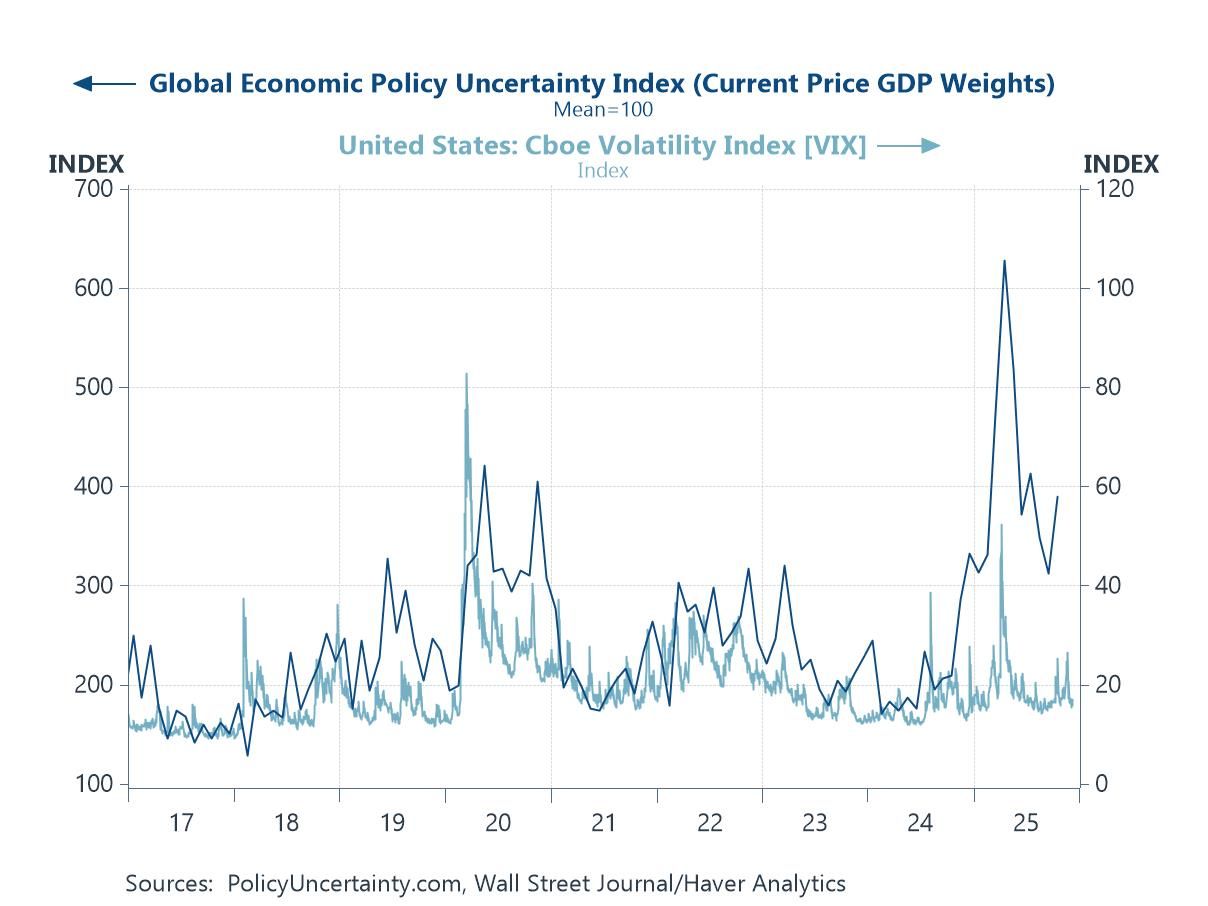

Financial market stress The third chart highlights another source of downside risk: the widening gap between financial-market calm and real-economy anxiety. The US VIX has spent most of the past year hovering near multi-decade lows, consistent with rich valuations, abundant liquidity and a broadly optimistic macro narrative. Yet measured global economic policy uncertainty remains unusually elevated, reflecting geopolitical fragmentation, shifting trade regimes, and highly uncertain fiscal trajectories. This disconnect matters. Periods in which markets price near-perfection while the policy environment deteriorates have often been precursors to sharp repricing episodes. With valuations stretched and volatility compressed, it would not take much—a policy misstep, a geopolitical shock, or a rapid shift in rate expectations—to trigger a correction big enough to destabilise confidence in 2026.

Chart 3: Global policy uncertainty versus the US VIX index

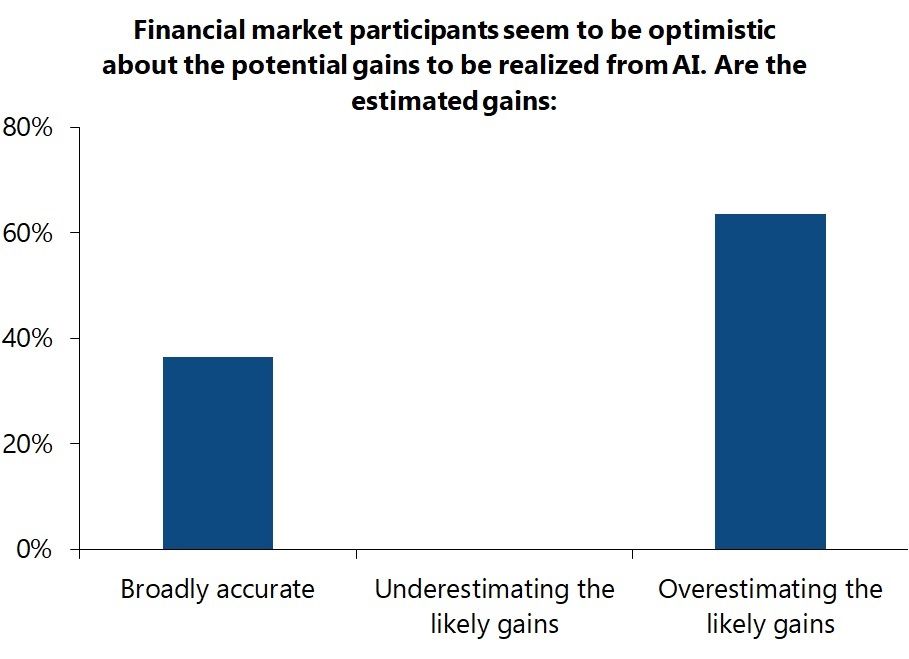

AI expectations Against that backdrop, our next chart highlights a more subtle but no less important vulnerability: expectations around AI-driven growth. While AI has undoubtedly been a powerful tailwind for market sentiment—and arguably a key reason why forecasters have nudged up 2026 growth projections—our survey suggests that most respondents believe financial markets are overestimating the likely economic gains. Only around a third think current expectations are broadly accurate; almost nobody believes markets are underestimating AI’s impact. This imbalance matters. When valuations are rich and optimism is heavily front-loaded, any disappointment in AI adoption, productivity gains or investment payoffs could unwind a meaningful chunk of the recent market strength. In other words, the same force lifting the outlook today could become a meaningful downside catalyst in 2026 if reality fails to keep pace with expectation.

Chart 4: Blue Chip Survey: The estimated gains from AI versus financial market expectations

Source: Wolters Kluwer/Haver Analytics

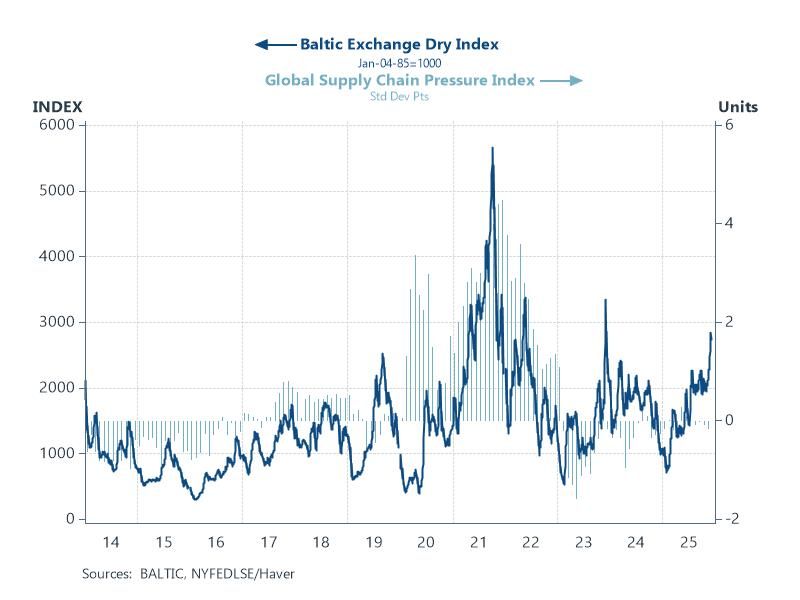

Trade disruption A further downside risk comes from the latent fragilities in global trade and logistics. The Baltic Dry Index has climbed sharply in recent months, hinting at firmer shipping demand and rising transport costs, even as the Global Supply Chain Pressure Index has edged lower. That combination is telling: headline congestion may not yet be building, but underlying pressures—tight vessel availability, shifting trade routes, selective port bottlenecks and stronger goods flows—are quietly re-accumulating beneath the surface. None of this resembles the acute disruptions of 2021–22, but the risk is that a seemingly contained system can tighten very quickly. For a global economy that remains vulnerable to cost shocks and production delays, any renewed squeeze in trade logistics would add another meaningful downside risk as we look toward 2026.

Chart 5: The Baltic Dry Index versus the FRBNY’s Global Supply Chain Pressure Index

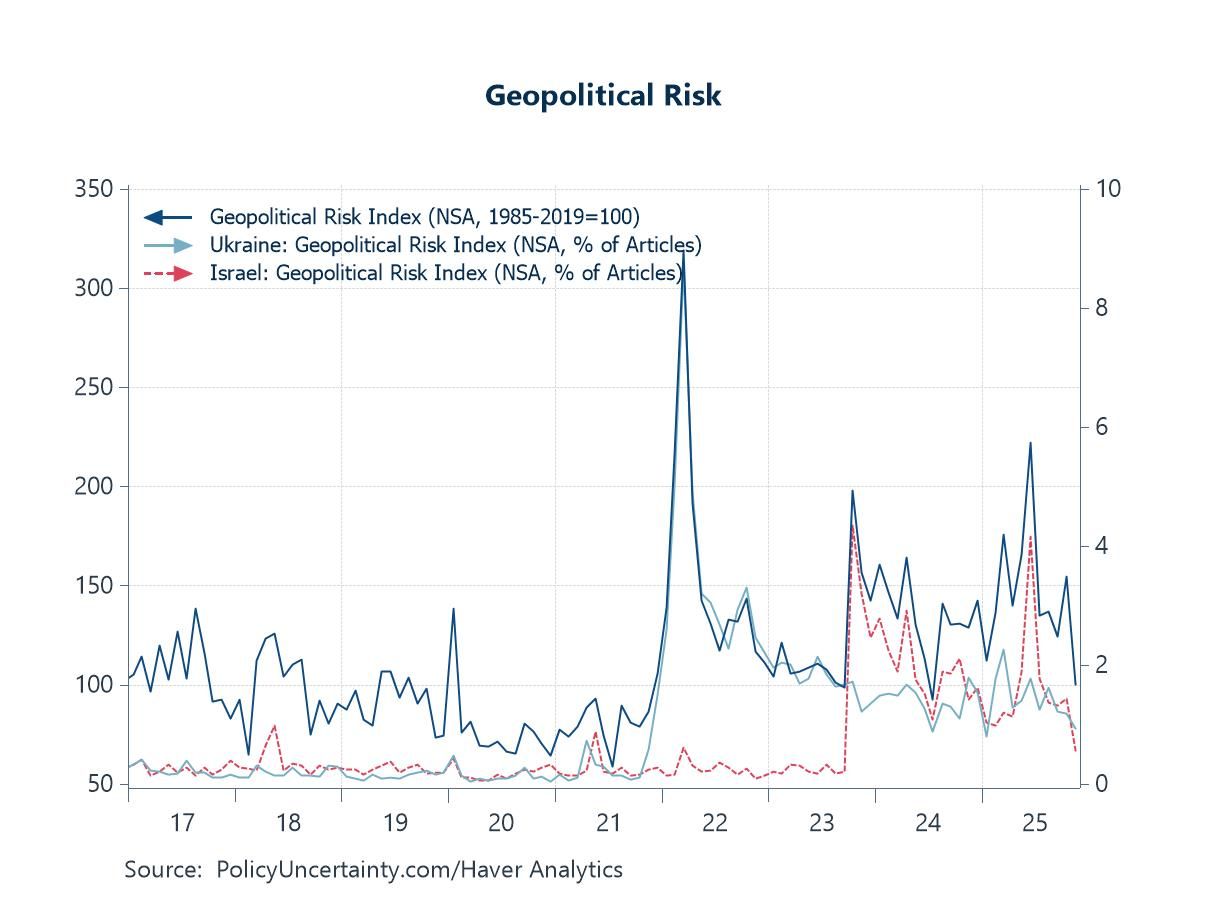

Geopolitical shocks Geopolitical risk has eased from the extremes seen during the early stages of the Israel–Gaza conflict, but the broader backdrop remains far from settled. The global Geopolitical Risk Index is still running well above its pre-pandemic norm, and volatility is now being driven less by any single flashpoint and more by a crowded field of simmering risks. These range from an unstable Russia–Ukraine stalemate and intensifying U.S.–China strategic rivalry to ongoing tensions across the Taiwan Strait, a fragile security environment in the South China Sea, periodic flare-ups in the Caucasus and Sahel, and rising political strain ahead of multiple major elections in 2026. Venezuela’s increasing instability—both domestically and in relation to its border dispute with Guyana—adds another potential source of disruption, particularly for energy markets. While none of these risks is dominating headlines at present, history shows that geopolitical shocks rarely give advance warning. A sudden escalation in any of these theatres could easily unsettle trade flows, energy prices or investor sentiment—another meaningful downside risk as we approach 2026.

Chart 6: Indicators of geopolitcal risk

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief